Archive for May, 2010

-

My Thoughts on Gold

Eddy Elfenbein, May 13th, 2010 at 1:02 pmA reader writes:

Hi Eddy,

I LOVE your blog…I read it everyday and really enjoy your insights. The key is that you keep it just simple enough as to not get too wonky. Please keep it up.

Question: isn’t it about time to short gold? I’m thinking I’d use a little ETF like GLL or DGZ and just sit on it for a while. With the market doing so well and me thinking that things will be looking up for a while, I’m thinking this a nice little play. Any thoughts? Any risks besides gold continuing on its upward path?This is a good topic and I’ve been getting lots of questions about gold recently. I want to take this opportunity to address the topic and I particularly want to focus on folks who may be new to investing.

If you’re not familiar with investing in gold, it may surprise you that many in the pro-gold camp are—shall we say—not terribly helpful for their cause.

Gold is one of those topics that seems to bring the loons out in full force. A sizeable portfolio of goldbugs see the entire world as corrupt and on the verge of bankruptcy, and gold is their only salvation. You can’t help wondering about the distance between their financial and religious beliefs.

Gold is an endlessly fascinating subject. Gold has been used as a store of wealth for thousands of years. Gold never rusts. I mean never! You can take gold out of an Egyptian pyramid and stick it in your cavity (though you might want to clean it first).

Gold is incredibly soft. One ounce can be stretched for 50 miles. It can be pounded down to a few MILLIONTHS of an inch thickness.

Gold is very heavy. Despite what you see in the Treasure of the Sierra Madre (“Badges? We ain’t got no badges!”) gold dust wouldn’t have blown away.

Gold has been found on every continent on earth. Gold has also had strong religious connections. It’s mentioned in the Bible more than 400 times. Karl Marx writes of commodity fetishism, which is meant to have a religious connotation. And I won’t even get into Freud’s talk of the psychological connection of gold to feces (no, I’m not making this up).

When Moses came down from Sinai with the Ten Commandments, the Jews were making a golden calf to worship. God instructed Moses to overlay a sanctuary for him in pure gold. In other words, gold had its bases covered—it was on both sides!

Plato mentions the gold/silver ratio to be 12. Recent historical evidence suggests that Isaac Newton was mainly an alchemist. The other stuff he did was just playing around on the side, and was probably an offshoot of his efforts to makes gold. Pieces of his hair have traces of lead and mercury.

Newton was also Master of the Mint and inadvertently put England in the gold standard. This means that one of the greatest geniuses in human history was also a civil servant who made economic policy based on a forecast. A forecast that was dead wrong.

In the 1964 film, Goldfinger, Auric Goldfinger plans to irradiate all the gold in Fort Knox thus increasing the value of his gold. He would have been a lot better off doing nothing, since gold increased dramatically over the next 16 years.

There’s more gold at the New York Fed, waaaay below 33 Liberty Street, than in Fort Knox. Gold is also a really good conductor. So despite its high prices, it’s used in many electronics.

What you need to understand about investing in gold is that you’re not really investing in gold. You’re investing against the U.S. dollar. It’s not that gold goes up, it’s that the value of a dollar goes down.

Actually, it’s even more subtle than that. What you’re doing is you’re betting against the interest rate on the dollar. I know this sounds odd, but any currency you carry around in your wallet has an interest tied to it. That’s essentially what the currency is—that rate—and it’s the reason why anyone would want to use it. Gold can be seen as the way to keep all those currencies honest.

People mistakenly believe that gold is all about inflation. That’s not quite it, but high inflation is usually very helpful for gold. What gold really likes is to see is very low real (meaning after inflation) interest rates. Gold is almost like a highly-leveraged short on short-term TIPs.

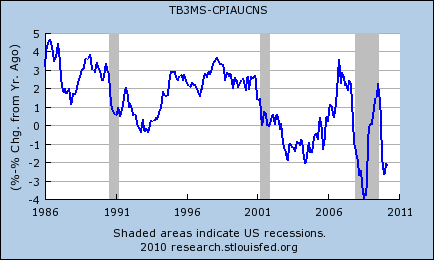

Here’s a good rule of thumb. Gold goes up anytime real rates on short-term U.S. debt are below 2% (or are perceived to stay below 2%). It will fall if real rates rise above 2%. When rates are at 2%, then gold holds steady. That’s not a perfect relationship but I want to put it in an easy why for new investors to grap. This also helps explain why we’re in the odd situation today of seeing gold rise even though inflation is low. It’s not the inflation, it’s the low real rates that gold likes.

This chart shows the three-month Treasury bill rate minus the one-year inflation rate (low is good for gold, high is bad):

In February, gold took a big hit when the Fed announced it was lifting the discount rate. This isn’t the all-important Fed funds rates, but you can see how nervous the market was over the threat of higher real rates.

This rule of thumb also tells us that gold can rise very quickly and it can fall very quickly. One Ben and his pals at the Fed raise rates, gold is in for a world of hurt. The history of the price of gold is long boring periods with sharp dramatic spikes. The up part of the spike is fun. The downside, less fun.

What’s tricky about gold is that it’s also impacted by geo-politics. Gold peaked in 1980 shortly after the Soviets invaded Afghanistan. It reached a low point not long before we did the same.

The pricing of any commodity can be tricky because commodities are subject to substitution. Let’s say that gold, despite its high price, is the cheapest way to make a part for a certain kind of semiconductor. That will drive demand for gold. However, let’s say that once gold crosses a certain level, it’s no longer the cheapest way to make the part. Maybe unobtanium is a better way to go. That will, in turn, undermine gold’s value. It’s price impacts its price.

This is a major difference between investing in equities and investing in commodities. Stocks are companies, filled with people aiming to make a profit. Gold is just a rock. It just sits there. In 10,000 years, it will still be a rock.

My view is that the Federal Reserve will raise interest rates earlier than expected. I don’t know exactly when that will be but it will put gold on a dangerous path. For now, my advice is to stay away from gold, either long or short. -

Best. Stock. Name. Ever.

Eddy Elfenbein, May 13th, 2010 at 12:14 pmI give you — Crazy Woman Creek Bancorp (CRZY)

-

Progressive +40,000%

Eddy Elfenbein, May 13th, 2010 at 11:34 amHere’s another entry in our series, “boring but highly profitable stocks.” Today’s entry is Progressive (PGR) the auto insurance company.

Insurance stock? You’re thinking snores-ville right? Well, check this out. Thirty years ago you could have picked up a share for a split-adjusted price of five cents.

The gold line is the S&P 500. It’s barely visible in comparison. -

Wendy’s Posts Loss

Eddy Elfenbein, May 13th, 2010 at 10:09 am

Now we know a little more about the turnaround at Wendy’s/Arby’s Group (WEN). The company just posted a loss for its first quarter (before charges). However, the company’s new focusing wasn’t fully implemented for the entire quarter.Revenue at Arby’s restaurants fell 12 percent in the quarter.

The lackluster Arby’s showing weighed on overall results, as the owner of Wendy’s and Arby’s restaurants said Thursday that it lost $3.4 million, or a penny per share, for the three months ended April 4. That compares with a loss of $10.9 million, or 2 cents per share, last year.

Removing 3 cents per share in charges, profit was 2 cents per share.

Total revenue fell 3 percent to $837.4 million from $864 million.

Wall Street expected the Atlanta company to earn 1 cent per share on revenue of $835.2 million. The estimates of analysts surveyed by Thomson Reuters generally exclude one-time items.The stock is down today about 3% although I don’t think the earnings report says much about WEN’s future. If this turnaround does work, it will take more time. On the other hand, we can see that this situation isn’t getting worse. I still view WEN as a highly speculative value stock.

-

You Can’t Be Serious

Eddy Elfenbein, May 12th, 2010 at 3:44 pmTheStreet.com is reporting the rumor-that-won’t-die

Netflix is spiking as rumors surface yet again that Amazon is interested in acquiring the company. (BWAHAHAHA)

These rumors have surfaced many times over the last several years in regards to Netflix, most recently in January. Each time analysts have dismissed the claims. (Duh)

While anything is possible (note the Hewlett-Packard-Palm deal), Needham analyst Charles Wolf says it is unlikely.

“Amazon would not acquire Netflix for its by-mail business, which will eventually go away” he says. While Netflix has a terrific digital-streaming business, its library consists of mostly older films. It can’t offer new releases as they are available because it is too expensive.

Amazon, itself, has a streaming pay-per-view service for new releases, and it doesn’t seem like there is a barrier preventing Amazon to offer old movies, Wolf says. “So the company has little reason to buy Netflix.”The rumor is moronic, yet the shares are up 7.5% today. Once again, welcome to Wall Street-istan!!

-

Sector Forecasts

Eddy Elfenbein, May 12th, 2010 at 1:41 pmThis is from S&P. Here are the full-year operating forecasts for the S&P 500 and each sector on March 31 and again two days ago, with the percent change:

Sector 3/31 5/10 Change S&P 500 $78.05 81.33 4.20% Discretionary $15.21 16.06 5.58% Staples $19.43 19.20 -1.19% Energy $33.26 34.51 3.74% Financials $13.17 15.03 14.12% Health Care $30.48 29.72 -2.51% Industrials $15.53 16.41 5.65% Technology $23.75 24.73 4.13% Materials $11.73 12.58 7.23% Telecom $7.50 7.94 5.79% Utilities $12.84 12.75 -0.70% You can see that the Financials have had the biggest improvement. The only sectors with lower forecasts are the defensive ones — Health Care, Staples and Utilities.

Here’s the same table but with 2011 forecasts and the first date in April 6.Sector 4/6 5/11 Change S&P 500 $93.56 $94.51 1.02% Discretionary $18.06 $18.52 2.56% Staples $21.45 $21.54 0.41% Energy $42.30 $41.21 -2.58% Financials $18.10 $19.05 5.23% Health Care $33.18 $32.67 -1.54% Industrials $18.85 $19.01 0.84% Technology $27.89 $28.42 1.89% Materials $12.06 $15.51 28.56% Telecom $8.30 $8.32 0.29% Utilities $12.96 $12.90 -0.49% Here’s a look at the P/E Ratios based on the 2010 and 2011 estimates:

Sector 2010 2011 S&P 500 14.21 12.23 Energy 12.37 10.36 Materials 15.49 12.56 Industrials 16.83 14.53 Discretionary 16.61 14.41 Staples 14.72 13.12 Health Care 11.87 10.80 Financials 14.20 11.21 Technology 14.97 13.02 Telecom 13.23 12.62 Utilities 11.93 11.79 -

Carney to CNBC.com

Eddy Elfenbein, May 12th, 2010 at 1:33 pm

Congratulations to John Carney formerly of Business Insider, formerly of DealBreaker who has joined cnbc.com. Guest of a Guest has the details:Following a ignominious and unexpected exit from softcore porn slide show purveyor Business Insider, writer John Carney has a new gig. He’ll be reporting for duty soon as a senior editor at CNBC.com and will serve as on air commentator for the site. No word yet on which channels he’ll be frequenting but with those looks he could be a serious threat for money honeys all across NBC Universal properties.

-

The Argument for Stock-Picking

Eddy Elfenbein, May 12th, 2010 at 12:12 pmTadas Viskantas has an excellent article arguing that we’re entering the Golden Age of Stock-Picking.

-

Goldman Sachs! The Musical

Eddy Elfenbein, May 12th, 2010 at 10:46 amThe New Yorker spots a musical. Here’s a sample

CARL LEVIN (D-MICH):

I want to know what you knew

And exactly when you knew it

And why you all believed

You’d manage to get through it

FABRICE TOURRE:

We didn’t prey on our clients’ stupidity

We showed them our prices and offered liquidity

CARL LEVIN (D-MICH):

To you it may have been a game

To me it all seems pretty real

I mean to make you feel shame

For how you made this shitty deal

FABRICE TOURRE:

I’m not deceitful or conniving

Did you see the picture of me skydiving? -

From the Department of No Surprise

Eddy Elfenbein, May 12th, 2010 at 10:38 amRecent financial collapses have focused policymakers’ attention on the financial industry. To date, empirical studies have concentrated on corporate issuer activity, such as securities offerings and class actions. This paper makes a first step in studying SEC enforcement against investment banks and brokerage houses. This study suggests that the SEC favors defendants associated with big firms compared to defendants associated with smaller firms in three ways. First, SEC actions against big firms are more likely to involve exclusively corporate liability, with no individuals subject to any regulatory action. Second, the SEC is more likely to choose administrative rather than court proceedings for big-firm defendants, controlling for types of violation and levels of harm to investors. Third, within administrative proceedings, big-firm employees are likely to receive lower sanctions, notably temporary or permanent bars from the industry. To explain this gap, the paper first investigates whether big-firm violations are qualitatively different from small firms’ violations, but finds no support for this. This paper next explores two hypotheses that could explain a systematic bias in enforcement patterns: that constraints in bureaucratic resources weaken the SEC’s negotiating position towards big firms, and that SEC officials favor prospective employers.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His