Archive for May, 2010

-

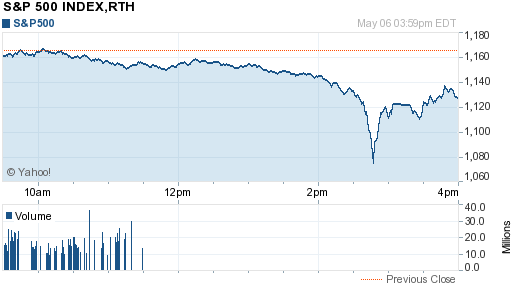

Watch the Market Tumble

Eddy Elfenbein, May 7th, 2010 at 12:01 am

(Via: TBI) -

The Buy List Survives

Eddy Elfenbein, May 6th, 2010 at 11:50 pmI’m happy to report that our Buy List survived today, bruised but still alive. The average of our 20 stocks was down -3.03% compared with 3.24% for the S&P 500.

AFL -3.86% BAX 0.77% BDX -0.97% BBBY -4.36% EV -5.74% LLY -1.94% FISV 1.51% GILD -2.56% INTC -2.99% JNJ -2.67% JOSB -3.91% LUK -4.37% MDT -2.65% MOG-A -5.16% NICK -4.44% RAI -3.77% SEIC -3.24% SYK -1.70% SYY -3.74% WXS -2.02% The only one of our stocks that appeared to be impacted by the glitch was Reynolds American (RAI). Reynolds dropped from $53.55 to $36.35 and rallied to $51.53.

-

WTF!

Eddy Elfenbein, May 6th, 2010 at 11:30 pm

So I head out for a meeting this afternoon and the market goes bananas. I trust you people to take care of these things when I’m not watching.

Ok, let’s dissect what happened. The market had been drifting lower during the early afternoon. Then at around 2:30, all hell broke loose. At one point the Dow was down 1,000 points (or 998.5 to be exact). The market then staged a furious 650.7-point rally to close down “only” 347.80 points.

Traders had been worried about Greece, the British election and tomorrow’s jobs report. However, something truly odd was going on. Accenture (ACN), for example, dropped from around $40 a share to a penny. Procter & Gamble (PG) and Philip Morris (PM) were also down sharply without explanation. Six companies traded at $0. Someone had clearly blundered

As of now, nobody knows exactly what happened but it seems that the computers started to rise up against us. Or more specifically, someone with a fat finger hit the wrong button. There was a rumor that a guy at Citigroup dumped $16 billion worth of S&P futures, instead of the $16 million he was supposed to. Hey, these things happen. Billion…million. Tomay-to…tomah-to.

What may have happened is that one series of program sells kicked in another serious of sells and it quickly snowballed. The Nasdaq has said that it will cancel hundreds of trades made between 2:40 p.m and 3 p.m. The quote of the day belongs to the WSJ’s Evan Newmark: “Today’s market was neither orderly nor efficient nor trustworthy. It was just a bunch of computers making ugly, messy love with each other. And your money hung in the balance.”

Bear in mind that on any given day, roughly 50% to 75% of all trades are done through high-frequency trading. The hero of the day turned out to be Jim Cramer. He was on CNBC with Erin Burnett and told viewers, “That’s not a real price. Just go buy Procter & Gamble.”

-

Score One for Efficient Markets!

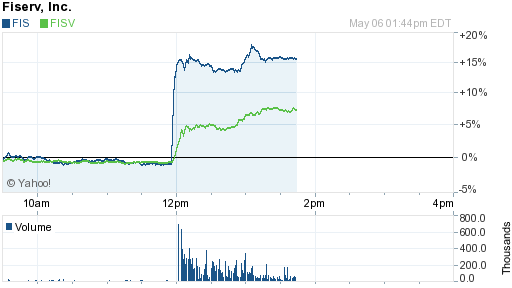

Eddy Elfenbein, May 6th, 2010 at 1:56 pmYou better sit down for this one.

Earlier I mentioned that Fiserv (FISV) started spiking around noon.

The reason seems to be that Blackstone (BX) and others are in talks to buy Fidelity National Information Services (FIS).

Yes, they’re confusing the ticker symbols.

Or possibly, folks are buying FISV because they think other people will mistake the ticker symbols which will lead to…even more people buying FISV!

In other worlds, welcome to Wall Street.

(I should add that the two companies are competitors so some reaction to the buyout should be expected.) -

The Midday Market

Eddy Elfenbein, May 6th, 2010 at 1:12 pmThe market started the day with the cyclicals zooming out of the gate. I thought this was a typical reverse reaction day when everything that had been doing poorly suddenly catches fire. But that gave way and the cyclicals are now down with the rest of the market. The S&P 500 has been as low at 1150 today. It seems like only a few weeks ago when we passed through 1150, which, of course, it was.

Our Buy List is showing a lot of resiliency. The S&P 500 lost -0.66% yesterday but the Buy List gained 0.15%. (Did anyone else jump up on their desk and do the Cabbage Patch when NICK hit $9.20? Um…good, me neither.) So far today we’re only down -0.56% compared with the S&P 500’s loss of -1.02%. So we’re sucking less but it shows you how our stocks can hold up when the cyclicals break down.

Around noon, shares of Fiserv (FISV) suddenly sprung to life. The stock is up about 6% today. AFLAC (AFL) is back down again today. The stock has been as low as $47 which is a very attractive price. -

Mark Haines for the Win

Eddy Elfenbein, May 6th, 2010 at 11:12 am -

This Just In….

Eddy Elfenbein, May 6th, 2010 at 10:49 amOhhhhh!

*Smacks Forehead*

Now they tell us! -

More on Repurchases

Eddy Elfenbein, May 6th, 2010 at 9:53 amI got a number of emails is response to yesterday’s screed against share buybacks. Here’s a thoughtful response from a reader.

First, I’m a fan of your blog, and read it every day. (I even own some NICK 🙂

I’m having trouble understanding your antipathy to buybacks.

If you believed (bear with me) that stocks were always correctly priced, then you would prefer buybacks to dividends for stocks in you taxable accounts because of the tax advantages. And this is true even if the nominal tax levels on dividends and capital gains are the same, because capital gains taxes can usually be deferred for a long time (maybe even forever, for example if you make a lot of charitable contributions), while dividend taxes are impossible to escape.

But of course stocks are not always correctly priced. In this case, you’d want the firm to buy back stock when the stock was cheap and issue stock when it’s expensive. Since the entire premise of your project is that you can identify cheap stocks, you should be happy to hear that one of your holdings is using their cash to buy back shares which you presumable believe are cheap.

You are a buy-and-hold investor, who will hold the firm for as long as it’s cheap, so you don’t need to worry about whether the buyback is immediately correctly reflected in the stock price…the buyback will increase earnings-per-share, and this will eventually be reflected in the price.

This also helps get rid of the excess cash which might otherwise be squandered by the firm. You could also do this via a one-time cash dividend, but then again there would be a big tax hit. You could raise your regular dividend, but then you might find you have to cut it, and firms are reluctant to do that for signaling reasons.

Of course the problem with buybacks is that firms might do them when the stock is expensive. In theory, executives should be able to use their inside knowledge to do more repurchases when the stock is cheap, but it’s not clear how much that really happens. Also, what is seen as “cheap” changes with the overall level of optimism in the economy.

But again, since you believe you can identify and hold cheap stocks, you should be happy when one of your holdings makes a purchase of cheap stock on your behalf. What am I missing?It’s hard for me to argue against this because everything he says is correct. My stand against share buybacks is far more primal. I just want the cash, and I’m happy to leave the theory stuff to someone else.

If it’s not advantageous tax-wise, fine—change the law. If the stock is still cheap, fine—give me the dividend and I’ll decide if I want to reinvest it or not. I just want the money.

David Berman, who writes the terrific Market Blog for the Globe and Mail, writes:Mr. Elfenbein’s argument would be a lot stronger if he could show that companies are notoriously bad at timing share buybacks – that is, buying their own stocks at high prices and therefore wasting their money.

According to Standard & Poor’s, companies in the S&P 500 bought $47.8-billion (U.S.) worth of shares in the fourth quarter of 2009, up more than 37 per cent from the previous quarter. However, this is still well below the frenzy of buyback activity in 2007, a year that coincided with a peak in the S&P 500 before the onslaught of the financial crisis.

Companies, it seems, like their own shares when they’re pricey.For me, it’s a point of principle (and principal, for that matter). I don’t want the companies I own to be in the business of timing their stock. That’s my job. Their job is to run the business and make as much money for me as they lawfully can. I’m the owner. Let me worry about what to do with the profits.

Another reader writes:I definitely agree with you on preferring dividends compared to repurchases, at least in 99% of cases. You cited the case of Cisco, which has spent tens of billions to no apparent effect. The more pernicious thing about repurchases is that many companies only use them to soak up the equity dilution from option issuance to employees. Yet billions of dollars are spent on repurchases, without actually shrinking the float. Take a look at the recent Goldman Sachs quarter; they spent a couple of billion buying back 13.2 million shares to offset option issuance, but actually had 16 million more average shares outstanding (basic) and 6 million more shares outstanding (diluted) at the end of the quarter, compared to the end at Dec. 31/2009.

I’m not sure if all companies are now required to report EPS including option issuance as compensation expense; if they are, that’s fine. But if they’re not, then companies get to boost EPS too, by diverting an expense item into the balance sheet item of retained earnings.

Give me the dividend!This is an excellent point. I don’t mind executives being compensated with stock, but share repurchases make it very easy for them to mask shareholder dilution.

-

Leucadia’s Earnings

Eddy Elfenbein, May 6th, 2010 at 9:04 amYesterday, Leucadia National (LUK) reported its earnings results. I almost have to place an asterisk next to Leucadia. The company is, shall we say, reserved about corporate communications. If you want to see what I mean, this is the company’s website. Yes, that’s the whole thing.

Let me back up and explain. Leucadia is very similar to Warren Buffett’s Berkshire Hathaway except it’s about one-thirtieth the size. The stock has done about as well as Berkshire over the last few decades. The big difference is that the owners, Ian Cumming and Joseph Steinberg, are extremely media shy. The company owns a grab bag of companies involves in several industries. It’s not an easy stock to evaluate. Leucadia has no analyst coverage and the earnings reports are celebrated by very thin press releases.

This is what they had to say yesterday:Leucadia National Corporation today announced its operating results for the three month period ended March 31, 2010. Net income attributable to Leucadia National Corporation common shareholders for the three month period ended March 31, 2010 was $191,479,000 or $.78 per diluted common share as compared to net loss attributable to Leucadia National Corporation common shareholders for the three month period ended March 31, 2009 of $(140,007,000) or $(.59) per diluted common share.

If you want to check out the details of their business, you can read the latest 10-Q. It’s fairly detailed. I’m pleased to note that Leucadia has a stake in AmeriCredit (ACF) which is in the lucrative field of financing for used cars.

Here’s a Barron’s article on Leucadia from 2008.

-

The Crossing Wall Street Tax Code

Eddy Elfenbein, May 6th, 2010 at 8:58 amI want to thank everyone who participated in our weekend poll, “How much federal income tax should a family of four that makes $25,000 pay?” We had over 600 responses.

This is the fifth time we’ve run that poll. The other income values we used were $40,000, $100,000, $250,000 and $1 million.

Using some interpolation, I tried to find the median vote for the tax rate for each poll. Here’s what we have:

$25,000: 2.66%

$40,000: 8.31%

$100,000: 16.33%

$250,000: 22.69%

$1,000,000: 28.23%So the collective wisdom favors a progressive income tax. (Please note that this is not necessarily my opinion, it’s what the poll said.)

Using a little math, we can make a three-bracket tax code that links the data above. It looks like this:

The first $21,249 is tax free.

$21,249 to $74,266 is taxed at 17.79%

$74,266 to $250,000 is taxed at 26.93%

Above $250,000 is taxed at 30.08%There are lots of ways to connect the poll results, and without more data, the three-bracket result is the simplest. We could add a fourth bracket to make things a bit more realistic. For example, if we added a 10% bracket at around $18,000, then a 20% bracket at $28,000, we could push the 27% bracket to $85,000 while leaving $250,000 and over at 30%. That’s just one example.

I didn’t have any larger point I was trying to prove with the poll. I was simply curious about what our readers thought.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His