Archive for May, 2010

-

Thumbs Down to Bristol-Myers Share Repurchase

Eddy Elfenbein, May 5th, 2010 at 1:56 pmI felt the need to do quick post on the news that Bristol-Myers Squibb’s (BMY) board approved a $3 billion share repurchase.

Ugh, these announcements make me groan. I loath share buybacks. After watching company after company waste billions of dollars buying their shares, I’ve come to the conclusion that these repurchases are a waste of time and money. I’d much rather see shareholders get more dividends.

In theory, it’s all the same money—share buyback or dividend—so it shouldn’t make a difference how shareholders are paid. The problem is that the stock market is far too volatile for investors to accurately see the results of a share repurchase.

Cisco (CSCO) is a prime example. The company has wasted several billion dollars buying back its stock. Would the stock have done worse without it? Probably, but I can’t say for certain. However, I absolutely know that shareholders would be wealthier with quarterly dividend checks.

Bristol-Myers is an excellent company and there’s a lot to like about the stock. They just had a very good earnings report. The company pays a quarterly dividend of 32 cents a share which translates to a yield of 5.1%. That’s about 150 points better than a 10-year Treasury.

Let’s look at some of the numbers: Bristol-Myers, like many other healthcare stocks, recently adjusted downward its 2010 earnings forecast due to Obamacare. They now see EPS coming in between $2.15 and $2.25. That means that the quarterly dividend of 32 cents (or $1.28 annualized) is very safe.

On top of that, Bristol-Myers is sitting on a mountain of cash. They have a net cash position of $3.4 billion which comes to $2.02 a share. This means they’re probably a bigger net lender than most banks. In short, they ain’t going bankrupt anytime soon. As a shareholder, wouldn’t it be so much nicer to get a check?

I actually get a little afraid when companies acquire too large a position in cash. This is what I like to call the “Bladder Theory of Corporate Finance.” Little mergers are fine, but mega-mergers are almost always trouble.

What’s most aggravating is that BMY’s board might be making the sensible move. If Congress doesn’t act soon, then dividend taxes are set to nearly triple for high-earners, rising from 15% now to 43.4% in 2013. President Obama wants dividends and capital gains to be taxed at the same level which would hopefully stem the tide of these silly share repurchases. -

The Cyclicals Continue to Plunge

Eddy Elfenbein, May 5th, 2010 at 10:16 amThe trading day is still young but the markets are heading lower and once again, it’s the cyclicals doing most of the damage. The Cyclical Index (^CYC) is currently off -1.29% (it had been more) while the S&P 500 is down -0.56%. The energy stocks seem to be getting hurt the most. Many consumer staples, like Reynolds American (RAI), are actually up on the day.

I’m very happy to see that Nicholas Financial (NICK) is now over $9 a share. Gilead Sciences (GILD) continues to fall and the stock has made another fresh 52-week low. As I’ve said before, trends can last much longer than you thought possible. Remember, it was only a little over one year ago that NICK was going for $1.80 a share (pre-split). -

Update on Cyclicals

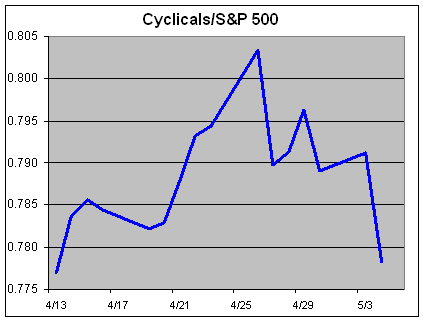

Eddy Elfenbein, May 4th, 2010 at 11:16 pmTwo weeks ago, I highlighted the fact that cyclical stocks had been on a roll. I was smart enough not to call a peak in cyclical outperformance, but it may have occurred just a few days after my post.

Last Monday, April 26, the ratio of the Morgan Stanley Cyclical Index (^CYC) divided by the S&P 500 broke 0.8 for the very first time and reached an all-time high. Since then, however, cyclicals have underperformed the market and yesterday was an especially ugly day. Since April 26, the S&P 500 has lost -3.17% while the CYC has lost dropped -6.19%. So if you’re a money manager, you can see where you don’t want to be.

It’s still far too early to say whether this is a turn in the cycle. But investors should take notice because once cyclicals start to underperform, the trend can last for a few years.

-

The Onion’s Stockwatch

Eddy Elfenbein, May 4th, 2010 at 7:37 pmAmerica’s Finest News Source:

C

Citigroup

$4.15 $.16 (up 4.0%)

Markets reacted positively to CEO Vikram Pandit’s announcements that the troubled financial titan would soon repay bailout money to the government in the form of a $45 billion prepaid Visa gift card.

GS Goldman Sachs $50.4 $1.23 (up .89%)

A large early-morning protest in front of the company’s headquarters Tuesday led to speculation that Goldman was once again making a lot of money.

BRKB Berkshire-Hathaway (up ) $3,32 $38.9 (+1.18%)

Investors have been aching to get their hands on this hot stock ever since the premiere of Lil Wayne and Birdman’s latest music video in which the two hip-hop icons shower strippers with fistfuls of the conglomerate’s famously high-priced shares. -

Nicholas Financial’s Earnings

Eddy Elfenbein, May 4th, 2010 at 2:08 pmGreat news! NICK made 28 cents a share (adjusting for two cents lost on swaps):

CLEARWATER, Fla., May 4, 2010 — Nicholas Financial, Inc. announced that for the three months ended March 31, 2010, net earnings, excluding change in fair value of interest rate swaps, increased 52% to $3,113,000 as compared to $2,048,000 for the three months ended March 31, 2009. Per share diluted net earnings, excluding change in fair value of interest rate swaps, increased 44% to $0.26 as compared to $0.18 for the three months ended March 31, 2009. See reconciliations of the Non-GAAP measures below. Revenue increased 8% to $14,256,000 for the three months ended March 31, 2010 as compared to $13,224,000 for the three months ended March 31, 2009.

For the year ended March 31, 2010, net earnings, excluding change in fair value of interest rate swaps, increased 80% to $10,228,000 as compared to $5,673,000 for the year ended March 31, 2009. Per share diluted net earnings, excluding change in fair value of interest rate swaps, increased 74% to $0.87 for the year ended March 31, 2010 as compared to $0.50 for the year ended March 31, 2009. See reconciliations of the Non-GAAP measures below. Revenue increased 6% to $56,472,000 for the year ended March 31, 2010 as compared to $53,102,000 for the year ended March 31, 2009.

According to Peter L. Vosotas, Chairman and CEO, “Our positive results for the fourth quarter and year were favorably impacted by a solid increase in revenues and a reduction in the net charge-off percentage of 41% and 26% for the three and twelve months ended March 31, 2010, respectively. We plan to open three to five new branch locations this year and will continue to evaluate additional markets for future branch locations.”Wow, the provision for credit losses dropped to 3.01%!! That’s huge! That’s the lowest since September 2007. This was another very good quarter for Nicholas.

Let’s run through some of the numbers. Most of my forecasts were pretty close to the mark. Average receivables rose to $229.4 million. I said to expect $230 million. Revenue was $14.2 million. I was expecting $14.5 million.

I pegged interest expense to rise to 2.4% but it rose even higher to 2.66%. However, NICK’s debt actually fell from last quarter so total interest expense was $1.5 million. I was expecting $1.4 million.

Even though I was slightly overly optimistic on those projections, I was too pessimistic on the provision for credit losses. I thought it would fall to 4.8%. Instead, it fell all the way to 3.01%. That made all the difference.

Twenty-eight cents is great news. Congratulations to everyone at Nicholas. This was a job well done.

The company made $3 million in three months. Now that cash can be used to grow the portfolio or pay down debt. If they keep this up, then NICK should easily make $1.10 for this calendar year.

For stat geeks, here are the numbers. -

The World’s Simplest Portfolio

Eddy Elfenbein, May 4th, 2010 at 12:39 pmScott Adams of Dilbert fame gives us his suggestion for the World’s Simplest Portfolio (“that is better than what the average money managing expert might concoct”).

He suggests half in the Vanguard Total Stock Market ETF (VTI) and half in the Vanguard Emerging Market ETF (VWO).

That’s not bad, but I can make it even simpler—put all of your money is a Treasury set for the date you need the money. Simple, right? Even better, use a zero-coupon Treasury which is like automatically reinvesting your dividends.

You can skip the transaction costs by buying the bond right from the Treasury. Your default risk is nil.

There’s a chance that you might not perform as well as the market as a whole, but over the past few decades, the equity premium hasn’t been much to write home about. Plus, most of the premium would be eaten away by expenses, even tiny ones from Vanguard.

If you were to design a ratio of Performance-to-Headaches, this portfolio is hard to beat.

This chart above shows how the two ETFs Adams recommends have performed, plus the American Century Target 2025 fund which I’m including as a proxy for long-term Treasuries. -

Ouch!

Eddy Elfenbein, May 4th, 2010 at 10:52 amThe market is getting hit hard today. The S&P 500 is down to 1176. The real problem is coming from cyclical stocks. The Morgan Stanley Cyclical Index (^CYC) is now down -3.36% compared with just -1.38% for the Consumer Index (^CMR).

On our Buy List, AFLAC (AFL) is now below $49 which is a very good entry point. Leucadia National (LUK) and Eaton Vance (EV) are also off sharply.

If you’re looking for income, Reynolds American (RAI) currently yields 6.75%. Gilead Sciences (GILD) is turning into one of the best buys on the Buy List. Some major pharma has to be looking at GILD for a buyout. -

This Just In: Members of Congress Say One Thing, Do Another

Eddy Elfenbein, May 4th, 2010 at 9:57 amAccording to The Journal’s analysis of congressional disclosures, investment accounts of 13 members of Congress or their spouses show bearish bets made in 2008 via exchange-traded funds—portfolios that trade like stocks and mirror an index. These funds were leveraged; they used derivatives and other techniques to magnify the daily moves of the index they track.

(…)

In February, Sen. Johnny Isakson (R., Ga.) argued on the Senate floor that “we don’t need those speculating in the marketplace to take unfair advantage of the values of equities that are owned by Americans all over this country for the sake of making a buck on a short sale.”

On Oct. 8 and 9, 2008—as the Federal Reserve was bailing out American International Group Inc.—an account Sen. Isakson held invested more than $30,000 in ProShares UltraShort 7-10 Year Treasury and UltraShort 20+ Year Treasury, the records show. These are “leveraged short” funds, designed to gain $2 for each $1 drop in the daily value of U.S. Treasury bonds.

(…)

“I don’t trade on margin”—money borrowed from a broker to raise potential returns—Rep. Bachus said in an email, “and don’t consider my investments leveraged to any risky extent.” He added: “Never have I traded on nonpublic information, nor do I trade in financial stocks.”

Rep. Bachus made roughly $28,000 on his trades in options and leveraged ETFs in 2008, according to a Journal analysis, a figure he called “essentially correct.”

(…)

Rep. Shelley Berkley (D., Nev.), a member of the House Ways and Means Committee, has been a critic of Wall Street. In a statement on the House floor Feb. 23, she said: “Representing Las Vegas, let me assure you, no casino on the planet behaves as irresponsibly and recklessly as Wall Street does. Wall Street ought to be ashamed, and take a lesson from the casino industry.”

An account held by her husband, Lawrence Lehrner, shows 57 trades in 2008 in ETFs designed to gain $2 for each $1 drop in the value of a market index, the disclosures show. Between July 25 and July 29, 2008—four months after Bear Stearns Cos. fell—records show four trades in and out of ProShares UltraShort Financial fund.(Via: Falkenstein)

-

Earnings Preview for Nicholas Financial

Eddy Elfenbein, May 4th, 2010 at 7:55 amI’ve written a great deal about Nicholas Financial (NICK), probably more than any other stock. The company is a small firm that provides loans for used cars. If you’ve read this blog for some time, then it’s no secret to you that I believe the stock is going for a tremendous bargain and that the investing public doesn’t properly understand the company. Currently, no Wall Street firms follow the stock. I think I’m the only person who writes about Nicholas.

Here’s my take: I think investors have mistakenly lumped Nicholas in with other subprime lenders. They see “used car loans” and instandly think toxic debt. The major difference is that Nicholas doesn’t securitize its loans and the company is rather conservative in its accounting.

Make no mistake, Nicholas’ customers have been hit hard by the recession that has impacted the company’s portfolio, but Nicholas is still a fundamentally solid business. I’ve spoken with senior management a few times and each time, I’ve come out feeling that Nicholas is well-run and will thrive. I will also reveal that Nicholas is currently my largest personal holding.

The fiscal fourth-quarter earnings report is due out sometime this week. My forecast is that Nicholas will earn about 25 cents per share (give or take). I think it’s very possible that Nicholas will earn as much as $1.20 per share during this calendar year (I’ll say $1 a share is the low end). Now bear in mind that this is a stock currently going for $8.75, or about seven to eight times forward earnings.

Nicholas tends to be a fairly stable business except for one metric—provision for credit losses. In other words, bum loans. This number skyrocketed but it’s been coming down. Last quarter, it hit 5.34% which is nearly half what it was in September 2008. Every inch that number falls, it’s better for Nicholas. I’m hoping it will fall below 5% for this report. The provision for credit losses has fallen now for five straight quarters.

Even if my forecast if off by a little, I’m not worried at all. The valuation is so low that there’s an enormous margin of safety. This post probably best spells out why Nicholas is such a compelling buy.

Here are some very basic projections: I think that receivable will be about $230 million. The gross yield will be about 25.4% which will make revenues around $14.5 million. Interest expenses will rise to about 2.4% or about $1.4 million. This will make net revenues of about $13.1 million.

I’m pegging the provision for credit loss at 4.8%. Since the economy in Florida is still rough, this number will see smaller and smaller declines. Ultimately, I think NICK is worth $12 to $15 a share. This is an outstanding buy.

(Be warned that NICK is a micro-cap so that shares are somewhat illiquid. I actually prefer that. The stock can trade with a wide bid-ask spread. It’s also common for NICK to go a whole day without trading one share. This may frustrate some investors.) -

The Stock Market’s Best Day in Two Month

Eddy Elfenbein, May 3rd, 2010 at 6:08 pmToday was a good day for Wall Street. The S&P 500 is back over 1200 as the index posted its best gain since March 5. The S&P 500 gained 1.31% today while our Buy List did slightly better gaining 1.43%. The only sore spot was Sysco (SYY) which dropped 1.6% after it reported decent earnings (don’t ask me).

I was very pleased to see Nicholas Financial (NICK) close at $8.75 which is a new two-year high. The company is set to report earnings this week and I’m expecting EPS of around 25 cents a share. I continue to believe this is a hugely under-priced stock.

I think I might get in trouble for writing this on the Internet, but this earnings season has been very, very good.The first-quarter earnings season is shaping up to be one of the strongest in decades. About two-thirds of S&P 500-stock index companies reported earnings by last Friday, with 78% beating analysts’ estimates, according to Thomson Reuters. And they beat them by an impressive 16.3% on average. If that rate holds, it will be the highest since 1994.

That performance has come amid signs of broad-based, sustainable growth. Fourth-quarter earnings were influenced by strong financial-sector results; strength appears to be more widely spread in the first quarter.

Excluding financials, year-on-year earnings growth is tracking at about 35% in the first quarter, up from 18% in the fourth quarter. Nine in 10 companies in the technology and consumer-discretionary sectors have beaten estimates.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His