Archive for August, 2010

-

From 1985: What Will Shopping Be Like in 2010?

Eddy Elfenbein, August 31st, 2010 at 12:05 amFrom 1985, peer into the distant future of 2010.

-

The WSJ Takes on the P/E Ratio

Eddy Elfenbein, August 30th, 2010 at 2:43 pmThe Wall Street Journal has a rather unusual column today claiming that the Price/Earnings Ratio is not only declining, but the metric’s importance is declining as well. For supporting evidence, they offer up the fact that corporate earnings were strong this past earnings season but the stock market has since fallen.

Sorry folks but that’s not a hard knot to entangle: The P/E Ratio looks backward while stock prices look forward. As a result, you can get some poor readings. I’m afraid to tell the WSJ that despite this minor conflict, the P/E Ratio remains very important (though we must be aware of its shortcomings).

The WSJ goes on to say that the P/E Ratio has plunged about 36% in the past 12 months which is the biggest drop in seven years. Again, this shouldn’t be much of a surprise because, as I just mentioned, the P/E Ratio looks backward. Corporate earnings have improved very dramatically since the depths of the recession. A higher E with a flat-to-lower P means a lower P/E Ratio. Mystery solved.

The WSJ also writes that the forward P/E Ratio has dropped from 14.4 in May to 12.2 currently. This probably means that stock prices are ahead of analysts’ forecast and that those projections may be headed lower soon.

Because of the time discrepancy in the P/E Ratio we sometimes get “false readings.” For example, when stocks are cheapest, the earnings line is often still headed lower. As a result, the very first stages of a bull market often shows the P/E Ratio dramatically expanding. The opposite happens when the market begins to look rich, which may be happening right now. Stocks are sluggish while earnings have improved. As a result, you have stocks falling after good earnings combined with a subdued P/E Ratio.Three months ago, analysts expected the companies in the Standard & Poor’s 500-stock index to boost profits 18% in 2011. Now, they predict 15%. Mutual-fund, hedge-fund and other money managers put the increase at closer to 9%, according to a recent Citigroup survey, while Mr. Levkovich’s estimate is for 7% growth.

“The sustainability of earnings is in doubt,” said Howard Silverblatt, an index analyst at S&P in New York. “Estimates are still optimistic.”The WSJ says that the P/E Ratio is plagued by the lack of certainty in future earnings, and on this point I agree. Think of it this way. Imagine we have two stocks that are similar in every way except for one difference. Stock A is projected to earn $1 a share next year, plus or minus 20 cents. Stock B is projected to earn $1 a share next year, plus or minus three cents. Which stock will be worth more? Outside of rare exceptions, we can assume that Stock B will be worth more. Why? Because the market rewards certainty.

The WSJ also claims that the P/E Ratio has had earlier bouts of loss of importance — from the Great Depression to the early post-war period and again during the inflation struggles of the 1970s and early 80s. I agree on the former, but the latter was hardly a refutation of the P/E Ratio. It’s simply that the P/E is closely tied to interest rates. As rates head higher, P/E Ratios headed lower so stocks could actively compete with bonds.

I can assure you that any obituary for the P/E Ratio is very premature. -

Genzyme Says No to Sanofi-Aventis

Eddy Elfenbein, August 30th, 2010 at 12:53 pmThe stock market is bucking the trend of 2010 as we’re currently heading lower on a Monday. The market, however, is still well above the lows from Friday morning. Most of the rally from Friday afternoon still holds. The cyclical stocks are leading the market lower today.

One of the big stories today is that Genzyme (GENZ) has rejected the $18.5 billion offer from Sanofi-Aventis (SNY) believing the bid is too low. I don’t have a strong opinion about either company but I’m happy to see companies reject buy-out offers right now.

As usual, the market had the right idea. GENZ’s had already been trading above SNY’s bid price of $69 a share. Sanofi’s CEO said they made a “compelling” offer and that Genzyme’s management “has a history of overpromising and under-delivering.” Ooooh, snap!

On the Buy List, Intel (INTC) is still in a buying mood. This time, they’re picking up the wireless unit of Germany’s Infineon Technologies for $1.4 billion. This is an area where Intel hasn’t been particularly strong.“The acquisition of Infineon’s wireless business strengthens the second pillar of our computing strategy–Internet connectivity–and enables us to offer a portfolio of products that covers the full range of wireless options from WiFi and 3G to WiMAX and the long-term evolution,” a standard for the new faster fourth generation mobile networks,” Intel President and Chief Executive Paul Otellini said in a statement.

Infineon will “now fully concentrate our resources towards strong growth in our core segments,” its CEO Peter Bauer said without elaborating. He added that the sale of its wireless operations “is a strategic decision to enhance Infineon’s value.”

Bauer added that acquisitions are an element of Infineon’s further growth strategy, although he added that there are no concrete talks and he fells no time pressure to buy.

Infineon got a “reasonable price” for its wireless unit “but might be below ambitious market expectations that failed to factor in upcoming investment” for fourth generation networks, said Commerzbank analyst Thomas Becker, who rates the shares buy, but cut his target price to EUR5.80 from EUR6.60 to reflect the divestment.Intel’s stock is currently hovering around $18 a share.

-

Buffett Turns 80

Eddy Elfenbein, August 30th, 2010 at 8:15 amHappy Birthday to Warren Buffett. Here’s to 80 more!

-

Ave Maria!

Eddy Elfenbein, August 28th, 2010 at 1:07 pmMaria Bartiromo singing!. Here’s Part 1:

Part 2:

-

Market Notes: August 27, 2010

Eddy Elfenbein, August 27th, 2010 at 3:53 pmThe Buy List had a very good day to close out August which was an ugly month for us.

Here are a few notes on some of our stocks:

Barron’s notes that First Global has downgraded Gilead Sciences (GILD).

Eli Lilly (LLY) won a court battle which extended the blocking of generic versions of Strattera, an attention deficit disorder drug.

Nicholas Financial (NICK) got as low as $8.06 today. The company’s book value is $8.59.

Here’s Ben Bernanke’s speech today in Jackson Hole. I thought it didn’t say much at all, but the market bond dropped sharply and stocks rose. -

Altria Raises Dividend

Eddy Elfenbein, August 27th, 2010 at 11:46 amAltria (MO) announced today that it’s increasing its quarterly dividend by 8.6% to 38 cents per share. Think of it this way: If you had bought the shares 25 years ago, the dividends alone are yielding you 192%.

-

Krugman and Bond 36,000

Eddy Elfenbein, August 27th, 2010 at 9:55 amTen years, I criticized the Dow 36,000 thesis for its bad math. Now I very cautiously criticize Paul Krugman’s defense of the bond bulls.

Professor Krugman had a post earlier this week saying that the low yield on the 10-year T-bond is justified. He backed up this claim by taking the CBO’s 10-year projections for unemployment and core inflation and ran that through Greg Mankiw’s Fed rate rule.

The output was a projection for the Fed funds rate for the next 10 years. What’s interesting is that it shows that the Fed ought to keep rates near 0% for a few more years.

The problem I have with Krugman is what he did next. He used the 10-year forecast of short-term rates to arrive at his estimate of what the 10-year yield ought to be—2.6%.

The problem with this is that the yield on the 10-year bond is not solely the summation of 10 one-year bonds, or 40 three-month bills, or whatever time slice you like to use. There’s also an added “term premium.” This is what makes the yield curve, well…curve.

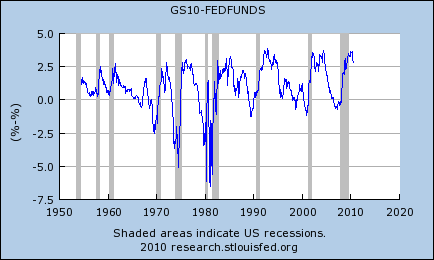

I looked at the historic spread of the 10-year bond over the effective Fed funds rate since 1954 (chart below). The spread has average 92 basis points. Bear in mind that this is a premium that’s over and above what the market has already factored for future rate increases. This is simply the premium you get for holding longer term debt.

Assuming a 10-year bond with a coupon of 2.6%, an increase in yield of 92 basis points translates to a drop in price of close to 8%. That may not sound like a lot but it’s a big move in the bond market and it’s especially large if you’re pricing in an historic bull market for bonds.

This ends today’s portion of my day when I criticize Nobel Prize winners in their field. -

The Lost Decade

Eddy Elfenbein, August 27th, 2010 at 9:03 amThe government revised the GDP growth number for Q2 today and it wasn’t good. Instead of growing by 2.4% which the original report said, the economy grew by just 1.6% for the second three months of the year.

As bad as that sounds, Wall Street was expecting even worse. The consensus was to expect 1.3%. Thanks to that “good news,” it looks like stocks are ready to open higher.

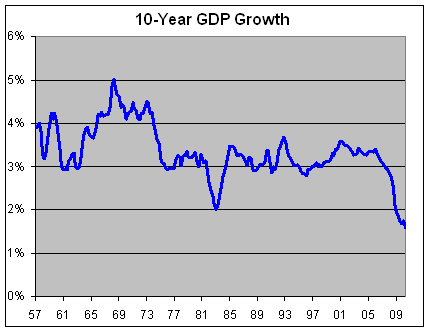

The 1.6% growth rate also matches what the U.S. economy has done over the last ten years. There’s talk of us having a lost decade; we’ve already had one!

Here’s a look at the annualized GDP growth rate over the preceding 10 years:

Since Q2 of 2000, the economy has averaged 1.6% a year which is less than half the growth rate of the preceding 10 years. -

The Low Point in the Presidential Election Cycle

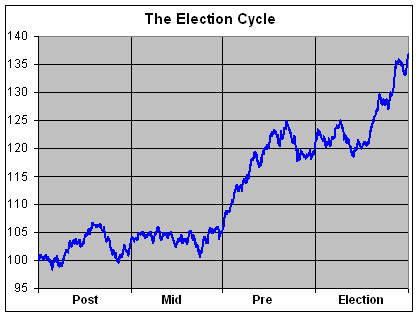

Eddy Elfenbein, August 27th, 2010 at 6:30 amWe’re coming up on an important day for investors. One month from now is the market’s historic low point during the Presidential Election Cycle. Historically, September 30 of the mid-term year is the best time to buy stocks.

A few years ago, I crunched the entire history of the Dow from 1896 to 2007. Here’s what I found:

Historically, the Dow has gained an average of 24.1% from September 30 of the mid-term election year to September 6 of the pre-election year. This means that nearly two-thirds of the Dow’s four-year gain (24.1% of 36.7%) comes in less than one-quarter of the time. That’s a pretty stunning stat.

After September 6 of the pre-election year, the Dow has historically pulled back 5.2% to May 29 of the election year. After that, it puts on a nice 23.2% climb to August 3 of the post election year. Then trouble starts. After September 3, the Dow then pulls back 5.6% and we’re back at our starting point, September 30 of the mid-term election year.

Warning: I don’t put much faith in this statistical oddities for gaining a trading advantage. I simply think they’re interesting in what they reveal about market history.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His