Archive for January, 2013

-

“Founding Father of the Quants Was Revolutionary Marxist”

Eddy Elfenbein, January 16th, 2013 at 5:51 pmCrazy! Here’s a snippet:

Jacob Marschak may not be a household name today, but he inspired a number of financial practitioners and thinkers, from Milton Friedman to Harry Markowitz, and his insights are now the backbone of trading strategies and computer algorithms worldwide.

Marschak was born to a Jewish family in Kiev, Ukraine, in 1898. He played a part in the Russian Revolution as a teenager, working as a Menshevik activist. The liberation of Ukraine from the czar’s Russian Empire vaunted Marschak into the position of labor minister of the short-lived independent state of Terek.

Within months, the state was absorbed by another region and then subsumed into the Soviet Union. A disillusioned Marschak fled to Germany, where he received training in the Austrian School of free-market economics. He hoped to make a permanent home in Germany, but when the Nazis came to power, the Jewish- radical-turned-Marxist-turned-Austrian-School-economist wisely left the country, moving first to England and then to the U.S., where he joined the New School in New York as part of an anti- fascist University in Exile.

-

Remember Volatility?

Eddy Elfenbein, January 16th, 2013 at 4:11 pmCheck out the last five closes for the S&P 500:

January 10: 1,472.12

January 11: 1,472.05

January 14: 1,470.68

January 15: 1,472.34

January 16: 1,472.63That’s an average daily swing over the last four days of just 0.085%. That’s the lowest in more than seven years.

-

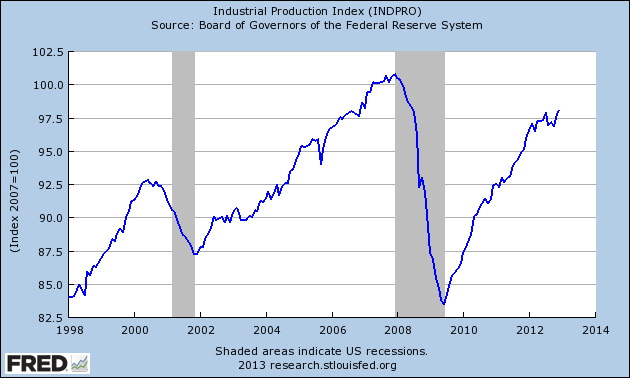

Industrial Production Reaches 4-1/2 Year High

Eddy Elfenbein, January 16th, 2013 at 1:57 pmWe had some important economic reports today. Let’s run down a few highlights:

The government said that consumer inflation was unchanged in December. The “core rate,” which excludes volatile food and energy prices, rose by 0.1%. This exactly matched consensus. For all of 2012, inflation rose by 1.7% while the core rate was up by 1.9%.

The Federal Reserve said that industrial production rose by 0.3% in December. That follows a 1% rise in November which was largely a post-Sandy rebound. Industrial production is now at its highest level since June 2008, and we’re not too far from the all-time high reached in December 2007. Capacity utilization is up to 78.8%.

Yesterday, the Census Bureau reported that retail sales rose 0.5% in December on a seasonally-adjusted basis. Sales were up 4.7% from a year ago. Bill McBride of Calculated Risk notes that retail sales are up 25.4% from the bottom of the recession, and are up 9.7% since the pre-recession peak.

-

VIX Drops to 67-Month Low

Eddy Elfenbein, January 16th, 2013 at 12:13 pmThe Volatility Index ($VIX) got down to 13.20 today. That’s the lowest reading since June 20, 2007.

Here’s a sense of how low volatility is: Three of the last four S&P 500 closes have had 1,472 handles (1,472.34, 1,472.05, 1,472.12), and we’re close to having another one today.

-

JPMorgan Chase Earns $1.39 Per Share

Eddy Elfenbein, January 16th, 2013 at 11:31 amBefore the bell, JPMorgan Chase ($JPM) reported very strong fourth-quarter earnings of $1.39 per share, which easily topped Wall Street’s forecast. CEO Jamie Dimon said, “The firm’s results reflected strong underlying performance across virtually all our businesses for the fourth quarter and the full year, with strong lending and deposit growth.” This was a very good report.

Overall revenue rose 10% to $23.7 billion. I was particularly impressed with JPM’s mortgage business. Revenue in that sector jumped to $2 billion from $723 million in Q4 of 2011. Clearly, the housing rebound is also spilling over to financial services.

Trading results, which were hurt in the third quarter as the price of bank debt rose, were similarly affected in the last three months of 2012. The bank booked a $567 million pretax loss from a so-called debt-valuation adjustment in the fourth quarter as the price of the bank’s debt rose, compared with a $211 million loss in the third quarter.

Fixed-income and equity-markets revenue climbed to $4.07 billion from $3.43 billion a year earlier and declined from $4.77 billion in the third quarter, the company said. Investment-banking and trading revenue is estimated to have jumped 44 percent across the industry from the same quarter in 2011, according to Betsy Graseck, a Morgan Stanley analyst in New York.

(…)

The investment bank’s fixed-income trading book, which contains the remaining credit derivatives position, generated $3.18 billion in revenue compared with $2.63 billion in the fourth quarter of 2011.

Fewer consumers fell behind on their credit-card payments in the fourth quarter compared with the same period in 2011. Loans at least 30 days overdue, a signal of future write- offs, fell to 2.1 percent from 2.81 percent in the fourth quarter of 2011. Write-offs dropped to 3.5 percent from 4.29 percent the prior year and 3.57 percent in the previous quarter.

Consumer banking, which includes home loans and checking accounts, earned $2.01 billion in the fourth quarter, up 28 percent from $1.57 billion a year earlier. Net interest margin, which measures the profit margin on lending, narrowed to 2.4 percent from 2.7 percent a year earlier.

A lot of the headlines around today’s earnings are focusing on the big trading loss from the London Whale. The government is rightly taking the company to task for this. The bank also took a charge of $700 million as part of a settlement for mortgage abuse allegations. In response to the London Whale debacle, JPM’s board slashed Jamie Dimon’s pay in half from $23 million to $11.5 million. On a per-share basis, that’s miniscule. It works out to 0.6 cents per share being cut to 0.3 cents per share.

As I’ve said before, Jamie Dimon gets a great deal of attention but that blurs the fact of how large JPM really is. For the year, the bank earned $21 billion on revenue of $97 billion. The London Whale loss amounted to $6 billion. Yes, it was awful, but hardly life-threatening. In just a few weeks last year, the stock plunged from $43 to $31.

The stock initially dropped this morning after the earnings came out, which is an odd reaction. Since then, however, JPM has steadily rallied and it’s at a new 21-month high.

-

Morning News: January 16, 2013

Eddy Elfenbein, January 16th, 2013 at 7:00 amWorld Bank Cuts Growth Forecasts as Developed Nations Lose Steam

Slowdown in Germany Worries Euro Zone

Japan’s Abe Turns to South East Asia to Counter China

Morgan Stanley Cuts Asia Commodity Jobs Including Two VPs

Fitch Unveils Two Possible Routes to Downgrading U.S. Debt Rating

Rosengren Sees QE Until Jobless Rate Hits 7.25%

ANA and JAL Ground Boeing 787 Fleets After Emergency

Jack Ma’s Retirement Might Mean A 2013 Alibaba IPO For Yahoo Shareholders

While ‘Math’ On Dell Private-Equity Buyout Works, Odds of a Deal ‘Probably Low’

GM Sees Modest Profit Gain This Year

Walmart Plans to Buy American More Often

A.I.G. Seeks Approval to File More Bank Suits

Krispy Kreme Adopts Poison Pill

Joshua Brown: 361 Capital Weekly Research Briefing

John Hempton: Notes On Visiting an Herbalife Nutrition Club in Queens

Be sure to follow me on Twitter.

-

Fiserv Offers Earnings Guidance for 2013

Eddy Elfenbein, January 15th, 2013 at 1:11 pmFiserv ($FISV) is in the news today. The company said that it’s buying Open Solutions for $850 million. Fiserv also offered some earnings guidance:

Based on preliminary information, the company anticipates its 2012 adjusted earnings per share to increase approximately 12 percent over 2011. The company also anticipates its 2012 adjusted internal revenue growth to be at 2 percent for the full year.

On a preliminary basis for 2013, the company expects adjusted internal revenue growth of 3 to 4 percent, and 15 to 18 percent adjusted earnings per share growth over 2012.

The company will supply its actual results for 2012, and formal guidance for 2013, in its year end conference call on February 5, 2013.

Let’s run the numbers. In 2011, Fiserv earned $4.58 per share. So 12% earnings growth comes to $5.13 per share for 2012. For the first three quarters of this year they’ve earned $3.75 per share, so working it out, Fiserv expects $1.38 per share for Q4. That’s below Wall Street’s forecast of $1.42 per share.

For 2013, Fiserv’s growth targets translate to earnings of $5.90 to $6.05 per share. The Street had been expecting $5.78 per share. Despite the poor guidance in the short-term, Fiserv has guided Wall Street significantly higher for this year. Still, the stock is currently down about 2.3% in today’s trading. I like this stock a lot and it’s hardly too expensive at less than 14 times this year’s earnings.

-

Morning News: January 15, 2013

Eddy Elfenbein, January 15th, 2013 at 7:17 amGerman Economy Contracted 0.5 Percent In Fourth-Quarter On Euro Crisis

UK Inflation Holds Steady At 2.7%

Bernanke to Weigh QE Costs as Fed Assets Approach Record

Treasuries Rise Second Day as Lawmakers at Debt Impasse

Fitch Warns of US Downgrade Over Debt Fight

Geithner Says Debt Limit Steps May Run Out By Mid-February

Dell LBO to Test Market’s Appetite for Return to Boom Era

Jack Ma Steps Down As Alibaba Chief

Anglo American to Close Some Platinum Mines

U.K. Retailer HMV Enters Administration

GM Hangs on to Lead Over Volkswagen in Full-Year China Sales

In Unlikely Comeback, Chrysler Is Outgaining Bigger Detroit Rivals

How Pursuit of Billionaire Hit One Dead End

Roger Nusbaum: Your Own Utopia

Cullen Roche: 12 Cognitive Biases that Prevent you From Being Rational

Be sure to follow me on Twitter.

-

Dell Jumps on Possible Buyout News

Eddy Elfenbein, January 14th, 2013 at 2:56 pm

Last month, shares of Dell ($DELL) jumped after an analyst at Goldman wondered whether the company could be the target of a buyout offer. Today Bloomberg is reporting that Dell is talking with two possible suitors.

Round Rock, Texas-based Dell is discussing going private with at least two firms, said one of the people, who declined to be identified because the talks are private. The discussions are preliminary and could fall apart because the firms may not be able to line up the needed financing or resolve how to exit the investment in the future, the people said.

Several large banks have been contacted about financing an offer, one of the people said.

Michael Dell owns 15.7% of the company, so he’s made about $400 million since the Bloomberg story came out.

By the conventional numbers, Dell is cheap at this price. But I wonder how sustainable their business is for the long term.

-

Apple Drops Below $500

Eddy Elfenbein, January 14th, 2013 at 11:39 amIt’s an oddly quiet day today on Wall Street. The indexes are down but not by much. The only news to catch my attention is that shares of Apple ($AAPL) briefly dropped below $500. The stock was over $700 in September. The shares now yield more than a 10-year Treasury bond. Of course, let’s keep in mind Apple’s great run. The stock was below $50 on October 13, 2005.

It’s rather stunning how quickly the market has turned against Apple. I suspect that Apple’s fall has farther to go. Going by the numbers, Apple appears to be cheap. The current consensus is that Apple will earn $57.07 per share in the fiscal year ending in September 2014. Of course, Apple missed earnings the last two reports. The one in July was particularly bad.

I had considered putting Apple on this year’s Buy List but ultimately, I didn’t want to move just yet. I’ve learned that when you use a value strategy for investing, you often get to good stocks too early. Ford is a good example. We were right that it was cheap but it took the market longer than I thought to realize that. There’s a saying on Wall Street that you often make the most money on an investment in the second or third year you own it. Apple’s earnings report is due next Wednesday.

I’m still a little puzzled by the reaction of Wells Fargo ($WFC) to its earnings report. I thought the numbers were pretty good. The stock opened lower on Friday but rallied as the day wore on. The shares opened down again today. Stay tuned for JPM’s earnings report on Wednesday. I’m expecting them to beat consensus.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His