Archive for January, 2013

-

Nicholas Financial Spikes Higher

Eddy Elfenbein, January 9th, 2013 at 11:20 amShares of Nicholas Financial ($NICK) have spiked higher today. I don’t know why. The stock has been as high as $13.89 today. Remember that’s equivalent to $15.89 pre-dividend.

-

Stryker Raises Guidance

Eddy Elfenbein, January 9th, 2013 at 11:07 amEven though none of our Buy List stocks has reported earnings yet, a second stock of ours raised its guidance today. Well, it was only by a penny, but still, we’ll take it. This morning, Stryker ($SYK) said that it expects to earn $4.05 to $4.07 per share for all of 2012. That’s an increase of one penny to the low end.

Stryker also said full-year sales rose 4.2% to $8.7 billion, compared with its October forecast for 4% to 5.5% sales growth.

Sales for the fourth quarter climbed 5.5% to $2.3 billion, while analysts surveyed by Thomson Reuters were expecting a 2% increase to $2.27 billion.

Stryker also said it will book an estimated fourth-quarter charge of $133 million, or 35 cents a share, for its previously disclosed voluntary recall of Rejuvenate and ABG II modular-neck hip stems.

For 2013, Stryker expects current foreign currency exchange rates to reduce sales by as much as 1% in both the first quarter and full year. On a constant currency basis, the company predicts 3% to 5.5% sales growth.

For 2013, Stryker reiterated its full-year forecast for earnings of $4.25 to $4.40 per share. Wall Street had been expecting $4.30 per share. The stock is up 2.3% this morning.

-

Morning News: January 9, 2013

Eddy Elfenbein, January 9th, 2013 at 6:50 amEuribor Rates Unchanged As ECB Seen On Hold

German Industrial Output Misses Expectations

Merkel Economy Shows Neglect as Sick Man Concern Returns

Global Shares Buoyed By Alcoa Earnings, Dollar Gains On Yen

Bank Hacks Were Work of Iranians, Officials Say

Gold Gains a 2nd Day in London on Signs of China Demand

No More Paper Social Security Checks Come March

IRS Delays Tax Season, Will Start Accepting Returns On January 30

A Bold Dissenter at the Fed, Hoping His Doubts Are Wrong

What The $8.5 Billion Foreclosure Deal Means For Borrowers

Barge Owners Say Drought May Wipe Out Mississippi Gains

Blackstone Steps Up Home Buying as Prices Jump

UBS Says Focused On Restoring “Honor” After Scandals

Epicurean Dealmaker: Wherein Your Droll, Semi-Victorian Bloggist Jumps the Shark

Be sure to follow me on Twitter.

-

Be Wary of Top-Down Investing

Eddy Elfenbein, January 8th, 2013 at 12:28 pmInvestors often ask me a question that follows this pattern: “I think X industry is going to be very big in the future, so I want to invest in Y stock. What do you think?”

The X industry is usually something like biotech or green energy or perhaps biotech using green energy. In any event, this thought process towards investing is a mistake. First, X industry may in fact turn out to be a big winner in the future, but that doesn’t mean Y will follow. .

Embryonic industries are notoriously difficult sectors to invest in. There’s a great deal of innovation, prices are plunging and anyone not in first is quickly left behind.

A century ago, if you thought automobiles were the wave of the future, you would have been correct. But, as Wikipedia notes, “there were over 1,800 automobile manufacturers in the United States from 1896 to 1930. Very few survived and only a few new ones were started after that period.” Think on that.

The problem with top-down investing is that it misses that point that profits can be found anywhere. Profits are made wherever a good or service intersects with a need. It’s just that simple; there’s no magic formula. The trick isn’t finding that special industry. Rather, it’s finding that special stock.

Consider the stock of Donaldson ($DCI). What does Donaldson do? I’ll let Hoovers explain:

Grime fighter Donaldson is cleaning up the industrial world. The company makes filtration systems designed to remove contaminants from air and liquids. Donaldson’s engine products business makes air intake and exhaust systems, liquid-filtration systems, and replacement parts; products are sold to manufacturers of construction, mining, and transportation equipment, as well as parts distributors and fleet operators. The company’s industrial products include dust, fume, and mist collectors and air filtration systems used in industrial gas turbines, computer disk drives, and manufacturers’ clean rooms. Founded in 1915, Donaldson now operates in 43 countries worldwide and has 39 manufacturing plants.

My apologies to anyone in the filtration biz but I have to confess that it sounds rather dull. Now imagine that it’s 1989 and you’re trying to think of companies that would be the “wave of the future.” I doubt filtration systems would have been at the top of your list. Yet, Donaldson’s stock is up 50-fold since then and that doesn’t include a dividend that’s risen every year since 1996.

The reason Donaldson has done well is that it’s a very good company. But you only could have known that through analysis that’s bottom-up. For the most part, don’t worry so much about the industry. First, find a very good company.

-

Wall Street Prepares to Celebrate Blah Earnings

Eddy Elfenbein, January 8th, 2013 at 10:33 amThe stock market is down again today but nothing too severe. What’s really interesting is how far the VIX has fallen. It’s been below 14 recently. It seems that once the Fiscal Cliff episode ended, that trade simply collapsed.

Earnings season begins today when Alcoa reports its fourth-quarter earnings. For the broader market, earnings growth is expected to increase by 2.8% from a year ago. That’s not great, but it’s the best growth rate in three quarters.

What’s disturbing is how far expectations for Q4 have fallen. Paul Vigna at the WSJ notes that at the end of September, the Street was expecting Q4 earnings growth of 9.2%. That’s been cut by two-thirds.

Estimates for the first half’s numbers are already coming down as well. Profit growth for the first quarter is now estimated to be about 2.5%, down from a 5.3% estimate at the end of September, and the second-quarter’s forecast has come down to 6.7% from 9.1%.

One curious thought to ponder is the trend in earnings multiples. In October 2011, the P/E Ratio for the market reached a multi-year low. Since then, it’s started to creep higher.

As an investor, it’s unwise to assume earnings multiples will rise. However, historically P/Es have to tended to move in large, multi-year trends. Meaning, if they’re rising, they’ve tended to rise for a long time. When they’ve fallen, they’ve continued to fall for many years. Was a major low reached 15 months ago? I just don’t know.

-

Morning News: January 8, 2013

Eddy Elfenbein, January 8th, 2013 at 6:54 amFiscal, Pay Imbalances Biggest Risks to Economy, WEF Says

Euro-Area Unemployment Rate Rises to Record 11.8% Amid Recession

Euro-Area Economic Sentiment Increased in December

London Quantitative Hedge Funds Report Second Year of Losses

China Throws Gillard Lifeline as Iron Ore Revives

US Banks To Pay $8.5 Billion In Mortgage Settlement

In Mortgage Settlements, B of A Comes Up $5 Billion Short

Rescued by a Bailout, A.I.G. May Sue Its Savior

Samsung Forecasts Record $8.3 Billion Profit

Shutterfly Acquires Cloud-Based Thislife

Sony and BMG Are Said to Team Up on Bid for EMI

Sears Holdings CEO Louis D’Ambrosio Stepping Down

Virgin Atlantic Names U.S.-Born AMR Executive Kreeger as CEO

Roger Nusbaum: The Dakar Rally!

Be sure to follow me on Twitter.

-

Medtronic Raises Guidance

Eddy Elfenbein, January 7th, 2013 at 1:56 pmGood news from Medtronic ($MDT) today. The company raised the lower end of their full-year guidance by four cents per share.

Ever since May, Medtronic has told us to expect fiscal year earnings to range between $3.62 and $3.70 per share. They’ve held firm to that forecast all year. Now they see earnings ranging between $3.66 and $3.70 per share.

Medtronic, which provided the update in conjunction with a presentation at the J.P. Morgan Healthcare Conference in San Francisco, estimated the tax credit will boost full-year earnings by $30 million to $35 million, or 4 cents a share. It expects about 3 cents in the third quarter and 1 cent in the fourth quarter of fiscal 2013.

The fiscal year ends in April, so Q3 earnings are due in about six weeks. For the first six months of this fiscal year, Medtronic earned $1.73 per share. That means we can expect $1.93 to $1.97 for the back end. Medtronic earned $3.46 per share last year.

-

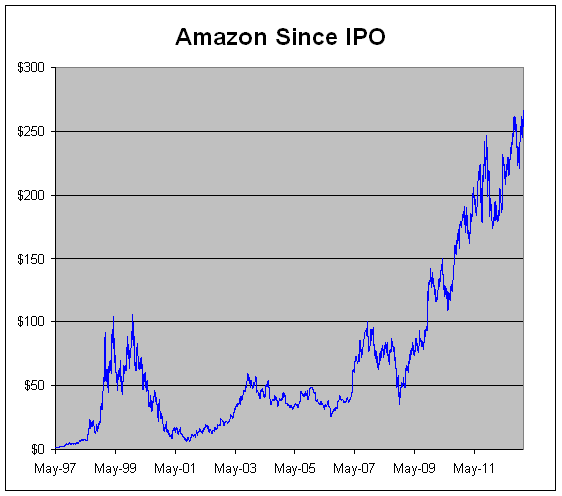

Amazon Breaks $1,600

Eddy Elfenbein, January 7th, 2013 at 1:05 pmIn December 1998, Henry Blodget famously gave Amazon.com ($AMZN) a price target of $400. At the time, the stock was at $242. That day, the stock rose $46, and it went on to break $400 three weeks later.

Since then, AMZN has had two stock splits which add up to 6-to-1. The stock is over $266.66 today which in terms of the day Blodget made his call, is $1,600 per share. Here’s how Amazon has done since its IPO.

Would you have had the nerve to hold on? I know I wouldn’t have. Shortly after 9/11, the stock got as low as $6 per share.

-

Most-Hated Stocks Are Rallying

Eddy Elfenbein, January 7th, 2013 at 12:47 pmSpeculators are abandoning money- losing bets that stocks with the closest links to the U.S. economy will fall as America’s most-hated shares stage the best rally in a year relative to the broader market.

The 20 stocks with the highest short sales in the Standard & Poor’s 500 Index rose an average of 5.1 percent in December, compared with 0.7 percent for the full gauge, according to data compiled by Bloomberg. The performance gap is the widest since January 2012. Companies from U.S. Steel Corp. (X) to J.C. Penney Co. are gaining at the expense of phone companies and utilities, which usually do best when the economy contracts.

Market bulls say the capitulation underscores growing confidence in the U.S. recovery, while bears say the rally shows indiscriminate buying as earnings estimates fall close to a one- year low. The change echoes money manager Laszlo Birinyi’s prediction that the four-year bull market will finally attract investors who have stayed away from equities.

“Let’s put it this way, I made more money on my longs than on my shorts,” Gilles Sitbon, who helps oversee $2.1 billion at Sycomore Asset Management in Paris, said in a phone interview on Jan. 3. His Sycomore Long-Short Opportunities fund rose 15 percent in 2012. “It’s not just hard to be short, it is painful.”

-

The Market Is Down on a Boring Day

Eddy Elfenbein, January 7th, 2013 at 10:52 amI have to confess that today’s a rather boring day on Wall Street. Earnings season hasn’t started yet and there’s not much in the way of economic reports or news. The stock market is down a bit today but that’s coming off Friday’s multi-year high close.

The euro has dropped to a three-week low against the dollar. The European Central Bank meets this week and traders are beginning to think they’ll cut rates. The ECB currently has interest rates at 0.75% but the European economy has been looking pretty weak lately. I’m not sure why they haven’t cut rates before.

Alcoa will be the first major company to report earnings, and that will come tomorrow. For the overall market, earnings growth is expected to improve from the third quarter which was pretty mushy.

Here’s an interesting investing story that’s come to an end today. I always say that hostile buyouts can be tricky for investors. Roche has been trying to buy Illumina for the past year. First, Roche offered Illumina $44.50 per share. They shot that down so Roche went to $51 per share. Well, they shot that down too. Now Roche has said “enough!” and they’re pulling out. Shares of Illumina are down 8% to $50. It will be interesting to see if they regret that move three years from now.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His