Archive for February, 2013

-

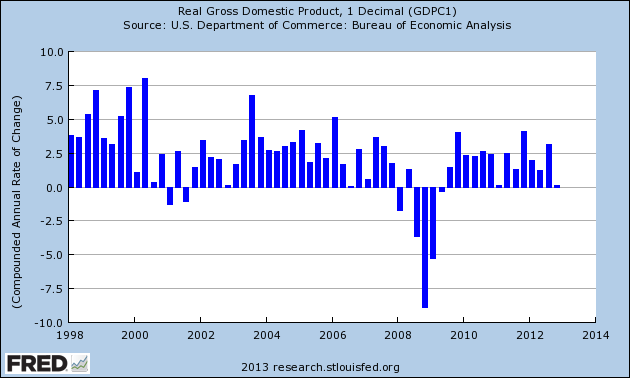

Remarkable Stat on Real GDP

Eddy Elfenbein, February 28th, 2013 at 10:42 amHere’s a stat that I find astonishing:

From 1947 to 1973, real GDP grew by 175.9603%.

From 1973 to 2012, real GDP grew by 175.9607%.In other words, the U.S. economy grew by the same amount over the last 39 years as it did in the 26 years before, despite the latter period being 50% longer. And when I say the same, I mean almost precisely exactly the same.

Here’s quarterly GDP growth for the last few years:

-

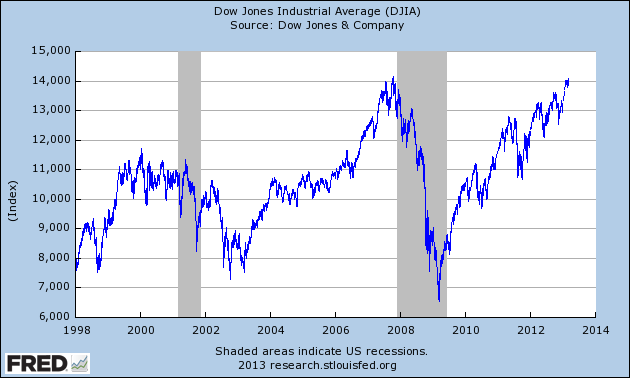

The Dow Closes in on All-Time High

Eddy Elfenbein, February 28th, 2013 at 10:27 amThe Dow closed yesterday just 89.16 points from an all-time high close. This was the highest close for the index in 64 months. To give you an idea of how close we are to making a record, the 30 stocks in the Dow need to rise by a combined total of $11.61. The index has been up as much as 30 points today.

-

Morning News: February 28, 2013

Eddy Elfenbein, February 28th, 2013 at 7:13 amDraghi Says ECB in No Rush to Tighten as Inflation Slows

Monti Says European Crisis Management, Populism Led to Defeat

Banker Bonuses Face Curbs in EU Basel Law Deal

Osborne’s ‘Shrink The Bank’ Strategy Means A Smaller, Less Profitable RBS

Bankia Posts Record 21.2 Billion Euros After-Tax Loss

Wheat Rises as U.S. Export Demand May Increase After Price Drop

Businesses Show Resilience Despite Drop in Goods Orders

Senate, in a More Affable Mode, Backs Treasury Nominee

Groupon Drops 24% On Weak Results, Forecast

Chief Talks of Mistakes and Big Loss at J.C. Penney

Samsung Armors Android to Take On BlackBerry

Wal-Mart Struggles to Restock Store Shelves as U.S. Sales Slump

The Excessive Uproar Over Marissa Mayer’s Telecommuting Ban

Cullen Roche: Nasdaq Sentiment Remains Near its Highest Levels Since March 2000

Jeff Miller: Investors: How tO Profit by Understanding the Fed

Be sure to follow me on Twitter.

-

Update on My Watch List

Eddy Elfenbein, February 27th, 2013 at 1:16 pmI’m often asked how I go about picking stocks for my Buy List. The answer is really quite simple. I don’t have a magic formula and I hate stock screeners.

Instead, I have a Watch List of stocks that I try to follow. These are what I would call “really good companies.” They’re in the top tier of Corporate America. It’s taken me years to build up this list and I change it often.

The Watch List serves as the minor leagues for my Buy List. It’s from this list that almost all candidates for the Buy List come, and it’s where they return after they’ve been deleted.

Let me make it clear that I’m not recommending any of these stocks listed below. That’s what the Buy List is for. I just wanted to show you which stocks make the first cut in the process. Honestly, this list is too large and I should knock off around 30 names. If a stock is on this list, you can be pretty sure it’s a decent company (the price may not be).

My secret formula is nothing more than watching really good companies and making a move when the price looks good.

Company Symbol Aaron’s AAN Abbott Laboratories ABT Advance Auto Parts AAP Alliance Data Systems ADS AmerisourceBergen ABC Ametek AME Ansys ANSS AT&T T AutoZone AZO Balchem BCPC Ball BLL Baxter International BAX Becton, Dickinson BDX Biogen Idec BIIB Carter’s CRI Cerner CERN CH Robinson Worldwide CHRW Cheesecake Factory CAKE Church & Dwight CHD CLARCOR CLC Clorox CLX Coach COH Coca-Cola KO Colgate-Palmolive CL Community Health Systems CYH Concur Technologies CNQR Cooper COO Corrections of America CXW Costco COST Crane CR Cummins CMI CVS Caremark CVS Danaher DHR Darden Restaurants DRI DaVita HealthCare Partners DVA Deckers Outdoor DECK Deluxe DLX DENTSPLY International XRAY Dick’s Sporting Goods DKS Dolby Laboratories DLB Donaldson Company DCI Endo Health Solutions ENDP Esterline Technologies ESL Expeditors International of Washington EXPD Express Scripts ESRX Fair Isaac FICO Fastenal Company FAST FMC Technologies FTI Foot Locker FL Gardner Denver GDI Gartner IT General Dynamics GD Gentex GNTX Gilead Sciences GILD Global Payments GPN Graco GGG Hasbro HAS HEICO HEI Henry Schein HSIC HMS Holdings HMSY Hologic HOLX Hormel Foods HRL Hospira HSP HSN HSNI Hubbell HUB-B Humana HUM IBM IBM IDEX IEX IDEXX Laboratories IDXX Informatica INFA Infosys Ltd. INFY Ingram Micro IM Ingredion Incorporated INGR Intel INTC IntercontinentalExchange ICE International Flavors & Fragrances IFF Intuit INTU Intuitive Surgical ISRG Iron Mountain IRM Jack Henry & Associates JKHY Jarden JAH JB Hunt Transport Services JBHT John Wiley & Sons JW-A Johnson & Johnson JNJ Kansas City Southern KSU Life Time Fitness LTM McCormick MKC McDonald’s MCD MEDNAX MD Mettler-Toledo International MTD MICROS Systems MCRS Mylan MYL NeuStar NSR Nike NKE Nordson NDSN Panera Bread PNRA Pentair Ltd. PNR PetSmart PETM Polaris Industries PII Progressive PGR Prosperity Bancshares PB Quest Diagnostics DGX Rackspace Hosting RAX Raven Industries RAVN Regal Beloit RBC Reinsurance Group of America RGA Rent-A-Center RCII ResMed RMD Reynolds American RAI Riverbed Technology RVBD Rollins ROL Seaboard SEB SEI Investments SEIC Seneca Foods SENEA Sensient Technologies SXT Sigma-Aldrich SIAL Signature Bank SBNY Silgan Holdings SLGN Snap-on SNA SolarWinds SWI St. Jude Medical STJ Starbucks SBUX State Street STT Stericycle SRCL Sysco SYY Target TGT Tech Data TECD Teradata TDC Thermo Fisher Scientific TMO Thoratec THOR TIBCO Software TIBX Tiffany & TIF TJX Companies TJX Towers Watson & TW Tractor Supply TSCO Trimble Navigation Limited TRMB Triumph Group TGI Tupperware Brands TUP U.S. Bancorp USB Universal Health Services UHS URS URS V.F. VFC Varian Medical Systems VAR VeriFone Systems PAY Visa V W.W. Grainger GWW Wabtec WAB Walgreen WAG Waters WAT WellPoint WLP Wells Fargo WFC Western Union WU Weyco Group WEYS World Fuel Services INT Yum! Brands YUM Zimmer Holdings ZMH -

My Plan

Eddy Elfenbein, February 27th, 2013 at 10:11 amStep One: Form bank holding company, the Bank of Eddy.

Step Two: Borrow $470 billion from the Federal Reserve at 0%.

Step Three: Announce tender offer to buy out Apple for $500 per share.

Step Four: Once I have control of Apple, use the $140 billion in cash to buy all the mortgage debt I can possibly find. (Also, buy CNBC.)

Step Five: Every six month, IPO a different Apple division. Spin-offs, you know, outperform.

Step Six: Use proceeds to pay off the Fed.

Step Seven: Distribute the rest to Bank of Eddy shareholders minus, of course, my $10 billion fee.

Step Eight: Relax at pool.

So…who’s with me?

-

The Yen’s Impact on AFLAC’s Earnings

Eddy Elfenbein, February 27th, 2013 at 9:55 amBelow I’ve tried to reproduce a chart from AFLAC’s latest 10-K. This shows the impact that the yen/dollar exchange rate is expected to have on AFLAC’s 2013 operating earings.

Exchange Rate EPS Range Growth Rate Yen Impact 79.81 $6.86 to $7.06 3.9% to 7.0% $0.00 85 $6.60 to $6.80 0% to 3% -$0.26 90 $6.37 to $6.57 (3.5%) to (0.5%) -$0.49 95 $6.17 to $6.37 (6.5%) to (3.5%) -$0.69 100 $5.99 to $6.19 (9.2%) to (6.2%) -$0.87 Here’s a look at the surge in the dollar since October:

Market Up a Bit, Ben’s Speaking Again

Eddy Elfenbein, February 27th, 2013 at 9:41 amThe market is signaling higher today. Ben Bernanke speaks again before Congress. This time, he heads over to the House of Capitol Hill.

This morning, we learned that durable goods orders fell 5.2% last month which was worse than Wall Street’s forecast of a 4.8% decline. But if we look at nondefense orders excluding aircraft, then durable goods rose by 6.3%. That was well above the Street’s forecast of no growth.

Morning News: February 27, 2013

Eddy Elfenbein, February 27th, 2013 at 6:54 amEuro Strengthens as Italian Bonds Fluctuate After Debt Auction

Italian Borrowing Costs Jump But Demand Remains Strong At Crucial Auction

EU Moves Closer To Imposing Caps On Banker Bonuses

India’s Downturn ‘More Or Less Over’

Bernanke Defends Asset Buying as Benefits Outweigh Risks

Austerity Kills Government Jobs as Cuts to Budgets Loom

S.E.C. Nominee Tries to Allay Skepticism

Wall Street Pay Rises, for Those Who Still Have a Job

Home Prices in 20 U.S. Cities Increase by Most Since 2006

Wall Street Junk Kings Selling Debt Poised to Lose Value

JPMorgan Mortgage, Community Units to Lose Up to 19,000 Jobs

AB InBev’s Profit Gains as U.S., Brazil Beer Shipments Rise

Teleworking: The Myth Of Working From Home

Edward Harrison: On Bernanke’s Testimony

John Hempton: Gulfport Energy’s Accounts Payable and Accrued Liabilities

Be sure to follow me on Twitter.

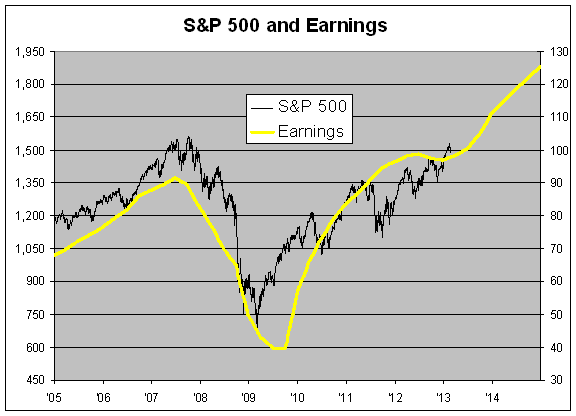

The S&P 500 and Its Earnings

Eddy Elfenbein, February 26th, 2013 at 4:04 pmHere’s an update of a chart I run every so often. This is the S&P 500 along with its operating earnings.

There are, however, two changes with this chart. One, this is the first time I’ve had earnings estimates for 2014. Please note that these aren’t my estimates. These are the consensus numbers provided by S&P.

The other change is that I normally scale the two lines at a ratio of 16-to-1. This time, I lowered it to 15-to-1. That’s not a judgment on proper valuation. I simply think it makes the chart look better.

I’m still surprised that Wall Street expects earnings growth to reaccelerate so robustly later this year and into 2014. I certainly hope it happens, but hope isn’t an investment strategy.

The final earnings number for 2012 should be about $96.95. The Street expects $111.22 for 2013 and $125.44 for 2014. Hmmm…not sure about that….

Bernanke’s Testimony Today

Eddy Elfenbein, February 26th, 2013 at 10:02 amChairman Johnson, Ranking Member Crapo, and other members of the Committee, I am pleased to present the Federal Reserve’s semiannual Monetary Policy Report. I will begin with a short summary of current economic conditions and then discuss aspects of monetary and fiscal policy.

Current Economic Conditions

Since I last reported to this Committee in mid-2012, economic activity in the United States has continued to expand at a moderate if somewhat uneven pace. In particular, real gross domestic product (GDP) is estimated to have risen at an annual rate of about 3 percent in the third quarter but to have been essentially flat in the fourth quarter. The pause in real GDP growth last quarter does not appear to reflect a stalling-out of the recovery. Rather, economic activity was temporarily restrained by weather-related disruptions and by transitory declines in a few volatile categories of spending, even as demand by U.S. households and businesses continued to expand. Available information suggests that economic growth has picked up again this year.

Consistent with the moderate pace of economic growth, conditions in the labor market have been improving gradually. Since July, nonfarm payroll employment has increased by 175,000 jobs per month on average, and the unemployment rate declined 0.3 percentage point to 7.9 percent over the same period. Cumulatively, private-sector payrolls have now grown by about 6.1 million jobs since their low point in early 2010, and the unemployment rate has fallen a bit more than 2 percentage points since its cyclical peak in late 2009. Despite these gains, however, the job market remains generally weak, with the unemployment rate well above its longer-run normal level. About 4.7 million of the unemployed have been without a job for six months or more, and millions more would like full-time employment but are able to find only part-time work. High unemployment has substantial costs, including not only the hardship faced by the unemployed and their families, but also the harm done to the vitality and productive potential of our economy as a whole. Lengthy periods of unemployment and underemployment can erode workers’ skills and attachment to the labor force or prevent young people from gaining skills and experience in the first place–developments that could significantly reduce their productivity and earnings in the longer term. The loss of output and earnings associated with high unemployment also reduces government revenues and increases spending, thereby leading to larger deficits and higher levels of debt.

The recent increase in gasoline prices, which reflects both higher crude oil prices and wider refining margins, is hitting family budgets. However, overall inflation remains low. Over the second half of 2012, the price index for personal consumption expenditures rose at an annual rate of 1-1/2 percent, similar to the rate of increase in the first half of the year. Measures of longer-term inflation expectations have remained in the narrow ranges seen over the past several years. Against this backdrop, the Federal Open Market Committee (FOMC) anticipates that inflation over the medium term likely will run at or below its 2 percent objective.

Monetary Policy

With unemployment well above normal levels and inflation subdued, progress toward the Federal Reserve’s mandated objectives of maximum employment and price stability has required a highly accommodative monetary policy. Under normal circumstances, policy accommodation would be provided through reductions in the FOMC’s target for the federal funds rate–the interest rate on overnight loans between banks. However, as this rate has been close to zero since December 2008, the Federal Reserve has had to use alternative policy tools.

These alternative tools have fallen into two categories. The first is “forward guidance” regarding the FOMC’s anticipated path for the federal funds rate. Since longer-term interest rates reflect market expectations for shorter-term rates over time, our guidance influences longer-term rates and thus supports a stronger recovery. The formulation of this guidance has evolved over time. Between August 2011 and December 2012, the Committee used calendar dates to indicate how long it expected economic conditions to warrant exceptionally low levels for the federal funds rate. At its December 2012 meeting, the FOMC agreed to shift to providing more explicit guidance on how it expects the policy rate to respond to economic developments. Specifically, the December postmeeting statement indicated that the current exceptionally low range for the federal funds rate “will be appropriate at least as long as the unemployment rate remains above 6-1/2 percent, inflation between one and two years ahead is projected to be no more than a half percentage point above the Committee’s 2 percent longer-run goal, and longer-term inflation expectations continue to be well anchored.” An advantage of the new formulation, relative to the previous date-based guidance, is that it allows market participants and the public to update their monetary policy expectations more accurately in response to new information about the economic outlook. The new guidance also serves to underscore the Committee’s intention to maintain accommodation as long as needed to promote a stronger economic recovery with stable prices.

The second type of nontraditional policy tool employed by the FOMC is large-scale purchases of longer-term securities, which, like our forward guidance, are intended to support economic growth by putting downward pressure on longer-term interest rates. The Federal Reserve has engaged in several rounds of such purchases since late 2008. Last September the FOMC announced that it would purchase agency mortgage-backed securities at a pace of $40 billion per month, and in December the Committee stated that, in addition, beginning in January it would purchase longer-term Treasury securities at an initial pace of $45 billion per month. These additional purchases of longer-term Treasury securities replace the purchases we were conducting under our now-completed maturity extension program, which lengthened the maturity of our securities portfolio without increasing its size. The FOMC has indicated that it will continue purchases until it observes a substantial improvement in the outlook for the labor market in a context of price stability.

The Committee also stated that in determining the size, pace, and composition of its asset purchases, it will take appropriate account of their likely efficacy and costs. In other words, as with all of its policy decisions, the Committee continues to assess its program of asset purchases within a cost-benefit framework. In the current economic environment, the benefits of asset purchases, and of policy accommodation more generally, are clear: Monetary policy is providing important support to the recovery while keeping inflation close to the FOMC’s 2 percent objective. Notably, keeping longer-term interest rates low has helped spark recovery in the housing market and led to increased sales and production of automobiles and other durable goods. By raising employment and household wealth–for example, through higher home prices–these developments have in turn supported consumer sentiment and spending.

Highly accommodative monetary policy also has several potential costs and risks, which the Committee is monitoring closely. For example, if further expansion of the Federal Reserve’s balance sheet were to undermine public confidence in our ability to exit smoothly from our accommodative policies at the appropriate time, inflation expectations could rise, putting the FOMC’s price-stability objective at risk. However, the Committee remains confident that it has the tools necessary to tighten monetary policy when the time comes to do so. As I noted, inflation is currently subdued, and inflation expectations appear well anchored; neither the FOMC nor private forecasters are projecting the development of significant inflation pressures.

Another potential cost that the Committee takes very seriously is the possibility that very low interest rates, if maintained for a considerable time, could impair financial stability. For example, portfolio managers dissatisfied with low returns may “reach for yield” by taking on more credit risk, duration risk, or leverage. On the other hand, some risk-taking–such as when an entrepreneur takes out a loan to start a new business or an existing firm expands capacity–is a necessary element of a healthy economic recovery. Moreover, although accommodative monetary policies may increase certain types of risk-taking, in the present circumstances they also serve in some ways to reduce risk in the system, most importantly by strengthening the overall economy, but also by encouraging firms to rely more on longer-term funding, and by reducing debt service costs for households and businesses. In any case, the Federal Reserve is responding actively to financial stability concerns through substantially expanded monitoring of emerging risks in the financial system, an approach to the supervision of financial firms that takes a more systemic perspective, and the ongoing implementation of reforms to make the financial system more transparent and resilient. Although a long period of low rates could encourage excessive risk-taking, and continued close attention to such developments is certainly warranted, to this point we do not see the potential costs of the increased risk-taking in some financial markets as outweighing the benefits of promoting a stronger economic recovery and more-rapid job creation.

Another aspect of the Federal Reserve’s policies that has been discussed is their implications for the federal budget. The Federal Reserve earns substantial interest on the assets it holds in its portfolio, and, other than the amount needed to fund our cost of operations, all net income is remitted to the Treasury. With the expansion of the Federal Reserve’s balance sheet, yearly remittances have roughly tripled in recent years, with payments to the Treasury totaling approximately $290 billion between 2009 and 2012. However, if the economy continues to strengthen, as we anticipate, and policy accommodation is accordingly reduced, these remittances would likely decline in coming years. Federal Reserve analysis shows that remittances to the Treasury could be quite low for a time in some scenarios, particularly if interest rates were to rise quickly. However, even in such scenarios, it is highly likely that average annual remittances over the period affected by the Federal Reserve’s purchases will remain higher than the pre-crisis norm, perhaps substantially so. Moreover, to the extent that monetary policy promotes growth and job creation, the resulting reduction in the federal deficit would dwarf any variation in the Federal Reserve’s remittances to the Treasury.

Thoughts on Fiscal Policy

Although monetary policy is working to promote a more robust recovery, it cannot carry the entire burden of ensuring a speedier return to economic health. The economy’s performance both over the near term and in the longer run will depend importantly on the course of fiscal policy. The challenge for the Congress and the Administration is to put the federal budget on a sustainable long-run path that promotes economic growth and stability without unnecessarily impeding the current recovery.

Significant progress has been made recently toward reducing the federal budget deficit over the next few years. The projections released earlier this month by the Congressional Budget Office (CBO) indicate that, under current law, the federal deficit will narrow from 7 percent of GDP last year to 2-1/2 percent in fiscal year 2015. As a result, the federal debt held by the public (including that held by the Federal Reserve) is projected to remain roughly 75 percent of GDP through much of the current decade.

However, a substantial portion of the recent progress in lowering the deficit has been concentrated in near-term budget changes, which, taken together, could create a significant headwind for the economic recovery. The CBO estimates that deficit-reduction policies in current law will slow the pace of real GDP growth by about 1-1/2 percentage points this year, relative to what it would have been otherwise. A significant portion of this effect is related to the automatic spending sequestration that is scheduled to begin on March 1, which, according to the CBO’s estimates, will contribute about 0.6 percentage point to the fiscal drag on economic growth this year. Given the still-moderate underlying pace of economic growth, this additional near-term burden on the recovery is significant. Moreover, besides having adverse effects on jobs and incomes, a slower recovery would lead to less actual deficit reduction in the short run for any given set of fiscal actions.

At the same time, and despite progress in reducing near-term budget deficits, the difficult process of addressing longer-term fiscal imbalances has only begun. Indeed, the CBO projects that the federal deficit and debt as a percentage of GDP will begin rising again in the latter part of this decade, reflecting in large part the aging of the population and fast-rising health-care costs. To promote economic growth in the longer term, and to preserve economic and financial stability, fiscal policymakers will have to put the federal budget on a sustainable long-run path that first stabilizes the ratio of federal debt to GDP and, given the current elevated level of debt, eventually places that ratio on a downward trajectory. Between 1960 and the onset of the financial crisis, federal debt averaged less than 40 percent of GDP. This relatively low level of debt provided the nation much-needed flexibility to meet the economic challenges of the past few years. Replenishing this fiscal capacity will give future Congresses and Administrations greater scope to deal with unforeseen events.

To address both the near- and longer-term issues, the Congress and the Administration should consider replacing the sharp, frontloaded spending cuts required by the sequestration with policies that reduce the federal deficit more gradually in the near term but more substantially in the longer run. Such an approach could lessen the near-term fiscal headwinds facing the recovery while more effectively addressing the longer-term imbalances in the federal budget.

The sizes of deficits and debt matter, of course, but not all tax and spending programs are created equal with respect to their effects on the economy. To the greatest extent possible, in their efforts to achieve sound public finances, fiscal policymakers should not lose sight of the need for federal tax and spending policies that increase incentives to work and save, encourage investments in workforce skills, advance private capital formation, promote research and development, and provide necessary and productive public infrastructure. Although economic growth alone cannot eliminate federal budget imbalances, in either the short or longer term, a more rapidly expanding economic pie will ease the difficult choices we face.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His