Archive for February, 2013

-

Inflation Is a Tax on Capital

Eddy Elfenbein, February 19th, 2013 at 11:36 amRoben Farzad writes at Bloomberg Businessweek:

Longtime readers of BusinessWeek (now Bloomberg Businessweek) will recall its Dewey-Defeats-Truman moment: A 1979 A 1979 cover story that heralded the “Death of Equities: How Inflation is Destroying the Stock Market.” Inflation was the bogeyman of the late 1970s and early ’80s, an oft-cursed scourge to the average family’s buying power. The problem with BusinessWeek’s headline declaration is that it came shortly before the Paul Volcker Federal Reserve vanquished runaway inflation, setting up an 18-year bull market.

Since that bull maxed out 13 years ago, the market has pretty much gone to hell and back, twice. While inflation has been consistently in the low single digits, it hasn’t been as irrelevant as many investors imagine. Indeed, like termites coring out a wooden house, rising prices have already set them back a long way.

“Inflation,” says Crossing Wall Street‘s Eddy Elfenbein, “is a tax on capital and it slowly eats away at your portfolio. Even a low rate of inflation—say, 3 percent per year—compounds to 50 percent in less than 14 years. It’s proverbial running to stand still.”

In simple terms, if you were to take the Standard & Poor’s 500-stock index’s fin de siècle high and factor in the subsequent growth in the consumer price index, the market is 27 percent below its inflation (as the government defines it)-adjusted high. So much for the few percent we need to hit that market record you’re hearing so much about of late.

-

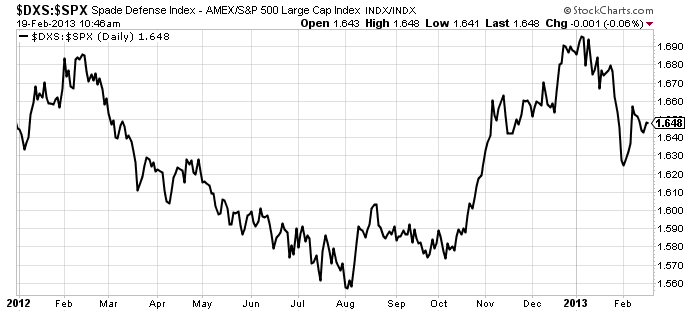

Is the Sequester Really Going to Happen?

Eddy Elfenbein, February 19th, 2013 at 10:51 amWe’re getting down to the wire and if nothing is done, automatic spending cuts will go into effect. The conventional wisdom seems to think the cuts will happen.

Fortunately, I have a better tool than the conventional wisdom and that’s the stock market. Here’s a look at the Spade Defense Index divided by the S&P 500. This is a key metric because much of the cuts will hurt the Pentagon.

Defense stocks started to lag the market at the beginning of the year, but have reversed course somewhat this month.

-

Medtronic Earns 93 Cents Per Share

Eddy Elfenbein, February 19th, 2013 at 10:35 amThe stock market is doing well this morning. The S&P 500 has been as high as 1,526.82, which is yet another multi-year high. The market is trying to extend its weekly winning streak to eight. This is a good way to start.

Investors have impressively run past a lot of minor negatives that easily could have hurt stocks in previous markets. The earnings news continues to be decent. The latest numbers show that 388 companies in the S&P 500 have reported Q4 earnings. Of that, 69.8% have beaten expectations. Compare that with the long-run average of 62%. Earnings are up 5.6% from one year ago, and 1.9% above expectations.

Our latest Buy List stock to report earnings was Medtronic ($MDT). For their fiscal third quarter, Medtronic earned 93 cents per share which was two cents better than Wall Street’s forecast. That’s an increase from 84 cents per share a year ago. Sales rose 2.8% to $4.03 billion which was $10 million below forecasts.

Medtronic once again reiterated their full-year earnings forecast of $3.66 to $3.70 per share. For clarity, Medtronic’s fiscal year ends in April. MDT is our first Buy List stock in the January-April-July-October cycle to report earnings. The shares are currently down about 3.3% although I don’t see why. In today’s earnings release, the CEO said:

“We are playing a leading role in transforming global healthcare by implementing our long-term strategies of economic value and globalization,” said Ishrak. “We are only at the beginning of establishing our track record, but we believe that crisp execution of both our baseline and long-term growth strategies, combined with strong and disciplined capital allocation, will enable us to create long-term dependable value in healthcare.”

Shawn Tully at CNN/Money makes a good point about Medtronic. The dividend yield is 2.3% and the repurchases come to 3.7% for a total shareholder yield of 6.0%.

-

Morning News: February 19, 2013

Eddy Elfenbein, February 19th, 2013 at 6:50 amMerkel Cites East German Lessons for EU’s Problem States

German February Investor Confidence Jumps to Three-Year High

Draghi Seeks to Ease Talk of Global Currency War

Yen Rises After Aso Rules Out Japan’s Foreign-Debt Buying

Chinese Army Unit Is Seen as Tied to Hacking Against U.S.

Japan’s Orix Buys Dutch Asset Manager

Swelling U.S. Labor Force Keeps Fed at Ease

Get A Social Security Check? Treasury Says It’s Time To Go Electronic

Buffett Cash Makes General Mills to Grainger Target

Reader’s Digest Brand is Key to Strategy in Bankruptcy

Xstrata Unit Wins Environmental Approval For $5.9 Billion Philippine Mine

Novartis Scraps Non-Compete Payment to Departing Chairman

Paulson Leads Funds to Bermuda Tax Dodge Aiding Billionaires

Cullen Roche: Barron’s Doesn’t Do Monetary Realism

Credit Writedowns: Will The Corporate Sector Expansion Peak In Spring Once Again?

Be sure to follow me on Twitter.

-

Morning News: February 18, 2013

Eddy Elfenbein, February 18th, 2013 at 6:46 amGerman Banks’ Use Of ECB Funds Drops Sharply In January

In Europe’s Tax Race, It’s The Base, Not The Rate, That Counts

Debt Bubble Born of Easy Cash Prompts Swedish Rule Review

China’s Yen For Currency Appreciation

“Nothing To Hide” In Helicopter Deal, India’s Prime Minister Says

Obama Faces Risks in Pipeline Decision

American Airlines Bankruptcy, Merger Deals Were Complex, Expensive

Independent News Plans $226 Million South Africa Disposal

Facebook, The Coolest Cutest Corporate Welfare Queen Of Them All

Tech Industry Sets Its Sights on Gambling

Danone Dairy Woes a Challenge for Peltz’s Heinz Playbook

Carlsberg Slumps as Brewer Scraps Medium-Term Margin Goal

Howard Lindzon: My Kingdom For A Hedge!

Jeff Miller: Weighing the Week Ahead: Is the Housing Rebound for Real?

Be sure to follow me on Twitter.

-

Paperman

Eddy Elfenbein, February 15th, 2013 at 4:02 pm -

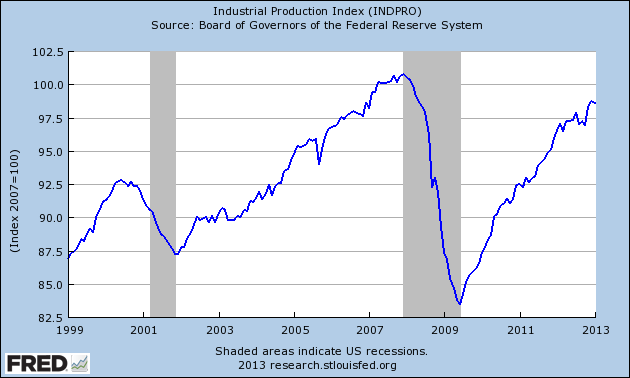

January Industrial Production Falls 0.1%

Eddy Elfenbein, February 15th, 2013 at 11:09 amIndustrial production fell by 0.1% in January. Economists were expecting an increase of 0.2%.

Output last month was pushed down by a 0.4 percent drop in manufacturing production, which reflected a 3.2 percent decline in motor vehicle assembly. Manufacturing output had increased 1.1 percent in December.

Production at the nation’s mines fell 1 percent.

With industrial output weak, the amount of capacity in use fell to 79.1 percent from 79.3 percent in December.

Industrial capacity utilization — a measure of how fully firms are using their resources — was 1.1 percentage points below its long-run average.

Officials at the Fed tend to look at utilization measures as a signal of how much “slack” remains in the economy, and how much room growth has to run before it becomes inflationary.

-

The VIX Hits Six-Year Low

Eddy Elfenbein, February 15th, 2013 at 10:19 amThis morning, the Volatility Index ($VIX) got down to 12.25 which is the lowest reading since April 23, 2007.

-

DirecTV’s Outlook for 2013

Eddy Elfenbein, February 15th, 2013 at 9:21 amAfter DirecTV ($DTV) reported great earnings yesterday, the stock opened higher, but the shares retreated throughout the day.

I think traders were unnerved by the company’s loss on Venezuela’s currency devaluation. According to the earnings call, the devaluation will cost DTV “approximately $160 million.”

Still, the company has a fairly upbeat outlook. DirecTV specifically said, “we’re forecasting earnings per share to be $5 or greater in 2013.”

Here are some key bits from the earnings call:

Next I would like to make a few comments about our consolidated outlook. Let me begin by providing some additional color on our EPS outlook for 2013. Depreciation expense at DIRECTV Latin America and DIRECTV U.S. will increase by roughly 30% and 10%, respectively, compared to 2012. In addition, our effective tax rate will also be a few percentage points higher in 2013 as our 2012 rate benefited from the completion of a prior year audit, and we don’t expect to have benefit going forward. As a result, we’re expecting our effective tax rate this year to be in the mid-to-high 30% range. Having said that, excluding onetime items such as the Venezuela pretax devaluation charge of approximately $160 million, our guidance that we provided at our Investor Day in December 2010 remains intact as we’re forecasting earnings per share to be $5 or greater in 2013. Free cash flow will likely come in lower than 2012 levels due mostly to the impact of the Venezuelan devaluation, as well as from higher taxes and interest. Cash taxes are expected to be higher in 2013 due to greater earnings before taxes, and a higher cash tax rate is expected to be in the mid-to-high 30% range, primarily due to an expected tax payment in 2013 upon the close of a tax audit, reversal of depreciation of benefits associated with prior year economic stimulus programs and the absence of a state tax credit carryforward that we had in 2012.

Finally, in terms of DIRECTV’s strategy for returning capital, I’d like to first point out that our top priority for creating shareholder value remains to reinvest in our businesses. And as you heard from Mike earlier, if opportunities do not arise that meet our regular strategic and financial hurdles, we will continue our capital allocation strategy for share repurchases as we believe DIRECTV stock remains significantly undervalued. As such, on Tuesday, our Board of Directors authorized a new $4 billion share repurchase program and terminated the balance of roughly $860 million that remained from the previous authorization. We’re expecting that this new authorization will provide sufficient funding to support our buyback program through early next year.

All in all, we entered 2013 from a position of strength, thanks to our strong balance sheet, cash flow, competitive position and quality subscriber base across the Americas. And if we accomplish all of our targets and deliver the expected financial results, I believe we will continue to lead the industry in revenue and earnings growth, as well as creating substantial shareholder value.

-

CWS Market Review – February 15, 2013

Eddy Elfenbein, February 15th, 2013 at 6:07 am“Individuals who cannot master their emotions are ill-suited to

profit from the investment process.” – Benjamin GrahamRemember when stock prices used to change each day?

OK, I’m exaggerating…but not by much. Bespoke Investment Group notes that the average daily spread between the high and the low on the Dow Jones is at a 26-year low. Stocks simply ain’t moving around very much these days.

While the stock market got off to a great start this year, since late January it’s nearly slowed down to a complete halt, particularly the intra-day swings. The Volatility Index ($VIX) is near a six-year low. Fortunately, the little volatility there has been has been positive, so the broad market indexes have continued to rise, albeit very slowly. On Thursday, the S&P 500 closed at its highest level since Halloween 2007.

One theme that’s been dominating Wall Street lately is the idea of a Great Rotation, meaning money will massively swarm out of bonds and into stocks. I do think some of that will happen—in fact, it’s currently happening—but I don’t foresee sky-high bond yields anytime soon. The 10-year T-bond is right at 2%, which is pretty darn low. Instead, what we’re seeing is investors gradually becoming bolder and taking on more risk. That’s very good for our style of investing.

In this week’s CWS Market Review, I want to take a closer look at this moribund market. As quiet as it’s been, I don’t think the market’s reticence will last much longer. I also want to highlight an outstanding earnings report from DirecTV ($DTV). The stock crushed Wall Street’s estimate by 42 cents per share! We’ll also focus on Bed, Bath & Beyond ($BBBY), which has finally drifted low enough to be a very compelling buy. But first, let’s look at what’s been happening on the street of dreams.

Investors Need to Focus on High-Quality Stocks

One important development is that economically cyclical stocks are again leading the market. If you recall, the cyclicals began a massive rally last summer right around the time when Mario Draghi promised to do “whatever it takes” to save the euro. The cyclicals were given another boost a few weeks after that when the Fed announced its QE-Infinity program.

Consider this: If the S&P 500 had kept pace with cyclicals, it would be at about 1,750 today instead of 1,521. Cyclical leadership finally petered out in late January but has come back with a vengeance. The Morgan Stanley Cyclical Index (CYC) has outpaced the S&P 500 for five days in a row. The ratio of the Cyclical Index to the S&P 500 is now close to an 18-month high.

I think there are two reasons for this trend. One is simply that many cyclical stocks got very cheap. I think our own Ford Motor ($F) is a perfect example of that. Harris ($HRS) and Moog ($MOG-A) are other good examples. But another reason is that economy is probably better than many analysts realize. The negative GDP report for Q4 understandably upset a lot of folks, but the recent trade numbers will probably cause that negative 0.1% to be revised upward to somewhere around +1.0%.

Earnings for Q4 have been pretty. According to data from Bloomberg, 73% of the 288 companies in the S&P 500 that have reported Q4 earnings have topped estimates; 67% have beaten sales estimates. As I’ve discussed before, the major concern is that corporate profit margins have been stretched about as far as they can go. I’m concerned that Wall Street’s earnings forecasts are too optimistic, and we’re going to see a spate of earnings as the year goes on.

One of the interesting aspects of the recent rally is that the large mega-caps haven’t really joined in. Since the beginning of October, the S&P 100, which is the biggest stocks in the S&P 500, has consistently lagged the S&P 500. That’s not necessarily bad news, but it means that the little guys are getting most of the gains. One possible worry is that the gains are largely going to low-quality names. That’s often a sign of a market peak. Our Buy List, for example, started trailing the overall market in 2007. But when the plunge came, we didn’t fall nearly as much as rest of the market.

Until this sleepy market eventually wakes up, I urge investors to focus on top-quality. Please pay close attention to my Buy Below prices on the Buy List. We don’t want to go chasing after stocks. Let the good stocks come to you. Speaking of which, my favorite satellite TV stock just reported great earnings, and the stock is lower than where it was five months ago.

Buy DirecTV Up to $55 per Share

We had very good news on Thursday when our satellite-TV stock, DirecTV ($DTV), reported blow-out earnings for Q4. The company raked in $1.55 per share for the quarter, which creamed Wall Street’s forecast by 42 cents per share. Wow! For comparison, DTV made $1.02 per share in the fourth quarter of 2011,

So what’s the secret to DirecTV’s success? That’s easy; it’s all about Latin America. DirecTV has done very well in the United States, but that’s a fairly saturated market. Not so in the Latin world, where satellite TV demand is just getting started. DTV now has 10.3 million subscribers in Latin America, up from 7.9 million one year ago. Last quarter, DirecTV added 658,000 customers in Latin America, which was a lot more than expected.

For Q4, DirecTV added 103,000 subscribers in America, which brings their total to 20.1 million. That’s a big business, and I especially like anything involving recurring revenue. The company said it expects to see mid-single-digit revenue growth in the U.S. over the next three years. I was also pleased to see that the cancellation rate in the U.S. dropped from 1.52% to 1.43%. DirecTV has specifically made an effort to increase retention. The cost of adding one new subscriber is far more than that of retaining an existing one. For all of 2012, DTV had a solid year, earning $4.58 per share.

The only negative is that DTV said its earnings will take a one-time hit from the currency devaluation in Venezuela. The company also announced a $4 billion share buyback, which is equivalent to about 13% of DTV’s market value. I think DTV should have little trouble earning $5 per share this year. This is a good stock going for a good value. DirecTV remains an excellent buy up to $55.

Bed, Bath & Beyond Is Finally Looking Cheap

I want to focus on Bed, Bath & Beyond ($BBBY), which had been one of my favorite Buy List stocks, but a string of earnings warnings rocked the shares last year. While 2012 was unpleasant, I think the stock has now fallen back into being a very good buy at this price.

Let’s review what happened last year. In June 2012, Wall Street had been expecting fiscal year earnings (ending February 2013) of $4.63 per share, which represented 14% growth over the year before. But the company surprised investors by telling us to expect earnings growth somewhere between the single digits and the low double digits.

No biggie, right? Guess again. Traders gave BBBY a super-atomic wedgie as the stock got crushed for a 17% loss in one day. Now here’s the odd part: Here we are eight months later, and it looks like BBBY will earn about $4.54 per share for the year, give or take. In other words, that dreaded earnings warning turned out to be about 2% or so.

After the earnings report in September, BBBY got hammered for a 10% one-day loss when it reiterated the exact same full-year forecast. Then, for the December earnings report, BBBY only got nailed for 6.5% after it reiterated, you guessed it, the exact same full-year earnings forecast.

For Q4 (which covers the holidays so it’s the big dog of BBBY’s fiscal year), the company said earnings would range between $1.60 and $1.67 per share. The Street was expecting $1.75 per share. C’mon, this lower guidance isn’t that bad. But traders have lost confidence in BBBY. The shares have plunged from over $75 in June to as low as $55 in December, although it’s come up a bit since then.

Now let’s run some numbers: If Bed, Bath & Beyond can increase earnings by 10% for next fiscal year (which begins in two weeks), that should bring them to roughly $5 per share. That means we’re looking at a stock that’s going for less than 12 times earnings and growing at 10% per year. Furthermore, the recovering housing market should continue to aid them. While BBBY looks cheap, I suspect it will take a while before the stock comes back to life. The earnings warnings really spooked traders. The next earnings call isn’t until April 10. Bed, Bath & Beyond is a good buy up to $60 per share.

That’s all for now. Next week, the stock market will be closed on Monday in honor of George Washington’s birthday. On Tuesday morning, Medtronic ($MDT) will report fiscal Q3 earnings. Last month, MDT bumped up the low end of their fiscal year guidance. We’ll also get the CPI report on Thursday. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

P.S. I recently posted a list of 11 very overpriced stocks that you should sell ASAP.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His {kind=link}