Archive for May, 2013

-

DirecTV Crushes Earnings

Eddy Elfenbein, May 7th, 2013 at 9:58 amExcellent news today for DirecTV ($DTV). The company absolutely demolished its earnings report. For Q1, DTV earned $1.43 per share which was 33 cents better than Wall Street’s forecast. The earnings were higher than all 18 forecasts made by analysts on Wall Street. Revenues rose 7.6% to $7.58 billion which was $50 million better than estimates.

Once again, Latin America was the key to DTV’s success. Subscriber count grew by 583,000 in that region and there are now 16 million subscribers in Latin America. They’re not doing so badly in North America either. DTV added 21,000 subscribers in the U.S.

I’ve often highlighted DTV as a company that does share repurchases right. Last quarter, they bought back $1.38 billion worth of their shares. The stock closed yesterday at $57.96. It’s been as high as $61.50 this morning, which is a 6.1% gain. Right now, it’s hanging in at $60.36, which is a 4.1% gain.

-

Morning News: May 7, 2013

Eddy Elfenbein, May 7th, 2013 at 6:44 amIMF’s Lagarde Urges All Euro Members To Push For Banking Union

China Names Yuan Convertibility Plan as Goal This Year

Senate Passes Online Sales Tax 69-27 But You Can Avoid It For Now

King Coal Losing Crown as U.S. Gains Energy Independence

HSBC Says Quarterly Profit Almost Doubles on Cost-Cutting

Munich Re First-Quarter Profit Jumps Led by Reinsurance Revenue

Facebook Still Worth Probably No More Than $25 A Share: Barron’s

Commerzbank Posts Second Quarterly Loss on Staff Reductions

Baidu Buys PPS Online Video Business to Contend With Youku Tudou

YouTube Is Said to Plan a Subscription Option

Facing Black Market, Pfizer Sells Viagra on Web

DirecTV Spurns Dish’s View That Wireless Is Satellite-TV Savior

Jeweler Agrees To Plead Guilty In KPMG Insider-Trading Case

Edward Harrison: How Bond Market Vigilantes Force Rates Higher

Cullen Roche: What’s Unique About Monetary Realism?

Be sure to follow me on Twitter.

-

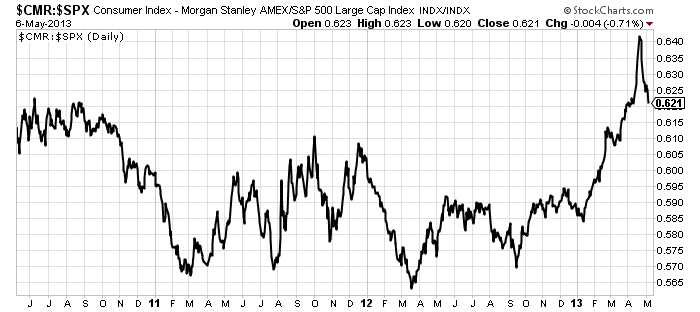

The Strength of Consumer Stocks

Eddy Elfenbein, May 6th, 2013 at 11:24 pmHere’s an interesting chart. This is the Morgan Stanley Consumer Index ($CMR) divided by the S&P 500.

The CMR is heavily defensive although it’s not an exact match for a defensive index. The consumer names have performed very well this year, although since April 19th, their relative performance has suffered a dramatic turn back. It’s unusual, but not unheard of, for defensive stocks to lead a rally. The post-election rally seems to have continued in stride with a quick change in leadership. The change occurred just after the big plunge in gold.

-

Rewarding CEOs for Share Buybacks

Eddy Elfenbein, May 6th, 2013 at 2:45 pmFelix Salmon writes that CEOs should be rewarded for share buybacks. Leaving aside the issue of compensation, I’m not a fan of companies buying back their own shares, although I do admire a few that truly lower their outstanding shares.

I have a few issues here. One is that too many firms use share repurchases to mask their options grants. From what I see, the buybacks routinely go to executives anyway.

Felix writes, “stock buybacks are a very efficient way of returning money to shareholders,” I disagree. In theory, yes, that money goes to shareholders. But the problem is that the volatility of your average stock easily swallows up any gain an investor would see. The daily standard deviation of the Dow, which are blue chip stocks, is 45 times its daily average gain. A generous share repurchase of, say, 4% over the course of a year is a teeny blip in that kind of market action.

Felix writes:

Safeway is faced with a choice right now: it can burn billions of dollars in what would probably be a fruitless attempt to compete with Walmart, or it can return those billions to shareholders, to be reinvested in more promising areas. Safeway’s CEO should choose between those options dispassionately, rather than simply assuming that more investment is always better — and his board should compensate him in such a way that he’s incentivized to make the best decision, rather than always going for growth.

I would say that choice is for the board, with the CEO’s input, and once the strategic decision has been made, the CEO should be in charge of implementation with, of course, a fair degree of latitude.

Felix presents Safeway as having two options. As an investor (though not in Safeway), I have a third: Write me a darn dividend check! After all, who the heck is a board anyway? They work for investors. That profit is mine. Gimme gimme gimme.

Don’t worry about me, I’ll find a use for my own money. I’m pretty good at that, and if I want to buy more stock, that’s my decision, and the same for my fellow shareholders. I only wish our tax system was better aligned to help these investor-friendly decisions.

How absurd is it that Apple, a company with $145 billion in the bank, is borrowing money? It’s a crazy move but math says, do it.

A back-of-the-envelope calculation shows that Apple’s net cost of capital will be roughly just over 1.5 percent per year — pretty cheap long-term money if you can get it. But you can’t. This is a privilege reserved for the largest Silicon Valley powers only.

Apple will have a total outlay of $19.5 billion vs. the $22.95 billion it would have cost the company to bring in the $17 billion from its overseas stash, saving the company more than $3.4 billion.

-

Berkshire Hathaway Breaks $166,000

Eddy Elfenbein, May 6th, 2013 at 10:04 amIt’s a quiet morning so far for our Buy List and the broader market. The S&P 500 is currently up just one point.

Warren Buffett was in the news a lot this weekend as Berkshire Hathaway ($BRKA) held its annual conference. I see that BRKA is currently the top-performer today in the S&P 100. The shares got over $166,000. In 1990, the stock was worth a mere $5,500. When the tech bubble peaked in March 2000, BRKA was worth 30 times the S&P 500. Now it’s up to 103 times the index.

BMC Software ($BMC) has agreed to be sold for $6.6 billion. I’m surprised that the premium is so small. The stock closed Friday at $45.42 and the deal price is $46.25. I think the buyout group, led by Bain Capital and Golden Gate Capital, is getting a decent value. I would have expected this move to have some impact on Oracle ($ORCL) and CA Technology ($CA) but the market doesn’t seem terribly impressed.

Alex Sherman at Bloomberg has an interesting article on the different strategies of Dish Network ($DISH) and DirecTV ($DTV). Dish is moving in the direction of wireless content with their giant purchase of Sprint Nextel, while DTV is sticking with satellite-TV. I’m not a fan of Sprint and I think Dish made its purchase from a position of weakness, not strength.

-

Some Notes on Friday’s Market

Eddy Elfenbein, May 6th, 2013 at 9:30 amI didn’t comment on Friday’s market since the weather was so nice here in D.C. and there are better things to do than watch stock tickers go up and down.

But I want to add a few notes about Friday’s big move. Thanks to the good jobs report, the market closed at yet another all-time high. The Dow broke 15,000 and the S&P broke 1,600. The rally since November has been very impressive.

Cognizant Technologies ($CTSH) was our big winner on Friday. The stock gained 3.5% and has made back much of what it lost. Earnings are due out this week.

Shares of Ford Motor ($F) got up to $13.83 which is the highest since January. Both Microsoft ($MSFT) and AFLAC ($AFL) hit fresh 52-week highs. Nicholas Financial ($NICK) spiked up to $15.13 in the morning before pulling back. Earnings are also due out soon. The only weak spot was Bed Bath & Beyond ($BBBY). The stock was downgraded by Oppenheimer.

-

Morning News: May 6, 2013

Eddy Elfenbein, May 6th, 2013 at 7:45 amFrance Declares Austerity Over as Germany Offers Wiggle Room

E.U. Rules Against Patent Play by Google’s Motorola Unit

Slovenia Falls From Economic Grace, Struggling to Avert a Bailout

Indonesia GDP Growth at Slowest in Over Two Years on Exports

Housing Crash Fades as Defaults Decline to 2007 Levels

Will Verizon Borrow Billions to Become the Biggest?

Bain, Golden Gate near $6.5B deal for BMC

Intel to Buy Finland’s Stonesoft for $389 Million in Cash

GM China April Sales Accelerate as Toyota Extends Decline

Apple Misses IPhone Customers as Global Carriers Balk

Credit Suisse Accuses Goldman Sachs Hire of Secrets Theft

JPMorgan Shareholders Urged to Reject 3 Directors

Occidental’s Chazen Free for Breakup Swan Song as Chairman Out

Joshua Brown: Leon Black is Selling Everything Not Nailed Down

Jeff Miller: Weighing The Week Ahead: New Leadership For Stocks?

Be sure to follow me on Twitter.

-

Dow 15,000

Eddy Elfenbein, May 3rd, 2013 at 10:25 amIt just happened.

The Dow first closed above 150 on October 20, 1925, and above 1,500 on December 11, 1985.

-

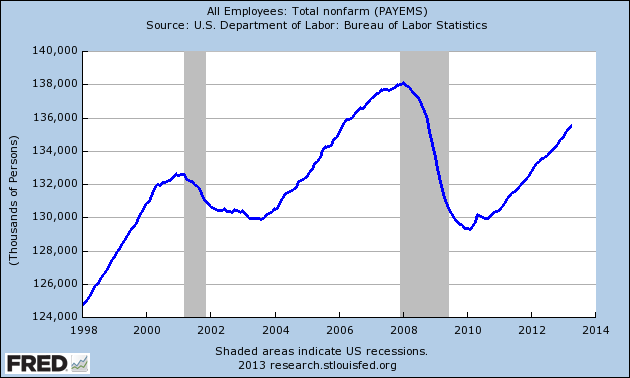

April NFP = 165,000

Eddy Elfenbein, May 3rd, 2013 at 9:25 amThe April jobs report is out and the economy created 165,000 jobs last month. The unemployment rate dropped to 7.5%. But what really caught everyone’s attention were the big revisions to the numbers for February and March. February’s NFP was revised higher from 268,000 to 332,000, and March went from 88,000 to 138,000. That’s a total of 114,000 jobs in revisions. The stock market looks to open higher today.

-

CWS Market Review – May 3, 2013

Eddy Elfenbein, May 3rd, 2013 at 8:31 am“They say you never go broke taking profits. No, you don’t. But neither do

you grow rich taking a four-point profit in a bull market.” – Jesse LivermoreI’m starting to feel a bit sorry for the bears. All the headlines have been in their favor (Debt Ceiling! Fiscal Cliff! Cyprus!), but stock prices don’t seem to be cooperating. On Thursday, the S&P 500 closed at—I hope you’re sitting down—yet another all-time high. April marked the index’s sixth consecutive monthly gain, and we’ve rallied for ten of the last eleven months.

But I have to confess that I’m starting to grow more cautious about this rally. We’ve gone a long way up so we’re probably due for bumps soon. Mind you, I don’t think we’re anywhere close to the danger zone. Instead, I think we’ll see more subdued gains for the rest of the year.

Fortunately, our style of investing doesn’t rely on broad market predictions. Trust me, those “forecasts” are a sucker’s game. Instead, we focus on good stocks going for favorable prices. Just look at our two top-performing stocks this year, Bed Bath & Beyond and Microsoft. Both are excellent examples of how we profited by picking good stocks when the market had soured on them.

In the February 22nd issue of CWS Market Review, I highlighted Microsoft ($MSFT) as an exceptionally good buy. Since then, the software giant has climbed more than 20%, and it just touched a five-year high. This week, I’m raising my Buy Below on MSFT to $35 per share.

In our February 15th issue, I said that Bed Bath & Beyond ($BBBY) was finally looking cheap. The stock has since rallied 18%, and it’s close to cracking $70 per share. This week, I’m raising my Buy Below on BBBY to $72 per share.

The lesson isn’t that every beaten stock eventually goes up. It’s that high-quality stocks that have been beaten down have a very good chance of going back up. Make sure your portfolio has enough of these, and you’re tilting the odds in your favor. That’s the heart of all sound investing.

In this week’s issue of CWS Market Review, I’ll cover our recent Buy List earnings reports and highlight the last batch for next week. Before I get to that, let’s look at how the market has been behaving recently.

The Market’s Leadership Has Changed

The stock market has responded well since its recent low on April 18th. The S&P 500 has rallied for eight of its last 10 days. What’s interesting is that up until the 18th, many of the defensive sectors had been leading the market. By defensive, I mean sectors like healthcare, consumer staples and utilities. That’s rather usual, but not unheard of. Typically, cyclical stocks lead the rallies, and defensive stocks take charge when the market sours (meaning, they fall the least).

So what’s going on? My take is that the recent rout of commodities, gold in particular, helped give the lead to defensive sectors. Energy and Material stocks have been laggards this year. I don’t think we can say yet whether this is a precursor of a broad decline in the economy, but it’s true that some of the recent economic data has been weak. The jobs report for March was lackluster, and last Friday’s GDP was decent but far from strong. But those reports covered periods earlier this year. We’re now well into Q2 and since April 18th, the market has been rallying on strength from cyclical stocks. Technology has been particularly strong.

The Federal Reserve’s policy statement this week specifically said that “fiscal policy is restraining economic growth.” The Fed also said that it may increase or reduce its bond buying to help the economy. I take this to mean that rates will remain very low. As a result, the math continues to be very favorable for stocks. Stocks may be less cheap but they’re still a lot cheaper than bonds. Just look at Apple. The company made news this week with its massive bond offering. Apple was able to issue five-year bonds with a negative real interest rate. Apple’s dividend yield is higher than their cost to borrow, so it wouldn’t make sense not to borrow.

What to do now: Investors should concentrate on high-quality stocks and particularly those that pay generous dividends.

Good News from Harris, Bad News from WEX Inc.

Last Friday, Moog ($MOG-A), the maker of flight control systems, reported first-quarter earnings of 80 cents per share which was two cents better than analysts’ estimates. The CEO said that the first half of this year has been difficult but the second-half should be better for them.

Moog now sees full-year earnings coming in between $3.40 and $3.50 per share but that includes a 15-cent charge for restructuring costs. Not counting the restructuring charge, this is an increase in their guidance. Originally, Moog said they saw full-year earnings ranging between $3.50 and $3.70 per share. Then they took the top end down to $3.60 per share. Now Moog sees earnings, without the charge, between $3.55 and $3.65 per share. This was a good quarter for them. Moog remains a solid buy up to $50 per share.

After the closing bell on Tuesday, Fiserv ($FISV) reported Q1 earnings of $1.33 per share which was one penny below consensus. Due to the earnings miss, the stock got hit for a 4.5% loss on Wednesday. Fiserv has done very well for us, and last week I cautioned you not to chase it. Honestly, I’m not at all worried about Fiserv. A one-penny miss is meaningless for a company like this. In the short-term, of course, it’s not pleasant, but let’s look at the larger picture.

For last year’s Q1, Fiserv made $1.15 per share so earnings are growing quite nicely. Fiserv’s CEO, Jeffery Yabuki, said the company is “on-track to achieve our targeted results for the year.” For the entire year, Fiserv expects adjusted revenue growth in excess of 10%, and earnings-per-share are expected to rise between 15% and 19% to a range of $5.84 to $6.03. The Street had been expecting $5.97 per share. For now, I’m keeping my Buy Below price at $88 per share.

On Tuesday morning, Harris ($HRS) reported fiscal Q3 earnings of $1.12 per share which matched Wall Street’s estimate. I think this was a big relief for traders who were expecting something much worse. The shares got a nice spike after the earnings report.

The most important news was that Harris reiterated its full-year earnings guidance of $4.60 to $4.70 per share. If you recall, the company originally expected earnings between $5.00 and $5.20 per share but lowered guidance due to the federal government’s sequester. Shares of HRS currently yield 3.2%. I’m raising my Buy Below on Harris to $47 per share.

WEX Inc. ($WEX) is turning into our problem child for the year. The stock got hammered this week after the company lowered its full-year guidance. So what’s causing them trouble? The Maine-based company processes fuel payments for fleet vehicles and they’re being impacted by lower fuel costs and unfavorable exchange rates.

First-quarter earnings came in at 98 cents per share which was two cents better than estimates. The results were also better than the range the company gave us three months ago of 89 to 96 cents per share. That’s the good news.

Their guidance, however, was lousy. For Q2, WEX expects earnings to range between 98 cents and $1.05 per share. That’s well below Wall Street’s consensus $1.11 per share. WEX also lowered their full-year guidance from $4.30 to $4.50 per share to $4.20 to $4.35 per share. The stock dropped over 10% on Wednesday. Frankly, the numbers here are pretty ugly. I’m very disappointed with WEX and I’m dropping my Buy Below down to $70 per share.

Four More Earnings Reports Next Week

Next week is the final big week for our Buy List stocks this year earnings season. On Tuesday, May 7th, CA Technologies and DirecTV are due to report. Cognizant Technology Solutions follows on Wednesday, May 8th. Nicholas Financial should also report next week but I don’t know which day.

CA Technologies ($CA) got off to a great start this year but has pretty much stagnated ever since. In January, I predicted the company would beat earnings, and that’s exactly what happened. On the surface, CA appears to be a dull company, but don’t let that fool you. The stock currently yields just over 4%. Wall Street expects earnings of 55 cents per share. I’m holding my Buy Below at $27 per share.

Shares of Cognizant Technology Solutions ($CTSH) recently shed 21% in two weeks. Traders are clearly nervous that a lousy earnings report is coming. For one, Infosys ($INFY), a similar company to CTSH, gave terrible guidance. IBM ($IBM) also had a big earnings miss. Plus, there are also concerns that new legislation will impact the status of foreign workers. But all of this is speculation. The company hasn’t reported yet. Wall Street currently anticipates earnings of 93 cents per share. My analysis says CTSH should beat that. Last week, I lowered my Buy Below to $70 per share.

Three months ago, DirecTV ($DTV) had a monster earnings report. The satellite TV operator crushed earnings by 28 cents per share. The company said they see earnings for this coming in at $5 or more. I’m not a fan of share buybacks, but DTV is a company that truly uses them to lower the amount of outstanding shares instead of a cover for executive compensation. Wall Street expects $1.09 per share for Q1. On Thursday, DTV hit a fresh 52-week high. DTV is a buy up to $59 per share.

There’s still not a single analyst on Wall Street who follows Nicholas Financial ($NICK) so I can’t say what the earnings estimate is. But I can speak for myself. Honestly, I don’t care what NICK’s bottom line is as long as it’s somewhere close to 45 cents per share (excluding any charges). A few pennies per share here or there don’t matter. What does matter is that they’re business continues to deliver steady earnings.

I also expect an update on the buyout offer. It’s been a while so I’ll be curious to hear what they have to say. Unfortunately, if a buyout offer falls through, which is fine by me, the stock will probably take a short-term hit. Nicholas Financial continues to be a good buy up to $15 per share.

Before I go, I want to raise my Buy Below price for AFLAC ($AFL) to $57 per share. The stock has responded well to its last earnings report. The underlying business continues to do well. On Thursday, AFL got over $55 for the first time in two years. Our patience is starting to pay off.

That’s all for now. Next week is the last big week for earnings. We have four Buy List earnings reports coming. Also, on Tuesday, the Federal Reserve will release its report on consumer credit. Then on Thursday, the Commerce Department will report on wholesale trade. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His