Archive for August, 2013

-

Morning News: August 19, 2013

Eddy Elfenbein, August 19th, 2013 at 6:40 amA Summer of Troubles Saps India’s Confidence

Sensex Falls 10% From High as Banks Extend Drop

Thailand GDP Highlights Policy Dilemma

Spanish Banks’ Bad Loan Ratio Rises to Record in June

Key Euribor Rate Steady as ECB Rate Cut Hopes Dim

Biggest Shipping Line Says Emerging Market Warnings Misplaced

Dylan Grice Articulates How Gold Is Money Even Though It’s Not Legally Money

Statoil Funds Growth, OMV Seals Output With $2.65 Billion North Sea Deal

Atlas Copco to Acquire Edwards, Expanding into Process Vacuum Solutions

Regulatory Headaches Worsen for J.P. Morgan

To Cover New York, Zillow Buys a Rival Site

If Bill Ackman Were A Stock, I’d Be Buying Right Now

Trader Joe’s Suing Man Who Resells its Products in Canada

Pragmatic Capitalism: The Case for Dow 20,000 – One Year Later

Jeff Miller: Weighing The Week Ahead: Will Rising Interest Rates Kill The Stock Rally?

Be sure to follow me on Twitter.

-

Israel’s Hi-Tech Boom Is Thanks to Its Military Intelligence

Eddy Elfenbein, August 16th, 2013 at 10:15 pmUnit 8200, Israel’s ‘GCHQ’, has spawned more technology millionaires than many business schools:

Until a decade ago, Unit 8200 was a secret. Then it starred in the book Start-Up Nation, which chronicled Israel’s emergence as a hi-tech powerhouse with more venture capital investment per person than anywhere in the world and the largest number of Nasdaq-listed companies after the US and China. Three years ago, 8200 alumni decided to emerge from the shadows and offer their expertise to other young Israeli entrepreneurs.

The result was the 8200 entrepreneurship and innovation support program (EISP), a five-month hi-tech incubator in which unit alumni volunteer to mentor early-stage startups. So far, 22 of them have received funding totalling $21m (£13.5m) and employ 200 people, joining the 230,000 employees of Israel’s 5,000 tech companies that earn $25bn a year – a quarter of Israel’s total exports.

Nir Lempert, a reserve colonel, former deputy commander of Unit 8200 and chairman of its alumni association, says the unit handpicks the brightest teenagers in the country then trains them to solve problems in multidisciplinary teams using methods usually associated with business, not battles. They are encouraged to think differently. “The central mission of the unit is to save lives, to prevent terror and other attacks,” says Lempert. “We teach our people that the mission is so important that there is no possibility of failure.”

The 8200 legend attracts increasing numbers of young Israelis into IDF tech units. Mamram, the main IT support unit of the IDF, now offers a six-month pre-army course at its headquarters base in a suburban street on the outskirts of Tel Aviv. From dawn into the night, recruits study programming skills, teamwork, project management and – most important – how to be creative. It’s the ultimate startup boot camp.

-

Larry Ellison on Charlie Rose

Eddy Elfenbein, August 16th, 2013 at 7:27 pm -

CWS Market Review – August 16, 2013

Eddy Elfenbein, August 16th, 2013 at 7:14 am“The voice of reason is small, but persistent.” – Sigmund Freud

Youch! Thursday was the worst day for the S&P 500 in nearly two months. By the time the closing bell rang, the index had dropped 1.43% for the day and was back to 1,661.32. Of course, we’re still higher than we were on July 4th. If you take a step back and look at the larger picture, Thursday’s loss was small potatoes. In fact, the most prominent feature of the recent rally is how tame it’s been.

Let’s look at some facts: Morgan Housel notes that 2013 is on track to have the fewest daily swings of 1% or more since 1995. Going by that measure, this year could be the seventh-least-volatile year since 1928.

What’s also interesting is that the stock market rally has been remarkably consistent. The S&P 500 has traded above its 150-day moving average every day for the last eight months. This is the ninth-longest such streak since 1980. In plainer terms, the market has climbed slowly upward almost nonstop since the election. It’s been so placid that this recent break appears more dramatic than the numbers say.

In this issue of CWS Market Review, we’ll take a look at what caused Thursday’s market headache. We’re only five weeks away from the Fed’s September meeting, and more folks on Wall Street think the guardians of the temple will start pulling back on their bond-buying program. We’ll also focus on the upcoming earnings reports from Medtronic ($MDT) and Ross Stores ($ROST). But first, let’s look at why good news for the jobs market is apparently bad news for investors.

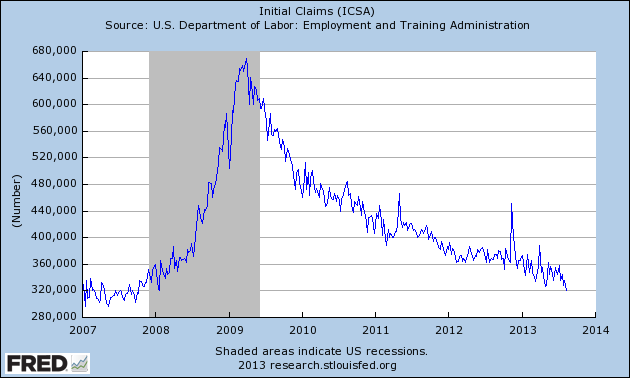

Initial Jobless Claims Lowest Since 2007

I’m always suspicious of any pat explanation for why the market does this or that on a given day. Just because some market activity coincides with some bit of news doesn’t mean the news is the cause. Oftentimes, traders are looking for an excuse to do something, and if some event in the larger world vaguely resembles a reason, they’ll take it.

On Thursday morning, we actually got a piece of very good news. The government reported that initial claims for unemployment had dropped to 320,000. This is significant because that’s the lowest reading since October 2007, which was the top of the market.

Any news about the labor market has to be viewed in the context of the Federal Reserve’s plans for later this year. The Fed has already told us that they’re looking to taper their bond purchases at some point, and that will largely be determined by how strong the jobs market is. So traders probably took the good news about yesterday’s jobless claims as evidence that the Fed will begin paring back on their bond purchases.

I’ve said before that I disagree with the view that the stock market will be stranded without the Fed’s help. The Fed is merely discussing pulling back on the level of support they’re giving investors. No one is pulling the rug out from under the market. As a general rule of thumb, investors place far too much emphasis on what the Fed does (I know, this is a screaming heresy to a lot of folks on Wall Street).

I’m also a doubter that the Fed will make any tapering decision at its September 17-18 meeting. I appear to be in the minority on this point. I should also add that my views on what the Fed will do have been pretty off the mark this year. The good news for us is that forecasting what government eggheads will do isn’t a prerequisite for being a good investor.

This leads to an odd situation where good news on the jobs market leads to bad news for investors, because it signals that the end of QE is within sight. The more dramatic response to any shift in Fed policy hasn’t been in the stock market, but in the bond market. On Thursday, the yield on the 10-year Treasury bond topped 2.8% for the first time in two years. The yield has nearly doubled in the last year. More broadly, last summer may have marked the peak of an astonishing 31-year rally for bonds.

The importance of long-term bond yields is that they usually (though not always) coincide with outperformance of cyclical stocks. They’re called cyclical for a reason, and if the cycle is in their favor, they can do very well. Two summers ago, the bond market gave the stock market a world-class beat down, and the cyclicals got hammered hardest of all.

If there’s any evidence against the Fed making a move next month, we got it with two reports this week. The first was a rather lackluster report on retail sales. This is usually a good clue on how strong consumer spending is. It also tells us how well some of our Buy List stocks, like Bed Bath & Beyond ($BBBY) or Ross Stores ($ROST), are doing.

I was also disappointed by this week’s report on industrial production. This is a key data series watched by the people who decide whether there’s a recession or not. Industrial production has been noticeably flat for the past five months. If there’s going to be a second-half pickup, we should see it soon.

As impressive as the market’s rally has been, a lot of it has been based on earnings growth ramping up later this year. As I’ve said, if that’s the case, the stock market is still quite cheap. But if that thesis doesn’t play out, stocks could take a tumble. The Street’s earnings estimates for Q3 have dropped from $30.27 in March 2012 to $27.17 today. The Q4 estimate is down, but not as much, falling from $31.18 in March 2012 to $29.13 today. Analysts now expect the S&P 500 to earn $108.51 this year, and $122.37 next year. As always, I caution against putting too much faith in estimates beyond a few months out.

What to do now: Our strategy is to be focused on high-quality stocks. Our Buy List has had a very good run since April, so we can expect it to catch its breath. Right now, I think Cognizant Technology Solutions ($CTSH) is a solid value. I also think Oracle ($ORCL) looks good below $33 per share. Please don’t get too worried about what the Fed may or may not do. Good companies can do well in any environment. Now let’s look at our Buy List earnings coming next week.

Medtronic Is a Buy up to $57 per Share

Medtronic ($MDT) is due to report its earnings next Tuesday, August 20th. The Street currently expects 88 cents per share. That sounds about right to me. I was very impressed by MDT’s last earnings report in May. The medical-device company topped consensus by seven cents per share.

The big surprise last quarter was that sales of pacemakers and defibrillators rose. Pretty much everyone was expecting more declines. Sales of defibrillators rose by 1.5%, and pacemakers were up by 2.6%. Company-wide, revenues were up by 3.8%. Medtronic’s CEO said that for the first time in four and a half years, sales of defibrillators and spinal products rose in the U.S. in the same quarter.

For their last fiscal year, which ended in April, Medtronic made $3.75 per share, which is up from $3.46 per share for the year before. In May, the company said it sees FY 2014 earnings ranging between $3.80 and $3.85 per share. Last week, MDT came within two cents of hitting $56 per share. The shares have pulled back with the market’s recent slide, but it’s nothing too severe. Remember that a few weeks ago, Medtronic raised its quarterly dividend for the 36th year in a row. Not many companies can say they’ve done that. Medtronic remains a very good buy up to $57 per share.

Ross Stores Is a Buy Below $70 per Share

Ross Stores ($ROST) is due to report earnings next Thursday, August 22nd. Unfortunately, the discount retailer has gotten punished over the last few days. At the beginning of August, ROST was closing in on $70 and threatening to make a new 52-week high. But some bad news for the retail sector, including disappointing earnings from Walmart and a tepid retail-sales report, brought shares of ROST down to $64.89 by the closing bell on Thursday.

Make no mistake, Ross is a very well-run outfit, and I’m not at all worried about its prospects. In May, the company reported fiscal Q1 earnings of $1.07 per share, which matched forecasts. Quarterly sales rose 8% to 2.54 billion, and same-store sales were up 3%.

Ross said that it sees Q2 earnings coming in between 89 and 93 cents per share. The Street foresees 93 cents per share, which may be a penny or two too high. But bear in mind that this is still a pretty nice increase over the 81 cents Ross earned in last year’s Q2. For the entire year, Ross projects earnings between $3.70 and $3.81 per share. Ross Stores is a very good buy up to $70 per share, and it’s especially good if you can get it below $65.

Nicholas Financial Announces Dividend of 12 Cents per Share

On Tuesday, Nicholas Financial ($NICK) said they’d be paying out another 12-cent quarterly dividend. I thought there was a chance they might increase their dividend. I think we may see a two- or three-cent-per-share increase this December, at the time of their shareholder meeting. Going by Thursday’s close, NICK now yields 3.16%.

That’s all for now. Next week will probably be another quiet week on Wall Street. All the big money guys are chillaxing at their cribs in the Hamptons. On Wednesday, the Fed will release the minutes from their last meeting. This might contain clues to what they have planned for their September meeting. Expect folks to read too much into it. We also have earnings reports from Medtronic and Ross Stores. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: August 16, 2013

Eddy Elfenbein, August 16th, 2013 at 7:08 amEasy Credit Dries Up, Choking Growth in China

Eurobonds at 50 Threatened by EU Transaction Tax

Western Financial Firms Sour on Indian Investments

Mexico’s Energy Reform: A Double-Barreled Problem?

Fed’s Bullard Advocates Caution In Tapering Bond Buying

ETFs Handling the ‘Taper Time’ Pressure

U.S. Retailers Say Uneven Recovery Keeps Consumers Cautious

Dell Results Underscore Challenges Facing Turnaround Plan

Is the Next Sam Walton Running Kroger?

Maersk Upgrades Earnings Forecast on Lower Costs

L’Oreal Proposes to Buy China’s Magic Holdings

Sony and Viacomm Reach Tentative Deal to Stream Cable Channels

The ‘Apple Of China’ Is Clobbering Apple In China–By Using Amazon’s Kindle Strategy

Jeff Carter: Branding Yourself

The Stocktwits ‘FrothMeter’ …A Pause to Refresh… and Howie on CNBC’s ‘Fast Money’ (Again)

Be sure to follow me on Twitter.

-

Worst Day Since June

Eddy Elfenbein, August 15th, 2013 at 10:54 pmThe stock market did not have a good day today. The S&P 500 fell 1.43% and our Buy List lost 2.00%. This was the S&P’s worst day since June 20th. Interestingly, cyclicals fell the least today.

The reason was…good news. Well, it’s hard to say exactly why the market did this or that. But this morning, the government said that initial claims for unemployment insurance fell to the lowest level since October 2007. This means, according to some, that the Fed will start tapering next month.

I’m not sure if I’m fully on board with that train of thought, but it seems to be attracting a lot of attention. If there’s a silver lining it’s that the S&P 500 held just above its 50-day moving average.

-

Morning News: August 15, 2013

Eddy Elfenbein, August 15th, 2013 at 8:51 amRussia Accused of Triggering Trade War with Ukraine

Confident Consumers Step Up Their Borrowing

Gold Investors Seek Alpine Haven in Swiss Army Bunkers

U.S. Stock Futures Drop on Forecasts Before Economic Data

Consumer Prices in U.S. Increase, Supporting Fed Forecast

Jobless Claims in U.S. Decline to Lowest Level Since 2007

Wal-Mart Cuts Profit Forecast as Higher Taxes Damp Sales

Cisco to Cut 4,000 Jobs, Blames Weak Economic Recovery

Soros Raises JC Penney Stake But Two Big Investors Exit in Q2

AMR-US Airways Merger Faced Antitrust Opposition From the Start

Smartphones and Tablets Outsell PCs at Lenovo

Cullen Roche: Failing the Great Recession Test

Joshua Brown: Three Lessons from the Twitter Hedge Fund Ponzi

Be sure to follow me on Twitter.

-

Blast from the Past

Eddy Elfenbein, August 14th, 2013 at 4:31 pmFrom the New York Times, April 30, 1997:

Head of Oracle Halts Bid to Buy Apple Computer

A quest by the chairman and chief executive of the Oracle Corporation, Lawrence J. Ellison, to acquire Apple Computer Inc. came to an abrupt — if temporary — halt late today, when he issued a statement saying that for the moment he had decided not to buy the troubled computer maker.

But in a one-paragraph statement, issued from Mr. Ellison’s Atherton, Calif., home, the billionaire software entrepreneur, raised as many questions as it answered.

While saying that Mr. Ellison had not purchased any Apple stock nor entered into negotiations with Apple executives, the statement added that he might reconsider a takeover at a later date:

”Mr. Ellison stated that he remains interested in developments at Apple and that he may well purchase stock for investment purposes or otherwise, or revisit in the future his decision regarding an acquisition or control of that firm,” the statement said. Mr. Ellison was traveling out of the country and could not be reached for comment today.

Analysts questioned whether Mr. Ellison had ever seriously intended a takeover.

”He played the media like a symphony conductor,” said Tim Bajarin, president of Creative Strategies, a San Jose, Calif., computer industry consulting firm.

Noting Mr. Ellison’s crusade for less-expensive desktop machines called network computers, Mr. Bajarin said, ”He talked about making the Macintosh into a network-computer platform, and that didn’t make any sense.”

There had been talk among industry executives in recent weeks that Mr. Ellison had succeeded in getting commitments for at least $700 million in his bid, but that he had wanted a $1.6 billion war chest.

Other people on Wall Street said that Mr. Ellison had failed to execute a cohesive hostile takeover strategy. Such hostile takeovers are rare in high technology because the assets are frequently the employees, who can leave in the event of a takeover.

Mr. Ellison’s statement was released after the stock market closed. Earlier, shares of Apple closed up 6.25 cents, at $17.6875, in Nasdaq trading.

In March, Mr. Ellison touched off a lively drama in Silicon Valley after he said he was planning to lead an effort to take over Apple and place his friend and the co-founder of Apple, Steven P. Jobs, on the board.

The next day, however, Mr. Jobs denied any knowledge of the plan. Mr. Jobs has returned to Apple as an adviser after selling his company Next Software Inc. to Apple.

The $17.6875 needs to be adjusted for two 2-for-1 stock splits, so at the time, AAPL was going for $4.42 per share.

-

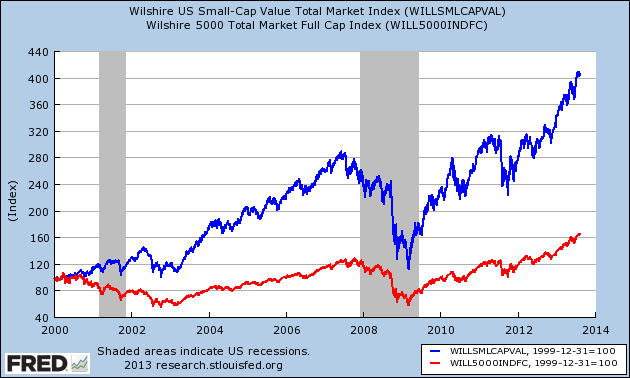

The Surge in Small-Cap Value

Eddy Elfenbein, August 14th, 2013 at 2:48 pmThe stock market didn’t have what experts call “a good” first decade of this century. It’s kind of rough when the stock market falls in half twice within nine years.

However, below the radar, small-cap value stocks have done quite well. They were severely underpriced at the peak of the Tech Bubble in 2000.

This chart shows the total return of the Wilshire 5000 (red line) compared with the total return of the small-cap value sector (blue line). It’s not even close:

This is another reason to be cautious when people discuss “the market” as if it’s one giant entity.

-

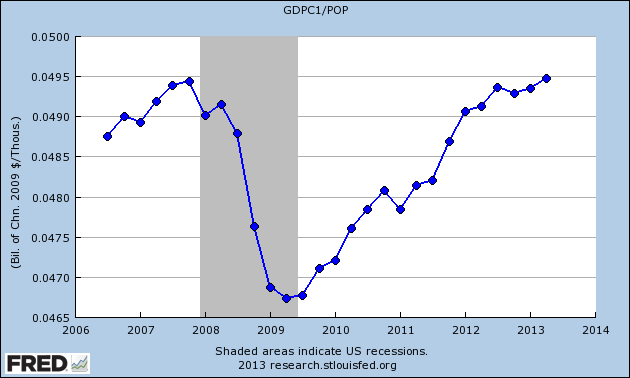

Six Years of No Growth

Eddy Elfenbein, August 14th, 2013 at 11:20 amHere’s an eye-opening chart. From the Fred database, I took the Real GDP (GDPC1) data series and divided it by the U.S. population (POP) to get GDP per capita.

After four years of recovery, we’re only now matching the high from the previous expansion in 2007.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His