Archive for September, 2013

-

CWS Market Review – September 6, 2013

Eddy Elfenbein, September 6th, 2013 at 6:58 am“Sometimes your best investments are the ones you don’t make.” – Donald Trump

The Labor Day weekend is behind us, and the stock market has so far shaken off its August blues. The S&P 500 has rallied for three straight days this week and is back over 1,655. In fact, the index is getting close to breaking above its 50-day moving average. Since August 16th, we’ve closed below the 50-DMA every day but one.

Now all eyes are on the Federal Reserve and what it will do at its next meeting on September 17-18. Make no mistake, this is the most-anticipated FOMC meeting in years. The bigwigs inside the central bank have more than hinted to us that we can expect a paring back in the Fed’s asset-buying program. Of course, no decision has been made yet. Plus, even if there is a tapering announcement, we still don’t know how much it will be. Either way, over the next two weeks, you can expect a lot of opinion-makers opining on what the Fed’s opinion ought to be.

Fortunately for us, we don’t have to fret over such decisions. Our strategy remains the same. We’re focusing on high-quality stocks going for good prices, and it’s working. Despite the August slump, our Buy List holds a nice 4.7% lead over the S&P 500 for the year. By the way, did you notice the nice rebound in Ford ($F)? The automaker just reported its best sales months since 2006.

In this week’s CWS Market Review, we’ll preview the upcoming Fed meeting. I also want to cover the terrible deal Microsoft ($MSFT) just struck with Nokia ($NOK). (I really wish awful dealmakers like Steve Ballmer were in my fantasy football league.) I also want to share with you some names that I’m considering for next year’s Buy List. Plus, I want to touch on the very good ISM reports from this week. But first, let’s look at what Ben Bernanke and his crew at the Fed have in store for the economy, Wall Street and our Buy List.

Countdown to the September FOMC Meeting

The Federal Reserve meets again in two weeks, and this meeting is a biggie. Without making anything definite, Fed officials have used speeches and the media to hint that an announcement of tapering bond purchases is on the table.

Here’s where we stand. Since short-term interest rates are already close to 0%, the Fed has had to use its bond buying as an extra-special tool to help the economy get back on its feet. The Fed has also said that it will stop the bond buying first before it considers raising short-term interest rates. The Fed’s policy is that it won’t raise short-term rates until unemployment falls to 6.5%, which they don’t see happening until the middle of 2015 at the earliest.

So has the bond-buying program worked? That’s hard to say, and to some extent, I don’t care. At the least, we can say that the program has correlated with a recovery in the housing market and a surge in U.S. auto sales. The big winners in the stock market for the last year have been anything at the intersection of consumer finance and large-ticket consumer items. In plainer words, stuff people buy with borrowed money. That’s why the Consumer Discretionary ETF ($XLY) and stocks like Visa ($V) have done so well.

The stock market has been gradually rewarding riskier investments lately at the expense of safer areas. For example, utilities and consumer staples have been rather weak, but industrials have been strong. While financial stocks have been big winners since late 2011, they’ve been underperforming lately. I think this market shift is in anticipation of improved economic growth.

I think it’s a mistake to assume that the entire economy has been aided by steroids from the Fed. More than a few folks on Wall Street think that once the Fed’s assistance is gone, stock prices are due to crash. I disagree. The economy appears to have reached escape velocity, where every improvement builds on what came before. Analysts on Wall Street expect to see earnings growth of over 12% for Q3, and over 25% for Q4. If those forecasts are in the ballpark, the stock market is still cheap.

What’s really shocked people, including myself, is the rout in the bond market. As we look back at the 2013 investing year, May 2nd may turn out to be the key date. That’s when the bond market started to turn south in a big way. Except for very short-term rates which haven’t budged, most Treasury yields are at two-year highs, and they continue to rise. On Thursday, the yield on the ten-year Treasury broke 3% for the first time since July 2011.

Consider that the yield on the five-year jumped from a measly 0.65% in early May to 1.85% by Thursday’s close. Of course, in absolute terms, that’s still a puny yield, but it’s a big turnaround from what we’ve seen. It’s hard to believe that in the spring of 2011, the five-year was inching up over 2.35%.

The rise in yields has been greatest with the seven- and ten-year bonds (more than 130 basis points for each). Interestingly, short-term yields haven’t moved. What’s also caught my eye is that the spread among the longer-dated bonds has actually narrowed a bit. In early May, the 30-year yield was 116 basis points higher than that of the 10-year; now it’s down to 90 basis points. The biggest impact on the yield curve is happening in the middle.

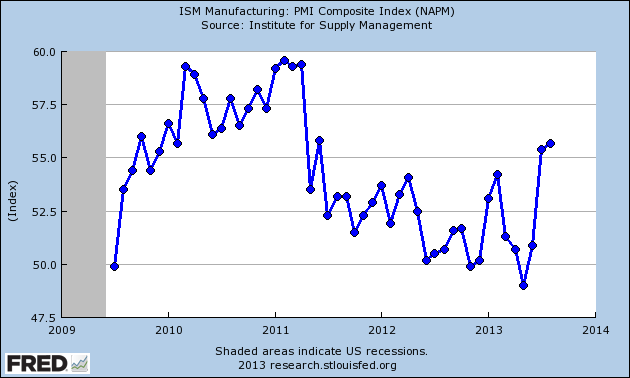

As I explained in last week’s issue, I don’t believe the downturn in the bond market is due to fears of inflation or of the Fed’s shutting off the spigots. Instead, the higher yields are actually in anticipation of an improving economy. We got more evidence of that this week with a very strong ISM report on Tuesday. Then on Thursday, we learned that the ISM Services Index hit its highest level since 2005. We should also add the great sales report from Ford to the positive economic news pile.

So what’s all this mean? It seems that in May, the market saw Fed rate increases as being a long way off. Now it doesn’t. In May, the futures contract for the Fed funds in July 2015 rates got to $99.72. Recently, it’s been as low as $99.13. That’s a big shift.

I suspect that traders are probably getting ahead of themselves in predicting any rate increases. The Fed has said it wants to see unemployment down to 6.5% before it starts raising rates. I’m writing this early on Friday, ahead of the August jobs report, so I don’t know what the results will be (check the blog for updates), but we’re still a long way from 6.5%. The key for investors to understand is that the Fed isn’t going away anytime soon.

We don’t have much hard evidence yet on how the economy has performed during the third quarter. The ISM reports offer some clues, and the August jobs report will shed some light. The ADP report on Thursday showed an increase of 176,000 jobs last month, which nearly hit consensus on the nose.

Investors should continue to favor high-quality stocks. Our own Harris Corp. ($HRS) got off to a shaky start this year, but it has been impressive lately. We recently got a 13.5% dividend increase, and the stock hit a new 52-week high on Thursday. Later this month, three of our Buy List stocks are set to report: Oracle ($ORCL), FactSet ($FDS) and Bed Bath & Beyond ($BBBY). I’ll preview these reports in greater detail in next week’s issue, but the one that’s concerning me is Oracle. The last two reports have been duds, and I’m very reluctant to go against Larry Ellison, but I want to see solid performance in this report. Speaking of large-cap tech stocks, let’s look at the big story from this past week.

Microhard: The Awful $7.2-Billion Deal with Nokia

On Labor Day, Microsoft ($MSFT) announced that it’s buying Nokia’s ($NOK) devices and services unit for $7.2 billion in a deal that includes Nokia’s patents. I think this is another one of Steve Ballmer’s lousy deals, and traders agreed with me. Shares of MSFT dropped more than 4.5% on Tuesday (see chart below), which erased the entire surge from Ballmer’s retirement announcement. The stock has lost more than $18 billion in market value since the $7.2 billion deal was announced.

To quote myself, it’s usually a bad sign when news of your resignation causes a market-value increase of $24 billion. This latest deal shows us why the market so distrusts Ballmer. I’m afraid this is another in a long line of bad deals for Microsoft. Ballmer wasn’t joking around when he said he wants MSFT to be a devices company. You have to wonder how much longer the “soft” will be a part of Microsoft.

The Nokia deal is a deal made from weakness, and that’s usually a bad sign. On one level, it makes sense in that it brings together Windows 8 with its biggest hardware supporter. I suppose they think they can replicate the Google-Apple model. I’m not sure what was going to happen. Perhaps Nokia was going to ditch MSFT and go with Android, or maybe NOK was going to declare bankruptcy. That’s not unthinkable. The stock is still down more than 90% from its tech-bubble high. It’s very probable that Microsoft saw only bad scenarios unfolding and decided to make a move. Most importantly, I’m not sure why MSFT can succeed where Nokia has failed.

Microsoft is still on my Buy List, and will be until the end of the year. I’m very unhappy with this recent decision. The only positive thing I can say is that the Nokia deal isn’t that big relative to MSFT’s overall position. It comes to about 86 cents per share. Microsoft is sitting on a cash position of $61 billion, so this doesn’t exactly stretch their finances.

I added MSFT to the Buy List this year, and I’m not sorry I did. I still think the stock was going for a discount relative to its fair value. I also expect to see Microsoft raise its quarterly dividend later this month. The current dividend is 23 cents per share. I’m expecting an increase to 26 cents. Going by Thursday’s closing price of $31.24, that comes to an annual yield of 3.33%. I’m going to lower my Buy Below price on Microsoft to $34 per share.

Ten Candidates for Next Year’s Buy List

Now that we’re in the final third of 2013, I wanted to pass along a few names that I’m looking at as candidates for next year’s Buy List. As usual, I’ll add five new stocks and delete five current ones.

Please understand, this is just a preliminary list, and I won’t finalize next year’s Buy List until mid-December. There are currently ten stocks that I’m keeping a close eye on; IBM ($IBM), CVS Caremark ($CVS), Tupperware ($TUP), Express Scripts ($ESRX), DaVita ($DVA), Varian Medical Systems ($VAR), AutoZone ($AZO), United Stationers ($USTR), Bio-Reference Labs ($BRLI) and St. Jude Medical ($STJ).

Honestly, that list is heavier on healthcare than I would prefer, but that’s where I’ve been seeing high-quality bargains. I plan to have another list of next year’s candidates before the official list comes out in December.

Before I go, I want to make a few small adjustments to our Buy Below prices. In addition to lowering Microsoft’s ($MSFT) Buy Below to $34 per share, I also want to drop WEX’s ($WEX) down to $89. Nothing’s wrong with the stock. I simply want our buy ranges to reflect last month’s pullback. I also want to raise Ross Stores’s ($ROST) Buy Below by $1 to $71 per share. ROST has been doing very well for us.

Lastly, I’m raising CR Bard’s ($BCR) Buy Below to $119. The company just picked up Rochester Medical for a cool $262 million. Bard is paying $20 per share for Rochester, which is a 44% premium. This looks to be a smart deal, and BCR rallied on the news. Bard looks very good here.

That’s all for now. Next week, we’ll get important reports on retail sales and consumer credit. On Thursday, the Treasury Department will update us on how the budget deficit looks for this fiscal year, which concludes at the end of this month. This looks to be the government’s lowest budget deficit in five years. Of course, that’s comparing apples to trillion-dollar oranges. Still, this year’s deficit is projected to come in at a mere $680 billion. That’s nearly 38% below last year’s red ink. I want to see this trend continue. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: September 6, 2013

Eddy Elfenbein, September 6th, 2013 at 6:41 amPlan at G-20 Is to Tighten Global Rules on Taxes

European Central Bank Chief Tamps Down Optimism

Bogged-Down Banking Fight Leaves EU Vulnerable to Relapse

Cyprus Lawmakers Adopt Key Terms For EU/IMF Bailout

The Next Emerging Market Crisis

Wall Street’s Most Bullish Forecast For Today’s Jobs Report

Behold The Bounty That Shale Oil And Natural Gas Have Wrought

Summers’s Fed Put Beats Bernanke’s for Potency: Cutting Research

Treasury Yields Pierce 3% With Employment Data Ahead

J.P. Morgan to End Student-Loan Business

Yahoo Needs a Lifeboat Not a Logo

Hearsay Social Raises $30 Million to Give Bankers an Online Presence

Hundreds Protest Against Wal-Mart In 15 Cities, Demanding Higher Wages

Jeff Carter: Commitment, Decision Making and Fear In Entrepreneurship

Cullen Roche: 3 Things I Think I Think

Be sure to follow me on Twitter.

-

Even When You’re Right, It Takes Time

Eddy Elfenbein, September 5th, 2013 at 12:17 pmAt one point in 2011, shares of Groupon ($GRPN) got as high as $31. But by late July 2012, the stock had fallen down to $6.90 per share.

That’s when I jumped in and tweeted.

I can't believe I'm saying this but $GRPN really isn't that absurd at this price.

— Eddy Elfenbein (@EddyElfenbein) July 31, 2012

The only problem is that the stock kept falling. By November, it hit $2.60 per share. That’s a 62% drop from what I thought wasn’t a bad price.

Since then, Groupon has rallied is currently close to $11 per share. Even if you think you’ve spotted a good value, you’ll never know when your bargain will materialize. Even if you’re right, the ride can be a lot rougher and longer than you think.

-

Ford’s Joe Hinrichs on Growth

Eddy Elfenbein, September 5th, 2013 at 11:52 amHere’s Ford’s Joe Hinrichs who has my favorite job title — President of the Americas:

-

Morning News: September 5, 2013

Eddy Elfenbein, September 5th, 2013 at 6:20 amKey Euribor Rate Steady As ECB Seen On Hold

BOJ Gov Kuroda: To Take Necessary Steps if Sales Tax Hike Makes Inflation Goal Difficult

Investors Seek Balance Between Central Banks, Syria And Rebounding Economy

Emerging Stocks Rise to Two-Week High as Indian Banks Rally

Salmon: Larry Summers and the Politicization of the Fed

Fed Says ‘Modest to Moderate’ Growth Aided by Homes, Cars

U.S. Car Sales Soar to Pre-Slump Level

Schwab Case Casts Spotlight on Securities Arbitration and Its Flaws

LinkedIn: Endorsed for Financial Acumen

With Chances Dimmer for Sale to Microsoft, BlackBerry May Have To Do The Splits

Samsung Has Hobbled Its Smart Watch Before It Even Launches

P&G to Test Waters Again on a Bargain Tide

How Yahoo Picked a New Look For An 18-Year-Old Brand

Credit Writedowns: Corporate Profits: In the Long Run, Valuation Means Everything

John Hempton: We Interrupt For a Brief Herbalife Update

Be sure to follow me on Twitter.

-

The Limits of Fundamental Analysis

Eddy Elfenbein, September 4th, 2013 at 1:17 pm

With my investment approach, I try to be as rational as is possible. If things had never worked out for Mr. Spock at Star Fleet Academy, he probably would have made a decent money manager. Sure, some work would have been needed on client relations, but you get my point. Still, it’s amazing to me how irrational people can be when they go about investing their money.

Being a rational investor, I rely on a great deal of numbers. But here’s the tricky part: even numbers can be deceiving. I’ve discussed this many times before. For example, your classic P/E Ratio doesn’t always work well with cyclical stocks. In fact, the market’s P/E Ratio is often elevated during the early phases of a bull market.

Also, not all earnings are created equal. When a company borrows money, they’re sacrificing near-term earnings for (hopeful) long-term success. Companies that have high assets relative to their profits tend to report ersatz earnings. Or a company with significant equity exposure in an overvalued stock will have its return-on-equity distorted.

All of these issues can confuse the job of attaching a proper valuation to a stock. I rely on numbers because that’s all I have. If I had prices ten years from now, I’d surely go on those. Because I don’t, I’m left with a bunch of flawed statistics. The hard part is knowing what’s flawed. But even fundamental analysis runs up against its own limitations.

I’d say there’s about 10% of stocks, maybe even just 5%, where fundamental analysis is totally useless. Take Tesla ($TSLA) for example. By any conventional metric, the stock is absurdly overvalued. Unfortunately, I’m not considered a genius for pointing that out. Everyone knows that. The reason is that conventional metrics don’t work on unconventional stocks. If a technology comes along which changes the entire ballgame, all those ratios go out the window.

Consider the case of Amazon.com ($AMZN). At its peak during the tech bubble, the stock was going for a ridiculous valuation. As it turns out, the stock was actually cheap. Since the turn of the century, Amazon has greatly outperformed the S&P 500. AMZN has more than tripled while the S&P 500 has had meager returns. The reason is that Amazon was a new business that changed the marketplace. Valuation didn’t tell you that.

How should someone have valued Eastman Kodak twenty years ago? The stock was a long-recognized stalwart of American business. It was a classic Nifty 50 stock and it paid a good dividend. As late as 2007, shares of EK were over $30. While all seemed calm on the surface, the company was quickly being made obsolete. Today, a share of EK goes for three cents. The dynamics changed and just by following the numbers, you would have been left in the dust.

I live in Washington D.C. and you can see the beautiful canal that runs through Georgetown. Where the canal hits the Potomac is the water’s gate hence the name of the Watergate complex and all the “scandal-gates” that followed.

What impresses me is that the canal was an astounding feat of engineering. It took a lot of men and a lot of money to dig this thing. Yet as soon as the canal was built, it was economically obsolete. The canal was done in by the railroad. The entire effort turned out to be a waste of time and money. This is the process of Creative Destruction identified by the economist Joseph Schumpeter. There’s always some innovation going on somewhere that threatens to upend the entire game, and fundamental analysis won’t see it coming.

-

Morning News: September 4, 2013

Eddy Elfenbein, September 4th, 2013 at 5:32 amGlobal Competitiveness Report: India Slips To 60th Rank, Switzerland On Top

Man Who Saw Japan’s 0.5% 10-Year Yield Now Predicts 0.25%

Spanish Services Post Jobless Growth With First Gain Since 2011

Ryanair Warns on Profit Expectations

S&P Calls U.S. Lawsuit ‘Retaliation’ for U.S. Downgrade

Fracking Boom Seen Raising Household Incomes by $1,200

Microsoft Jettisons Windows Playbook With Nokia Devices

Kodak Moments Just a Memory as Company Exits Bankruptcy

Hedge Funds Load Up on J.C. Penney Shares

Jarden Buying Yankee Candle for $1.75 Billion

LinkedIn Cashing In: Social Network To Raise $1 Billion In Share Offering As Stock Flies High

KitKat Revamped Its Entire Website In A Hilarious Parody Announcing Its New Partnership With Google

H&R Block Declines After Saying Bank Sale Possibly Delayed

Howard Lindzon: CNBC Ratings at New Lows…How? …and Why Can’t Business TV Do What ESPN Does?

Phil Pearlman: Sunk Costs: Microsoft Throws Good Money After Bad

Be sure to follow me on Twitter.

-

The Bad Time of the Year for Stocks

Eddy Elfenbein, September 3rd, 2013 at 11:11 amWe’re nearing the bad time of the year for the stock market. I crunched all the numbers going back to the start of the Dow in 1896, and I found that the index has historically peaked on September 6th. From there, it pulls back an average of 2.51% to October 29th.

Historically, there’s some sluggishness in May, and a drop in early December, but nothing comes close to the September-October slowdown.

As usual, I caution against basing any investment decision on this type of data. I simply think these are interesting trends.

-

Microsoft Buys Nokia Handset Business

Eddy Elfenbein, September 3rd, 2013 at 10:14 amI hope everyone had a nice three-day weekend. The day after Labor Day always feels like a giant “reset” on Wall Street. All the major players are back from their summer retreats. This is also a big week for economic news. This morning, the August ISM was 55.7 which is a very good reading. This is the highest ISM in more than two years.

Thanks to some lessening of the tensions regarding Syria, the stock market is doing well today. The S&P 500 briefly broke 1,650 this morning which is more than 1% higher than Friday’s close.

The big news today is that Microsoft ($MSFT) is buying Nokia’s ($NOK) handset business for $7.2 billion. Many observers think this is the marriage of two companies desperately behind the times. Under Ballmer, Microsoft has wasted billions of dollars on overpriced deals so it’s easy to see this as just one more. Interestingly, the deal also includes NOK’s patents.

Traders are not pleased with the deal. While the rest of the market is rallying, shares of MSFT are currently down more than 4%. Consider that since December 31, 1999, shares of Microsoft are down more than 42% while shares of Nokia are down 91%. The deal is huge for Nokia, but works out to about 86 cents per share for Microsoft. Henry Blodget calls this a smart deal for MSFT but notes that it has a low probability of succeeding.

-

Morning News: September 3, 2013

Eddy Elfenbein, September 3rd, 2013 at 6:16 amOECD Warns Global Growth Could Weaken

ECB’s Draghi Tries To Shepherd Markets Fixated On Fed

RBA Leaves Rates On Hold At 2.5% Amid Fractious Election Campaign

Abe All Ears on Growth Proposals

Phablets a Big Hit With Asian Consumers

Belarus Charges Kerimov in Potash Probe

As Summers’s Odds Rise, Stimulus Easing Is Seen

Microsoft to Buy Nokia’s Devices Unit for $7.2 Billion

Nokia Sale Marks End of an Era

Verizon-Vodafone Talked Merger Before Agreeing to Stake Sale

How Velti, One Of The Largest Mobile Ad Companies On The Planet, Lost $130 Million

Steve Ballmer Tells Employees: ‘Stephen Elop Will Be Coming back to Microsoft’

Roger Nusbaum: Barron’s Interviews Cliff Asness

Joshua Brown: The Number One Threat to the Market

Be sure to follow me on Twitter.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His