Archive for January, 2014

-

Comedians in Cars Getting Coffee: Tina Fey

Eddy Elfenbein, January 31st, 2014 at 8:15 pm -

CR Bard’s Outlook

Eddy Elfenbein, January 31st, 2014 at 10:53 amThis is from CR Bard‘s ($BCR) earnings call:

That all adds up to adjusted cash earnings per share in 2014 between $8.20 and $8.30 per share, excluding any items that affect comparability. The adjustment for amortization is about $0.90 per share after tax in 2014.

For comparative purposes, the adjusted cash EPS number for 2013 was $6.51. So our EPS growth this year is projected to be between 26% and 27%. The sequential ramp between quarters this year will be meaningful as we expect the 2013 acquisitions and the investments we are making to deliver improving profitability as the year develops.

We’re forecasting Q1 2014 with adjusted cash EPS between $1.83 and $1.87 per share compared to the prior year at $1.61. We expect Q1 sales growth to be between 6% and 7%, including the first quarterly royalty payment being received from Gore.

-

CWS Market Review – January 31, 2014

Eddy Elfenbein, January 31st, 2014 at 7:11 am“Go for a business that any idiot can run—because sooner

or later, any idiot probably is going to run it.” – Peter LynchIt seems like the stock market’s had a difficult time making up its mind recently. On Wednesday, the S&P 500 closed at an 11-week low, but Thursday was the index’s best day all year. Overall, the earnings news continues to be good, but that’s largely because expectations were so low.

There are several things weighing on the market’s mind. Late last week, Wall Street was spooked by troubles in the emerging markets (I’ll have more on that in a bit). There are also signs that China’s economy is slowing. On top of that, the Federal Reserve this week decided again to taper its bond purchases by $10 billion next month. The Fed declined to make any changes to its language vis-a-vis raising short-term interest rates. I think we can expect interest rates to remain low for a good deal longer.

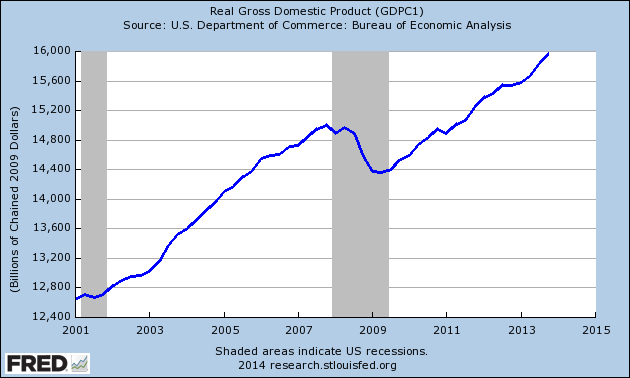

On Thursday, the government said that the U.S. economy grew, in real terms, by 3.2% in the final three months of 2013. Relative to the past few years, that’s not bad. It’s especially good considering that spending by the federal government was down. But in order to see the stock market continue to rally, and see the unemployment rate continue to fall, we still need to see a lot of improvement in GDP growth.

If the economy could grow at an average rate of, say, 3.5% over the next three years, and if inflation could bump up to 2.5%, then our fiscal situation would be vastly improved. I’m not saying it will happen. I’m just saying it would be a great help for investors. Corporate America has stretched profit margins about as far as they can go, so it’s time to see some top-line growth.

The earnings news for our Buy List continues to be good. Both Ford and Qualcomm released impressive results this week, although we had a lousy report from Moog. Some of our stocks are holding up well despite the market’s fragile mood. Express Scripts, for example, just hit a new 52-week high. In this week’s CWS Market Review, I’ll discuss the issues affecting the emerging markets. I’ll also take a look at our recent earnings report and preview next week’s reports. But first, let’s see why the bond and currency markets have been so worried over the “Fragile Five.”

Don’t Blame the Fed for the Emerging-Markets Mess

The stock market’s been rattled lately, and for once, it’s not due to fears from Europe. Instead, there’s been growing concern about the stability of emerging markets, and more specifically, what’s been call the “Fragile Five” (Brazil, India, Indonesia, Turkey and South Africa). Many talking heads are blaming the Federal Reserve for the recent unpleasantness, but this is one case where the Fed isn’t to blame, although it was the instigator of events.

Let’s take a step back. When the financial crisis hit, the Fed and other central banks lowered interest rates to the floor. Econ 101: Money goes to where it’s treated best, so people started investing heavily in emerging markets where the yields (and risks) were higher.

The problem is that a lot of the emerging economies have some serious structural problems. The inflow of cash bought them time, but they haven’t done much to change their ways. Now that the Fed is winding down Quantitative Easing, investors realize that near-0% interest won’t last much longer. Naturally, that will dry up the capital flow to the emerging markets. This problem is compounded by the fact that the governments in the emerging markets loaded up on dollar-dominated U.S. Treasury debt. As a perverse result, they’re doubly sensitive to moves in U.S. interest rates.

People knew this day would eventually come; they just didn’t know when. “When” is apparently now. The governments in the emerging markets are somewhat like a person who builds a balsa-wood house in a tornado zone. When the house goes to smash, they blame the poor foresight on the builder’s part, not the tornado.

The situation in Argentina is especially screwed up—although when I use the phrase “screwed up” in conjunction with our friends on the Rio Plata, it’s like saying there’s “trouble” in the Middle East. The president of Argentina promised not to devalue the currency, but reality intervened. Of course this was after the government spent a pile of cash trying to defend the indefensible peso. In the last three years, Argentina’s currency reserves have been cut in half, and no one really knows what the inflation rate or dollar-peso exchange rate truly is.

I don’t want to pick on Argentina. Turkey is in bad shape as well. The Turkish central bank just jacked up interest rates by 4.75%, and the lira still fell. (Forex traders are an ornery lot.) Brazil doesn’t look so hot, either. The one saving grace for a lot of EMs was their monster customer in China. But when we got sluggish economic reports from China, that really spooked EM investors.

It’s gotten so desperate that even the poor battered yen has done well (see my AFLAC discussion later). I’ll give you another easy rule: If your country exports a lot of commodities (especially to China), then your currency probably got whacked. Places like Turkey, Argentina and Venezuela are running very low on their forex reserves. Broadly speaking, I think currency devaluations can be the best of several bad options, but they don’t work all by themselves. You need reform, too, and that can be politically unpopular.

Several years ago, Bill Gross of PIMCO made a daring investment when he loaded up on Brazilian bonds. That was a shrewd move, and it turned out to be a big winner. So it was a bit jarring when Gross recently said that Brazil is no longer attractive.

I don’t know where all these recent EM developments are headed, but we’re going to soon find out who’s been responsible and who hasn’t. Mexico, for example, will probably pull through just fine. Poland as well. But I’m not so sure about others. Until then, we can expect a little more volatility in our markets and a lot more in the emerging markets. Now let’s run through some of our recent Buy List earnings reports.

Moog Is a Buy up to $66 per Share

Last Friday, we got our first earnings dud of this earnings season. Moog ($MOG-A), the maker of flight control systems, reported fiscal first-quarter earnings of 88 cents per share, which was one penny below estimates.

But the troubling part was that Moog lowered its full-year guidance. The company now sees earnings for this fiscal year (ending in September) of $3.65 per share. That’s down from its earlier range of $3.95 to $4.10 per share. The market was not at all pleased, but remember that guidance is still above the $3.50 per share that Moog made last year.

The lower guidance has three causes. First, Moog plans to spend 15 cents per share more on R&D for its aircraft business. Secondly, they also see their business-system conversion costing 10 cents per share more than originally expected. Finally, Moog projects revenue for this year to fall by 2%, which will knock 10 cents per share off the bottom line.

John Scannell, Moog’s CEO, addressed their slow start: “Our commercial-aircraft business is strong, but our defense and industrial markets are weaker than planned. Despite the difficult market conditions, we continue to invest in programs which will deliver long-term benefits. Although we have revised our fiscal ’14 outlook downward somewhat, it is still a step up from fiscal ’13.”

The shares got banged up last Friday, and the stock continued to drift lower this week. In fact, shares of Moog came very close to dipping below $60 on Thursday. While this news is disappointing, it doesn’t change my fundamental opinion of the company. Moog is a well-run outfit that’s facing a tough environment. We’re in this game for the long-term. I’m lowering my Buy Below to $66 per share.

More Impressive Earnings from Ford Motor

On Tuesday, we got another good earnings report from Ford Motor ($F). For Q4, the automaker earned a cool $3.04 billion, or 31 cents per share, which beat Wall Street’s consensus by three cents per share.

This is a huge year for Ford, as they’re introducing several new vehicles. The basic story remains intact. Ford’s doing a great business in North America, but Europe is struggling, although the Old World is beginning to show signs of improvement. The success story in North America continues to be the F-Series trucks. They’ve been the top-selling vehicle in the U.S. for the last 32 years in a row.

In Europe, Ford lost $1.61 billion last year. They expect more losses this year, but a profit by 2015. Slowly, things are getting better. Ford lost $571 million in Europe last quarter, which is bad, but it’s better than the $732 million they lost in Q4 2012. Also, Ford had a small loss from Latin America and a small profit from Asia, but those are still pretty minor parts of their overall business.

Ford reiterated that profits will fall a bit this year ($8 billion to $7 billion pre-tax), but that’s because the company has very ambitious plans to roll out new models. Ford is introducing 23 new vehicles, of which 16 are in North America. Overall, these were good results. Ford remains a buy up to $17 per share. The stock is especially attractive below $15.30 per share.

Qualcomm Beats Earnings by Eight Cents per Share

After the closing bell on Wednesday, Qualcomm ($QCOM) reported fiscal Q1 earnings of $1.26 per share. That topped Wall Street’s forecast by eight cents per share. Going into this earnings report, a lot of people on Wall Street were expecting weak smartphone sales to hurt earnings. Qualcomm’s shares had dropped four straight days prior to the earnings report.

Fortunately, the earnings report helped calm some nerves, and QCOM rallied 3% on Thursday. I often say that our new buys appear to be damaged merchandise. Investors assume that something is wrong, and in Qualcomm’s case they jump to the conclusion that Apple and Samsung are their only customers. That’s just not so.

The best news is that Qualcomm raised its full-year forecast. For this fiscal year, which ends in September, Qualcomm now sees earnings ranging between $5 and $5.20 per share. The previous range had been $4.95 to $5.15 per share. They also reiterated their full-year-sales range of $26 billion to $27.5 billion, which is an increase of 5% to 11%. The big gains are coming from emerging markets.

For the current quarter, Qualcomm expects earnings to range between $1.15 and $1.25 per share. That’s a bit weaker than expected. Wall Street had been expecting $1.26 per share. Qualcomm sees revenues coming in between $6.1 billion and $6.7 billion. The consensus was for $6.72 billion.

Qualcomm had said they expected a slow start this fiscal year. On the plus side, they were able to improve profit margins in their chips business due to cutting costs. For Qualcomm, their big opportunity is the arrival of LTE in China. However, the Chinese government is currently investigating Qualcomm to see if they’ve broken any anti-monopoly laws. Overall, this was a good quarter for Qualcomm. The company is sitting on $31.6 billion in cash. I’m keeping our Buy Below at $79 per share.

CR Bard Earns $1.42 for Q4

After the closing bell on Thursday, CR Bard ($BCR) reported fourth-quarter earnings of $1.42 per share. That was three cents more than estimates. This is becoming a nice habit for them. You may recall that three months ago, Bard beat earnings by 10 cents per share, and the stock gapped up 7% the next day.

For all of 2013, Bard earned $5.78 per share. Bard’s board also authorized a $500 million buyback program. As usual, I’d rather have that as a dividend, but at least it’s something. The company has increased its dividend every year since 1972, and I think we can expect another increase this spring. I’m keeping my Buy Below on Bard at $142 per share.

Three Buy List Earnings Reports Next Week

Earnings season rolls on. We have three more Buy List earnings reports coming next week.

On Tuesday, AFLAC ($AFL), the supplemental insurance company, is due to report their fourth-quarter earnings. Three months ago, AFLAC told us to expect operating earnings to range between $1.38 and $1.43 per share. They also gave us full-year guidance for 2014, but a lot of that depends on what the Japanese yen does since so much of their business comes from Japan.

If the yen stays between 95 and 100 to the dollar, then AFLAC sees 2014 earnings as ranging between $6.28 and $6.52 per share. The yen is currently about 103 to the dollar. In 2012 and 2013, the yen fell sharply as a result of the government’s weak-yen policy but it’s been creeping up a bit lately. Either way, AFLAC is still going for about 10 times this year’s earnings. AFLAC is an excellent company.

Cognizant Technology Solutions ($CTSH) had a great run during the last half of 2013 (see below), and I think it will continue into 2014. The company will report its fourth quarter results on Wednesday, February 5. For the third quarter, CTSH beat estimates by three cents per share. They also raised their full-year 2013 guidance from $4.32 to $4.37 per share, which translates to Q4 earnings of $1.10 to $1.15 per share. Jefferies raised their price target on CTSH to $112 per share, and Barclay’s raised theirs to $120. For now, our Buy Below is at $104.

Fiserv ($FISV) is also due to report on Wednesday. Wall Street expects earnings of 81 cents per share, which is a nice increase over the 70 cents per share they made one year before. (Remember that FISV split 2 for 1 in December.) The company has been doing very well lately; free cash flow rose 21% for the first nine months of 2013. I think Wall Street’s guidance for 2014 might be a little too high.

Before I go, I also want to lower the Buy Below on our retailers. Bed Bath & Beyond ($BBBY) is a buy up to $71 per share, and Ross Stores ($ROST) is a buy up to $74 per share.

That’s all for now. Next week, we’ll get more Buy List earnings reports. There will also be some important economic reports. The ISM Index comes out on Monday. The ADP jobs report is on Wednesday. On Thursday, we’ll have a look at productivity and trade. Then on Friday is the important January jobs report. The last jobs report was pretty weak, so it will be interesting to see if that was a blip or the beginning of a trend. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: January 31, 2014

Eddy Elfenbein, January 31st, 2014 at 7:05 amFall in Eurozone Inflation Rate Fuels Deflation Concerns

BBVA, Spanish Peers Post 2013 Earnings Recovery

US Downgrades India’s Air Safety Rating to Sub-Saharan Standards

Economy Grew 3.2% in Fourth Quarter, Fueling Hopes for Faster Recovery

A Guide to Obama’s Plan for Retirement Savings

Amazon Looks at Boosting Prime Fee, as Earnings Miss

Exxon Stumblies as Major Oil Producers Try To Find Footing

Honda Q3 Profit Doubles, Sales Get Weak Yen Boost

Zynga Announces NaturalMotion Acquisition Alongside Layoffs

Microsoft Seen Testing Insider Nadella’s Will to Revamp

To Grow, Bitcoin May Need to Shed Its World of Intrigue

For Millions, the Super Bowl Action Will Be on Twitter

Cullen Roche: When the Foundation of Modern Econ Begins to Crumble…

Jeff Miller: When Good Models Go Bad

Be sure to follow me on Twitter.

-

Report: Satya Nadella to Be Microsoft CEO

Eddy Elfenbein, January 30th, 2014 at 7:55 pmReports are coming out that Microsoft ($MSFT) is about to name Satya Nadella as their new CEO:

The board of directors at Microsoft is preparing to tap Satya Nadella as CEO Steve Ballmer’s successor and is holding discussions to replace Chairman Bill Gates, according to a report.

A candidate to replace Gates as chairman, John Thomson, the software giant’s lead independent director, has emerged as well, according to Bloomberg News, citing people briefed on the process.

USA TODAY could not independently confirm the decision. Microsoft did not immediately respond to a request for comment.

As of Thursday night, Microsoft’s board was meeting. An announcement was expected as soon as Friday. Microsoft shares were up 1%, to $37.20, in after-hours trading.

Should Ballmer and Gates depart, the software giant would be without its two most recognizable figures for the first time in its 39-year history.

The report said that Nadella jumped forward as the front runner in recent weeks as Ballmer’s replacement. However, the plans aren’t finalized, according to the report.

Nadella, who joined Microsoft in 1992, is in charge of the company’s enterprise and cloud businesses.

-

Q4 GDP = 3.2%

Eddy Elfenbein, January 30th, 2014 at 8:49 amThe government just reported that the economy expanded by 3.2% in the last three months of 2013. That’s one of the better growth rates in the past few years.

This also breaks a small three-quarter streak of accelerating growth rates. For all of 2013, the economy grew by 1.9%. This was the eighth-straight year that GDP grew by less than 2.8%.

-

Morning News: January 30, 2014

Eddy Elfenbein, January 30th, 2014 at 7:14 amGlobal Markets Slip After Fed’s Decision on Stimulus

Europe’s New Volcker Rule Enrages Everyone Equally

Calm Broken in Markets Amid Concern of Emerging Contagion

Spain Says Post-Recession Recovery Speeds Up End 2013

Lenovo Swallows Motorola: Indigestion Coming?

Google Still Wins by Selling Motorola for Cheap

Facebook Shares Surge On First Ever $1 Billion Mobile Ad Revenue Quarter

Time Warner Cable Reports 2013 Fourth-Quarter and Full-Year Results

Dassault Systèmes and Accelrys to Join Forces

Royal Dutch Shell Halts Alaska Exploration as Profits Fall

BSkyB Revenue Increases as It Signs Up Record TV Customers

Diageo Boss: ‘Emerging Markets Remain Attractive’

Target Says Criminals Attacked With Stolen Vendor Credentials

Roger Nusbaum: Do Portfolio Diversifiers Belong in Client Portfolios?

The Reformed Broker: Games People Play: That 1929 Analogy

Be sure to follow me on Twitter.

-

Qualcomm Earns $1.26 Per Share

Eddy Elfenbein, January 29th, 2014 at 4:05 pmQualcomm ($QCOM) just reported fiscal Q1 (Dec) earnings of $1.26 per share which was eight cents more than the Street was expecting:

Qualcomm Incorporated, a leading developer and innovator of advanced wireless technologies, products and services, today announced results for the first quarter of fiscal 2014 ended December 29, 2013.

“We are pleased with the start to our fiscal year, with record results in quarterly revenues, device sales reported by licensees and MSM chip shipments,” said Dr. Paul E. Jacobs, Chairman and CEO of Qualcomm. “Looking forward, we expect our performance to reflect the continued strong global growth of smartphones, our chipset leadership position and our competitive strengths in 3G/4G technologies and products.”

(…)

Non-GAAP First Quarter Results*

Non-GAAP results exclude the QSI (Qualcomm Strategic Initiatives) segment and certain share-based compensation, acquisition-related items and tax items.

Revenues: $6.62 billion, up 10 percent y-o-y and 2 percent sequentially.

Operating income: $1.85 billion, down 24 percent y-o-y and 5 percent sequentially.

Net income: $2.16 billion, down 2 percent y-o-y and up 19 percent sequentially.

Diluted earnings per share: $1.26, even y-o-y and up 20 percent sequentially.

Effective tax rate: 18 percent.

Detailed reconciliations between results reported in accordance with GAAP and Non-GAAP results are included within this news release.

* The following should be considered in regards to the year-over-year and sequential comparisons:

The first quarter of fiscal 2014 results included:

$665 million gain ($430 million after tax), or $0.25 per share, in discontinued operations associated with the sale of substantially all of the operations of our Omnitracs division; and

$444 million charge ($346 million after tax), or $0.20 per share, that resulted from an impairment charge on certain property, plant and equipment related to our QMT division.

The fourth quarter of fiscal 2013 results included:

$173 million charge (before and after tax), or $0.10 per share, related to the verdict in our litigation with ParkerVision.

First Quarter Key Business Metrics

MSMTM chip shipments: 213 million units, up 17 percent y-o-y and 12 percent sequentially.

September quarter total reported device sales: approximately $61.6 billion, up 16 percent y-o-y and 2 percent sequentially.

September quarter estimated 3G/4G device shipments: approximately 276 to 280 million units, at an estimated average selling price of approximately $219 to $225 per unit.

Cash and Marketable Securities

Our cash, cash equivalents and marketable securities totaled $31.6 billion at the end of the first quarter of fiscal 2014, compared to $28.4 billion a year ago and $29.4 billion at the end of the fourth quarter of fiscal 2013. On January 22, 2014, we announced a cash dividend of $0.35 per share payable on March 26, 2014 to stockholders of record as of the close of business on March 5, 2014.

For fiscal Q2 (ending March), QCOM sees revenues between $6.1 billion and $6.7 billion, and EPS between $1.15 and $1.25. Wall Street had been expecting $1.26 per share.

They kept their full-year revenue guidance the same at $26 billion to $27.5 billion, but they raised their full-year EPS guidance range by five cents; from $4.95 to $5.15, to $5.00 to $5.20. Wall Street had been expecting $5.09 per share.

The shares are up about 2% after hours.

-

Today’s Fed Statement: More Tapering

Eddy Elfenbein, January 29th, 2014 at 2:02 pmInformation received since the Federal Open Market Committee met in December indicates that growth in economic activity picked up in recent quarters. Labor market indicators were mixed but on balance showed further improvement. The unemployment rate declined but remains elevated. Household spending and business fixed investment advanced more quickly in recent months, while the recovery in the housing sector slowed somewhat. Fiscal policy is restraining economic growth, although the extent of restraint is diminishing. Inflation has been running below the Committee’s longer-run objective, but longer-term inflation expectations have remained stable.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that, with appropriate policy accommodation, economic activity will expand at a moderate pace and the unemployment rate will gradually decline toward levels the Committee judges consistent with its dual mandate. The Committee sees the risks to the outlook for the economy and the labor market as having become more nearly balanced. The Committee recognizes that inflation persistently below its 2 percent objective could pose risks to economic performance, and it is monitoring inflation developments carefully for evidence that inflation will move back toward its objective over the medium term.

Taking into account the extent of federal fiscal retrenchment since the inception of its current asset purchase program, the Committee continues to see the improvement in economic activity and labor market conditions over that period as consistent with growing underlying strength in the broader economy. In light of the cumulative progress toward maximum employment and the improvement in the outlook for labor market conditions, the Committee decided to make a further measured reduction in the pace of its asset purchases. Beginning in February, the Committee will add to its holdings of agency mortgage-backed securities at a pace of $30 billion per month rather than $35 billion per month, and will add to its holdings of longer-term Treasury securities at a pace of $35 billion per month rather than $40 billion per month. The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. The Committee’s sizable and still-increasing holdings of longer-term securities should maintain downward pressure on longer-term interest rates, support mortgage markets, and help to make broader financial conditions more accommodative, which in turn should promote a stronger economic recovery and help to ensure that inflation, over time, is at the rate most consistent with the Committee’s dual mandate.

The Committee will closely monitor incoming information on economic and financial developments in coming months and will continue its purchases of Treasury and agency mortgage-backed securities, and employ its other policy tools as appropriate, until the outlook for the labor market has improved substantially in a context of price stability. If incoming information broadly supports the Committee’s expectation of ongoing improvement in labor market conditions and inflation moving back toward its longer-run objective, the Committee will likely reduce the pace of asset purchases in further measured steps at future meetings. However, asset purchases are not on a preset course, and the Committee’s decisions about their pace will remain contingent on the Committee’s outlook for the labor market and inflation as well as its assessment of the likely efficacy and costs of such purchases.

To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that a highly accommodative stance of monetary policy will remain appropriate for a considerable time after the asset purchase program ends and the economic recovery strengthens. The Committee also reaffirmed its expectation that the current exceptionally low target range for the federal funds rate of 0 to 1/4 percent will be appropriate at least as long as the unemployment rate remains above 6-1/2 percent, inflation between one and two years ahead is projected to be no more than a half percentage point above the Committee’s 2 percent longer-run goal, and longer-term inflation expectations continue to be well anchored. In determining how long to maintain a highly accommodative stance of monetary policy, the Committee will also consider other information, including additional measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial developments. The Committee continues to anticipate, based on its assessment of these factors, that it likely will be appropriate to maintain the current target range for the federal funds rate well past the time that the unemployment rate declines below 6-1/2 percent, especially if projected inflation continues to run below the Committee’s 2 percent longer-run goal. When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent.

Voting for the FOMC monetary policy action were: Ben S. Bernanke, Chairman; William C. Dudley, Vice Chairman; Richard W. Fisher; Narayana Kocherlakota; Sandra Pianalto; Charles I. Plosser; Jerome H. Powell; Jeremy C. Stein; Daniel K. Tarullo; and Janet L. Yellen

This is pretty much what I expected. The only minor surprise was that Narayana Kocherlakota didn’t dissent. Binyamin Appelbaum of the NYT tweeted: “Kocherlakota told me he would only dissent if he thought doing so would influence his colleagues. Apparently he decided it wouldn’t.”

-

Triumph Group Bombs

Eddy Elfenbein, January 29th, 2014 at 12:21 pmIn the CWS Market Review from December 27, I listed some of the finalists for this year’s Buy List. One of them was Triumph Group ($TGI), which is a maker of aerospace parts.

I’m glad we didn’t choose Triumph Group because it just bombed earnings. Earnings for Q4 came in 24 cents below expectations ($0.99 versus $1.23). Triumph also lowered this year’s guidance from $5.25 per share to $4.75 per share. The stock has been down as much as 19% today.

Triumph Group is a well-run company and I suspect they’ll come back. This is one to keep an eye on.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His