Archive for February, 2014

-

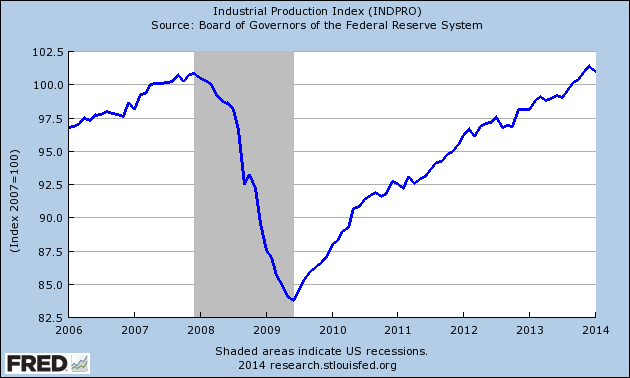

Industrial Production Drops in January

Eddy Elfenbein, February 14th, 2014 at 2:17 pmThe Federal Reserve reported that industrial production dropped 0.3% last month. This was the biggest fall in nearly five years.

The 0.8 percent decrease at manufacturers followed a revised 0.3 percent gain the prior month that was weaker than initially reported, figures from the Federal Reserve showed today in Washington. The median forecast in a Bloomberg survey of economists called for a 0.1 percent advance. Total industrial production dropped 0.3 percent even as utility output climbed the most in almost a year.

Assembly lines slowed last month as colder weather tempered production, the Fed said, showing a pause in the momentum of an industry that’s helped bolster the economy. A pickup in capital spending and faster hiring that drives consumer purchases will be needed to spur production gains.

-

CWS Market Review – February 14, 2014

Eddy Elfenbein, February 14th, 2014 at 7:51 am“If I had asked people what they wanted, they would have said faster horses.”

– Henry FordLast Friday, the government released another disappointing jobs report. The economy created only 113,000 net new jobs last month, and the report for December was even worse: just 75,000 new jobs. In December, we got an advanced warning of the bad news when there was a one-week spike in initial jobless claims.

Strangely, the poor reports calmed some nerves on Wall Street, and stock prices have rallied over the past few days. The Volatility Index, or VIX, in particular, has chilled out in a major way. On Tuesday of this week, the S&P 500 broke above its 50-day moving average for the first time since January 24 (see below).

Let me explain what’s been happening. These jobs reports started a debate on Wall Street about the possibility that the Federal Reserve, now under the leadership of Janet Yellen, might abandon its plans to scale back on its monthly bond purchases. After all, the whole purpose of gobbling bonds by the boatload was to help the labor market.

To add some context, for the 12 months prior to December, the economy had created an average of 200,000 jobs per month, so there’s really been some cooling. What’s the reason for the apparent slowdown? Well, that’s hard to say. It could be a temporary blip. Some analysts are blaming poor weather, but this induces a lot of eye-rolling and snarky laughs from market bears. To be fair, some soggy retail sales numbers seem to confirm the notion that inclement weather did keep consumers at home. Retail sales dropped 0.4% last month. The number for November was revised downward from a 0.2% gain to a 0.1% drop.

Yellen Gives Wall Street the All-Clear Signal

Naturally, the gloomy mood put the spotlight on Janet Yellen. On Tuesday, the new Fed chairman ventured up to Capitol Hill for her debut testimony as Grand Poobah. In accordance with the Humphrey-Hawkins Act, the Fed Chairman tells Congress twice each year what the Fed’s been up to. The prepared remarks are the interesting part, and the Q&A is usually pretty embarrassing. To her credit, Yellen made it clear that the Fed is still on course to buy bonds and doesn’t see evidence yet that greater easing is needed. I think we can infer from this that the Fed’s plan is to taper throughout this year but that any rate increases won’t come until next year, or perhaps later.

Now here’s the good news. Yellen’s most significant remark was her saying that assets are not at “worrisome levels.” Specifically, she said, “Our ability to detect bubbles is not perfect, but looking at a range of traditional valuation measures doesn’t suggest that asset prices broadly speaking are in a bubble territory.” In plain English, this was her Valentine’s Day gift to Wall Street. This is also a good example of how events that are not really unexpected can still markedly boost the confidence of the bulls who have been running scared for the past few weeks.

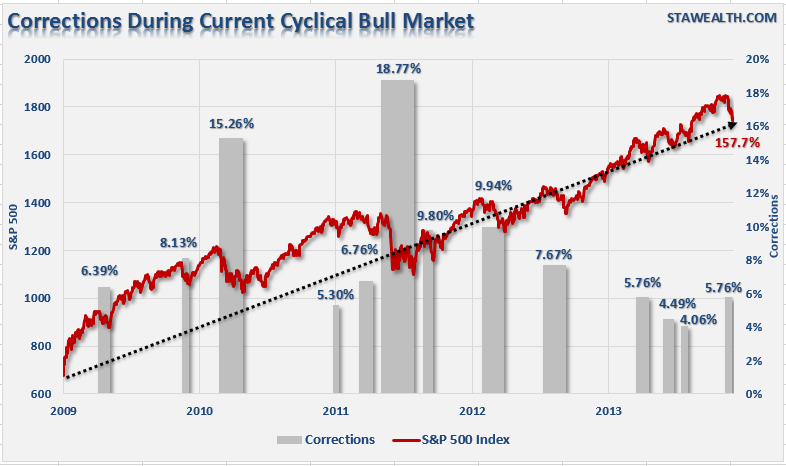

The market’s new optimism has nearly vanquished the late-January slide. From January 15 to February 3, the S&P 500 lost 5.76%. But over the last eight days, the index is up 5.05%. If it weren’t for a minor down day on Wednesday, the S&P 500 would be up for six days in a row. In a four-day stretch, the index gained more than 1% three times. At Thursday’s close, the S&P 500 is almost exactly 1% below its all-time high close from January 15.

Next month, the bull market will celebrate its fifth birthday. The S&P 500 has rallied for an amazing 170% gain. Even though this has been one of the greatest rallies in market history, it’s had several corrections—and a few were quite severe. The latest blip was due to concerns about Emerging Markets and a possible slowdown in China. Traders enjoy worrying about vague threats while ignoring actual good news. While the emerging markets are still a problem, we can now see that not every EM is in such dire straits. We’ve already seen improvements in markets like Italy, Brazil and Australia.

The best news is that earnings continue to churn along. Frankly, I think earnings growth could have been better this season, but there were a lot of folks who expected much worse. Of course, going into earnings season, many companies had pared back their forecasts, so they’ve been beating lowered expectations. According to data from Bloomberg, almost 76% of companies have beaten expectations. Earnings for the S&P 500 are tracking at 8.3% growth for Q4, while sales are on track for a 2.7% increase.

Our Buy List is currently trailing the S&P 500, but not by much. Through Thursday, we’re down 1.37%, while the S&P 500 is off by 1.00%. I’m not happy, but I’m not at all worried. I’m very confident that by the end of the year, we’ll beat the market for the eighth year in a row.

We had more good news on Tuesday when Congress voted to extend the debt ceiling. Please note that I’m not offering an opinion on whether this is a wise move or not, but I will note that the stock market is pleased that we’re not going to have another debt ceiling showdown for at least another year.

We also learned this week that four months into this fiscal year, the federal budget deficit is running 36.6% below last year’s deficit. Compared with last year, revenues are up 8.2%, and spending is down 2.8%. The CBO currently forecasts that this year’s deficit will be a mere $514 billion. Again, I’m not saying that’s ideal, but it’s the lowest deficit in six years. This also helps explain why Treasury bonds continue to do well despite repeated predictions of their demise. Only a few weeks ago, the 10-year Treasury broke above 3%, but it’s already back down to 2.73%. Now let’s take a look at some Buy List earnings coming our way next week.

Earnings from DirecTV, Express Scripts and Medtronic

We’re not quite done with earnings season. Three Buy List stocks are due to report next week: DirecTV, Express Scripts and Medtronic. DTV and ESRX ended their quarter in December, but MDT is our first stock on the January cycle to report. Ross Stores will follow the week after.

Interestingly, DirecTV ($DTV) just got a boost thanks to the mega-deal announced between Comcast and Time Warner Cable. The satellite-TV operator has reported outstanding earnings in recent quarters. In November, they reported earnings 26 cents above estimates. For Q3, DTV added 139,000 subscribers, which doubled expectations. The company is also doing a booming business in Latin America.

DirecTV is scheduled to report earnings on Thursday, February 20. The consensus on Wall Street is for earnings of $1.28 per share, which is too low by my numbers. DTV is on track to earn about $5 per share for 2013, which is a nice increase over the $4.44 from last year. For now, I’m going to keep our Buy Price at $72 per share, which is a bit tight, but I want to see solid results before I’m willing to raise our Buy Below. DTV is a sound stock.

Express Scripts ($ESRX) is one of our new stocks this year, and it’s already doing well for us, with a 9% YTD gain. One of the things I like about ESRX is that its earnings tend to be very stable. The pharmacy benefit manager is due to report fourth-quarter earnings on Friday, February 21.

In October, Express Scripts told us to expect Q4 earnings to range between $1.09 and $1.13 per share. That’s slightly below what I had been expecting, but not enough to change my outlook on the stock. I’ll be very curious to hear any guidance for 2014. The shares are currently above my $74 Buy Below price. Again, I want to see the results before I feel an increase is warranted. As always, I want to caution investors that there’s no need to chase after stocks. Patience, young Skywalker. Our strategy is to wait for good stocks to come to us.

I’ve been waiting more than 13 years for Medtronic ($MDT) to finally break above its all-time high of $62 from December 28, 2000. Well, the stock’s been getting close. Earlier this year, MDT jumped over $60 per share, and I think we may see a new high sometime soon.

Medtronic will report fiscal Q3 earnings on Tuesday, February 18. This is for the quarter that ended in January. The medical-device maker has been doing very well lately, and the CEO noted that they’re outperforming in nearly every business line. I don’t expect much in the way of surprises from MDT. Wall Street expects earnings of 91 cents per share, and that matches my numbers. The company has given us a range for full-year earnings of $3.80 to $3.85 per share. Medtronic remains a solid buy up to $61 per share.

Some Buy List Updates

Several of our Buy List stocks have shown some strength recently. Stocks like Oracle ($ORCL) and CR Bard ($BCR) have rebounded impressively. Qualcomm ($QCOM) just broke out to a 14-year high this week. Shares of Stryker ($SYK) are also at a new high. Feast your eyes on this stat: Over the last 35 years, SYK has crushed the S&P 500 by a score of 100,000% to 1,700%.

Some particularly attractive buys on our Buy List include Ford ($F), AFLAC ($AFL) and Qualcomm ($QCOM). The big loser for us has been Bed Bath & Beyond ($BBBY). The home-furnishing stock has been such an outlier on our Buy List that if its YTD loss were cut in half, it would still be the second-to-worst performer, but our Buy List would be outperforming the S&P 500. I’m not ready just yet to say that it’s a screaming buy, but it’s getting close. BBBY doesn’t report its fiscal Q4 numbers until early April. Until then, it’s a decent buy up to $71 per share.

Ross Stores ($ROST) is another stock that looks cheap, but I want to see numbers first. Ross will report its earnings on February 27. One last stock I like a lot is Cognizant Technology Solutions ($CTSH). The shares pulled back below $90 recently and came within four pennies of hitting $100 on Thursday. CTSH is a very good buy.

That’s all for now. The stock market will be closed on Monday in honor of Presidents’ Day. (Officially, the NYSE calls this Washington’s Birthday, which is celebrated on Presidents’ Day. Don’t ask me why.) On Wednesday, the Federal Reserve will release the minutes from their last meeting. On Thursday, the government will release its inflation report for January. It will be interesting to see if there’s been any upward pressure on consumer prices. We also have three more Buy List earnings reports next week Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: February 14, 2014

Eddy Elfenbein, February 14th, 2014 at 6:45 amFrance and Germany Beat Growth Estimates as Europe Recovers

China Inflation Stays Subdued as Producer Prices Drop: Economy

Italian Economy Registers First Quarterly Growth Since 2011

Portuguese Economy Grew at Faster Pace in Fourth Quarter

Malone Left Seeking Consolation Prize After Second Deal Defeat

Wells Fargo Edges Back Into Subprime as U.S. Mortgage Market Thaws

Jos. A. Bank to Buy Parent of Eddie Bauer in Deal Worth $825 Million

Lenovo Profits and Sales Reach Beyond Expectations

Kraft Expects ‘Soft Start’ to 2014

ThyssenKrupp’s Q1 Profit Buoyed by Brazilian Improvement

Margin Cloud Casts Shadow Over Cisco

California Solar Plant Greeted With Fanfare, Doubts About Future

Investigation into Sands Hack Ongoing

Jeff Carter: Can Bitcoin Lose to An Established Business?

EM Investing: Past GDP Meaningless, Future GDP Invaluable

Be sure to follow me on Twitter.

-

Scotland Can’t Keep the Pound

Eddy Elfenbein, February 13th, 2014 at 11:13 amThe Brits — or I suppose, the English — have told the Scots that if they want to be independent, then they can’t keep the pound as their currency. The Scots are voting later this year on independence, and the currency issue is a big deal.

The nationalists have been saying, if you like your currency, then you can keep it. Apparently not.

The two countries had separate coinage up until the Act of Union merged them into the U.K. Interestingly, the person who oversaw the coinage union was none other than Sir Isaac Newton:

Following the 1707 union between the Kingdom of Scotland and the Kingdom of England, the Scottish silver (but not gold nor copper) coinage was replaced with new silver coins, with the aim of creating a common currency for the new Kingdom of Great Britain as required by the Treaty of Union.[8] The exercise was conducted under the guidance of Sir Isaac Newton, who had previously directed the recoinage in England some years earlier in his role as Warden of the Mint (and subsequently as Master of the Mint).

-

JM Keynes: The Investor

Eddy Elfenbein, February 13th, 2014 at 9:48 amI recently wrote about how investing is a bottom-up activity. I was reminded of that when I read about John Maynard Keynes the investor:

In researching a book on Keynes, I was astounded to find that none of his many biographies contained meaningful detail on his investment activities, although they were fairly well known by the cognoscenti in London and New York during the 1920s and 1930s. What I found was that Keynes stumbled several times before he succeeded — he was almost financially wiped out three separate times — but he got back in the game and altered his thinking to build wealth long term.

Most of what Keynes did in terms of investment innovation has been intricately documented by David Chambers, a professor at the Judge School of Business at Cambridge, and Elroy Dimson, emeritus professor at the London Business School. “Discovering a high degree of overlap with his personal stock portfolio,” Professor Chambers notes, the two researchers took an incisive look at Keynes’s portfolios at the King’s College endowment he managed from 1922 to 1946, when he died.

What emerges from Professor Chambers and Professor Dimson’s research, published in a Journal of Economics Perspectives paper, is a surprising portrait of an investment pioneer who started out as a “top-down” manager relying upon macroeconomic predictions of the economy’s movement and switched to become a “bottom-up” value investor focused on finding solid companies that paid dividends and had promising, long-term prospects.

Keynes vaulted into professional investing with a cocksure insider’s attitude. He had been an adviser to the British Treasury during World War I — until he walked out of the Versailles Treaty talks. Although he maintained and enhanced his Treasury and London financial district connections, he would publicly denounce the Versailles reparations forced upon Germany. Keynes correctly predicted that the treaty would lead to catastrophic economic instability in Germany, which he detailed in his classic “The Economic Consequences of the Peace.”

After the war, Keynes speculated heavily in currencies, but lost most of his capital in 1920 when several European currencies he was betting against recovered. Undaunted, he broadened his portfolio to commodities and eventually common stocks, which at the time was a rarity for institutional investors, who preferred safe bonds and real estate.

Although he was building wealth for his own account and the institutional funds throughout the 1920s, he did not see the 1929 debacle coming and was almost cleaned out again.

The 1929 crash and resulting Great Depression left Keynes intellectually shellshocked, so he changed his strategy. Professor Chambers and Professor Dimson discovered that sometime in the early 1930s he backed away from short-term trades and commodities and focused on stocks. No longer would he pay attention to overarching economic theories or short-term sentiment: The “animal spirits” of the market’s unpredictable pixies could not be trusted. He sensed that security prices were not true indicators of company values.

”Keynes anticipated Eugene Fama, the 2013 Nobel Economics Prize co-winner, in that he clearly did not believe that stock prices must be good indicators of fundamental value,” Professor Chambers said in a recent email. “Consequently, there could be periods when the irrational behavior of investors and what he called animal spirits play a significant role in determining prices on both the upside and downside.”

Unlike millions of modern investors, who latch onto every headline and interview on business television shows to gauge market sentiment, Keynes went about-face in the early to mid-1930s to concentrate on a company’s “enterprise” value, which is also known as “book” or “breakup” value. This intrinsic view of a company’s true worth stripped out the overly emotional component that is often reflected in stock prices. As a result, he often picked companies that had promising futures, but were unloved at the time.

When Keynes adopted his new investment strategy — which paralleled work by Benjamin Graham, a Columbia University professor and mentor to Mr. Buffett — he did quite well. Even with setbacks in 1929-30, 1937-38 and the early years of World War II, Keynes managed a 16 percent annualized return in the Cambridge discretionary portfolio, which mirrored his other holdings. That compares with 10.4 percent for a basket of British stocks over the same period, Professor Chambers and Professor Dimson found.

More important, Keynes staged some striking rebounds after two major declines from 1929 to 1940. According to Professor Chambers and Professor Dimson, although his Cambridge discretionary portfolio lagged the British market by a cumulative 12 percent in 1930 from inception, his performance rallied in the 1930s and ’40s and posted a 0.73 risk/return or Sharpe ratio during his tenure, compared with 0.49 for the British market.

Considering that Keynes was investing during some of the worst years in history, his returns are astounding. How did he do it?

In addition to focusing on bargain-priced small and midsize stocks, Keynes carefully evaluated managements. Could they prosper long term? Did they have a plan for when the economy turned around? “I get more and more convinced that the right method in investment is to put fairly large sums into enterprises which one thinks one knows something about and in the management of which one thoroughly believes,” Keynes wrote in 1934.

Shades of Benjamin Graham and Warren Buffett, and the whole school of value investing. Keynes also loved dividend payers, some of which were paying up to 6 percent during the deflationary 1930s. His portfolios were full of old-line companies in mining, railroads and shipping. Although they were perhaps boring and suspect choices at the time, he bought more shares when they became cheaper and predicted they would be worth more when the general economy recovered.

Ultimately, Keynes was vindicated, building wealth for all of his institutional clients, and he built a personal fortune worth more than $30 million in 2013 dollars at the time of his death, which did not include a tally of his extensive collection of artwork and rare manuscripts. Keynes was not only an investment innovator, but one of the richest economists ever.

While Keynes was most likely the recipient of price-sensitive information during his career, it is hard to discern if he profited from it. Insider trading was not broadly restricted in Britain until 1980. It is also hard to pin down whether Keynes invested along the lines of his famous economic theories, although it is clear that his investment activities informed his view of economics.

Nevertheless, one of Keynes’s most important insights was one that most investors still ignore: A prudent plan does not include timing the market, but focuses on long-term value and total return. It is a view that has not only worked for millions of investors who now invest in index funds — and do not time the market — but is also the foundation of a long-term strategy.

Although Keynes’s economic persona may still be the St. Sebastian of intellectual debate, Keynesian investing has proved to be a solid way to build wealth over time.

-

Morning News: February 13, 2014

Eddy Elfenbein, February 13th, 2014 at 6:46 amBOE’s Dale Says Bets for 2015 Rate Increase Are ‘Reasonable’

Italian Leadership Squabble Weighs as Shares Halt Hot Run

Putin Sochi Bill Seen Rising $7 Billion After Flame Dies

China January Vehicle Sales Up 6%: Industry Group

Conflict in Oil Industry, Awash in Crude

BNP Paribas Net Falls After $1.1 Billion U.S. Legal Charge

Comcast Said to Agree to $44 Billion Time Warner Cable Deal

Lenovo Aims For Third Position in Global Smartphone Market

Nestlé Hurt by Emerging Markets

Cisco’s Third-Quarter Revenue May Miss Some Analysts’ Estimates

Apple Says Suppliers Forgo a Disputed Metal

Renault 2013 Profit Advances 59% on Dacia Brand Gains

Whole Foods Says Competition Cooling Sales, Shares Tumble

Howard Lindzon: Cable and TV are Dead…Give or Take $1 Trillion… and Price is All That Matters

Credit Writedowns: BoE Shatters Quiet Session

Be sure to follow me on Twitter.

-

Comcast Is Buying Time Warner Cable

Eddy Elfenbein, February 12th, 2014 at 10:14 pmThe deal was just announced. Comcast ($CMCSK) is buying Time Warner Cable ($TWC). It’s an all-cash deal and it will be for $159 per share. David Faber is reporting (tweeting) that the ratio will be 2.875.

I’m agnostic on the deal, but it doesn’t seem to be a bad price. I think Comcast had to do something, so this makes sense. However, I’m always a bit skeptical of mega-deals.

Interestingly, check out the trading in TWC today.

Markets are efficient, right?

-

Morning News: February 12, 2014

Eddy Elfenbein, February 12th, 2014 at 6:47 amCarney Renews BOE Low-Rate Pledge to Fight Slack in U.K. Economy

China Strength in Trade Growth Defies Signs of Slowdown

Spot Gold Comes Off A Bit, But Holds Most Of Yellen Gains

How Coca-Cola’s Deal With Green Mountain Shakes Up the Nonalcoholic Beverage Industry

CVS Profit Up After Fourth Quarter Prescription Volume Increases

Marissa Mayer: Yahoo Isn’t Done With Search

Irish company to buy Cadence Pharmaceuticals of San Diego

AOL’s Armstrong Joins Parade of CEOs Apologizing

Everybody Wins When Icahn Gives Up on Apple

SocGen Raises Dividend Payout After Swing to Fourth-Quarter Profit

A World Unprepared, Again, for Rising Interest Rates

U.S. Targets Buyers of China-Bound Luxury Cars

GM Had To Say It: We Didn’t Promote Barra To Pay Her Less

Jeff Carter: The Bitcoin FlashCrash

Cullen Roche: About That 1929 Chart…The Details Matter

Be sure to follow me on Twitter.

-

Thanks, Janet

Eddy Elfenbein, February 11th, 2014 at 4:43 pmOn the heels of Janet Yellen’s Congressional testimony, the S&P 500 rallied for the fourth day in a row — three of those days were more than 1%.

Going by daily closes, the S&P 500 dropped 5.76% from January 15th to February 3rd — and we’ve gained 4.47% in the six trading says since then.

-

Reynolds American Yields 5.55%

Eddy Elfenbein, February 11th, 2014 at 1:56 pmA tobacco stock I like a lot is Reynolds American ($RAI). In fact, it used to be a member of our Buy List. Reynolds is a very good company and I like to check in every so often to see how they’re doing.

Today the company reported Q4 earnings below estimates (77 cents vs 81 cent est.) and the shares are taking a hit. The good news is that Reynolds sees 2014 EPS ranging between $3.30 and $3.45. That’s especially good to get that kind of guidance so early in the year. Wall Street had been expecting $3.44 per share. They earned 3.19 per share for all of 2013.

The other good news is that Reynolds raised their quarterly dividend from 63 cents to 67 cents per share. That comes to $2.68 per share for the year. Notice also how RAI pays out about 80% of their earnings as dividends.

With the lower share price and higher dividends, Reynolds now yields 5.55% which is the equivalent of 890 Dow points.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His {kind=link}

{kind=link}