CWS Market Review – March 14, 2014

“Don’t look for the needle in the haystack. Just buy the haystack!” – John C. Bogle

This was a quiet week on Wall Street up until Thursday when renewed worries over Ukraine sent the S&P 500 down 1.2%. The index is once again in the red for the year, however, our trusty Buy List remains in the black.

Despite the dearth of news this week, things will get a lot more interesting next week when the Federal Reserve meets on Tuesday and Wednesday. This will be Janet Yellen’s first meeting as Fed Chair. This will also be her first post-meeting press conference. But the most important news is that there’s a very good chance the Fed will officially drop the Evans Rule.

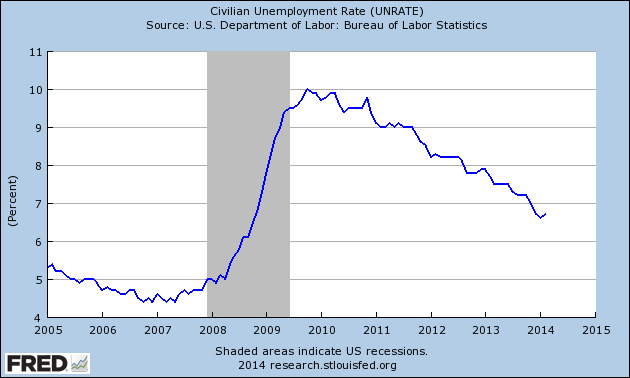

The Evans Rule, named after Chicago Fed President Charles Evans, states that the Fed won’t raise short-term interest rates until the unemployment rate drops below 6.5%. The problem is that the jobless rate is 6.7% at last count and nearly everyone agrees that the economy is nowhere near ready for higher interest rates. The Evans Rule has been in effect since December 2012, and the Fed has been very careful to say that it’s a threshold and not a trigger.

I first talked about the Fed ditching the Evans Rule in CWS Market Review from January 10. I didn’t think it would happen at the time, but I considered the possibility of it happening later this year. Apparently, later is now.

What does the ditching of the Evans Rule mean for us? It’s very good news for investors. I’ll explain more in a bit, but it’s a clear message from the Fed that they’re going to be on the side of investors. Also in this newsletter, I’ll highlight some of the recent news from our Buy List. Plus, I’ll preview next week’s earnings report from Oracle. Larry Ellison’s firm has turned a corner and I expect more good news. I’ll also talk about the recent earnings warning from Bed Bath & Beyond. But first, let’s look at what’s on the Fed’s mind.

It’s Time to Ditch the Evans Rule

In last week’s CWS Market Review, I talked about the debate on Wall Street regarding how much of the soggy economic news was due to the soggy weather. I explained that most of the incoming data confirmed that the cold weather was in fact keeping shoppers at home.

We recently got two more important pieces of evidence that underscored the bad weather hypotheses. Last Friday, shortly after I sent out last week’s newsletter, the Labor Department reported that the economy created 175,000 new jobs in February, which beat expectations. More importantly, it snapped a two-month streak of pretty bad jobs reports. Bear in mind that the jobs report is by far the most important monthly economic report.

The other encouraging news was that retail sales showed its first increase in three months. Retail sales for February rose by 0.3%, which was 0.1% better than expectations. The numbers for December and January were pretty bad. I should add that Thursday’s initial jobless claims report was especially strong; 315,000 Americans filed first-time unemployment claims. That’s the lowest number since November, and the sixth-lowest in six-and-a-half years.

Last Friday’s jobs report showed us that the pre-weather trend of mediocre jobs growth is still in tact. When the bad data came out, some folks started to wonder if the Fed may have started tapering their bond purchases too early. But most Fed officials stuck to their guns and made it clear that unless something really dramatic happened, they were going to continue paring back their monthly bond purchases.

The plan with Quantitative Easing was that the Fed would purchase each month, $85 billion in bonds. That’s $40 billion in mortgage-backed securities and $45 billion in Treasuries. Twice now, the Fed has lowered the monthly number by $10 billion ($5 billion for each group), and they’re almost certainly going to do it again next week.

Is the Labor Market Really Getting Tight?

There are some concerns that the labor market may be getting “tight” right now, meaning there aren’t enough folks out there to fill up the job needs. As a result, wages are starting to rise. I don’t buy this argument. At least not yet. While it’s true that wage growth is starting to creep up, that’s working off a very low base.

The trouble is that the current labor market is in uncharted territory. The workforce participation rate is near its lowest level in more than 35 years. Many folks have simply walked away from the job market. Some of that is due to demographics, most specifically retiring Baby Boomers, but we don’t know exactly how much.

The unsettling aspect of the current jobs market isn’t the high level of unemployed people, but it may be the high level of unemployable people. I hate to sound so negative, but why would the economy rather pay existing employees higher wages than take on new recruits? Like I said, I’m not on board with the tight labor market idea, but the change in workforce participation has been quite startling.

Here’s the bottom line: The Fed will continue to taper. They seem pretty set on that. The Fed wants to get QE out of the way before they start raising interest rates. Right now, most folks expect the first rate increase will come around the middle of next year. The best early warning sign to watch is rising wages. Of course, that’s good news for workers, but at some point that will turn into higher inflation.

We also want to keep an eye on commodity prices which have risen very sharply in the past few months. Coffee prices, for example, have surged dramatically. For now, your local Starbucks can absorb the blow, but at some point, those commodity prices will take a bit out of consumers’ wallets.

The risk/reward ratio is still very much on the side of stocks. Consider that a Buy List stock such as McDonald’s ($MCD) currently yields 3.33%. That’s 68 basis points more than a 10-year Treasury bond. In other words, investors are still vastly over-paying for safety. Until interest rates rise, the math is clearly on the side of stocks. Now let’s look at some of our Buy List stocks.

Oracle Is a Buy Up to $41 per Share

Oracle ($ORCL), the enterprise software king, will report fiscal Q3 earnings next Tuesday, March 18. Three months ago, the company told us to expect Q3 earnings to range between 68 and 72 cents per share. That sounds about right to me. They see revenues rising between 2% and 6%.

I’m pleased to say that reports of Oracle’s demise have been greatly exaggerated. The company is far more “cloudy” than a lot of folks realize. Safra Catz, Oracle’s President and CFO, recently said, “We decided that we were really going to lean in to the cloud to get market share.” That they have.

In December, Oracle reported Q2 earnings of 69 cents per share which was at the top their range. Bookings for Oracle’s cloud enterprise offerings jumped an impressive 35%. The weak spot is new software license subscriptions; revenue there fell by 1%.

I’m in the optimistic camp on Oracle for a few reasons. One is I never go against Larry Ellison. I’ve also been impressed by their headway into the cloud sector. The company has reorganized its sales staff and strategy. I also like how Oracle has been buying back its shares. While I’m not normally a fan of buybacks, Oracle is truly reducing share count and thereby raising EPS.

I’m very curious to see what guidance Oracle offers for Q4, which ends in May. The Street expects 96 cents per share which may be a bit too high. I’ll warn you that the bears love to pounce on ORCL. Either way, Oracle continues to be a very good buy up to $41 per share.

Bed Bath & Beyond Shakes Off the Bad Weather Blues

After the closing bell last Friday, Bed Bath & Beyond ($BBBY) released a statement saying that the lousy weather had zapped six or seven cents per share off their fiscal Q4 earnings. Their fourth quarter ended on March 1, and the earnings report will come out on April 9.

Let’s look at some math. The home furnishings store now says it sees Q4 coming in between $1.57 and $1.61 per share. The previous guidance has been for $1.60 to $1.67 per share. If you recall, the stock gotten beaten up in January when they lowered their initial guidance of $1.70 to $1.77 per share.

Here’s what’s interesting: I was almost convinced that the market was going to punish the shares at Monday’s open. Didn’t happen. Instead, BBBY was one of the top performers on our Buy List. It looks like the bad-weather message finally got through to traders.

The company said that during Q4, a store had to be closed for the entire day due to the bad weather 464 times. On top of that, there were 1,923 partial closings. Obviously people can’t shop at closed stores. There may be good news for BBBY in the future. Williams Sonoma, a close competitor, just reported earnings above expectations thanks to new home construction. That could be a lift for the industry. In fact, the entire retail sector has snapped back recently. For now, Bed Bath & Beyond remains a good buy up to $71 per share.

More Buy List Updates

I wanted to add a few quick notes on some of our other Buy List stocks. Cognizant Technology Solutions ($CTSH) split 2-for-1 on Monday. The stock has been weak lately after Infosys, a competitor, gave poor guidance. For the most part, CTSH has been executing much better than Infosys so I don’t know if this is such a bad omen. CTSH is a solid buy up to $56 per share.

The Icahn Vs. eBay ($EBAY) battle got even louder, if you can imagine that. This week, eBay (are you sitting down?) rejected both of Carl Icahn’s nominees for eBay’s board. eBay said they’re unqualified and urged shareholders to vote against them. This feud is getting tiresome. eBay has made it clear that they’re not going to sell PayPal. Carl, if you’re reading this, move on. eBay continues to be a good buy up to $62 per share.

McDonald’s ($MCD) has made an embarrassing amount of errors recently. That’s why the stock has lagged, and partly why I like it. At BusinessWeek, Vanessa Wong takes a look at how MickeyD’s is working to right the ship. McDonald’s is a good buy up to $102 per share.

That’s all for now. In addition to next week’s Fed meeting, the government will release the industrial production report for February on Monday. Then on Tuesday, we’ll get reports on inflation and housing starts. It will be interesting to see if any of the rise in commodities shows up in consumer prices. I suspect that it’s too early. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on March 14th, 2014 at 7:53 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His