Archive for March, 2014

-

What Causes Value and Momentum?

Eddy Elfenbein, March 12th, 2014 at 8:33 amTwo of the curious anomalies in finance are the value and momentum effects. Simply put, the momentum effect means that the best-performing stocks have a tendency to keep on rallying and outpace the market. The value effect, by contrast, means that stocks with low valuations often outperform the rest of the market.

What’s odd is that these two effects seem to run counter to each other. The hottest stocks, one would think, would almost always have to be richly valued. Yet there is clearly a disconnect between price and performance. How can this be?

In the Financial Times, John Authers talks with Paul Woolley, a former fund manager, who thinks he’s threaded the needle. But first, a few nitpicking points. Authers writes:

Markets are not perfectly efficient. More or less everyone agrees to this in the wake of the financial crisis. And while asset bubbles have recurred from time to time throughout history, bubble production has accelerated sharply.

So not only are markets inefficient, but they are more inefficient than they used to be. This is despite rapid technological improvement to make markets faster and more liquid. So why are markets inefficient, and what can be done about it?

I certainly agree that markets aren’t perfectly efficient. Heck, my website is dedicated to the idea that patient investors can beat the market. But I disagree that bubbles have “accelerated sharply.” True bubbles are fairly rare. The tech bubble and the housing bubble were very real, but just because prices fall doesn’t mean that every downtrend is a bubble. I would argue that, market-wide, stocks weren’t excessively valued in 2007. Maybe prices were a little high, but nothing crazy. Furthermore, I don’t see how the supposed proliferation of bubbles means that the market is less efficient. I suspect that the market is actually becoming more efficient, but that’s in a very general sense.

Back to Mr. Woolley. Authers writes:

His intuition is as follows. Funds holding an asset suffer poor returns. This leads to outflows, which force them to sell that asset, creating momentum. It will also lead to “comovement.” As assets flow out of a fund, so all the assets it holds will tend to drop in price. This can extend effects across whole sectors. Eventually, this creates the cheapness that subsequently allows the value effect to prosper.

For an example, look at “value” funds during the tech bubble of the late 1990s. In absolute terms, they kept rising. In relative terms, they performed terribly compared to the booming tech sector, and a great deal of money was pulled from them. This caused value’s underperformance to deepen and also ensured that the value effect, once the inevitable reversal occurred, would be particularly strong.

After much mathematics, the momentum effect proves overwhelming for a matter of some years. And momentum, divorced from the real-world fundamentals, leads eventually to bubbles and mispricings.

As I understand this, he’s saying that the value effect eventually becomes the momentum effect. Honestly, that doesn’t seem right, but I concede that it could be so. My hunch is that value and momentum are separate. I think value is mean reversion writ large, while momentum is simple greed.

-

Morning News: March 12, 2014

Eddy Elfenbein, March 12th, 2014 at 7:21 amETF Outflows Biggest in World on Economy

Losing Crimea Could Sink Ukraine’s Offshore Oil and Gas Hopes

Europe Makes a Stink About American Cheese Names

Obama Will Seek Broad Expansion of Overtime Pay

U.S. Senate Wind-Down Bill Clips Fannie Mae, Freddie Mac Shares

U.S. is Said to Probe GM Recall

Airline Industry Profit Forecast Is Cut on Ukraine Crisis

Mt Gox Gets US Bankruptcy Protection

Citi Upgrades J.C. Penney, Says It’s a Comeback Story

Jos. A. Wearhouse Is Almost a Reality

Prudential Says Asia Helps it Boost 2013 Profits

Is a PayPal Split Best For eBay?

‘Candy Crush’ Maker King Prices IPO at as Much as $24 a Share

Credit Writedowns: Russia: Economic Vulnerabilities

Roger Nusbaum: IPOs: Hot Again

Be sure to follow me on Twitter.

-

What Should Investors Expect?

Eddy Elfenbein, March 11th, 2014 at 4:10 pmIn the Wall Street Journal, Brett Arends writes about a subject close to my heart: what can investors expect from the stock market.

The problem is we can only go on past information. Most long-term studies begin the 1920s, and they show that the stock market has returned about 7% per year, once we include dividends and inflation.

The problem with that is it covers what Henry Luce called the “American Century,” when our way of life of democratic capitalism spread all over the world. I don’t think that’s repeatable. I’m still optimistic for America, mind you, but I don’t think we’ll see quite the triumph of free minds and free markets that we saw in the 20th century.

The great bull market from 1942 to 1966 was astonishing. I don’t think many investors realize this. It’s not really discussed because, I suppose, the market never truly crashed again. We have to remember how poorly valued stocks were for many years. The real yield for stocks was often much higher than inflation. Arends writes:

For example, from the 1920s through the early 1990s stock investors collected an average annual return of 4% just from their dividends. Today the figure is less than 2%. Logically we should expect future total returns to be at least two percentage points lower.

I disagree that lower dividend yields will translate to lower returns. Even putting aside buybacks (which I don’t like), the payout ratio is far lower than it used to be. Companies used to shell out a large percentage of their profits as dividends. Nowadays, it’s far less.

Back in the 1950s, U.S. stocks traded at an average of about 11 times the previous year’s earnings, according to analysts. In the 1940s and the early 1980s, valuations fell as low as eight times earnings.

But after 1982 they became sharply revalued upward. Today the S&P 500 trades at about 18 times earnings. To expect the same again is to engage in Bubble Logic—the belief that things will keep going up simply because they have.

Again, my view is slightly different. The valuations of the 1940s and 1950s were, indeed, very low. But I believe the valuation revolution of the 1960s is still in place. The problem is that low inflation brought earnings multiples back down again in the 1970s, and that appeared to be mean reversion. I don’t believe it’s reasonable to assume that we’ll revert to single-digit multiples, unless there’s high inflation.

Strip out these one-off gains and inflation, Rob Arnott recently suggested, and investors ought more realistically to expect about 1.5% a year plus dividends—meaning, in the current environment, an annual return of about 3.5% in real terms. That’s a far cry from 10%.

I think that’s slightly pessimistic. I would say that investors should expect real returns of 5% from common stocks. That’s 2.5% from capital gains and 2.5% from dividends.

-

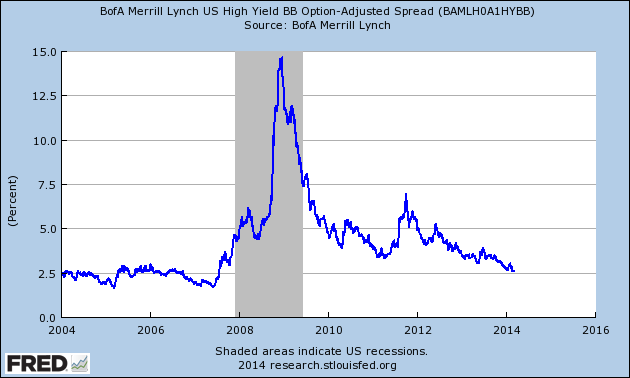

Lowest Spreads in Six Years

Eddy Elfenbein, March 11th, 2014 at 11:54 amIn a recent CWS Market Review, I discussed the market’s growing appetite for risk. We can see this effect by looking at the narrowing yield spread between risky bonds and secure bonds. Before, I looked at CCC bonds, but here’s the spread between BB bonds and Treasury bonds. Double B bonds are among the lowest-rated investment grade bonds.

It recently dipped below 2.6% which it hasn’t done since July 2007.

-

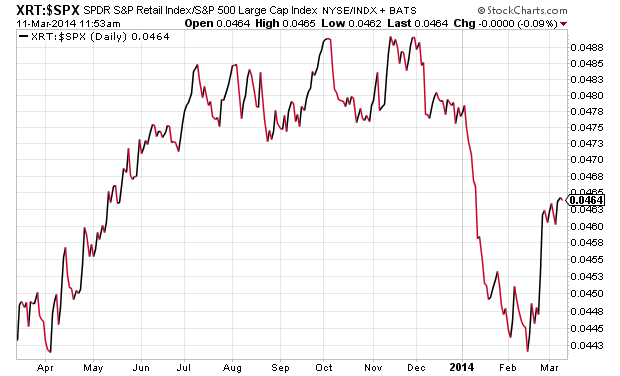

Retail Rebound

Eddy Elfenbein, March 11th, 2014 at 11:49 amHere’s the best way to see the weather’s effect on the stock market. This is the relative strength of the retail sector. After a terrible start to this year, retail is finally showing some strength.

-

Four Million Job Openings

Eddy Elfenbein, March 11th, 2014 at 11:34 amThe stock market is quiet again today. There’s not really much economic news this week. The JOLTS report, which is Job Openings and Labor Turnover, today said there were four million job openings in the economy. That’s actually the number for January, there’s a little lag in the JOLTS report.

The S&P 500 has been as high as 1,882.35 this morning, which is a little over one point from Friday’s intra-day high. We have a good shot of reaching another closing high today.

I was surprised to see Bed Bath & Beyond ($BBBY) behave so well yesterday despite Friday’s profit warning. Perhaps the market is finally looking past the weather-related events. McDonald’s ($MCD) is particularly strong today. The company reported some sluggish sales numbers, but the CFO made some optimistic comments at an investment conference. It’s simply a cheap stock. The eBay/Icahn spat continues. eBay ($EBAY) said they’ve rejected his board nominees. I’m sure we’ll hear more on this.

Qualcomm ($QCOM) got to a new high today of $77.20. Express Scripts ($ESRX) is also on the new high board today. ESRX is getting very close to $80 per share.

-

Morning News: March 11, 2014

Eddy Elfenbein, March 11th, 2014 at 5:10 amChina Suggests Full Interest Rate Liberalisation in Two Years

China to Pilot Five Private Banks

Bank of Japan Sticks to Easing Plan as Sales-Tax Bump Looms

Three Years After Fukushima, Japan Still Struggles to Cope

Manpower Employment Outlook Survey Points to Confidence Around the World

Virtu Filing Shines Light on Business of High-Frequency Trading

Colorado’s First Month of Recreational Pot Tax Yields $2 Million

Despite Rough Winter, Airlines See Strong Profits

Regulators, GM Under Fire After Deaths

Sbarro Files Second Bankruptcy as Mall Traffic Dwindles

EBay Rejects Icahn’s Board Nominees

McDonald’s Stock Not on Value Menu Amid Weak Sales

On the Herbalife Fight, Natural-Gas Plays

Cullen Roche: “Keynesian” Myths and Misunderstandings

Jeff Carter: Everyone is a Node on a Network

Be sure to follow me on Twitter.

-

Josh on the Easy Money Myth

Eddy Elfenbein, March 10th, 2014 at 9:31 pmJosh Brown destroys the myth that this has been an easy market:

It’s been one of the hardest environments in market history. Never before have investors’ wounds been so raw. Never before have there been so many voices polluting the popular consciousness with half-baked conspiracy theories and calls for collapse. Never have there been such a dizzying array of investment vehicle options to confuse and confound. Never have the perceived risks been quite as ferocious.

In the last five years, investors have dealt with a non-functioning congress, a downgrade of the US Treasury, mass unemployment, exploding deficits, record debt, a possible dissolution of Europe and a slow-motion crash in China and the emerging markets – and that’s before we even get into any specifics. And not only have the threats been unprecedented, the amplification of them – thanks to the desperation of the mainstream media for attention coupled with the advent of a whole new chattering class on social media – has been like an orchestra of clanging pots and pans, car alarms and doberman barks, shrieks and howls, thunder and lightning. Every step of the way some motherf*cker’s been screaming about something about to crash, the calamity waiting around the corner, the next shoe to drop.

Read the whole thing.

-

Cognizant Technology Split 2-for-1

Eddy Elfenbein, March 10th, 2014 at 10:21 amThis morning, shares of Cognizant Technology Solutions ($CTSH) split 2-for-1. The new buy is $56 per share.

For track record purposes, I assume our Buy List is a $1 million portfolio that’s equally weighted among our 20 stocks at the start of the year.

As such, the CTSH position was 495.1476 shares bought at $100.98. The split changes that to 990.2952 shares bought at $50.49 per share.

I always want to go out of my way to make sure our Buy List is as transparent as possible.

-

Morning News: March 10, 2014

Eddy Elfenbein, March 10th, 2014 at 7:05 amCarney Faces Leadership Test as Currency Scandal Snares BOE

China’s CSI 300 Index Plunges to Five-Year Low on Export Slump

Crude Oil Sheds Gains After Weak Chinese Data

China passenger vehicle market rose 18% in February

EC to Delay Russian South Stream Gas Pipeline Talks

Spot Gold Extends Losses and Seen Vulnerable if Ukraine Situation Improves

Tencent-JD.com Partnership Goes Straight For Alibaba’s Throat

Japan Display Prices IPO at Bottom of Range

United Rentals to Acquire National Pump

Comcast Challenging Disney’s Hold on Tourism Trade

Alleged Bitcoin Millionaire Nakamoto Gets $28,000 Donations

Hackers Allege Mt. Gox CEO Still Controls ‘Stolen’ Bitcoin

Joshua Brown: US Healthcare Spending by the Numbers (spoiler alert: it’s not working)

Jeff Miller: Weighing The Week Ahead: What Is The Risk And Reward For Stocks?

Be sure to follow me on Twitter.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His