Archive for June, 2014

-

CWS Market Review – June 20, 2014

Eddy Elfenbein, June 20th, 2014 at 7:06 am“In this game, the market has to keep pitching, but you don’t have to swing. You can stand there with the bat on your shoulder for six months until you get a fat pitch.” – Warren Buffett

The news got a lot more interesting this week. First, Medtronic ($MDT) announced a mega-merger deal with Ireland’s Covidien. The shares celebrated by jumping to an all-time high. MDT is a 13% winner on the year for us.

Also this week, the Federal Reserve decided on another taper, their fifth in a row. Investors liked what they saw, and the S&P 500 has now rallied for five days in a row. That’s our longest winning streak since April. The index just notched its 21st record high this year. The Nasdaq touched a 14-year high (see below), and the Volatility Index plunged to an 88-month low.

In this issue of CWS Market Review, I’ll walk you through the Medtronic-Covidien deal. Frankly, it’s not ideal, but I recognize that Medtronic had to make a move, and it’s probably the best deal they could get. I’ll also take a look at the recent earnings report from Oracle, and we’ll preview next week’s earnings report from Bed Bath & Beyond. BBBY has gotten beaten down this year, and I think it’s going for a very good price here. I’ll also discuss the Fed’s latest taper move and why the economy is finally looking better (no, really). But first, let’s take a closer look at the $42.9-billion deal Medtronic did with Covidien.

Medtronic Buys Covidien for $42.9 Billion

Two weeks ago, I told you that Medtronic ($MDT) was seriously considering a merger with Smith & Nephew ($SNN). This past weekend, however, the company announced that it’s buying Ireland’s Covidien ($COV) for $42.9 billion. In 2007, Covidien was spun off from Tyco International ($TYC).

What makes this deal interesting is that it’s an “inversion,” which means that Medtronic’s HQ will move from Minneapolis to Ireland, where corporate taxes are much lower. Americans are often surprised to learn that our corporate tax rate is higher than many European countries’ rates. The main corporate rate in Ireland is 12.5%, compared with 35% in the U.S. I think we can expect to see more of these inversion deals in the future. In Medtronic’s case, the tax savings won’t be that dramatic since they already have a modest tax bill thanks to R&D tax breaks.

The deal calls for Medtronic to pay $93.22 per share for Covidien ($35.19 in cash and 0.956 shares of MDT). That was a 29% premium to Covidien’s share price. As an interesting footnote, to qualify as an inversion, the deal has to be at least 20% in stock. With acquisitions, the rule of thumb is that the acquirer’s stock falls. Not this time. Shares of Medtronic initially stumbled, but then a rash of upgrades caused traders to push MDT as high as $65.50 per share on Thursday. That’s an all-time high.

Is this a good deal for Medtronic? It’s complicated. I’m not a fan of mega-mergers. Small rollups are fine, but trying to merge two large enterprises is often more difficult than the planners realize. Having said that, I realize that Medtronic had to make a move. All medical device companies need to. After all, their customers (hospitals and physician groups) have been merging for the last few years, and the device makers are facing those same economic pressures. You can be sure that many of these upcoming deals will be inversions, so expect to hear more talk about Stryker ($SYK) and Britain’s Smith & Nephew.

Ironically, by setting up in Ireland, Medtronic will be able to free up more cash, which they can reinvest in the United States. Medtronic said they plan to invest $10 billion in the U.S. over the next ten years. A lot of these inversions will be between companies that make strange bedfellows, but Medtronic and Covidien are a natural fit. For all the options Medtronic faced, this was the best deal for them to make, so I cautiously support this deal.

As if there’s not enough Medtronic news this week, the company also announced an 8.9% increase to its dividend. I love me a good dividend increase. The quarterly dividend will rise from 28 cents per share to 30.5 cents per share. For the year, that’s $1.22 per share. This is the 37th year in a row that Medtronic has increased its dividend. Going by Thursday’s close, Medtronic yields 1.9%. This week, I’m raising my Buy Below on Medtronic to $67 per share.

The Fed Tapers Again

The Federal Reserve held a two-day meeting this week, and as everyone expected, the central bank tapered its bond purchases again. Starting in July, the Fed will purchase $20 billion in Treasuries each month, plus $15 billion per month in mortgage-backed securities. This is the fifth-straight meeting in which the Fed has tapered.

Tapering by $10 billion at each meeting ($5 billion in Treasuries and $5 billion in MBS) has been the Fed’s game plan all year, and they’ve stuck to it, even when the economy got polar-vortexed earlier this year. In their post-meeting statement, the Fed said that the economy is slowly improving, although housing remains weak.

The Fed has four more meetings left this year. So if we assume they stay on course, they’ll be done with Quantitative Easing (QE) by the end of the year. (I’m assuming the final $5 billion in Treasuries will be tapered in December, but there could be a clear-the-decks move in October.) Janet Yellen has said to expect a rate increase about six months after the end of QE.

As part of this Fed meeting, they also updated their economic projections. You can see them here. Let me caution you that the Fed isn’t exactly known for its accuracy, but it’s interesting to see what its assumptions are. Here’s where it gets interesting. Check out Figure 2 on the PDF. The broad consensus is that the first rate hike will come next year. Twelve of the 16 members agree on that, and I think they’re right. But the consensus falls apart for year-end 2015. There’s a small clustering around 1% to 1.25%, which means that real rates are projected to be negative for at least another 18 months. As long as the lid stays on inflation, that’s very good for the stock market and our Buy List. One of the basic rules about finance is that the stock market loves cheap money.

This week’s inflation report shows that inflation continues to trend upward. Of course, we’re still far from it being a problem, but the rate of inflation is no longer falling. That’s key. The Bureau of Labor Statistics reported on Tuesday that core inflation rose at its fastest rate since October 2009, which is still quite modest. Only now is inflation finally moving into the Fed’s target area.

The Fed’s consensus for year-end 2016 is even more scattered. Their range for short-term interest rates goes from 0.5% to 4.25%, and there are never more than two members that agree on any one rate. I don’t expect a consensus, but I’m shocked to see so little agreement on where the economy will be in 30 months. In short, they see rates going up, but there’s no agreement on how high.

I should point out that two Fed regional surveys this week were quite optimistic. The Philly Fed Manufacturing Survey noticed a big increase in activity this month. Also, the Empire State survey showed that activity in New York is quite good. On Monday, the Fed reported that Industrial Production rose a healthy 0.6% last month. For the first time in a long time, we can say that things are looking up for the economy. Expect to see the economy average over 3% annualized growth for the next few quarters. After five years, the recovery is beginning to be felt on Main Street.

Oracle Misses Earnings by Three Cents per Share

After the closing bell on Thursday, Oracle ($ORCL) reported fiscal Q4 earnings of 92 cents per share. Frankly, that’s disappointing; it’s three cents below Wall Street’s consensus. Oracle said they lost two cents per share due to the currency loss in Venezuela. Shares of ORCL, which had rallied to a 14-year high during the day on Thursday, got smacked around for a 6% loss in the after-hours market.

Three months ago, Oracle said to expect Q4 earnings to range between 92 and 99 cents per share. As it turns out, they hit the low end of their guidance, and business was pretty sluggish in Q4. Quarterly revenue rose 3.4% to $11.32 billion, which was $160 million below expectations.

One of the keys for Oracle‘s business is sales of new software licenses. For Q4, that came in at $3.77 billion, which is flat. Their hardware revenue, now finally growing, rose only 2% to $1.5 billion. One bright spot is that Oracle’s cloud revenue jumped 23% to $327 million. There have also been rumors that Oracle is considering buying Micros Systems ($MCRS) for $5 billion, which would be their largest deal since they bought Sun Microsystems four years ago. Micros makes software for hotels, restaurants and retailers.

Now for guidance. On the earnings call, Oracle said they see Q1 earnings ranging between 62 and 66 cents per share. That’s not so bad. Wall Street had been expecting 64 cents per share. Oracle sees quarterly revenue growth between 4% and 6%. Breaking that down, they expect new software-license revenue to be up by 6% to 8%. Hardware will be between -1% and 3%, but cloud revenue is expected to be up by 25% to 35%. If this guidance is accurate, that tells us that last quarter’s weakness won’t last. Oracle remains a good buy up to $44 per share.

Stay Tuned for Bed Bath & Beyond’s Earnings Report

Our biggest dud this year, by far, has been Bed Bath & Beyond ($BBBY). The stock is off more than 24% YTD. Last week, the shares traded below $60 for the first time in 15 months.

I apologize for the rough ride with this one, but make no mistake, I haven’t given up on BBBY. In the CWS Market Review from May 9, I announced that I was ready to pound the tables for BBBY. This coming Wednesday, June 25, is our first big test. That’s when BBBY will report their fiscal Q1 earnings.

Let’s review where we stand. Three months ago, Bed Bath & Beyond reported terrible results for Q4 (December, January, February). The home-furnishings store earned $1.60 per share. That was eight cents lower than the year before. That was quite a shock, because BBBY delivered earnings increases like clockwork. They estimated that poor weather knocked six to seven cents off their bottom line.

For their Q1 outlook, BBBY had more bad news. They said to expect earnings to range between 92 and 97 cents per share. The consensus on Wall Street had been for $1.03 per share. They made $4.79 all of last year, and for this fiscal year, they expect earnings to rise by “mid-single digits.” If we take that to mean 4% to 6%, their guidance works out to a range of $4.98 to $5.08 per share. Wall Street had been expecting $5.27 per share.

Now let’s look at the items in BBBY’s favor. First is the low share price. The stock is going for about 12 times forward earnings. If we look at one of my favorite valuation metrics, Enterprise Value/EBITDA, BBBY’s is down to 6.15, which is quite low. The company also has a very clean balance sheet: no debt and lots of cash. Let’s remember that the store is well managed, and they’ve ridden through storms such as this before. As the Fed indicated this week, the housing market is still weak, but that won’t last, and stronger housing helps BBBY. You need to be patient with this one, but Bed Bath & Beyond remains a very good buy up to $66 per share.

That’s all for now. Next week is the last full week of Q2. On Wednesday, the government will revise its Q1 report for the second time. The initial report showed growth of 0.1%, but last month it was revised down to -1%. I’m curious to see what happens this time. Also on Wednesday, we’ll get a key report on orders for durable goods. On Thursday, we’ll get the report on personal income. Also on Wednesday, we’ll get the earnings report from Bed Bath & Beyond. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: June 20, 2014

Eddy Elfenbein, June 20th, 2014 at 6:55 amInternational Monetary Fund Says Europe Should Weigh Bond-Buying

What Will Argentina Do With Its Vultures?

Treasury Inflation Linked Auction Tail Dims Sale for Dealers

The Social Security Administration’s Diminishing Footprint

Shire Rejects AbbVie’s $46.5 Billion Takeover Bid

Siemens-Mitsubishi Raise Alstom Offer as End-Game Nears

Oracle Earnings, Revenue Miss Estimates; Shares Plunge

BlackBerry Results Top Forecasts, Fueling Recovery Hopes

Strong TSB Debut Lifts Prospects for Future Share Sales

I.P.O. Values Euronext Exchange Operator at $1.9 Billion

Latvian Rating Raised by Fitch on Positive Debt Dynamics

BofA Must Face U.S. Suit Over Mortgage-Securities Fraud

Ousted American Apparel CEO Undone by Controversial Past

Cullen Roche: 5 Investment Lessons We Can Learn From Futbol (Err, Soccer)

Joshua Brown: “Hedge Funds Set the Price of Stocks”

Be sure to follow me on Twitter.

-

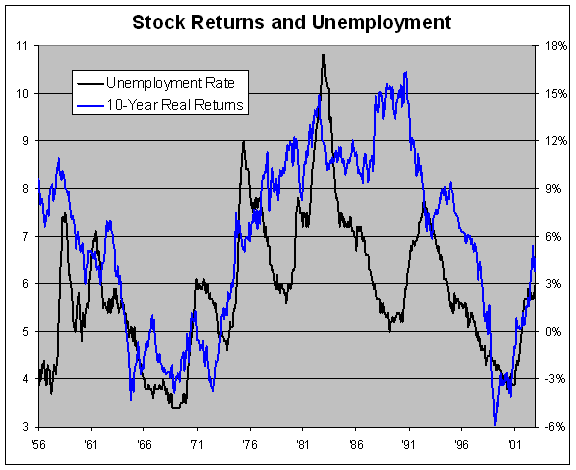

Unemployment and Future Stock Returns

Eddy Elfenbein, June 19th, 2014 at 11:29 am“Be greedy when others are fearful” is one the old adages of investing, and the numbers appear to back that up, at least going by the unemployment rate. I went through the historical data and took the current employment rate going back to 1956 (black line, left scale) and compared with the future 10-year real returns of the stock market (blue line, right scale). So that includes both dividends and inflation.

The lines seem to line up fairly well. Let me caution you that it’s dangerous to read too much into charts like this. Instead, investors should understand the broad lesson that it’s usually a good time to invest when the economy is flat on its back. Conversely, when the economy is roaring along, that’s often a sign of trouble for stocks. In fact, one of the better estimates of the real cost of equity capital just might be the current employment rate.

(You can sign up for my free newsletter here.)

-

Morning News: June 19, 2014

Eddy Elfenbein, June 19th, 2014 at 6:44 amChina Shares Post Biggest Loss Since Late April as IPOs Divert Funds

Japan Business Mood Defies Economic Headwinds, Backs BOJ Optimism

Argentina Says Next Bond Payment ‘Impossible’, Default Looms

Beware the Hype Over the Shale Boom

Post FOMC: What Strategists Read in Yellen’s Words

Currency Probe Widens as U.S. Said to Target Markups

Wheat Extends Gains as Rain Threatens to Thwart U.S. Harvest

Siemens Joins Mitsubishi to Pledge Guarantees for Alstom

Adobe Brings Lightroom To iPhone, Adds Photoshop Tablet App

FedEx Delivers A 33% Dividend Increase And Stronger Than Expected Earnings

Rolls Royce to Return 1 Billion Pounds to Investors, Shares Jump

Why Elon Musk Is Doubling Down on Solar Power

Are The Two Most Notorious Men in Fashion Finally Getting Their Comeuppance?

Jeff Carter: Defending the For Profit Exchange

Be sure to follow me on Twitter.

-

The Stock Market’s Reaction

Eddy Elfenbein, June 18th, 2014 at 2:55 pmThe stock market seems mildly pleased with today’s Fed statement:

-

The Fed’s Economic Projections

Eddy Elfenbein, June 18th, 2014 at 2:34 pmHere are the updated economic projections from today’s FOMC meeting.

The bottom line is that the Fed sees the economy and labor market improving. Most Fed members think that the first rate increase will come next year. The blue dots for interest rate projections are very widely dispersed for 2016. In other words, there’s little consensus on what will happen beyond 18 months out.

-

Today’s Fed Statement

Eddy Elfenbein, June 18th, 2014 at 2:04 pmMore tapering. Starting in July, the Fed will buy $20 billion in Treasuries and $15 billion in MBS. Here’s today’s Fed statement:

Information received since the Federal Open Market Committee met in April indicates that growth in economic activity has rebounded in recent months. Labor market indicators generally showed further improvement. The unemployment rate, though lower, remains elevated. Household spending appears to be rising moderately and business fixed investment resumed its advance, while the recovery in the housing sector remained slow. Fiscal policy is restraining economic growth, although the extent of restraint is diminishing. Inflation has been running below the Committee’s longer-run objective, but longer-term inflation expectations have remained stable.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that, with appropriate policy accommodation, economic activity will expand at a moderate pace and labor market conditions will continue to improve gradually, moving toward those the Committee judges consistent with its dual mandate. The Committee sees the risks to the outlook for the economy and the labor market as nearly balanced. The Committee recognizes that inflation persistently below its 2 percent objective could pose risks to economic performance, and it is monitoring inflation developments carefully for evidence that inflation will move back toward its objective over the medium term.

The Committee currently judges that there is sufficient underlying strength in the broader economy to support ongoing improvement in labor market conditions. In light of the cumulative progress toward maximum employment and the improvement in the outlook for labor market conditions since the inception of the current asset purchase program, the Committee decided to make a further measured reduction in the pace of its asset purchases. Beginning in July, the Committee will add to its holdings of agency mortgage-backed securities at a pace of $15 billion per month rather than $20 billion per month, and will add to its holdings of longer-term Treasury securities at a pace of $20 billion per month rather than $25 billion per month. The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. The Committee’s sizable and still-increasing holdings of longer-term securities should maintain downward pressure on longer-term interest rates, support mortgage markets, and help to make broader financial conditions more accommodative, which in turn should promote a stronger economic recovery and help to ensure that inflation, over time, is at the rate most consistent with the Committee’s dual mandate.

The Committee will closely monitor incoming information on economic and financial developments in coming months and will continue its purchases of Treasury and agency mortgage-backed securities, and employ its other policy tools as appropriate, until the outlook for the labor market has improved substantially in a context of price stability. If incoming information broadly supports the Committee’s expectation of ongoing improvement in labor market conditions and inflation moving back toward its longer-run objective, the Committee will likely reduce the pace of asset purchases in further measured steps at future meetings. However, asset purchases are not on a preset course, and the Committee’s decisions about their pace will remain contingent on the Committee’s outlook for the labor market and inflation as well as its assessment of the likely efficacy and costs of such purchases.

To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that a highly accommodative stance of monetary policy remains appropriate. In determining how long to maintain the current 0 to 1/4 percent target range for the federal funds rate, the Committee will assess progress–both realized and expected–toward its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial developments. The Committee continues to anticipate, based on its assessment of these factors, that it likely will be appropriate to maintain the current target range for the federal funds rate for a considerable time after the asset purchase program ends, especially if projected inflation continues to run below the Committee’s 2 percent longer-run goal, and provided that longer-term inflation expectations remain well anchored.

When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent. The Committee currently anticipates that, even after employment and inflation are near mandate-consistent levels, economic conditions may, for some time, warrant keeping the target federal funds rate below levels the Committee views as normal in the longer run.

Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; Stanley Fischer; Richard W. Fisher; Narayana Kocherlakota; Loretta J. Mester; Charles I. Plosser; Jerome H. Powell; and Daniel K. Tarullo.

I need to add that there’s no excuse for an FOMC statement to ramble on this long. It should be short and to the point.

-

Morning News: June 18, 2014

Eddy Elfenbein, June 18th, 2014 at 6:33 amNew EU Resolution Rules Mark Progress in Removing Support

Gilts Advance as BOE Minutes Damp Bets of Imminent Rate Increase

BOJ to Provide Almost 5 Trillion Yen to Banks to Boost Lending

Japan’s Parliament Begins Debate on Introducing Casinos

China’s Shipping Alliance Rejection Underscores Protectionist Worries

Grand Central: Why The market Doubts Fed Rate Dot Plot

Consumer Price Index Jumps 0.4% in May as Inflation Heats Up

French Government Rejects Siemens-Mitsubishi Bid for Alstom

Elon Musk Seeks to Hasten Shift to Solar By Building Factory

Why Buying Micros Would Be a Bad Deal for Oracle

Popeyes Buys Its Recipes for $43 Million. Wait, Popeyes Didn’t Own Its Recipes?

What’s Up With This Green Coca-Cola?

Adobe’s Cloud Solutions Fuel Strong Financial Results

Roger Nusbaum: Nothing New Under the Sun

Joshua Brown: “the essence of shadow banking is giving people a liquid claim on illiquid assets.”

Be sure to follow me on Twitter.

-

Benzinga’s PreMarket Prep

Eddy Elfenbein, June 17th, 2014 at 12:06 pmYesterday, I was on Benzinga’s PreMarket Prep show. I think my audio was a bit low, which isn’t what I’m like in real life. Thanks to everyone at Benzinga for inviting me!

-

Inflation Continues to Rise

Eddy Elfenbein, June 17th, 2014 at 11:32 amThe government reported that inflation rose again last month. Consumer prices edged up 0.4% in May which was the largest increase in more than a year. The “core rate,” which excludes food and energy, rose by 0.3% which was the largest increase since 2009.

I want to be careful not to overstate the case. No, there’s no danger of hyperinflation. Rather, the trend of disinflation, lower price increases, seems to have come to an end. In the last year, headline inflation is up 2.1% and core inflation is up 2.0%. Overall, I think this is a good thing as inflation moves closer to the Fed’s target zone.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His