Archive for August, 2014

-

CWS Market Review – August 29, 2014

Eddy Elfenbein, August 29th, 2014 at 7:08 am“The market can do anything.” – Jesse Livermore

It finally happened! Shortly after the opening bell on Monday morning, the S&P 500 broke 2,000 for the first time in history. Of course, breaking through some arbitrary number doesn’t mean anything for the stock market’s future, but it’s a good time to reflect on how amazing this rally has been. To give you some perspective on what 2,000 means, consider that each point in the index is worth about $8.8 billion.

Less than three years ago, the S&P 500 stood at 1,100. We’re now closing in on double that number. Measuring from the big low in March 2009, the index has tripled in a little less than five and a half years. Add in dividends and we’re up more than 230%! That’s more than 24%, annualized. It took just 94 days to go from 1,900 to 2,000. The index got as high as 2,005 on Tuesday before settling back to 1,996.74 by the close of trading on Thursday.

Without question, this has been one of the greatest bull markets in history. It’s also been one of the most hated. From the day it started, people have predicted its imminent demise. Of course, the current bull market came about after a long and painful bear market. But this shouldn’t be too surprising since bull markets have a habit of starting with a low. Even adjusting for inflation, the S&P 500 is still below its high from March 2000. That’s why I always keep in mind the wise words of Mr. Livermore: “the market can do anything.” Not only can it…it probably has.

In this week’s CWS Market Review, we’re going to take a look at some of the recent economic news. Slowly, things are improving. This week, the government revised higher its estimate of Q2 GDP growth. Next Friday is the big jobs report for August, and we could extend our streak of adding 200,000-plus jobs to seven months in a row. Let’s hope these good numbers continue.

Of course, hope is not an investment strategy. Around here, we focus on cold, hard facts. The good news is that our Buy List has been rallying with the overall market. Fiserv just hit a new all-time high. Ross Stores continues to float higher after its strong earnings report; the shares just broke out to a nine-month high. Microsoft is nearing a 14-year high. Heck, even Bed Bath & Beyond is moving up. In fact, I’m raising BBBY’s Buy Below this week. I didn’t see that coming a few weeks ago. But first, let’s look at the latest news on the economy.

Q2 GDP Revised Higher

I always try to be careful when discussing the broad economy because at CWS Market Review, we’re primarily focused on the business end of things: profit, loss, debt and margins. We can lose sight of the fact that there’s still a lot of weakness in the economy, especially in the labor market. There are also many people with homes that are underwater, even years after the crisis. So when I point to signs of improvement, I don’t want to feel that I’m gliding over the distressed areas.

On Monday, the Census Bureau reported that new-home sales declined for the third month in a row. I should add context here by saying that sales are up more than 12% compared with one year ago. Look at any numbers from housing: you’re struck by how much things fell apart during the recession. Even though sales are up, they’re still running at the rate we saw during the lows in previous recessions. Economic recoveries are typically led by housing, but there was so much over-building before the crash that it’s taken us years to burn off the excess inventory. Only recently have new-home sales started to pick up.

Now let’s look at the price side. On Tuesday, the Case-Shiller Index said that home prices, as measured by the 20-City Index, rose by 8.1% in the 12 months ending in June. Once again, we’re better than where we were, but still below the crazy bubble peak. The 20-City Index is still more than 17% below its high, but it’s more than 24% above its crisis low. To borrow from Stealers Wheel, we’re stuck in the middle with you. Home prices are still rising, but the pace of increases appears to be slowing down.

On Tuesday, the Commerce Department said that durable goods soared 22.6% in July. That’s the biggest percentage increase on record. However, it was driven by a surge in orders for new aircraft. I like to keep an eye on orders for durable goods because these are the kinds of things companies wait to pay for when they think times are going to be good. During a recession, companies usually put off their plans to buy big-ticket items.

Digging into the durable-goods report, once we exclude aircraft, durable-goods orders dropped by 0.8% in July. But the number for June was revised upward to 3%. Compared with a year ago, orders are up 6.6%. Like housing, the trend looks good, but there’s been a summer slowdown.

On the technical side of the report, orders for non-defense capital goods, excluding aircraft (there’s a mouthful), fell 0.5% in July. But the June figure was revised up to 5.4%. The year-over-year increase is 8.3%. The message from these stats is that companies are out there buying things. They only do that if they see more revenue coming to cover the costs. This should also hint that more hiring will follow later this year.

We’ve seen a bunch of folks on Wall Street raise their forecasts for Q3 GDP. As many of you know, I’m not exactly a big fan of these forecasts, but it gives us a sense of what the institutions are thinking. Morgan Stanley just raised their estimates for Q3 GDP from 3% to 3.5%.

This Tuesday, we’ll get the ISM Index for August. These reports have a pretty good track record of lining up with recessions and expansions. The last few reports have been quite good. In July, the ISM hit 57.1, which is its highest point since April 2011. Any reading above 50 means that the economy is expanding. The ISM has dropped below 50 just once in the last five years.

Last month, Wall Street was shocked when the government’s initial report for Q2 GDP came in at 4%. That was well above what most people were expecting. On Thursday, it was time for the government to revise that report, and obviously people thought it would be revised down an inch or two. Not at all. It was revised higher, to 4.2%.

Breaking into the details, I noticed that gross domestic income rose by 4.7% last quarter. That’s the biggest increase in more than two years. I like to look at this metric because it better reflects the financial health of consumers.

Now that August is coming to a close, we’re already two-thirds of the way through Q3. In mid-September, earnings season will begin again. According to figures from Standard & Poor, Wall Street expects Q3 earnings for the S&P 500 of $30.11. Remember, that’s the index-adjusted figure (one point is $8.8 billion). This would be the highest quarterly total ever, and it would be the first time the S&P 500 has earned more than $30 in a single quarter.

For context, we earned $57 for the whole year in 2009. Wall Street’s estimate for Q3 earnings have been falling over the past few months. At the start of the year, the Street had been expecting Q3 earnings of $30.89. The falling estimates are actually much more modest than the big earnings cuts we saw in previous quarters. In fact, the estimates for Q4 have actually been increasing by a small bit. The Street now sees earnings of $32.39 for Q4. That’s up $0.22 since the start of the year.

The results are almost all in for Q2, and it looks like the S&P 500 earned $29.45. That’s up 11.7% over last year’s Q2. (Note that the earnings numbers from S&P sometimes differ from those of other media outlets.)

The S&P 500 is currently on track to earn $119.27 per share this year, give or take. That’s an increase of 11.2% over last year. Through Thursday, the S&P 500 is up 8% for the year. That roughly translates to a 12% rate for the entire year. In other words, stocks and earnings have been rising at about the same rate. That’s why I’ve ignored all this silly talk about another stock bubble. The market is going for 16.7 times this year’s estimate earnings. That’s in the dead center of historic valuations. Now let’s look at some of the news impacting our Buy List stocks.

The AT&T/DirecTV Merger Is Moving Along

We finally got some news on the big AT&T ($T) merger deal with DirecTV ($DTV). The New York Post reported this week that AT&T is working closely with the government on what it needs to do to win approval for its deal for DTV. I’m assuming this means they’ll have to ditch some assets to appease anti-trust regulators. The article didn’t have many details, which probably means negotiations are still going on. But this news was enough for UBS to raise its price target from $82 to $95 per share.

The merger deal is for $95 per share for DTV. Once we get past the “will it happen” question, the next hurdle is “when.” Shares of DTV are currently about 10% below the $95 deal price. That probably means that the market sees some risk in the deal falling through. The news this week is good for DirecTV. AT&T has too much at stake to let this deal fall through. DirecTV remains a buy up to $95 per share.

Three New Buy Below Prices

Trading hasn’t merely been low lately, it’s been absurdly low. Stock prices simply don’t move around very much each day. Perhaps that will change once all the Wall Street Poobahs get back from their beach cribs.

Despite the low volume and volatility, I want to raise my Buy Below prices on a few of our Buy List stocks. Two weeks ago, I raised my Buy Below on Fiserv ($FISV) from $64 to $66 per share, and it’s already threatening to climb above that. FISV recently rallied 10 times in 12 days. This week, I’m raising my Buy Below on Fiserv to $68 per share.

One of the rules of the Buy List is that our stocks are locked and sealed for the entire year. No matter how badly we want to, we can’t make any changes until the end of the year. This rule has probably helped us far more than it’s hurt us. When Bed Bath & Beyond ($BBBY) plunged this year, I’m sure a lot of nervous investors bailed out.

Ever since BBBY reached its low in late June, the stock has rallied impressively. Two months ago, I lowered my Buy Below to $61 per share. Later on, I raised it to $65 per share. The stock got as high as $64.70 on Wednesday, which is a four-month high. Fiscal Q2 earnings are due on September 23. The company said they expect earnings to range between $1.08 and $1.16 per share. I’m raising our Buy Below to $70 per share.

Express Scripts ($ESRX) is another good example of why we stay with high-quality stocks even when the market doesn’t. The shares had been having a rough year. But last month, the pharmacy-benefits manager beat earnings by a penny per share. ESRX also narrowed their full-year guidance to a range between $4.84 and $4.92 per share. The stock gapped up after earnings and continued to rally for most of August. I’m raising my Buy Below on Express Scripts to $79 per share. This is a solid stock.

The Elfenbein Theory

I wanted to draw your attention to a long post I did earlier this week on the blog site. I discussed my view for how different parts of the market behave.

I encourage you to read the entire piece, but the basic idea is that there are two important “dimensions” of the stock market. The first is between Cyclical and Defensive stocks. The other is between Value and Growth stocks. The first dimension is correlated with long-term interest rates, while the latter is correlated with short-term rates.

The idea that different sectors do well at different points in the economic cycle isn’t new. But by adding a larger framework to this cycle, I hope to give investors a better idea for what drives equity returns. You can read the post here.

That’s all for now. The stock market will be closed on Monday for Labor Day. In the U.S., the Labor Day weekend traditionally marks the end of summer, and trading volume typically picks up in September. We’ll get the ISM report on Tuesday. July Factory Orders are on Wednesday. Friday will be the big jobs report for August. Nonfarm Payrolls have topped 200,000 for the last six months in a row. Let’s see if we can make it seven. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: August 29, 2014

Eddy Elfenbein, August 29th, 2014 at 6:06 amHow Draghi Seeking QE Trade-Off May Find Austerity Trap

Euro Sags Ahead of Inflation Test, Ukraine Nerves Weigh

Yen at 120 Seen Needed by UBS Wary of Weimar-Japan Redux

US Economy Grew at Brisk Rate in 2nd Quarter

Wanda Teams With Tencent, Baidu to Challenge Alibaba

Instagram Like2Buy Merges Social Media and Shopping

Malaysia Airlines to Eliminate 6,000 Jobs Amid Overhaul

Abercrombie & Fitch Sheds Once-Prized Logo From Clothing

Tesco Slumps as Retailer Slashes Dividend 75% on Forecast

Jessica Alba ‘The Honest Co’ Valued at $1 Billion

Virgin Raises Private-Equity Cash to Keep Qantas Pressure

Morgan Stanley Plans Natural Gas Export Plant in New Commodities Foray

Businesses Are Winning Cat-and-Mouse Tax Game

GaveKal Capital: The Modern Day Widow Maker Trade

Ben Carlson: How Framing Affects Investment Decisions & Outcomes

Be sure to follow me on Twitter.

-

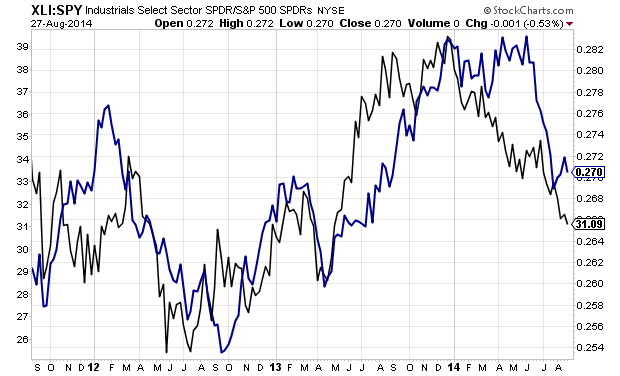

Industrials and Long-Term Rates

Eddy Elfenbein, August 28th, 2014 at 12:45 pmThis time, here’s a look at the relationship between industrial stocks and long-term interest rates.

The blue line is the Industrials ETF divided by the S&P 500 ETF. The black line is the yield on the 30-year Treasury.

-

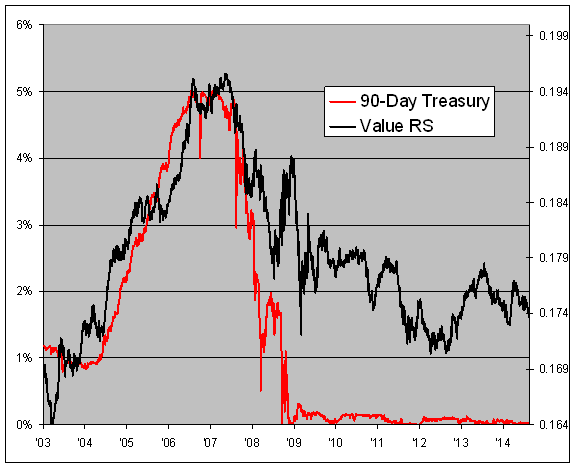

Value Stocks and Short-Term Rates

Eddy Elfenbein, August 28th, 2014 at 9:57 amHere’s a small addendum to yesterday’s post on how the stock market behaves. This chart shows the Vanguard Value Index divided by the Vanguard Index 500 fund. That’s the black line and it follows the right scale. The numerical value of the black line is irrelevant, but what’s important is that whenever the black line is moving up, it means that value stocks are outperforming the overall market. When it’s declining, value stocks are lagging.

The red line is the yield on the 90-day Treasury (left scale). Note how the two lines have a decently strong correlation. As I tried to stress in yesterday’s post, these cross-market relationships are far from overwhelming, but something is clearly going on. The correlation is especially strong in the near-term. Rising rates are good for value. Falling rates are not.

I think it’s interesting to note that ever since the Fed brought interest rates to the floor, there doesn’t seem to have been any great trend toward growth or value. I could be wrong, but to my eyes it mostly looks like noise.

I would think that over the very long term, value stocks would outperform the stock market, but there’s no reason to expect short-term rates to rise indefinitely. At least, I hope not.

-

Q2 GDP Revised to +4.2%

Eddy Elfenbein, August 28th, 2014 at 9:35 amSome good economic news this morning. Wall Street was surprised when the initial report for Q2 GDP came in at 4%. Today it was revised higher to 4.2%. A lot of economists had been expecting a downward revision.

Domestic demand increased at a brisk 3.1 percent rate, instead of the previously reported 2.8 percent pace. It was the fastest pace since the second quarter of 2010 and suggested the recovery was becoming more durable after output slumped in the first quarter because of an unusually cold winter.

Third-quarter growth estimates range as high as a 3.6 percent rate.

Economists polled by Reuters had expected the second-quarter GDP growth pace would be revised down to 3.9 percent. The economy contracted at a 2.1 percent pace in the first quarter.

Gross domestic income, which measures the income side of the growth ledger, surged at a 4.7 percent rate, consistent with strong job gains during the quarter. That was the fastest increase since the first quarter of 2012.

-

Morning News: August 28, 2014

Eddy Elfenbein, August 28th, 2014 at 4:43 amRussian Hackers Said to Loot Gigabytes of Big Bank Data

Philippine Q2 GDP Growth Fastest in Five Quarters, Rate Hike Likely

SEC Shelves Plan for Private Asset-Backed Bond Disclosure

Lending Club Could Be One of Silicon Valley’s Biggest Tech IPOs of 2014

Vivendi receives GVT bids from Telecom Italia, Telefonica

Kia Struggles as Sibling Hyundai Speeds Ahead

Kia Motors To Build $1 Billion Car Assembly Plant In Mexico

Market Basket Revolt Ends as Arthur T. Demoulas Wins Bid

Are Uber’s Aggressive Recruitment Tactics Legal?

Qantas Result Challenges Alan Joyce Leadership

Weaker Corporate Tax Receipts Worsen U.S. Budget Picture

Snapchat Founders Likely Billionaires With New, Reported Investment

Drones Could Rule the Skies Over Disney

Cullen Roche: Malkiel’s Mendacity

Roger Nusbaum: Is This Bull Market Real?

Be sure to follow me on Twitter.

-

Ross Stores Reaches Nine-Month High

Eddy Elfenbein, August 27th, 2014 at 11:58 amRoss Stores ($ROST) is finally getting some love from investors. ROST has been as high as $75.53 this morning. The shares were at $62 just six weeks ago.

-

Morning News: August 26, 2014

Eddy Elfenbein, August 26th, 2014 at 4:31 amEurope Bank Cleanup Driving $1.72 Trillion of Asset Sales

Nene Sees 1.8% South African Growth With Budget Under Strain

Napa Mops Up Wine and Tallies Its Losses After Quake

Deep Tax Cuts Opens Northern Front for U.S. Companies

Surging U.S. Stocks Echo Dot-Com Rally With Cheaper P/E

Slowing Home Sales Show U.S. Market Lacks Momentum

Time Warner Prepares To Offer Buyouts At Turner Cable Division

Roche to Acquire InterMune for $8.3 Billion

Accor H1 Profit Rises, Summer Business Trends Stable

What’s Twitch? Gamers Know, and Amazon Is Spending $1 Billion on It

Shareholders Sour on GrubHub Filing

Ann Taylor (ANN) Shares Soar on Activist Investor Pressure

HP $48 Million Lawyer-Pay Plan to Sue Autonomy Shot Down

Howard Lindzon: Kill All The Data Scientists! …and The Timeline is Everything.

Be sure to follow me on Twitter.

-

NY Post: AT&T Reaches Deal with Feds on DTV Merger

Eddy Elfenbein, August 25th, 2014 at 5:04 pmHere’s some potentially good news about the AT&T/DirecTV merger. The New York Post is reporting that AT&T has reached a deal with the feds on the conditions by which they can buy DirecTV.

Agreeing to comply means the Department of Justice will likely clear the AT&T deal in October. The FCC still has not ruled on the merger.

The move will allow AT&T to add DirecTV’s 20 million satellite-TV subscribers to its 5.7 million U-Verse TV service subscribers, which currently spans 22 states.

This merger has caused concern among those who believe the convergence of the few remaining telecom and cable giants will cause a rise in prices.

The deal has raised some eyebrows among consumer activities. We still don’t know what these conditions entail. It may mean the companies will have to spin-off some assets. If the Justice Department approves the merger, then it will mostly like get approval from the FCC. Still, nothing is guaranteed.

DTV closed today at $85.47. The merger deal is for $95. So that’s an 11% premium but I have no idea what the timeframe is.

-

The S&P 500 Breaks 2,000

Eddy Elfenbein, August 25th, 2014 at 10:18 amMoments ago.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His