Archive for August, 2014

-

Morning News: August 20, 2014

Eddy Elfenbein, August 20th, 2014 at 7:54 amBank of England Officials Break Ranks on Rates

Pound Fluctuates on BOE Minutes

China Levies Record Antitrust Fine on Japanese Firms

Argentina to Sidestep U.S. Ruling by Paying Bonds Locally

Jackson Hole Rally at Risk as Investors Preempt Yellen

Standard Chartered’s Headwinds Come From Many Directions

Target Lowers Earnings Outlook, Still Reeling From Data Breach

Lowe’s Shares Fall After Trimming Full-Year Outlook

Wells Fargo Launches Startup Accelerator for Financial Services-Inspired Tech Innovators

Glencore to Buy Back $1 Billion of Stock as Profit Gains

Uber Hires Top Obama Adviser Plouffe as ‘Campaign Manager’

Home Depot Profits Shine; Stock Still Undervalued

Cullen Roche: What Backs the Value of Money?

Joshua Brown: Google IPO: The Ten Year Anniversary

Be sure to follow me on Twitter.

-

Apple Breaks $100 per Share

Eddy Elfenbein, August 19th, 2014 at 4:31 pmShares of Apple (AAPL) broke $100 today. The stock split 7-for-1 in June, so it’s not at a new all-time high. Apple got to $705.07 two years ago, which is $100.72 post split. Apple got as high as $100.68 today before closing at $100.53.

On July 8, 1982, Apple closed at $11 per share. Adjusting for splits of 56-for-1, that works out to 19.6 cents per share. That means Apple is up 511-fold in just over 32 years.

As recently as April 17, 2003, Apple was going for 93.7 cents per share. The stock has averaged 51% per year since then (not including dividends). That means Apple has gained, on average, 1% every 8.8 days for over 11 years.

Apple’s gain has been so massive that the S&P 500 looks like a flat line in comparison.

-

Google Turns 10

Eddy Elfenbein, August 19th, 2014 at 12:25 pmThe company Google ($GOOGL), which I believe is some kind of Internet “search engine,” went public ten years ago today. On August 19, 2004, the company offered 19.6 million shares to the public at $85 apiece. The stock has since split 2-for-1 so that the $85 price is $42.50 in terms of today’s stock. The stock opened at $100 (or $50 post-split) on its first day of trading.

The shares are currently at $597, so Google is up more than 13-fold since the IPO, which is nearly 30% annualized. If an investor had paid $240 per share for Google, or more than five times the underwriting price, they still would have beaten the market (assuming they held on).

To describe the share history a bit more fully, Google raced to $373.62 (post-split) by November 7, 2007. That’s an amazing gain of 730% in about 3-1/4 years. That’s more than 93% annualized. The shares then plunged by more than two-thirds over the next year.

Measuring from Google’s extreme peak in 2007 to today, it’s been a decent stock, but not an outstanding one. Google has only barely outperformed the Wilshire 5000 (remember that Google doesn’t pay a dividend). But that’s a bit of cherry-picking with the data since the 2007 peak was so dramatic. The shares have gone on to make new highs. In February, Google reached its all-time high of $610 per share.

Google is expected to earn $31.57 per share next year. That’s 74% of their 2004 offering price, which is a nice ROE if you can find it.

-

Inflation Cools Off in July

Eddy Elfenbein, August 19th, 2014 at 10:39 amLately I’ve talked about how inflation has heated up. With this blog, I try to focus on the data and not let any larger economic/political views cloud my judgment. That’s why I’m taking a step back on my inflation views. For the second month in a row, the CPI data has come in soft.

This morning, the government reported that headline inflation rose by just 0.1% in July. That’s the lowest rate in five months. The core rate, which excludes food and energy, also rose by 0.1%.

Here’s a look at the monthly annualized changed in core prices since 2011. As you can see, the trend jumped higher in March, April and May but pulled back in June and July.

-

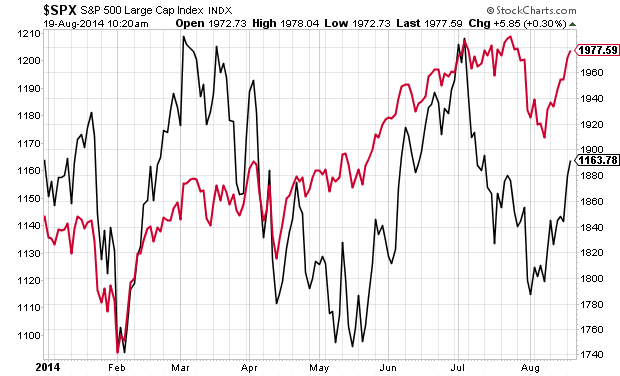

The Diverging Market

Eddy Elfenbein, August 19th, 2014 at 10:27 amHere’s a chart showing the point I was trying to make earlier. The black line (left scale) is the Russell 2000. Note how it peaked in March. In early July, it challenged that peak and failed to break it.

Since then it’s lagged the market. While the S&P 500, in red, has gradually pushed upward and is close to making a new all-time high.

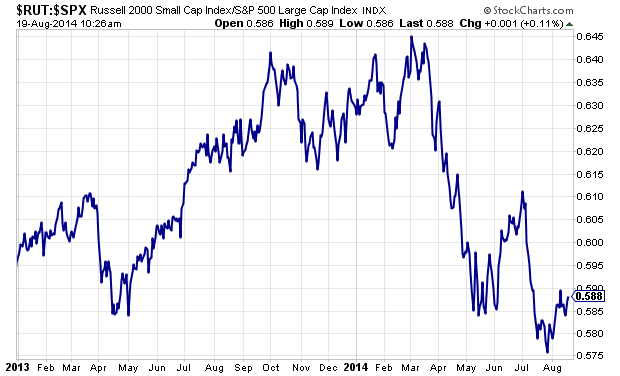

Here’s the Russell 2000 divided by the S&P 500 since the start of last year. See how sharply the Russell has lagged since early this year.

-

The Nasdaq Breaks Out to 14-Year High

Eddy Elfenbein, August 19th, 2014 at 10:11 amThe stock market is drifting higher in early trading on Tuesday morning. Yesterday, the Nasdaq Composite closed over 4,500 for the first time in more than 14 years. The last time the Nazz closed this high was March 31, 2000, just three weeks after the peak. The Nasdaq is up again today and has been as high as 4,519 this morning.

It’s interesting to note that the stock market made a new high on July 3, then pulled back and rallied to a new high on July 24. However, that’s not the case for the small-cap Russell 2000. That index made a new high on March 4 (1,208.65), then came just shy of that on July 3 (1,208.15), and well short on July 24 (1,158.11). In other words, the rally has become narrower.

-

Medtronic Earns 93 Cents Per Share

Eddy Elfenbein, August 19th, 2014 at 9:17 amMedtronic ($MDT) just reported fiscal Q1 earnings of 93 cents per share which was one penny better than expectations. Quarterly revenues rose 4.7% to $4.27 billion which was $20 million better than expectations.

Medtronic reaffirmed full-year guidance of $4.00 to $4.15 per share. They also reaffirmed their commitment to the Covidien deal.

From the earnings report:

“Our first quarter results are a solid start to fiscal year 2015,” said Omar Ishrak, Medtronic chairman and chief executive officer. “Our growth was broad based across businesses and geographies. I was especially pleased that our innovation pipeline is delivering strong results, particularly in the U.S., which had its highest revenue growth performance in 5 years.”

The company noted that it had the strongest growth for U.S. medical devices in five years. Shares of MDT are largely unchanged so far in today’s trading.

-

Morning News: August 19, 2014

Eddy Elfenbein, August 19th, 2014 at 8:33 amProfit Growth Rises at Bank of China, But So Do Bad Loans

China Antitrust Regulator Fines Two Japan Auto Parts Makers

Oversold Pound to Test 6-Year High on Interest Rate View

U.S. Consumer Prices Rise Modestly in July

US Home Construction Jumps 15.7% in July

Credit Swaps Polished in $19 Trillion Derivative Overhaul

Greener Pastures Signaling Rebound in U.S. Beef Supplies

Bidding War Breaks Out to Dominate Dollar Stores

Good News For The Housing Market? Home Depot Raises Full-Year Forecast

BHP Billiton Profit Up But Shares Down On Missed Capital Buyback

Google: Still an Unconventional Company

Medtronic Tops Views, Reaffirms Covidien Bid

Maersk to Buy Back Shares for First Time, Earnings Rise

Credit Writedowns: The Italian Runaway Train

Cullen Roche: The “Secular Stagnation” Theory is Massively Overblown

Be sure to follow me on Twitter.

-

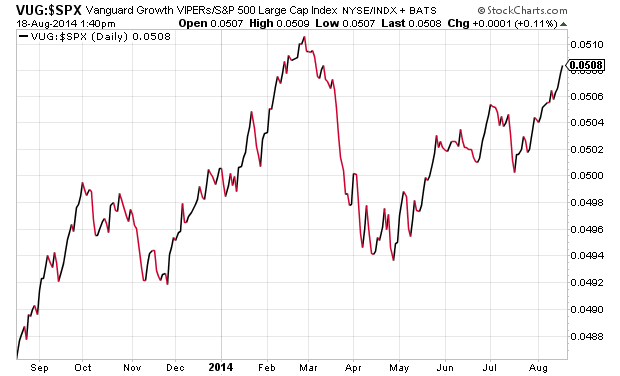

Growth Takes the Lead

Eddy Elfenbein, August 18th, 2014 at 1:52 pmIn March and April of this year, the stock market sharply turned against Growth stocks in favor of Value stocks. Bear in mind, we’re talking about relative strength, not absolute performance. Lately, however, Growth stocks have taken the lead again.

Here’s a look at the Vanguard Growth ETF ($VUG) divided by the S&P 500.

Growth has beaten the market consistently since mid-July.

-

Stock Prices and the Titantic Theory

Eddy Elfenbein, August 18th, 2014 at 1:37 pmAs I’ve written before, I’m not a fan of Robert Shiller’s “CAPE” valuation metric, which is the stock market’s P/E ratio based on the last ten years of earnings. I don’t see why we need to go back that far. Also, the CAPE has been above average almost consistently for the last 20 years. A good rule of thumb is that if some valuation metric reveals a big mispricing, the problem probably lies with the metric, not the price. In this weekend’s New York Times, Professor Shiller writes on stock market valuations:

It’s possible that bond prices account for today’s stock market valuations. But that raises another question: Why are bond prices so high? There are short-term explanations: the role of central banks, for example. But is there a compelling reason for prices of stocks and bonds (and maybe houses, too) to remain high indefinitely?

I’ve looked for untraditional answers. Perhaps today’s prices have something to do with anxiety about the future. I suspect that after the financial crisis, working people are much more worried about their future pay. Many are concerned that they might lose their jobs to cost-cutting, or that they might eventually be replaced by a computer or robot or website. Such anxiety might push them to try to make up for these potential shortfalls by investing in stocks and bonds — even if they worry that these assets are overvalued.

Extrapolating from a theory of Robert E. Lucas Jr. of the University of Chicago, one might well expect lofty stock prices amid such worries: When there aren’t enough good investing opportunities, people wishing to save more for the future may succeed only in bidding up existing assets even if they think they’re overpriced. Call it the “life preserver on the Titanic” theory.

This explanation, though, is probably not the whole story. The problem, as shown in my work with Sanford Grossman, founder of QFS Asset Management, and in work by Lars Peter Hansen of the University of Chicago and Kenneth Singleton of Stanford, is that the market just moves up and down more than Professor Lucas’s theory would suggest.

So nothing I’ve come up with is a slam-dunk explanation for the continuing high level of valuations. I suspect that the real answers lie largely in the realm of sociology and social psychology — in phenomena like irrational exuberance, which, eventually, has always faded before. If the mood changes again, stock market investments may disappoint us.

I don’t accept the notion that stock prices are elevated. For one, the market’s dividend yield is near 2% as it’s been for the last decade (except for the worst of the financial crises). The stock market’s one-year P/E Ratio has been fairly stable over the last 15 months. That may come as a shock to many people, but it’s true.

Consider that the S&P 500 is up 6.65% so far this year and earnings are projected to grow 11.14%. The calendar year is 63% over which means valuations are basically the same now as they were at the start of the year.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His