Archive for September, 2014

-

“Wild in the Streets”

Eddy Elfenbein, September 17th, 2014 at 9:26 pmThe voting age in tomorrow’s referendum in Scotland is just 16. Personally, I think the voting age should be constantly readjusted to one day younger than myself.

In any event, this mandates that I post the trailer to 1968’s “Wild in the Streets,” one of the grooviest and most fantabulous movies ever made. Yes, this movie really happened. It has real stars and everything. It happened and we let it happen.

-

The 10-Year Yield Today

Eddy Elfenbein, September 17th, 2014 at 3:03 pmIf you squint your eyes tight and look really hard, you might be able to make out when the FOMC statement came out.

Btw, I’m pretty sure the time axis is an hour behind.

-

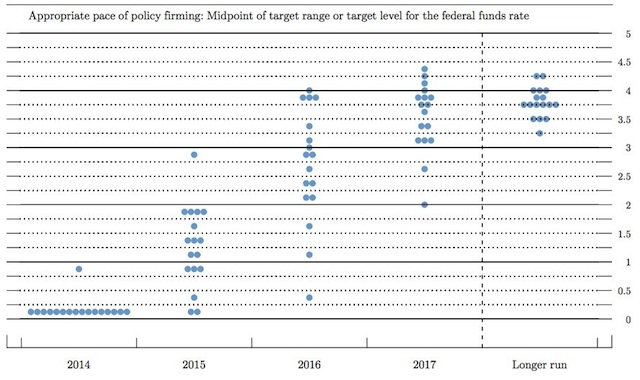

The Feds New Dots

Eddy Elfenbein, September 17th, 2014 at 2:55 pmHere’s a look at the Fed’s latest projections for interest rates. These are referred to as the dots since we get to see where all 17 FOMC members are.

It’s interesting how the Fed goes from certainty in the near-term to wide dispersion, then back to certainty. I’m most puzzled by 2016 since the FOMC members seem so widely dispersed. It also seems quite high. If I were on the FOMC (I’m not, btw), I would probably be at 2% to 2.25% for 2016. That’s closer to where the futures market is.

-

The Fed Tapers Again

Eddy Elfenbein, September 17th, 2014 at 2:16 pmThe FOMC just released their latest policy statement. Actually, two statements. One is the regular policy statement; the other was a “statement on policy normalization principles and plans.” More on that in a bit.

The central bank said it will taper its bond purchases yet again. No surprise there. Starting in October, the Fed will buy $15 billion in bonds. This timeframe strongly suggests that they’ll be done with QE at the next meeting, which is in late October.

The Committee decided to keep the words “considerable time” to describe the period between the end of QE and the first rate hike. There had been some speculation that those words might be changed. Chairwoman Janet Yellen has previously said six months, which was probably a rookie error on her part.

They also kept the phrase, “there remains significant underutilization of labor resources” which seems quite dovish. Overall, it’s a pretty straightforward statement. They slightly changed their wording on inflation: “Inflation has been running below the Committee’s longer-run objective.” Last time, they said inflation had “moved somewhat closer to” their long-run objective.

Now let’s turn to the “Policy Normalization Principles and Plans.” This is what the Fed has to say:

The Committee will determine the timing and pace of policy normalization–meaning steps to raise the federal funds rate and other short-term interest rates to more normal levels and to reduce the Federal Reserve’s securities holdings–so as to promote its statutory mandate of maximum employment and price stability.

When economic conditions and the economic outlook warrant a less accommodative monetary policy, the Committee will raise its target range for the federal funds rate.

During normalization, the Federal Reserve intends to move the federal funds rate into the target range set by the FOMC primarily by adjusting the interest rate it pays on excess reserve balances.

During normalization, the Federal Reserve intends to use an overnight reverse repurchase agreement facility and other supplementary tools as needed to help control the federal funds rate. The Committee will use an overnight reverse repurchase agreement facility only to the extent necessary and will phase it out when it is no longer needed to help control the federal funds rate.

The Committee intends to reduce the Federal Reserve’s securities holdings in a gradual and predictable manner primarily by ceasing to reinvest repayments of principal on securities held in the SOMA.

The Committee expects to cease or commence phasing out reinvestments after it begins increasing the target range for the federal funds rate; the timing will depend on how economic and financial conditions and the economic outlook evolve.

The Committee currently does not anticipate selling agency mortgage-backed securities as part of the normalization process, although limited sales might be warranted in the longer run to reduce or eliminate residual holdings. The timing and pace of any sales would be communicated to the public in advance.

The Committee intends that the Federal Reserve will, in the longer run, hold no more securities than necessary to implement monetary policy efficiently and effectively, and that it will hold primarily Treasury securities, thereby minimizing the effect of Federal Reserve holdings on the allocation of credit across sectors of the economy.

The Committee is prepared to adjust the details of its approach to policy normalization in light of economic and financial developments.

-

Inflation Drops in August

Eddy Elfenbein, September 17th, 2014 at 10:35 amToday is Fed Day. We’ll find out at 2 pm what the FOMC has decided. Janet Yellen will also host a post-meeting press conference. Today, it’s all about the language.

We got a surprising inflation report this morning. The government reported that consumer prices fell 0.2% last month. Economists were expecting no change.

Don’t think this was due to lower gasoline prices. If we look at the “core rate.” which excludes food and energy prices, then consumer prices were flat last month. Expectations were for an increase of 0.2%.

This is the lowest seasonally-adjusted core CPI in more than four years.

The S&P 500 still hasn’t topped its high from March 2000 when we adjust for inflation (with dividends, it has). Adjusting for the latest CPI data, the S&P 500 would have to make it to 2,126.48 to make a new all-time inflation-adjusted high. That’s about another 6.3% from where we are now.

Interestingly, the S&P 500’s all-time inflation-adjusted high isn’t from March 24, 2000, which had been the peak in nominal terms. The S&P 500 closed that day at 1,527.46. Rather, the inflation-adjusted peak came the previous day, on March 23, when the index closed at 1,527.35. That small one-day increase in stock prices was actually less than inflation.

-

Morning News: September 17, 2014

Eddy Elfenbein, September 17th, 2014 at 6:53 amChina Central Bank Injects $81 Billion Into Major Banks to Support Economy

Eurozone Inflation Stabilized in August

Bank Remains Split on Interest Rates as Scottish Referendum Clouds Future

Yellen Rate Raises Seen as Slow in Survey as Inflation Muted

Janet Yellen vs. the Inflation Zombies

Alibaba Buyers Say IPO Too Cheap to Miss Even With Risks

Sony Predicts Increased Losses Due to Struggling Mobile Business

Adobe Revenue Misses on Disappointing Digital Media Sales

Sears Cash Burn Has Suppliers Growing Leery of Lampert

Trian Partners Delivers Letter and White Paper Summary to DuPont Board

U.S. Consumer Bureau Sues Corinthian, Alleging Predatory Lending

Zara Owner Inditex Sees Profits Dip But Sales Rise

Sky Deutschland Advises Minority Shareholders to Reject BSkyB Takeover Offer

Cullen Roche: The Worst Call of the Last 5 Years

Edward Harrison: Country By Country Macro Update, September 2014

Be sure to follow me on Twitter.

-

Microsoft Raises Dividend By 11%

Eddy Elfenbein, September 16th, 2014 at 7:40 pmIn Friday’s CWS Market Review, I wrote:

Be on the lookout for a dividend increase soon from Microsoft ($MSFT). The software giant isn’t normally thought of as a dividend stock, but they’ve been working to change that. In the last four years, Microsoft has increased its dividend by 115%. The quarterly payout is currently 28 cents per share. I think MSFT will raise it to 31 cents per share.

I was right. After the bell, Microsoft ($MSFT) raised their quarterly dividend to 31 cents per share. That’s an increase of 10.7%. Over the last five years, MSFT has raised its dividend by 138%. The new dividend works out to $1.24 for the year. Going by today’s close and the new dividend, Microsoft now yields 2.65%.

-

Time is Running out for “Considerable Time”

Eddy Elfenbein, September 16th, 2014 at 1:15 pmThe Federal Reserve began its two-day meeting today. The real news will come tomorrow afternoon when we find out what they decided. I think we can expect another taper decision. The next meeting, which is in late October, should be the final taper decision, and then QE will be done for.

The Fed will also update its projections and include forecasts for 2017. But what a lot of people are watching for is the inclusion of the Fed’s “considerable time” language. This has been the phrase the Fed has used to describe the time period between the end of QE and the first rate increase. This is from the July statement:

The Committee continues to anticipate, based on its assessment of these factors, that it likely will be appropriate to maintain the current target range for the federal funds rate for a considerable time after the asset purchase program ends, especially if projected inflation continues to run below the Committee’s 2 percent longer-run goal, and provided that longer-term inflation expectations remain well anchored.

For now, it looks like the language will stay, but I’m curious how much longer it will last. I’m guessing they’re debating that right now. I like to look at the futures market, and the latest prices suggest that rates will rise next June. But remember, that’s just one increase. Assuming inflation stays at 2% (year-over-year is currently 1.99655%), that means that real short-term rates are expected to stay negative for another 2.5 years.

Slowly, things are getting back to normal. Very slowly.

-

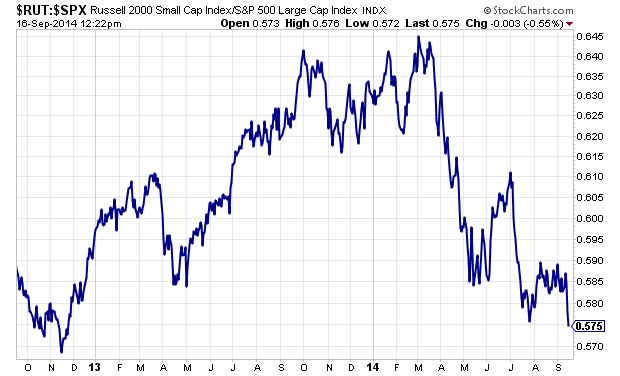

Russell 2000 Hits Underperformance Low

Eddy Elfenbein, September 16th, 2014 at 12:24 pmSmall-caps continue to lag. The ratio of the Russell 2000 divided by the S&P 500 is at a 21-month low today.

-

The Stealth Bear

Eddy Elfenbein, September 16th, 2014 at 12:19 pmWhen we look at “the stock market,” we’re usually talking about an index of stocks. Sometimes that isn’t the entire picture. Bloomberg notes that nearly half of the stocks in the Nasdaq are 20% or more off their high, which is the usual definition of a bear market.

About 47 percent of stocks in the Nasdaq Composite (CCMP) Index are down at least 20 percent from their peak in the last 12 months while more than 40 percent have fallen that much in the Russell 2000 Index and the Bloomberg IPO Index. That contrasts with the Standard & Poor’s 500 Index (SPX), which has closed at new highs 33 times in 2014 and where less than 6 percent of companies are in bear markets, data compiled by Bloomberg show.

This is a direct result of the flagging performance of small-cap stocks.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His