Archive for January, 2015

-

Morning News: January 13, 2015

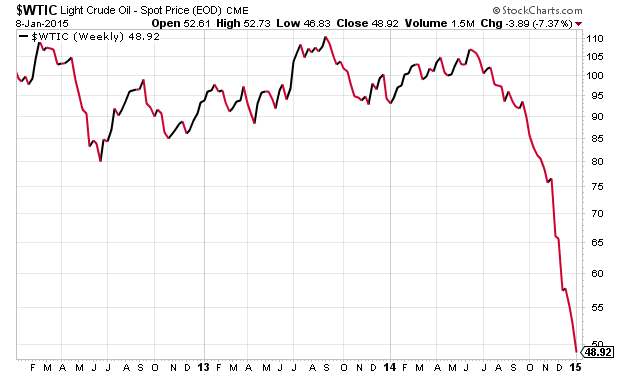

Eddy Elfenbein, January 13th, 2015 at 7:11 amPlummeting Oil Price Explained in Four Graphs

China Commodity Imports Surge on Low Prices

Iron Ore Imports by China Advance to Record as Price Collapses

This Is How India Controlled Its Once Untameable Inflation Problem

Treasury Yield Matches 20-Month Low as Notes Rise Before Auction

S.&P. Nears Settlement With Justice Dept. Over Inflated Ratings

Gold Rises to Highest Since October as U.S. Rate Outlook Weighed

How To Trade JPMorgan, Intel And Goldman Sachs

Uber Agrees to Share Data With Boston for Municipal Solutions

McDonald’s Walks Fine Line With ‘Signs’ Commercial

Citigroup Quietly Scales Back in Consumer Banking

$18.4 Billion Bankruptcy Bet on Caesars Is Backfiring With Lenders

Gross Says Pimco Fired Him After Offer to Scale Back Role

Jeff Carter: It’s About Effort, Not Difficulty

John Hempton: The Return of Cookie-Jar Earnings: United Technologies Edition

Be sure to follow me on Twitter.

-

10-Year Yield Approaches October Low

Eddy Elfenbein, January 12th, 2015 at 1:55 pmThe bond market reached a generational high in the summer of 2012. I didn’t think yields could go any lower. Now I’m not so sure.

During the ebola scare in October 2014, the 10-year yield got as low as 1.87% intra-day. We’ve gotten close to that level recently but haven’t busted through. That may happen soon.

-

Morning News: January 12, 2015

Eddy Elfenbein, January 12th, 2015 at 6:58 amECB’s Debate on QE Intensifies as Media Window Narrows

China Vehicle Sales Growth Forecast at 7% Amid Slowdown

Asia’s Richest Man Just Got Much Wealthier

Palm Oil Output in Malaysia Slumps Most Since 2006 on Floods

Yellen Proves Master of Math Forecasting U.S. Economy

U.S. Drivers Start 2015 With Cheapest Gas in Six Years

Shire to Buy NPS For $5.2 Billion to Boost Rare Disease Drugs

JD.com and Tencent Confirm $1.3 Billion Bitauto Investment

Roche Holding to Pay $1.03 Billion for Diagnostics-Firm Stake

Dollar Tree, Family Dollar See FTC Analysis Favorable to Their Merger

Volkswagen Aims to Tune in to Local Tastes in Latest U.S. Turnaround Plan

Two Blue-Chip Companies Drop UBS As Corporate Broking Adviser

Silicon Valley Turns Its Eye to Education

Howard Lindzon: The Passive Investing Bubble

Jeff Miller: Weighing the Week Ahead: A Message From the Bond Market?

Be sure to follow me on Twitter.

-

Justin Fox: “The Myth of the Rational Market”

Eddy Elfenbein, January 10th, 2015 at 1:13 pm -

Bed Bath & Beyond Drops 6.5%

Eddy Elfenbein, January 9th, 2015 at 4:22 pmIt was a rough day for Bed Bath & Beyond ($BBBY). I didn’t think there was anything surprising in the earnings report, but the market felt differently. At the closing bell, the shares were at $74.09 for a drop of 6.75%.

The stock has been surging lately. As rough as today was, it only erases the last three weeks.

-

December NFP +252K

Eddy Elfenbein, January 9th, 2015 at 8:30 amThe December jobs report is out. The economy created 252,000 net new jobs last month. The unemployment rate fell to 5.6%. (Or 5.565% to be precise.)

The NFP for October was revised higher by 18,000, and the one for December was revised higher by 50,000.

The shocker was that average hourly earnings fell by 0.2%. Economists were expecting an increase of 0.2%.

Here’s a look at the growth of NFP:

Here’s the annualized seasonally-adjusted rate of change for average hourly earnings:

We’ll get the December CPI report next week. As weak as AHE was, there’s a chance it was higher than the deflation we had. In other words, it could be that real wages rose last month.

-

CWS Market Review – January 9, 2015

Eddy Elfenbein, January 9th, 2015 at 7:08 am“I guess I should warn you, if I turn out to be particularly clear,

you’ve probably misunderstood what I’ve said.” – Alan GreenspanAlan, I know what you mean. Lately, the stock market has been rather difficult to make out as well. After going all of 2014 without a single four-day losing streak, the S&P 500 decided to give us a five-day losing streak this year (technically it started in 2014).

Santa Claus may have been hard at work on Christmas Eve, but the famous Santa Claus Rally was a monster no-show this year. If we narrow the Santa Claus Rally to the final five trading days of December and then add the first two of January, this was the second-worst Santa Claus Rally in the last 25 years and the third-worst in the last 65 years.

So if Santa took a breather this year, who’s willing to come in and save the market? That’s easy: central banks, that’s who. The stock market finally turned a corner on Wednesday, thanks to positive notes from the minutes of the Federal Reserve’s last meeting. Then on Thursday, the potential for more aggressive action from our friends at the European Central Bank helped power big gains for many European markets, and that spilled over into our exchanges.

Since the big bull market began nearly six years ago, the S&P 500 has fallen more than 5% on 12 separate occasions. Every single time, it’s rallied back. That nearly happened again this week, but the fall wasn’t that much. The big action lately hasn’t been in stocks—it’s been in the overseas bond pits. Bond yields in Europe have fallen to microscopic levels. It’s actually getting ridiculous. Ambrose Evans-Pritchard says that bond yields in Europe are at their lowest since the Black Death.

In this week’s CWS Market Review, we’ll take a closer look at what’s driving the ultra-low yields, and what it means for us. I’ll also focus on some good news from our Buy List. Ford Motor ($F) announced a 20% dividend hike. That’s a very strong signal from management. Shares of Ford now yield close to 4%. We also had a decent earnings report from Bed Bath & Beyond ($BBBY). Later on, I’ll preview the upcoming earnings report from Wells Fargo ($WFC). But first, let’s look at what’s happening in Europe.

Europe Is Battling Deflation

Europe is currently waging war against deflation—and losing. Yields on two-year notes in France, Germany and the Netherlands are all negative. Mario Draghi, the head of the European Central Bank, has been doing his best to warn lawmakers across the Eurozone that things aren’t looking good. Mostly, he’s been ignored.

That may have changed this week when Germany reported that inflation there fell to a five-year low. In December, prices in Europe’s largest economy fell by 0.1%. Economists were expecting an increase of 0.2%. Deflation is even worse in Spain. Consumer prices there fell by 1.1% last month. The fear is that once a deflationary spirals starts, it’s hard to stop.

Sure, some of this is due to lower energy prices, but that’s not all of it. The European economy is still very weak. This week, the euro fell to a nine-year low (see the chart below). The currency is now back where it was when it launched in 1999. There’s even talk that the euro and dollar could soon reach parity. Could you imagine one euro equaling one dollar?

In Italy, the unemployment rate rose to 13.4% in December. That’s the highest since the data series began in 1977. In Portugal, the unemployment rate is 13.9%. That’s actually good compared with other countries in Europe. In Greece and Spain, about one-fourth of the workforce is unemployed. In Germany, by contrast, there are plenty of jobs. The unemployment rate in Germany is currently the lowest since reunification.

The strong dollar, combined with deflation, has sparked a mad scramble for bonds in Europe and Asia. The yield on 10-year bonds fell to 0.484% in Germany and 0.287% in Japan. For five-year notes, German yields recently went negative, and France isn’t far behind. These are not the signs of a healthy economy.

But here’s what’s changed: The weak inflation report gives Draghi cover to take more aggressive action. Just the news that he’s considering more action ignited a big rally on Thursday. Clearly, the market wants more stimulus, and I’ve learned that the market usually gets what it wants.

The ECB meets again in two weeks, and they’re reportedly preparing a stimulus package for officials to consider. However, it’s unclear what exactly Draghi wants to do. Or can do. The German Bundesbank has been dead set against any type of European QE. Germany famously had massive hyperinflation in the 1920s, and that memory still scares the wits out of any German banker. Draghi has slowly waited these guys out. He’s even said that buying sovereign debt is on the table.

For the first time, the average 10-year bond yield in Germany, Japan and the U.S. has fallen below 1%. Bond yields are lower now than they were during the Great Depression. There’s an old saying on Wall Street: “don’t fight the Fed.” That’s good advice. They have more ammo than you do. I’d add that it’s not a good idea to fight the ECB as well. If he’s committed, I think Draghi will win his fight against deflation in Europe. His predictions have now come to pass.

Here in the U.S., the 10-year yield recently fell below 2% for the first time in 19 months. But we’re currently doing much better than the rest of the world. Higher rates are coming. The futures market now says there’s a 58% chance that the Fed will raise rates to at least 0.5% by September. I don’t know exactly when the rate hike will come, but I think it’s not too far away.

On Wednesday, the Fed released the minutes of their most recent meeting. The minutes made it clear that the Fed isn’t in a hurry to raise rates. The strong dollar is already helping keep prices low. I’ve talked a lot about the Strong Dollar Trade, and that’s still alive. This week, oil fell below $50 per barrel. At one point on Wednesday, oil dropped below $47 per barrel. It’s hard to justify higher rates with prices plummeting.

We’re continuing to witness the predictable market reactions to the Strong Dollar Trade. Energy and Materials stocks are lagging. Healthcare and Consumer Staples are in the lead. Utilities are also doing well. The only notable difference is that small-caps aren’t hit as hard as they had been.

As investors, how do we fight lower interest rates? Instead of chasing yields, it’s much better for us to focus on strong and rising dividends. I often tell investors that dividends are easily the most important and most overlooked part of investing. Dividends tend to grow, and reinvesting those dividends gets you more shares, which begets still more dividends. The effect may be small each week, but it adds up. Consider that in the last 20 years, the S&P 500 price index is up 348%. But the Total Return Index, which includes dividends, is up 555%.

The numbers are in for the fourth quarter, and dividends paid out by companies in the S&P 500 rose by 9.96% over last year’s Q4. That’s actually the second-slowest growth rate in the last 16 quarters. The slowest was Q4 of 2013, which came one year after the big dividend surge in late 2012 to pay out dividends before the tax rate went up. In the last four years, dividends paid out by the S&P 500 are up more than 73%.

For the year, the S&P 500 paid out $39.44 in index-adjusted dividends. That’s an increase of 12.72% over 2013. But here’s what interesting: The S&P 500 price index rose 11.39% last year. In other words, dividends grew faster than prices! That means the S&P 500 ended the year with a slightly higher dividend yield than it had when the year started. Despite all the talk of a stock bubble, at least one measure of the market’s valuation has moved lower.

Speaking of rising dividends, let’s take a look at the big dividend hike from Ford.

Ford Raises Dividend by 20%

On Thursday, Ford Motor ($F) had great news for investors. The automaker announced that it’s raising its quarterly dividend by 20%. The dividend will rise from 12.5 cents to 15 cents per share. This is the third time in three years that Ford has raised its dividend. The dividend is payable on March 2 to shareholders of record at the close of business on January 30.

This is a strong signal from Ford’s management. This is especially true because Ford’s earnings declined last year. We won’t get the Q4 report for another three weeks, but we can already estimate that Ford’s earnings fell around 30% in 2014. A few months ago, CEO Mark Fields said that Ford should make $6 billion in pre-tax earnings for 2014.

But last year was a transition year for Ford. The automaker spent a lot of time and money upgrading its plants and introducing new models. Unfortunately, there were also a few unpleasant recalls. We should start to see better results for Ford starting with the Q1 report in late April.

With the new dividend, shares of Ford now yield 3.89%. That’s a good deal. Ford remains a buy up to $17 per share.

Bed Bath & Beyond Earns $1.19 for Q3

After the close on Thursday, Bed Bath & Beyond ($BBBY) reported fiscal Q3 earnings (which ends in November) of $1.23 per share. That includes four cents in non-recurring money, so let’s say they earned $1.19 per share, matching Wall Street’s forecast. Sales rose 2.7% to $2.94 billion, which was a little bit less than the Street was expecting.

Three months ago, BBBY gave us Q4 guidance of $1.78 to $1.83 per share. I was pleased to see them reiterate that forecast this week. The fourth quarter (December, January and February) is the holiday quarter, and that’s very important for BBBY. For the full year, they see earnings ranging between $5.05 and $5.09 per share. That’s up from $4.79 per share last year.

Frankly, I’m a bit concerned about BBBY’s operating margins. They’ve always been very good, much better than those for the rest of the industry. Lately, however, they’ve drifted downward. I’d like to see some improvement here, but it’s not yet a big problem. This stock gave us a lot of headaches last year, but I’m glad we held on. This is a good company, and BBBY went on a furious rally in the second half of the year.

On Thursday afternoon, the stock got hit in the after-hours market, so Friday may be a bad day for BBBY. That’s just how the market reacts. Honestly, there wasn’t a single item in this report that should have surprised anyone. It’s just traders being traders. Don’t let that rattle you. Bed Bath & Beyond is a buy up to $77 per share.

Earnings Preview for Wells Fargo

Q4 earnings season is set to begin next week. As usual, Wells Fargo ($WFC) leads off for our Buy List. This is quite simply the best-run big bank in America.

Wells is due to report Q4 earnings on Wednesday, January 14, before the opening bell. Wall Street currently expects earnings of $1.02 per share, which is a slight increase over the $1 per share Wells made in Q4 of 2013.

Wells has been on a terrific run, but I think their earnings growth will slow down some for the next few quarters. It’s nothing they’ve done; it’s just the tougher environment for banking that exists right now. In fact, Wells would have missed Wall Street’s earnings consensus three months ago, but the bank’s bottom line was helped out by some technical factors.

Wells is doing well. They’re well-capitalized and their underperforming loans are getting smaller. The mortgage sector is weak, but I think that will gradually improve this year and next year. The key factor is that young home buyers are slowly returning to the market. That demographic wind should pick up for a few more years. Shares of WFC currently go for less than 13 times this year’s earnings. That’s a good deal. Wells Fargo remains a buy up to $57 per share.

That’s all for now. Earnings season starts up next week. Several of the big banks are due to report, including our own Wells Fargo ($WFC). We’re also going to get several key economic reports. Retail sales come out on Wednesday. Industrial production and CPI are on Friday. I’ll be curious to see if we had more deflation last month. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: January 9, 2015

Eddy Elfenbein, January 9th, 2015 at 6:59 amEuropean Markets Lower After German Industrial Production Falls

Santander Stock Sale Seen Pushing Europe Banks to Boost Capital

Swiss Inflation Rate Tumbles as Economic Worries Worsen in Region

U.K. Manufacturing Production Rises; Trade Gap Narrows on Oil

China December Inflation Near 5-year Low, More Policy Easing Seen

Want to Hire a Private Car in China? There Will Be No App for That

Fed’s JPMorgan Oversight Marked by Turf Battles, Watchdog Says

GM CEO Sees Higher U.S. Auto Sales in 2015

DuPont Investor Trian Starts Proxy Fight for Board Seats

XL Group Agrees to Acquire Catlin for $4.2 Billion

Google May Bring Auto Insurance Shopping Service to U.S.

Tycoon Li Ka-Shing to Revamp Empire to Address Valuation Discount

BMW Keeps Luxury Sales Crown, Beats Rivals in December

Ben Carlson: What Returns Can Investors Expect in Long-Term Treasuries?

Cullen Roche: Is Economics Becoming More Left Wing?

Be sure to follow me on Twitter.

-

Bed Bath & Beyond Earns $1.19 per Share for Q3

Eddy Elfenbein, January 8th, 2015 at 4:33 pmBed Bath & Beyond ($BBBY) just reported Q3 earnings of $1.23 per share, but that includes a four-cent benefit for non-recurring items, so it was really $1.19 per share.

That’s right in the middle of the guidance they gave us three months ago of $1.17 — $1.21 per share. Quarterly revenues rose 2.7% to $2.943 billion.

BBBY now sees full-year earnings coming in between $5.05 and $5.09 per share. For Q4, they see earnings ranging between $1.78 and $1.83 per share.

The shares got clocked after-hours, but I doubt that will last.

Here are the sales and earnings figures for the past few quarters:

Quarter Sales Gross Profit Operating Profit Net Profit EPS May-99 $356,633 $146,214 $28,015 $17,883 $0.06 Aug-99 $451,715 $185,570 $53,580 $33,247 $0.12 Nov-00 $480,145 $196,784 $50,607 $31,707 $0.11 Feb-00 $569,012 $238,233 $77,138 $48,392 $0.17 May-00 $459,163 $187,293 $36,339 $23,364 $0.08 Aug-00 $589,381 $241,284 $70,009 $43,578 $0.15 Nov-01 $602,004 $246,080 $64,592 $40,665 $0.14 Feb-01 $746,107 $311,802 $101,898 $64,315 $0.22 May-01 $575,833 $234,959 $45,602 $30,007 $0.10 Aug-01 $713,636 $291,342 $84,672 $53,954 $0.18 Nov-02 $759,438 $311,030 $83,749 $52,964 $0.18 Feb-02 $879,055 $370,235 $132,077 $82,674 $0.28 May-02 $776,798 $318,362 $72,701 $46,299 $0.15 Aug-02 $903,044 $370,335 $119,687 $75,459 $0.25 Nov-03 $936,030 $386,224 $119,228 $75,112 $0.25 Feb-03 $1,049,292 $443,626 $168,441 $105,309 $0.35 May-03 $893,868 $367,180 $90,450 $57,508 $0.19 Aug-03 $1,111,445 $459,145 $155,867 $97,208 $0.32 Nov-04 $1,174,740 $486,987 $161,459 $100,506 $0.33 Feb-04 $1,297,928 $563,352 $231,567 $144,248 $0.47 May-04 $1,100,917 $456,774 $128,707 $82,049 $0.27 Aug-04 $1,273,960 $530,829 $189,108 $120,008 $0.39 Nov-05 $1,305,155 $548,152 $190,978 $121,927 $0.40 Feb-05 $1,467,646 $650,546 $283,621 $180,980 $0.59 May-05 $1,244,421 $520,781 $150,884 $98,903 $0.33 Aug-05 $1,431,182 $601,784 $217,877 $141,402 $0.47 Nov-06 $1,448,680 $615,363 $205,493 $134,620 $0.45 Feb-06 $1,685,279 $747,820 $304,917 $197,922 $0.67 May-06 $1,395,963 $590,098 $148,750 $100,431 $0.35 Aug-06 $1,607,239 $678,249 $219,622 $145,535 $0.51 Nov-07 $1,619,240 $704,073 $211,134 $142,436 $0.50 Feb-07 $1,994,987 $862,982 $309,895 $205,842 $0.72 May-07 $1,553,293 $646,109 $154,391 $104,647 $0.38 Aug-07 $1,767,716 $732,158 $211,037 $147,008 $0.55 Nov-08 $1,794,747 $747,866 $203,152 $138,232 $0.52 Feb-08 $1,933,186 $799,098 $259,442 $172,921 $0.66 May-08 $1,648,491 $656,000 $118,819 $76,777 $0.30 Aug-08 $1,853,892 $739,321 $187,421 $119,268 $0.46 Nov-08 $1,782,683 $692,857 $136,374 $87,700 $0.34 Feb-09 $1,923,274 $785,058 $231,282 $141,378 $0.55 May-09 $1,694,340 $666,818 $142,304 $87,172 $0.34 Aug-09 $1,914,909 $773,393 $222,031 $135,531 $0.52 Nov-09 $1,975,465 $812,412 $245,611 $151,288 $0.58 Feb-10 $2,244,079 $955,496 $370,741 $226,042 $0.86 May-10 $1,923,051 $775,036 $225,394 $137,553 $0.52 Aug-10 $2,136,730 $874,918 $296,902 $181,755 $0.70 Nov-10 $2,193,755 $896,508 $305,110 $188,574 $0.74 Feb-11 $2,504,967 $1,076,467 $461,052 $283,451 $1.12 May-11 $2,109,951 $857,572 $288,948 $180,578 $0.72 Aug-11 $2,314,064 $950,999 $371,636 $229,372 $0.93 Nov-11 $2,343,561 $958,693 $357,020 $228,544 $0.95 Feb-12 $2,732,314 $1,163,669 $550,765 $351,043 $1.48 May-12 $2,218,292 $887,199 $313,398 $206,836 $0.89 Aug-12 $2,593,015 $1,032,669 $365,137 $224,330 $0.98 Nov-12 $2,701,801 $1,074,010 $361,649 $232,750 $1.03 Feb-13 $3,401,477 $1,394,877 $598,034 $373,872 $1.68 May-13 $2,612,140 $1,032,971 $323,101 $202,490 $0.93 Aug-13 $2,823,672 $1,113,484 $389,766 $249,304 $1.16 Nov-13 $2,864,837 $1,121,690 $374,647 $227,197 $1.12 Feb-14 $3,203,314 $1,297,437 $527,073 $333,299 $1.60 May-14 $2,656,698 $1,030,885 $300,701 $187,052 $0.93 Aug-14 $2,944,905 $1,134,045 $368,741 $223,953 $1.17 Nov-14 $2,942,980 $1,128,974 $352,683 $225,408 $1.23 -

Ford Raises Dividend 20%

Eddy Elfenbein, January 8th, 2015 at 4:13 pmGood news for Ford Motor ($F) investors. The company just bumped up the quarterly dividend from 12.5 to 15 cents per share. That’s a 20% increase. Ford will now pay out 60 cents for the year (assuming the dividend stays constant). The dividend is payable March 2 to shareholders of record at the close on Jan. 30.

Going by yesterday’s close, Ford yields 3.98%.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His