Archive for February, 2015

-

Morning News: February 23, 2015

Eddy Elfenbein, February 23rd, 2015 at 7:11 amGreece Readies Reform Plans to First Sign of Leftist Unrest

Britain Sells 1.0% Stake of Lloyds Bank for 500 Million Pounds

Fed Rate Rise Timing Back in the Spotlight

Yellen Faces Congress Amid Direst Threat to Fed Since Dodd-Frank

Obama to Lead Push to Toughen Broker Rules for Retirement Funds

Strike at U.S. Refineries Widens

West Coast Ports Face Several Months’ Backlog

Apple to Spend 1.7 Billion Euros on New European Data Centers

HSBC Profit Drops Sharply Amid Tax Backlash

Ergen to Lead Dish Again as Pay-TV Provider Loses Subscribers

Takanobu Ito to Step Down as Honda Chief Executive After 6 Years

Holcim-Lafarge Merger Terms Intact After Franc’s Gain on Euro

Canada’s Valeant to Buy Salix in $10.1 Billion Deal

Edward Harrison: How to Look at the Greece Bailout Deal

Jeff Miller: Weighing the Week Ahead: Help for the Economy from Housing?

Be sure to follow me on Twitter.

-

Erroll Garner

Eddy Elfenbein, February 20th, 2015 at 7:19 pmThe week’s over and we’re at an all-time high. Have a listen to the great Erroll Garner…then go home!!

Garner was famous for playing while seated on a phone book, which I think you can barely see around 2:26.

He would also play a few bars of nonsense “teaser” music before each song to fool his audience as to what he was about to play.

Garner used to sing/mumble along to his playing, which you can make out a bit around 1:25 to 2:10.

-

Newsletter Feedback

Eddy Elfenbein, February 20th, 2015 at 10:37 amIt’s been a while since I’ve done this. I’d like to ask you for feedback about the newsletter, CWS Market Review. Tell me what you like about it, and what you don’t like. Is it too short? Too long? Too in-depth or not deep enough? Should it come more often or on different days of the week? Is it too expensive? Let me know! I want to hear from you.

Just send me an email with “Feedback” in the subject line. Also, don’t be shy in saying that it’s fine as is. That’s important feedback as well. Thanks!

-

CWS Market Review – February 20, 2015

Eddy Elfenbein, February 20th, 2015 at 7:14 am“It was never my thinking that made the big money. It was always my sitting.”

– Jesse LivermoreOnce again, the Federal Reserve has given a green light for investors. This week, we got the minutes from the Fed’s last meeting, and once again we have clear evidence that the Fed isn’t about to raise interest rates anytime soon. With interest rates dragging on the floor, stocks continue to be the best alternative; and high-quality stocks like those on our Buy List are doing especially well.

Historically, the stock market has done well during Christmas, but February is typically lackluster. This year has been just the opposite. January was poor, but February has been quite good. So far this month, the S&P 500 is up 5.14%, which puts it on pace for the best month since October 2011. I’m happy to say that our Buy List is doing even better. We’re up 8.51% this month, and we already have three stocks that are up more than 10% on the year, including Cognizant Technology Solutions ($CTSH) which is up 17.7%.

This has been a good earnings season for us, and this past week, we got good earnings reports from Hormel ($HRL) and Wabtec ($WAB). Both stocks broke out to new 52-week highs. I’ll have more on their earnings reports in a bit. I’ll also preview upcoming earnings reports from Express Scripts ($ESRX) and Ross Stores ($ROST). But first, let’s take a closer look at what’s on the Fed’s mind.

The Federal Reserve Is on the Side of Stocks

Actually, it’s a little more complicated, because it’s not solely about what’s on the Fed’s mind, but it’s also about what the market thinks is on the Fed’s mind. Furthermore, it’s what the Fed thinks the market thinks the Fed is thinking. We’re quickly entering an infinite regress of central bankers, which is a highly disquieting thought indeed.

I’ll try to bring some clarity. The Federal Reserve has gone to extreme lengths to help the economy get back on its feet. Only now are we starting to see real gains. In the last year, the economy added 3.2 million jobs. This led to a series of speculations that the Fed is about to pull back on what central bankers like to call “accommodation.”

The Fed successfully wrapped up its bond-buying program despite many predictions that they would keep it going. So far, the Fed has acted smoothly. But recently, the Fed has gotten ahead of the game on interest rates. I believe the Fed has led investors to believe rates are going up sooner than they really are. The Fed has strongly implied that rates will start rising around the middle of this year. Call me a doubter. For one, prices are falling. I don’t see how you can raise interest rates when you have actual deflation. This week’s PPI report showed that wholesale prices fell 0.8% in January. Also, the futures market has begun to doubt that a rate increase will come by mid-year.

The key factor to look at is real interest rates, meaning the interest rate adjusted for inflation. So even if rates are near 0%, deflation translates into higher real interest rates. That’s not what we need right now. Next week we’re going to get the CPI for January, and I expect to see more deflation at the consumer level.

But I don’t think the deflation will last. The early evidence shows that gasoline prices stopped falling a few weeks ago and have risen about 20 cents per gallon on average. Longer-term interest rates have climbed as well. The yield on the 10-year Treasury is back above 2.1%. That’s still low in an absolute sense, but it’s higher than where it was. Coupled with this increase in yields, the stock market has divided as well. Bloomberg recently noted that since February 6, stocks with the lowest yields have done the best, while those with higher yields have done the worst.

On Wednesday, the Federal Reserve released the minutes from their last meeting. I should explain that the Fed minutes are a study in indefinite pronouns (“many said this, some said that”). But the overall tone shows a central bank worried about the fragility of the recovery. The futures market currently implies a 20% chance that interest rates will rise by June. Before the Fed minutes came out, it was 25%. While the number of jobs has grown, workers haven’t seen much in the way of a pay increase. That’s certainly not putting any pressure on prices. Since the summer, inflation expectations have plunged.

The Fed has said they’ll be “patient” in their decision to raise rates. Now investors are debating how long the word “patient” will appear in Fed policy statements. At this rate, I don’t think the Fed will raise rates until 2016, or possibly late 2015. This newly found reticence has been good for stocks. Just look at a one-year Treasury, which currently yields 0.23%, compared with a blue-chip like Microsoft ($MSFT), which yields 2.85%.

The stock market has responded. The S&P 500 touched another new all-time high this week. The Nasdaq Composite has rallied seven days in a row and is finally within sight of its all-time high, which it reached 15 years ago. (If only the Pets.com sock puppet were alive to see this day.) As Jesse Livermore said, it’s the sitting that made him money. That patience has paid off for us this month. Now let’s take a look at some of our recent Buy List earnings reports.

Wabtec Is a Buy up to $99 per Share

Two of our new Buy List stocks reported earnings this week. On Wednesday, Wabtec ($WAB) said they earned 95 cents per share for Q4. That’s a good number, and it was a penny per share above Wall Street’s consensus. If you’re not familiar with Wabtec, they make locomotives, brakes and other systems for the freight- and passenger-rail sectors. It’s one of those fairly dull industries that’s more profitable than you might think. That is, if you ever thought about it.

CEO Raymond T. Betler said: “We finished the year with a strong performance in the fourth quarter, and we are anticipating record results again in 2015. While we expect to face challenges this year, including global economic uncertainty and foreign currency-exchange headwinds, we will benefit from ongoing investment in freight-rail and passenger-transit projects around the world. Our long-term growth prospects remain solid, thanks to our diversified business model, balanced strategies and rigorous application of the Wabtec Performance System.”

That’s the theme of many of our companies—things are going well, but forex is a headwind. Wabtec earned $3.62 per share for all of 2014, which was a healthy increase over the $3.01 they earned in 2013. For 2015, Wabtec issued guidance of $4.05 per share. That was below Wall Street’s expectations. Going into the earnings report, the Street had been expecting earnings of $4.15 per share.

But it couldn’t have been much of a disappointment, as the shares rose 2.3% on Wednesday and another 2.4% on Thursday. The stock is up more than 10-fold in the last ten years. On Thursday, WAB closed above $95 for the first time ever. This week, I’m raising my Buy Below on Wabtec to $99 per share.

Hormel Foods Beats Earnings and Raises Guidance

On Thursday, Hormel Foods ($HRL) reported earnings for the first quarter of their fiscal year. Their fiscal year ends in October. For Q1, Hormel earned 69 cents per share. That was five cents better than expectations. Quarterly revenue rose 6.8% to $2.4 billion. That was a bit below consensus of $2.47 billion.

“We are off to an excellent start to our fiscal year, with double-digit earnings growth and record sales in the first quarter,” said Jeffrey M. Ettinger, chairman of the board, president and chief executive officer.

“Jennie-O Turkey Store increased operating profit by 56 percent, with strong value-added product-sales growth, robust turkey markets and favorable input costs,” remarked Ettinger. “Refrigerated Foods also turned in an excellent quarter by driving increased value-added sales, aided by the benefit of lower pork costs. Grocery Products was challenged by high input costs and soft sales on some brands, while International & Other delivered increases despite difficult export markets,” commented Ettinger. “Specialty Foods is focused on driving higher margins in the newly acquired CytoSport business, and going forward we believe the business is well positioned to deliver results in line with our expectations.”

Thanks to the strong Q1, Hormel raised its full-year guidance. They now see earnings ranging between $2.50 and $2.60 per share. That’s an increase of five cents at both ends, which matches the earnings beat. Wall Street had been expecting $2.54 per share. Shares rallied nearly 3% on Thursday. I’m lifting my Buy Below on Hormel Foods to $61 per share.

Ball Corp. Buys Rexam

In the CWS Market Review from two weeks ago, I told you that Ball Corp. ($BLL) was in talks to buy Rexam, a British aluminum-can maker. After a long courtship, Ball finally made an honest woman out of Rexam. On Thursday, they announced a $6.8 billion merger agreement. The combined entity will be the largest maker of food and beverage cans in the world.

Ball estimates cost savings of $300 million by 2018. I’m always skeptical of these cost-savings estimates, but clearly there will be some. The combined company will have 22,500 employees and $15 billion in sales.

Shares of Ball rallied strongly on anticipation of the deal and fell 4% after the deal was announced. The specifics of the deal are a bit complicated, but I’ll give you the simple version. Ball is paying a 17% premium for Rexam. The deal will be financed with $2.2 billion in new equity, a $3 billion revolving-credit facility and a 3.3 billion-pound bridge loan. (Pounds are, apparently, what British people use for money.)

There are still regulatory hurdles in Europe and the United States, plus shareholders have to approve the agreement as well. As part of the deal, Ball agrees to pay a “break fee” of 302 million pounds if the merger falls though due to regulatory reasons. The companies say they expect the deal will ultimately be completed sometime during the first half of 2016. This is a bold move on Ball’s part. Ball Corp remains a solid buy up to $75 per share.

Two Buy List Earnings Reports Next Week

We have two more earnings reports next week. Express Scripts ($ESRX), the pharmacy-benefits manger, is due to report Q4 earnings on Monday, February 23. Express Scripts was one of our stronger performers late last year. The company has hit expectations on the nose for the last two quarters.

In October, ESRX narrowed their 2014 estimates to $4.86 — $4.90 per share. That implies Q4 earnings of $1.36 to $1.40 per share. Wall Street’s consensus is for $1.38 per share, which sounds right to me. I’ll be curious to hear what guidance they have for 2015. I’m expecting around $5.35 per share, give or take. ESRX is a buy up to $87 per share.

Ross Stores ($ROST) is due to report their fiscal Q4 earnings on Thursday, February 26. The stock has done an amazing turnaround over the past seven months. At one point, shares of Ross dropped below $62 last July. This week, it cracked $97.

The deep discounter said that earnings for Q3 would range between 83 and 89 cents per share. I thought that was obviously too low and said so. I was right—Ross earned 93 cents for Q3. For Q4, Ross said that earnings should range between $1.05 and $1.09 per share. That’s more realistic. The Street, however, thinks Ross is still playing games. The current consensus is for $1.11 per share. Given that the Street expects an earnings beat, the short-term risk is to the downside. That’s just a warning that Ross may slide next week. Don’t be alarmed. Ross is a very good stock. I’m keeping my Buy Below at $96.

That’s all for now. Next week is the final trading week of February. We’ll also get some of the important end-of-the-month economic reports. On Thursday, the government releases the CPI report for January. Spoiler Alert: I think we’ll see another big drop in consumer prices, but deflation may soon peter out. Then on Friday, the government will revise its estimates for Q4 GDP. The initial report said the economy grew by 2.6% in real terms for the final three months of 2014. I think that might be bumped up a little. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: February 20, 2015

Eddy Elfenbein, February 20th, 2015 at 7:08 amEuro Region Economy Strengthens Amid Wrangling on Greece

Europe’s Firewalls May Not Be Enough to Stem Grexit Investor Panic

US Shale Leader EOG Resources Confidence No Match for Cheap Oil

Dollar Remains Stronger as Traders See Fed Set for ’15 Rate Rise

Yellen Confronts Economists’ Ignorance

Trappings of Chinese New Year Left at Sea by West Coast Port Dispute

Wal-Mart Just Put Huge Pressure on Target

The Bad News for American Express Just Won’t Stop

Morgan Stanley Predicts New Highs for Tesla’s Stock Even as Cash Could Get Tight

FTC Files Lawsuit Challenging Sysco-US Foods Merger

U.S. and British Spies ‘Hacked World’s Largest Sim Card Maker’

TransCanada to Seek U.S. Approval for $600 Million Upland Pipeline

Ex-Qualcomm Executive Pleads Guilty to Insider Trading

Jeff Carter: Valuations-Be Careful

Be sure to follow me on Twitter.

-

Beginning of the Week Is the Winner

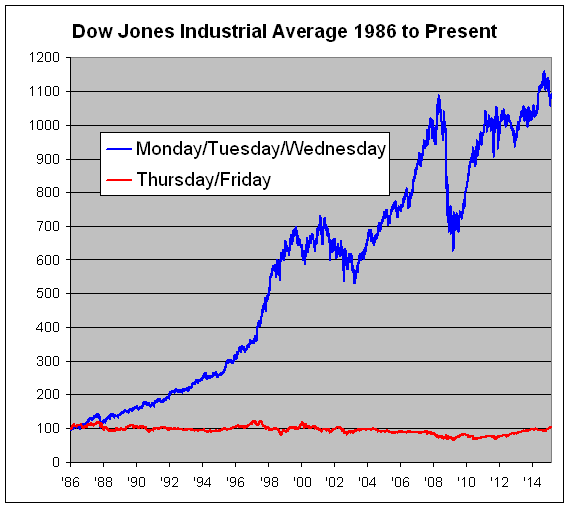

Eddy Elfenbein, February 19th, 2015 at 11:27 amSince 1986, the Dow Jones Industrial Average has had a pretty good run. The index has increased from 1,546.67 on the last day of 1985 to 18,029.85 today. That’s an increase of more than 1,000% in a little over 29 years. Not too shabby.

But here’s an interesting catch—nearly the entire gain has come at the beginning of the week. The combined gain on Monday, Tuesday and Wednesday comes to 988.46%. But the combined gain of Thursday and Friday is just 7.10%. That’s an amazing gap.

The Dow’s been taking four-day weekends on us and no one’s noticed! Of course, there’s no way this stat can translate into usable investment advice, but it’s interesting how the market can have a mind of its own. For nearly three decades, all that Thursday and Friday trading has added up to nothing.

Here’s a chart of how the Dow has performed since 1986. I divided it into two lines — the blue line is the combined return of being invested on Monday, Tuesday and Wednesday. The red line is for Thursday and Friday. I baselined both lines to start at 100.

-

Hormel Rises on Good Earnings

Eddy Elfenbein, February 19th, 2015 at 9:54 amThis morning, Hormel Foods (HRL) reported Q1 earnings of 69 cents per share which beat estimates by five cents. Quarterly revenue rose 6.8% to $2.4 billion. That was a bit below consensus of $2.37 billion.

“We are off to an excellent start to our fiscal year with double-digit earnings growth and record sales in the first quarter,” said Jeffrey M. Ettinger, chairman of the board, president and chief executive officer.

“Jennie-O Turkey Store increased operating profit by 56 percent, with strong value-added product sales growth, robust turkey markets, and favorable input costs,” remarked Ettinger. “Refrigerated Foods also turned in an excellent quarter by driving increased value-added sales, aided by the benefit of lower pork costs. Grocery Products was challenged by high input costs and soft sales on some brands, while International & Other delivered increases despite difficult export markets,” commented Ettinger. “Specialty Foods is focused on driving higher margins in the newly acquired CytoSport business, and going forward we believe the business is well positioned to deliver results in line with our expectations.”

The best news is that Hormel raised their full-year guidance. They now see earnings ranging between $2.50 and $2.60 per share. That’s an increase of five cents at both ends, which matches today’s earnings beats. Wall Street had been expecting $2.54 per share.

The stock has been up as much as 3% this morning.

-

Morning News: February 19, 2015

Eddy Elfenbein, February 19th, 2015 at 7:03 amECB Profit Declines as Interest Rates Drop, Staff Costs Surge

Greece Asks Eurozone for Loan Extension

Oil Prices Fall as U.S. Crude Stockpiles Grow

Port Dispute is Felt All Along the West Coast

Could Apple Compete With Tesla?

Ball Corp. Rolls Up Rexam With Sweetened $6.7 Billion Offer

Barrick Gold Reveals Asset Sale and Debt Reduction Plan

Nestle Forecasts Improvement in 2015

TurboTax, Phishing, E-Filing, And IRS Security

Strike Creates Turbulence for Air France-KLM

Is Snapchat Really Worth What Silicon Valley Thinks It Is?

T-Mobile US Swings to Profit As Revenue Surges

BAE Systems Posts More Than Fourfold Rise in 2014 Net Profits

Joshua Brown: Where Does the Fed See Systemic Risk?

Jeff Carter: Go Big or Go Home

Be sure to follow me on Twitter.

-

PPI Drops 0.8% in January

Eddy Elfenbein, February 18th, 2015 at 10:04 amHere’s a look at the seasonally-adjusted PPI. That’s the index of wholesale prices. This means that the Fed is in no hurry to raise rates.

-

Wabtec Earns 95 Cents per Share

Eddy Elfenbein, February 18th, 2015 at 8:47 amWabtec ($WAB) earned 95 cents per share for Q4. That was a penny above consensus. For the year, WAB earned $3.62 per share. They also issued guidance of $4.05 per share for all of this year.

CEO Raymond T. Betler said: “We finished the year with a strong performance in the fourth quarter, and we are anticipating record results again in 2015. While we expect to face challenges this year, including global economic uncertainty and foreign currency exchange headwinds, we will benefit from ongoing investment in freight rail and passenger transit projects around the world. Our long-term growth prospects remain solid, thanks to our diversified business model, balanced strategies and rigorous application of the Wabtec Performance System.”

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His {kind=link}

{kind=link}