Archive for May, 2015

-

Morning News: May 5, 2015

Eddy Elfenbein, May 5th, 2015 at 7:06 amEU Commission Sharply Cuts Greek Surplus Forecasts

Forget Tanks. Russia’s Ruble Is Conquering Eastern Ukraine

The Bloom Is Off The Chinese Rose

Australia’s RBA Cuts Rates, Markets Wonder If That’s All

Venezuela’s Economy Suffers as Import Schemes Siphon Billions

Central Bankers Reconsider Inflation Targets They Can’t Hit

Why Elizabeth Warren Makes Bankers So Uneasy, and So Quiet

HSBC Profit Up Slightly on Market Uptick in First Quarter

Adidas’ Upswing Continues Thanks to New Focus on Urbanites

Lufthansa Says to Restart Plan For Hybrid Bond

GE Hooks Up With Qualcomm and Apple for Smart Lighting

Marcellus Shale Extraction Fluids Discovered in 3 Water Samples

Los Angeles Sues Wells Fargo, Alleges Unlawful Conduct

Jeff Carter: History Doesn’t Repeat Itself, But Echoes

Roger Nusbaum: Poland Has Negative Yields?

Be sure to follow me on Twitter.

-

Ndamukong Suh Arm Wrestles Warren Buffett

Eddy Elfenbein, May 4th, 2015 at 3:46 pm -

Cognizant Earns 71 Cents per Share

Eddy Elfenbein, May 4th, 2015 at 8:02 amGood news this morning from Cognizant Technology Solutions (CTSH). The company earned 71 cents per share last quarter, one penny more than estimates. Their guidance was for EPS of at least 69 cents per share. (CTSH is a fan of using “at least” in their forecasts.) Revenue rose 20.2% to $2.91 billion. Guidance was for at least $2.88 billion.

“The clients we serve are experiencing tremendous change in their businesses and are increasingly turning to Cognizant to navigate that change,” said Francisco D’Souza, Chief Executive Officer of Cognizant. “The investments we have made in digital, automation, utility-based delivery models, consulting and industry-specific expertise are clearly paying off. Given how fast the landscape is changing, clients typically don’t have the skillsets to manage this transformation in-house and are turning to Cognizant to help them re-architect their core business and organizational models. As a result, we’re building deeper relationships with CEOs and boards, CIOs, and business and functional leaders to help them transform their businesses into digital enterprises.”

“The Cognizant approach of helping clients from setting strategy, to implementing and maintaining technology, to transforming and running business operations is enabling us to establish greater mindshare and market leadership,” said Gordon Coburn, President. “It’s evident across all geographies and industries that businesses are being forced to manage growth, innovation and scale while simultaneously managing costs. The shift to a digital enterprise is driving greater demand for our traditional services and solutions as clients find the need to keep pace with the speed and scale of innovation and maintain their competitive advantage.”

For Q2, the company sees earnings of at least 72 cents per share on revenue of at least $3.01 billion.

For the whole year, they see earnings of at least $2.93 per share. That’s an increase of two cents per share from their earlier guidance. They increased their revenue guidance from at least $12.21 billion to at least $12.24 billion.

Overall, this was a very good earnings report.

-

Morning News: May 4, 2015

Eddy Elfenbein, May 4th, 2015 at 7:08 amDraghi Starting Euro Bond Buying Turns Out Not to Be One-

Greek Jobless Legacy Adds to Danger for Tsipras as Funds Dwindle

Long Before British Vote, Financiers Weigh In

China April HSBC PMI Shows Biggest Drop in Factory Activity In A Year

Oil Prices Rise, Hovering Just Below Multiyear Highs

Takeover Fuel Begins to Flow as S&P 500 Bull Run Makes History

Comcast Profit Beats Estimates on Internet, Enterprise Growth

Cognizant Profit Rises on Double-Digit Gains in Health Care

McDonald’s Puts Its Plan on Display

Tesla Is Facing Stiff Competition In Its Plan To Generate New Revenue Through Batteries

GM Cuts Price On Next-Gen 2016 Chevrolet Volt: Will It Move The Needle?

The Truth About ‘Sell in May and Go Away’

Buffett Celebrates 50th Year at Berkshire, Faces Tough Crowds

Cullen Roche: How Warren Buffett’s Misunderstanding of QE Left Billions on the Table

Jeff Miller: Can Employment News Change the Fed’s Course?

Be sure to follow me on Twitter.

-

Wabtec Jumps on New Rules

Eddy Elfenbein, May 1st, 2015 at 11:42 amWabtec (WAB) is up strongly today. WSJ reports.

U.S. transportation regulators Friday will issue tough new rules for railroads hauling crude oil and ethanol that will require trains be equipped with expensive new brake systems, according to a person familiar with the rules.

The regulations will also require that sturdier tank cars be built for hauling oil, ethanol and other flammable liquids and prescribes upgrades for an estimated 154,500 tank cars already carrying flammables.

The person familiar with the new tank car rules said that trains carrying large volumes of crude oil will be restricted to 30 mile an hour speeds if they don’t have new electronic brakes installed by 2021. Other flammable liquids, including ethanol in high volumes would be speed-restricted after 2023.

The rules, which will be unveiled Friday in a joint announcement by U.S. and Canadian regulators, were tougher than expected. The electronically controlled pneumatic brakes deploy faster than the air brakes now used on freight trains.

Freight railroads maintain that installing them on existing railcars and locomotives would be prohibitively expensive and take years of work fully implement. The cost of installing ECP brakes on an existing railcar is estimated at $8,000 to $10,000, according to rail industry consultants. It wasn’t immediately clear whether Canadian regulators will also require electronic brakes.

The decadelong phase-in requirement for upgrading tank cars already in service is double the time originally suggested by U.S. transportation regulators for completing retrofits. Transportation safety advocates and railcar builder Greenbrier Cos. have said that 10 years is too long and have urged that older cars be upgraded or removed from service sooner.

Several fiery crashes of crude-oil trains, including four this year alone, have ratcheted up pressure on government officials to reduce the risks posed by dozens of crude-oil trains a day traveling through metropolitan areas on their way to refineries.

-

April ISM = 51.5

Eddy Elfenbein, May 1st, 2015 at 11:06 amThe good news is that ISM did not fall for the sixth month in a row. The bad news is that it stayed the same at 51.5.

-

Moog Earned 96 Cents per Share

Eddy Elfenbein, May 1st, 2015 at 10:16 amFor their fiscal Q2, Moog (MOG-A) brought in 96 cents per share. That was five cents more than estimates.

Moog Inc. today announced second quarter net earnings of $32 million and earnings per share of $.80, a 2% decrease from last year. Adjusted EPS of $.96 was up 17%. Total sales of $637 million were also down 2% from a year ago.

The results for the quarter included a non-cash charge of $8 million related to an accounting correction in the Space and Defense segment and a non-cash charge of $1 million on the sale of two small operations in the Medical Devices segment.

Aircraft segment sales in the quarter were $274 million, unchanged from a year ago. Commercial Aircraft sales were 5% higher, at $140 million, with commercial OEM sales, up 12% to $111 million. Sales to Boeing were $64 million and Airbus sales were $22 million. Commercial aftermarket sales of $29 million were off 16% on last year’s strong initial provisioning spares for the 787 program.

Military aircraft sales were down $7 million, to $134 million. OEM sales were down $2 million, to $80 million, with lower revenues on F-18 production and the KC-46 tanker development program offsetting higher F-35 Joint Strike Fighter and V-22 tilt rotor sales. Military aftermarket sales were down 8%, to $54 million.

Space and Defense segment sales were $93 million, down 2% from a year ago. Defense sales were up 2% on strong sales of missile and naval controls that were offset by weak security sales. Space sales were down 6%.

The Company’s Industrial Systems segment had sales of $129 million, down 15%, with the decline primarily tied to negative foreign currency effects. A general weakness across global industrial markets resulted in lower sales for industrial automation applications, down 15%. Sales of energy controls were off 16% and sales of simulation and test products, including motion bases for flight training simulators, were 12% lower.

Sales for the Components segment were 7% higher, at $109 million. Sales of aerospace and defense products were $46 million, up 11%. Industrial product sales were up 9%, energy sales were 6% higher and medical sales were mostly unchanged.

The Medical Devices segment had sales of $32 million, a 16% increase, with improvements in sales for pumps and administration sets.

The Company’s twelve month backlog is $1.3 billion.

The Company updated its projections for 2015 to include sales for the year at $2.54 billion, net earnings of $142 million and earnings per share of $3.55. The moderated guidance includes $.24 of negative special adjustments.

“We had some unusual charges this quarter,” said John Scannell, Chairman and CEO. “Excluding these charges, our underlying business performed well in the face of an adverse shift in our aircraft sales, and on-going macroeconomic headwinds. As we navigate through these challenges, we continue to focus on operational improvements, strong cash flow and allocating capital to create value for our shareholders.”

-

CWS Market Review – May 1, 2015

Eddy Elfenbein, May 1st, 2015 at 7:08 am“If being the biggest company was a guarantee of success, we’d all be

using IBM computers and driving GM cars.” – James SurowieckiOur earnings streak came to an end this week. Our first nine Buy List stocks to report Q1 earnings all beat expectations, but this week, two of our stocks met expectations and another two missed expectations. Fortunately, the misses weren’t that bad, and our Buy List continues to lead the overall market.

So far, the major trend of this earnings season is this: the weak dollar did a lot of damage, but not as much as initially feared. Before earnings season started, analysts had been expecting earnings to fall by 5.8%. It looks like the decline will be 2.9%. I suspect that people have underestimated the improvements in productivity.

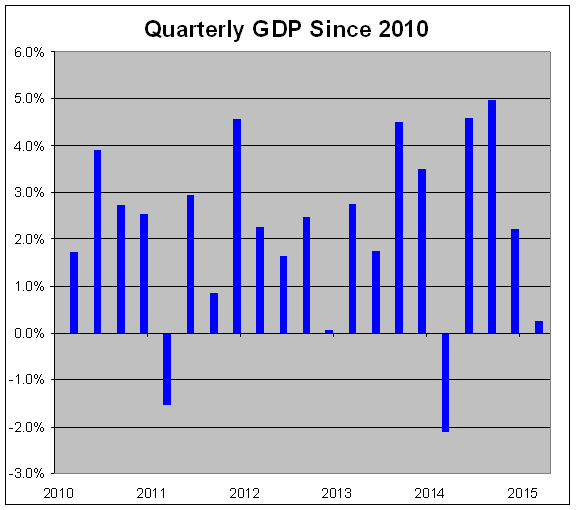

In this week’s CWS Market Review, we’ll take a closer look at the earnings parade. I’ll also preview the Buy List earnings coming next week. We also had a Fed meeting, plus a GDP report that was just ugly. The bright spot came on Thursday with the second-lowest number of initial jobless claims in the last 43 years. That may bode well for the April jobs report, which comes out next Friday. But first, let’s look at that GDP report and what it means for us.

The Economy Was Bad in Q1, but Will It Last?

On Wednesday, the government reported that the U.S. economy grew at a 0.2% annualized rate for the first three months of the year. That was well below expectations.

So what happened? Well, a number of factors. The strong dollar took its toll. Net exports fell by 7.2%. The bad weather most likely did some damage, as did the West Coast port strike. The plunge in oil prices also hurt the energy sector. Public-sector spending was also down.

If we dig a little deeper into the numbers, the details were still bad, but not quite so dire. Personal-consumption expenditures, which is the fancy term for consumer spending, grew at a 1.9% annualized rate.

The economy is probably rebounding this quarter. The dollar is beginning to stabilize, and the price of oil is firming up. On Thursday, we learned that real personal income rose by 0.3% in March. It appears that workers are finally getting a (small) wage increase. In the last year, the Employment Cost Index is up 2.6%.

Janet Yellen and her friends at the Federal Reserve are certainly paying attention to wage figures. Even though the unemployment rate has fallen, we haven’t seen much in the way of higher labor costs. The last jobs report was pretty weak, but there are hints the April jobs report will be a lot better. As I mentioned before, Thursday’s report for initial jobless claims was quite strong.

The Fed has held firm to the view that a rate hike is coming, and most likely this year, even though it’s hedged on exactly when. There’s now a slowly-emerging consensus that the Fed will raise rates in September. In fact, there’s now some daylight between the six-month and one-year Treasury yields, which suggests that rates will be rising sometime soon.

The Fed met again this week, and the policy statement confirmed their belief that the softness in Q1 was probably temporary. As a result, the Treasury climbed higher this week. For the first time in a month, the 10-year yield broke above 2%. Mirroring that move, many defensive stocks like utilities and healthcare lagged behind this week. CR Bard (BCR), for example, gapped up after its earnings beat, but it has gradually slid back since.

I think the Fed is getting ahead of itself. It’s hard to say for certain, but I don’t think the economy will need a rate hike for several more months. But once rates go higher, there will be less demand for stocks with solid dividends. With higher rates, growth stocks tend to be in greater demand.

Earnings from Ford, AFLAC, Express Scripts and Ball Corp.

On Tuesday, Ford Motor (F) reported Q1 earnings of 23 cents per share. Technically, that was an earnings miss since it was three cents below consensus, but truthfully, it was a decent report. Ford said that it got dinged for two cents due to a higher-than-expected tax rate.

Quarterly revenue fell 6% to $33.9 billion. The story is largely what we expected. North America is doing well, while Europe and South America are still weak. One bright spot is China, where Ford is gaining ground, but it’s far behind the competition.

Ford made it clear that they’re ramping up production to meet demand for their F-150 trucks. The automaker spent a lot of money (and time) retooling its plants to make the new aluminum-based trucks. That was a big gamble, and it’s starting to pay off. We’ll see more evidence as the year goes on. The F-Series has been the top-selling truck for 33 years in a row.

Traders apparently agreed that Ford’s Q1 wasn’t so bad because despite the earnings miss, the stock rose on Tuesday. Ford Motor remains a good buy up to $17 per share.

After the bell on Tuesday, AFLAC (AFL) reported Q1 operating earnings of $1.54 per share. That matched Wall Street’s forecast. The duck stock said that the weak yen knocked off 13 cents per share last quarter.

Again, there’s nothing really surprising in this report. The company reiterated that they aim to grow their operating earnings by 2% to 7% this year, on a currency-neutral basis. For Q2, AFLAC expects earnings to range between $1.46 and $1.57 per share. That assumes the yen averages between 120 and 125 to the dollar. The yen has actually gained a bit recently.

For the full year, AFLAC sees operating earnings coming in between $5.74 to $6.15 per share. Again, that assumes the yen stays between 120 and 125 to the dollar. The shares pulled back after the earnings report, but the damage wasn’t too bad. The stock is still going for a little over 10 times this year’s earnings. I’m keeping my Buy Below at $65 per share.

Express Scripts (ESRX) also met Wall Street’s forecast. The pharmacy-benefits manager earned $1.10 per share for Q1. Overall, it was a good quarter for Express Scripts.

“As our industry evolves, and plan sponsors have more business models to choose from, it is increasingly clear that Express Scripts is the best choice to manage America’s pharmacy benefits,” stated George Paz, Chairman and Chief Executive Officer. “At every turn, we add value to healthcare by combining a superior model of patient care with aggressive payer advocacy. Our unique combination of scale, client alignment and unmatched will, consistently creates greater value for patients and payers, while delivering solid results for our shareholders.”

Express Scripts also narrowed its full-year guidance by two cents per share at both ends. The old range was $5.35 to $5.49 per share. The new range is $5.37 to $5.47 per share, which translates to a growth rate of 10% to 12%. That’s not bad. For Q2, which ends on June 30, ESRX expects earnings of $1.39 to $1.43 per share. That’s better than the $1.37 Wall Street had been expecting.

The shares had an unusual ride this week. The stock initially gapped up after the earnings report. ESRX got as high as $88.99 on Wednesday morning before pulling back to $84.79 by the end of the day. Then after the closing bell on Wednesday, the company announced that it was accelerating its share-repurchase program. Express Scripts will get about 55.1 million shares in exchange for a payment of $5.5 billion. That helped the stock open strongly on Thursday.

Then news broke late Thursday that ESRX, among others, might be interested in buying Omnicare (OCR), a supplier of drugs to nursing homes. I won’t even begin to guess whether a deal will come about, but ESRX certainly has the financial muscle to make it happen. Frankly, they’re going to be named in any discussion of a buyout in this sector. Express Scripts is a solid buy up to $89 per share.

On Thursday, Ball Corp. (BLL), one of our new stocks this year, announced Q1 earnings of 69 cents per share. That was a big earnings miss—10 cents below consensus. But again, looking at the details, the results weren’t that bad. Revenues slightly beat consensus, and Ball lost 16 cents per share last quarter due to currency costs. The can maker also reiterated that it expects full-year free cash flow of $600 million.

John A Hayes, Ball’s CEO said, “First-quarter results were largely impacted by expected headwinds totaling 16 cents per diluted share from foreign currency translation, higher metal premiums in Europe and start-up costs related to growth capital investments. We continue to invest in our future with ongoing capital projects in North America, Europe and Southeast Asia that will fully ramp up in the second half of 2015 and the first half of 2016.”

Scott C. Morrison, the CFO, added, “Operationally, our first-quarter results were largely in line with our expectations. While metal premiums and start-up costs will persist in the second quarter, and currency translation will remain a headwind for the balance of the year, our business remains solid.” He also said that the company has begun several hedges in order to mitigate currency costs.

Traders seemed to agree that Ball’s quarter was just fine. The stock dropped 0.6% on Thursday, which was less than the 1% fall for the S&P 500. Ball Corp. remains a good buy anytime it’s below $75 per share.

I also want to add a quick word on Microsoft (MSFT). In last week’s CWS Market Review, I said I wanted to hold off on changing my Buy Below on Microsoft because I wanted to see how the market responded to the strong earnings report. Well, now we know. The market liked it. A lot!

Shares of MSFT soared more than 10% last Friday—and kept going. At one point on Thursday, Microsoft got as high as $49.54 per share. That’s not far from its 15-year high. Even with the price surge, the dividend still yields more than 2.5%. It’s about time this stock got some attention from the market. I’m raising my Buy Below on Microsoft to $51 per share.

Earnings Next Week from Cognizant and Fiserv

We have our final two earnings reports next week. Cognizant Technology Solutions reports on Monday, May 4. Fiserv follows on Tuesday, May 5.

Cognizant Technology Solutions (CTSH) has been our top-performing stock this year (+11.2%). Three months ago, the company reported very good Q4 results. Revenues rose 16.4% to $2.74 billion, and EPS beat expectations by two cents. Cognizant has been helped by its aggressive expansion into healthcare.

For Q1, Cognizant said they see earnings of at least 69 cents per share. I assume that means they expect 70 cents per share. They also see Q1 revenues of at least $2.88 billion. For all of 2014, Cognizant projects earnings of at least $2.91 per share on revenue of at least $12.21 billion. That means CTSH is going for about 20 times this year’s earnings. I’m not a pure-value investor, so I don’t mind paying a growth premium as long as the company is worth it, and CTSH surely is.

Last year was Fiserv’s (FISV) 29th year in a row of double-digit earnings growth. In February, the company said they expect internal revenue growth of 5% to 6% for this year. They also expect EPS to range between $3.73 and $3.83. That represents a growth rate of 11% to 14%, so the earnings streak should continue. Wall Street expects Q1 earnings of 86 cents per share. That sounds about right to me.

Moog (MOG-A) confirmed that their fiscal Q2 earnings report will come out later today. I’ll have details on the blog. Last quarter was weak due to the strong dollar. The company also cut full-year guidance to $3.85 per share (it could be $3.95 with buybacks). As with a lot of companies, I don’t think the damage from the dollar will be quite so bad.

That’s all for now. Still more earnings to come next week. On Wednesday, we’ll get the productivity report. Also, ADP will release its jobs report. Initial jobless claims follow on Thursday, and that leads us up to the big April jobs report on Friday morning. The March report was a dud, so it will be interesting to see if there’s a rebound. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: May 1, 2015

Eddy Elfenbein, May 1st, 2015 at 7:05 amChina’s Struggles Argue For Stimulus All Round

South Korean Exports Drop for Fourth Month as Won Strengthens

UK Factories Suffer Slower Growth in April

Stress Tests Reiterate Lack of Capital for Fannie Mae, Freddie Mac

As The NLRB Attacks Franchisors Like McDonald’s, Is `Quasi-Franchising’ The Answer?

Tesla Charges Into Home Battery Market Despite Challenges

Lloyds Says It’s Poised to Beat Lending Profitability Target

LinkedIn Slashes Full-Year Profit Forecast

Virgin America Mulls Picking Up New Jets During Delivery Drought

DreamWorks Animation’s Loss Deepens Even as Revenue Rises

Uber Office in Guangzhou ‘Raided’

Visa Forecasts Current-Quarter Profit Below Street

OmniVision Agrees to $1.9 Billion Sale to Chinese Consortium

Howard Lindzon: Speculation Fever

Joshua Brown: The New New New Normal – US Wages Rising

Be sure to follow me on Twitter.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His {kind=link}