Archive for April, 2016

-

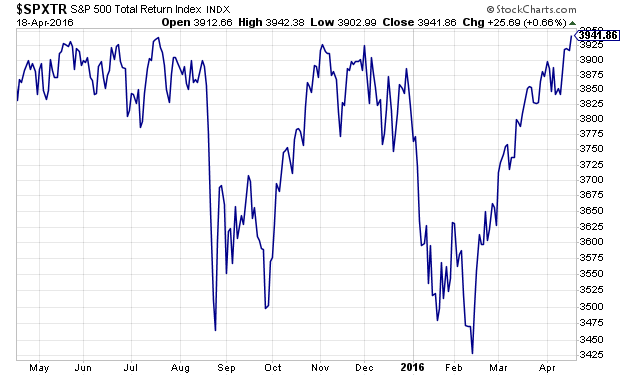

ATH

Eddy Elfenbein, April 18th, 2016 at 5:18 pm

Not for the S&P 500, but for the S&P 500 Total Return Index, which includes dividends. The S&P 500 Total Return Index closed today at 3,941.86, which is an all-time high. It surpassed the previous peak of 3,939.35 from July 20. Note that the S&P 500’s current high came on May 21. The index needs to rally another 1.7% to make a new high there.

-

This Year’s Blogger Wisdom

Eddy Elfenbein, April 18th, 2016 at 1:13 pmFor the last few years, Tadas Viskanta has asked a number of financial bloggers their opinions of important questions facing the industry. I was fortunate enough to be included in this year’s edition.

Here’s a list of the questions, along with my answers and the answers from some of my fellow finance bloggers.

Question: Venture capital has likely dried up for stand-alone robo-advisors. If so, where does the business of rob-advising go? Or said another way, is robo-advising simply going to be the way advisors manage client accounts going forward?

I skipped that one because I felt I don’t have anything profound to add but here’s Ben Carlson:

The competition for robo-advisors will continue to heat up because almost every wealth management or fund firm is going to have their own version of robo-advisor software at some point. I think the best way for robo-advisors to continue their growth will be to make a huge push into the workplace retirement business (something Betterment is already doing). The 401(k) and 403(b) markets are ripe for disruption by a low-cost provider as most of these plans are filled with terrible fund choices and high costs to plan users. Plus, the 401(k) market is much stickier in terms of clients because you have money automatically going into client accounts out of every pay check. Most companies don’t have the expertise to understand these plans on their own so offering a simple, low-cost solution would seem like an obvious way for robo-advisors to gain market share. This is especially true among small businesses who are the most over-charged group in need of a better solution.

Question: The ‘smart beta’ or factor-investing bubble seems to be in full bloom. Is ‘smart beta’ simply the new active investing? If so, what happens to the entire fund industry which was built on the high fees associated with active management?

Here’s me: I’m honestly not terribly impressed with Smart Beta. It’s mostly driven by marketing pitches. To my mind, it’s another form of chasing return. To the extent that any of these strategies work, it tends to be small and fleeting. (Make no mistake, I believe some are real.) The bottom line is that straight vanilla indexing is probably better for most investors, and simply buying and holding great stocks is even better than that.

Here’s David Merkel: Smart beta is a form of enhanced indexing. It is not active management. As in the quant quake in August 2007, “smart beta” will have its own episode of failure when too much money pursues it. It will be uglier due to the lack of human intervention. Active management will continue to shrink, but those who do it will have better opportunities. Fees will be under pressure, but less so than most imagine.

Question: Like just about every other blogger I have been writing on the rise on index investing. Should we care that the percentage of assets in indexes is on the rise, or should we just sit back and enjoy the (low cost) ride?

Here’s me: No, I’m not worried about the rise of indexing. The investment world loves to find things to be “concerned” about. Indexing is a great benefit for investors. I find the efficient versus inefficient debate to be pretty tedious. If you’re willing to accept what the market does, then indexing is a fine strategy. Still, with a little work, you can do better.

Here’s Josh Brown: Enjoy the ride. And know that the cure for “too much indexing” is already in progress in the form of a flat, choppy market that rises and falls but ultimately goes nowhere, which is the story of the MSCI All Country World Index heading into its third year of nothing. A few more and you’ll see a lot of the enthusiasm for low cost, passive dim.

Question: It does not escape me that the entire distribution list on this “Blogger Wisdom” e-mail chain is entirely male. I have written extensively on why this is an issue for the investment industry. What, if anything, can be done to make the investment industry more inclusive?

I didn’t have an answer but here’s Cullen Roche: If the men on this planet don’t exterminate each other in the future I am certain that the women will come to their senses one day and do it for us. A perfectly efficient stock market will be the result.

Question: Think back to the last edition of this series a couple of years ago. Have you changed your mind about something (big or small) over that time period? If so, what and why?

Here’s me: This may be an odd response, but I’ve recently changed my mind about volatility. Specifically, I think it’s incorrect to see volatility as some kind of gnome that stands above and apart from the market. To put it bluntly, the market doesn’t fall on volatility. Instead, volatility is up because the market is down. It falls when the market rises. The correlation between the VIX and the distance the market is from its six-month high is about 70%. I was surprised to see that it’s true.

Here’s Michael Batnick: I can’t think of anything that I’ve done an about face on, but one thing I am sticking with is my conviction to minimize the home country bias. I do not believe that investing in companies that generate a majority of their sales overseas is the same thing as investing in international stock markets. These giant multinationals are highly correlated with their domestic index and do not provide the same diversification benefits.

Question: What are you jazzed about that no one else is talking about? That could include a book, blog, Twitter feed, song, movie, app, online series, etc….

Here’s me: A few things. It looks like an ETF based on the Buy List will become a reality. We’re still in the planning stages, but it looks promising so far.

Another idea that’s bouncing around my head is the relationship of different market groups to each other. For example, why do bonds follow stocks for a while then break apart?

There’s been some quant work here (multi-dimensional scaling, etc). I think this is an unexplored vein, and it could reveal some important insights on the market.

Here’s Conor Sen: As I believe with rate hikes underway we’re in the late cycle in the US, I’m trying to think ahead to what the next cycle’s boom will be. At the moment from a tops-down perspective in the cycle from…I don’t know…2018-25? — I’d love to be in companies that are using some combination of data/analytics/information/automation/robotics, sensors, solar energy, and transportation to solve problems for consumers. More capex-heavy, less trivial app-conomy stuff.

Lastly, here are Tadas’ answers.

-

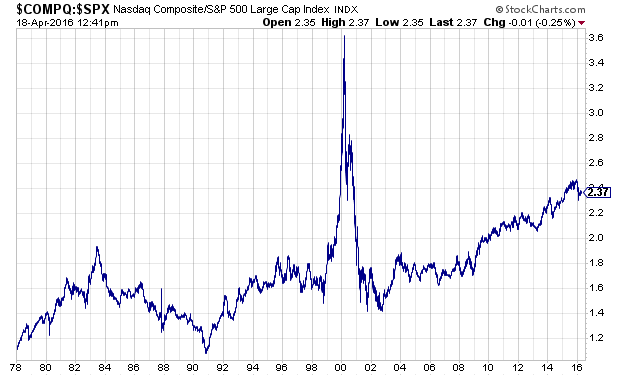

This Is What a Bubble Looks Like

Eddy Elfenbein, April 18th, 2016 at 12:56 pmOne of the frustrating aspects of finance is the eagerness of so many to proclaim a bubble. But an investment bubble isn’t a stock rallying from 15 times earnings to 19 times earnings. Not at all. A true bubble is when valuations leave earth’s orbit — and true bubbles have been relatively rare.

Here’s a simple chart to show you how extraordinary the 1990s tech stock bubble was. This is the Nasdaq divided by the S&P 500.

In a few months, the entire relationship changed. That’s what happens when there’s a bubble. Bubbles do happen, but not very often.

-

Apple’s Gold Mine

Eddy Elfenbein, April 18th, 2016 at 10:36 amI thought this was fascinating:

In its annual environmental report released this week, Apple said it recovered 2,204 pounds (more than a ton) of gold from recycled iPhones, iPads and Macs last year. That’s $40 million worth.

Gold is used in consumer electronics because it is highly averse to corrosion and an excellent conductor of electricity. Silver is actually the best conductor, but it corrodes easily. Copper is super-cheap, but it moves electrons too slowly for some of the most important computing tasks.

Of the 90 million pounds of e-waste through its recycling programs, Apple said 61 million was in reusable materials. Gold made up a relatively trivial amount. But since gold is currently trading at more than $1,200 per troy ounce, it’s among the most valuable materials it pulled from all those old gadgets.

Apple said it also collected 23 million pounds of steel; 13 million pounds of plastic; 12 million pounds of glass; 4.5 million pounds of aluminum; 3 million pounds of copper; and 6,600 pounds of silver.

-

The Market Yawns After Doha

Eddy Elfenbein, April 18th, 2016 at 9:53 amIn the trading pits, oil is down sharply this morning after this weekend’s non-OPEC OPEC meeting.

There’s been a lot of talk about implementing a production freeze, but ultimately, no one could agree on one. The Saudis wanted Iran to go along but the Iranians just got off sanctions so they want to pump at full speed. So for now, there’s no production freeze and world oil should keep on flowing.

Right now, West Texas Crude is going for about $40 per barrel, but it was even lower earlier today.

The market seems to be indifferent. The S&P 500 is currently down about 0.17%. Even most energy stocks don’t seem to care.

-

Morning News: April 18, 2016

Eddy Elfenbein, April 18th, 2016 at 7:11 amGreece’s Latest Bailout Negotiations: Kicking The Can Again

China’s Home-Price Gains Spread as Easing Measures Spur Demand

Rousseff Hangs by a Thread After Losing Impeachment Vote

Oil Prices Drop After Doha Talks Fail to Bring Production Freeze

Gold Boosted by Dollar and Equities After Oil Freeze Fails

Insurers May Leave Obamacare Markets, But Don’t Expect A Mass Exodus

Verily, Truth Telling From China: Donald Trump Is Irrational On Trade

Spain’s CaixaBank Expects To Close Deal For Banco BPI

Verizon Tops Pack of Suitors Chasing Yahoo

The Error In Robert Samuelson’s Tax Proposal

Morgan Stanley Profit Beats Estimates on Stock, Bond Trading

Media Websites Battle Faltering Ad Revenue and Traffic

New McDonald’s Location Will Feature All-You-Can-Eat Fries/a>

Jeff Carter: An Exchange Goes Public

Jeff Miller: Time to Sell the News?

Be sure to follow me on Twitter.

-

Industrial Production Fell 0.6% Last Month

Eddy Elfenbein, April 15th, 2016 at 10:03 amFrom CNBC:

Industrial output decreased 0.6 percent last month after a downwardly revised 0.6 percent drop in February, the Federal Reserve said on Friday. Industrial production has declined in six of the last seven months.

Economists polled by Reuters had forecast industrial production slipping 0.1 percent last month after a previously reported 0.5 percent drop in February.

Industrial production peaked in November 2014. The March report was 3.1% below the peak.

-

60 Straight Quarters of Sales Growth

Eddy Elfenbein, April 15th, 2016 at 9:58 amMarketWatch has an interesting article where it lists 12 companies that have grown their sales every quarter for the last 15 years. But what truly caught my eye was that five of the 12 stocks are on our Buy List.

Here are the twelve, with our Buy List stocks in bold.

Amazon.com (AMZN)

C.R. Bard (BCR)

Biogen Inc. (BIIB)

Cognizant Technology Solutions (CTSH)

Dollar General (DG)

DaVita HealthCare Partners (DVA)

Equinix Inc. (EQIX)

O’Reilly Automotive (ORLY)

Ross Stores (ROST)

Stericycle (SRCL)

Tractor Supply (TSCO)

UnitedHealth Group (UNH) -

CWS Market Review – April 15, 2016

Eddy Elfenbein, April 15th, 2016 at 7:08 am“Doubt is not a pleasant condition, but certainty is absurd.” – Voltaire

Earnings season has begun, and so far, the market seems quite pleased. On Thursday, the S&P 500 closed at its highest point this year. What a turnaround for stocks. The index is up nearly 14% from its February low, and it’s now less than 2.5% from a new all-time high.

On Thursday, Wells Fargo (WFC) was our first Buy List stock to report earnings for this season. The big bank beat Wall Street’s consensus by two cents per share. Wells is continuing to churn out a steady profit despite a tough environment for banks. I’ll have more details in a bit.

Several of our Buy List stocks have been quietly rallying lately ahead of their earnings reports. Stocks like AFLAC (AFL), Stryker (SYK) and CR Bard (BCR) just hit fresh 52-week highs. Other stocks like HEICO (HEI) aren’t far from new highs. The earnings parade is about to get much busier. Next week, we have five Buy List earnings reports including Microsoft (MSFT) and Biogen (BIIB). I’ll preview them later on.

But first, I want to focus on some recent economic news. I realize this sounds like a parody of an economist, but the numbers have been mixed. Some good and some bad. Let’s take a look.

Retail Sales Unexpectedly Tank

Since the Financial Crisis, there’s been a small industry of folks predicting the imminent return of inflation. So far, all those predictions have gone bust. Personally, I try to avoid the macro-forecasting game and instead focus on the numbers.

That’s why I was concerned about the consumer inflation reports for January and February. The headline numbers were quite tame, but the “core” number, which excludes food and energy, started to concern me.

In January, seasonally-adjusted core inflation rose by 0.293% (that’s monthly, not annualized). That may not sound like a lot, and quite frankly, it’s not, but it was the highest in more than nine years. Then in February, the core rate came in at 0.283%, which was the fourth highest in the past nine years.

On Wall Street, two data points count as a trend. Personally, I like to see a little more data, which is why I chose M. Voltaire for today’s epigraph. On Thursday, the government reported that the core inflation rate for March was a tame 0.069%. So there’s no apparent trend. At least not yet.

I wouldn’t mind seeing a bit of inflation. They key part here is “a bit.” It would give the Federal Reserve some more latitude with interest rates. Inflation expectations are very low. As it stands right now, there’s a good chance that the Fed won’t touch interest rates until after the election. I still believe investors are overpaying for risk-averse assets while they’re ignoring assets that are slightly more risky but have much more potential.

Of course, an improving economy needs more shoppers, and that means more people with jobs. The jobs reports have gradually improved, but the best news this week was that the initial jobless report fell to 253,000. That’s the lowest in more than 42 years. Obviously, the country has a lot more people than it did back then. Initial jobless claims have now been below 300,000 for 58 consecutive weeks.

These good numbers are probably due to seasonal factors as much as the jobs market. While the labor picture has improved, there are still many Americans out of work or not even looking for work. There have been some signs of improvement here. The labor-force participation rate finally ticked higher, and wage growth is slowly picking up after a long stretch of flatlining.

I had expected that this would cause more folks to head out shopping. That wasn’t the case. Maybe it was March Madness, but too many people sat at home last month instead of buying things at the mall. On Wednesday, the Commerce Department reported that retail sales fell 0.3% last month. Wall Street had been expecting an increase of 0.1%.

The Atlanta Fed has a cool new estimate of future GDP. They dump tons of numbers into a blender, hit puree, and somehow get an estimate for GDP growth. Right now, they say Q1 real GDP rose by just 0.3%. I had thought their estimate was too pessimistic, but this week’s retail sales report tells me they may be right. We’ll get the first estimates of Q1 GDP on April 28.

Heading into this earnings season, analysts had pared back their estimates by the most since the financial crisis. At the start of the year, Wall Street had been expecting flat earnings for Q1. Now expectations are down 10%. The Wall Street Journal noted that a near-record number of companies in the S&P 500 issued guidance below Wall Street’s expectations. This is expected to be the first earnings season where earnings growth, excluding energy, is negative.

I’m optimistic for our stocks this earnings season because they tend to be much higher quality than the rest of the market. When investors get nervous, they seek out quality. I especially think we’ll see good results from companies like Biogen (BIIB) and Microsoft (MSFT). More on those soon, but first let’s look at this week’s earnings report from Wells Fargo.

Wells Fargo Earns 99 Cents per Share

On Thursday, Wells Fargo (WFC) reported Q1 earnings of 99 cents per share. That was two cents better than Wall Street’s expectations and one penny below my expectations.

There’s not much new to this story. Wells is doing fine, but the environment for banks is choppy. Some bank stocks started to perk up last year. But once it seemed that interest rates would stay lower for longer, the bank stocks got crushed. So far, this has been a terrible year for the big names like JPMorgan Chase, Citigroup and Bank of America.

Going into earnings season, one question mark about Wells was how big was the damage from bum energy loans? The plunging price of crude has wrecked the balance sheets of tons of energy firms, and they owed money to Wells. Now we have some numbers: during Q1, Wells charged off more than $200 million in energy loans. That’s an increase of 75%. The bank also added $200 million to reserves for potential losses. This was the first time they raised reserves in seven years.

The energy loans are an issue, but it’s a small part of their overall business. Last quarter, Wells’s total loan portfolio rose by 10% to $947.26 billion, and commercial loans were up 19% thanks to GE’s commercial lending unit. The bank’s “efficiency ratio” for Q1 was 58.7%. The ratio is expense as a percent of revenues. Wells’s net interest margin is down to 2.9%. I’d like to see that improve, but it’s tough to do in a low-rate world.

Wells also got stung this week when the government rejected its living will. The government has required any of the “too big to fail” banks to explain what they would do in the case of bankruptcy. WFC wasn’t the only bank to have its plan criticized. The CEO has said they’ll work to address whatever issues the government has.

Overall, I think this was a decent quarter for Wells. They’re working their way through some rough seas. The stock is cheap here, but I don’t expect any fireworks. Investors should know that Wells is a stock for the long term. I’m keeping my Buy Below for Wells Fargo at $53 per share.

Q1 Buy List Earnings Calendar

Over the next month, 16 of our 20 Buy List stocks are due to report Q1 earnings. Here’s a handy calendar. I’ve included each stock’s name, ticker, reporting date, Wall Street’s consensus estimate and actual reported result. Please note that some of these dates and numbers are subject to change. This info is the latest I have.

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His