Archive for December, 2016

-

Irrational Exuberance 20 Years On

Eddy Elfenbein, December 5th, 2016 at 8:25 amIt was 20 years ago today that Alan Greenspan made his famous “irrational exuberance” speech. Here’s the money paragraph from that speech:

Clearly, sustained low inflation implies less uncertainty about the future, and lower-risk premiums imply higher prices of stocks and other earning assets. We can see that in the inverse relationship exhibited by price/earnings ratios and the rate of inflation in the past. But how do we know when irrational exuberance has unduly escalated asset values, which then become subject to unexpected and prolonged contractions as they have in Japan over the past decade? And how do we factor that assessment into monetary policy? We as central bankers need not be concerned if a collapsing financial asset bubble does not threaten to impair the real economy, its production, jobs, and price stability. Indeed, the sharp stock market break of 1987 had few negative consequences for the economy. But we should not underestimate or become complacent about the complexity of the interactions of asset markets and the economy. Thus, evaluating shifts in balance sheets generally, and in asset prices particularly, must be an integral part of the development of monetary policy.

It doesn’t seem that dramatic, but at the time, it was taken very seriously. The next day, the Dow dropped 144 at its open. That may not sound like much today, but it was a loss of 2.2%. That’s equivalent to 430 points today. However, the Dow soon recovered some lost ground, and by the closing bell on December 6, it had shed 55 points (all the way down to 6,381.94).

Greenspan’s famous phrase came from Robert Shiller. I can’t confirm if Shiller was referring to his cyclically adjusted price/earnings ratio, also known as CAPE. Instead of using trailing earnings for one year, CAPE goes back ten years.

I’m not a big fan of CAPE. It’s shown the market to be overpriced for almost all of the last 25 years. I’m also not a big fan of trying to time the market based on any valuation measure. The stock market continued to rally for another three years after Greenspan’s speech. Incidentally, Shiller later came out with a book titled Irrational Exuberance.

I get complaints every time I say this, but I’ll repeat that market bubbles are actually quite rare. A bubble is not when p/e ratios go from 15 to 18. A bubble is when they go to 30 and beyond, and the IPO market goes nuts.

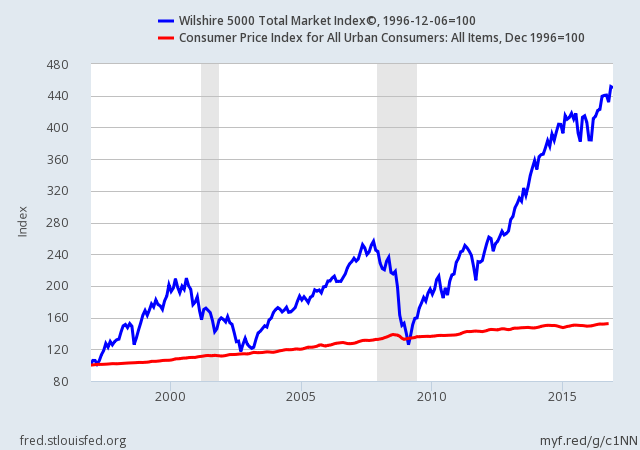

Here’s a look at how the market has done over the last 20 years. This is the Wilshire 5000 Total Return Index, which includes dividends. The red line is the Consumer Price Index:

Since Greenspan’s speech, the total return of the Wilshire 5000 has been 346.5%. That’s 7.77% annualized. I’m reminded of Peter Lynch’s words: “Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.”

-

Morning News: December 5, 2016

Eddy Elfenbein, December 5th, 2016 at 7:07 amOil Advances to 16-Month High as Focus Shifts to Non-OPEC Cuts

British Services PMI Hits 10-Month High, Points to Solid Fourth Quarter Growth

What Italy’s Referendum Means for Monte Paschi

Greenspan’s Irrational Exuberance Looks Entrenched, 20 Years On

How Trump Plans To Punish Firms That Leave US

Trump Advisors Aim to Privatize Oil-Rich Indian Reservations

Silicon Valley’s Culture, Not Its Companies, Dominates in China

Automotive Tech Flying Off the Lot

Aixtron Sees Slim Path to Save China Sale After Obama Order

Hong Kong’s CKI Returns to Australia With $5.4 Billion Bid For Duet Group

SoftBank’s Masayoshi Son Chases First Place With Tech Deals

RBS Will Pay Up to $1 Billion Over 2008 Rights Issue Claims

Israeli Businessman Nochi Dankner Gets Jail Term for Stock Fraud

Josh Brown: Chart o’ the Day: Unemployment Plunges

Howard Lindzon: AngelList and Product Hunt…Smart!

Be sure to follow me on Twitter.

-

How One Trader Made Big Money By Betting on Trump

Eddy Elfenbein, December 4th, 2016 at 9:14 am -

20th Anniversary of “Irrational Exuberance”

Eddy Elfenbein, December 3rd, 2016 at 5:38 pm -

Can GS, UNH & CAT Continue to Drive Dow?

Eddy Elfenbein, December 2nd, 2016 at 4:10 pmFor some reason, my ear thing played a delayed echo of me as I spoke. That’s very hard to speak over. I have newfound respect for television hosts who can manage that, because it’s not easy. I hope I didn’t come across as too awkward.

-

November NFP = 178K, Unemployment Rate Drops to 4.6%

Eddy Elfenbein, December 2nd, 2016 at 9:29 amThe November jobs report shows that 178,000 net new jobs were created last month. The jobless rate fell to 4.6%. Spitting out the decimals, that’s the lowest jobless rate since August 2007.

Average hourly earnings for private-sector workers rose 2.5% in November compared with a year earlier. Wage gains had been accelerating this year as competition for workers intensified. October’s 2.8% was the strongest annual wage growth since June 2009.

The U.S. labor market has been one of the brightest spots in a long recovery marked by sluggish growth. But even with consistent job creation, a historically large share of Americans have opted out of the workforce and wage gains have remained below prerecession levels.

The unemployment rate is lower now than it was for every month from October 1973 to November 1997.

-

CWS Market Review – December 2, 2016

Eddy Elfenbein, December 2nd, 2016 at 7:08 am“The intelligent investor is a realist who sells to optimists and buys from pessimists.”

– Jason ZweigI hope everyone had a great Thanksgiving. On Wall Street, the market gods appear to be thankful for the “Trump Rally,” which continues to roll on. On Thursday, the Dow Industrials closed at yet another all-time high. Over the summer, I said on CNBC that the Dow could hit 20,000 before the end of the year. Brian Sullivan said he should start calling me, Eddy Elfenbull. Now 20,000 doesn’t seem quite so far away.

This is an interesting rally because it’s highly selective. This is an important point investors need to understand. Bonds, for example, have been left behind. During the month of November, the global bond market lost an astounding $1.7 trillion. All across the globe, investors are shifting their assets towards areas of growth. Or perhaps I should say, “towards areas believed to offer prospects for growth.”

In this issue, I’ll tell you what it all means. I’ll also survey some of the recent economic data. As I’ve been saying, the case for modest optimism for the economy continues to be strong. I’ll also bring you up to speed on our Buy List stocks. Remember that I’ll unveil the 2017 Buy List in three weeks. Before we get to that, let’s look at what’s driving the Trump Rally.

The Trump Rally Rolls On

Over a three-week span ending on the Friday following Thanksgiving, the S&P 500 vaulted more than 6.1%. Like the election itself, this was almost completely unexpected. What’s happened is that investors are sharply favoring areas based on robust economic growth. This move is mirrored by a shunning of conservative, income-based assets.

I’ll give you a good example. Over the summer, the Consumer Staples ETF (XLP) reached an all-time high of $56 per share. I love many consumer-staple stocks (like Hormel Foods), but these are areas that tend to flourish when folks get nervous about the economy. After all, when the economy gets weak, people cut back on vacations, not on soap. On Thursday, the XLP closed at $50.25 per share. That’s a 10% drop in a few months during a largely bullish overall market.

On the flip side, banks and financial stocks have been doing very well. Since November 4, the Financial Sector ETF (XLF) is up 17.5%. That’s a huge move for less than one month’s work, but it makes perfect sense. Banks love to see a resurgent economy because it means fewer bum loans. It also means wider yield spreads, which is how the banks make ends meet.

I always think it’s interesting to look at how small-cap stocks are performing. Smaller companies tend to be skewed toward domestic manufacturers. That’s because there aren’t many small-cap conglomerates. The Russell 2000, which is a small-cap index, rallied for 15 days in a row. From November 3 to 25, the index added 16.5%. I think this is clearly a positive omen for the industrial sector. Sure enough, the recent data confirm this. On Thursday, the ISM Manufacturing Index came in at 53.2, compared to 51.8 for October. Any number above 50 means the factory sector of the economy is growing.

Perhaps the best economic news we had this week was the Q3 GDP revision. Now I should add that this is a bit of old news since it deals with the third quarter. Still, we learned that the economy grew by 3.2% during Q3. That’s an upward revision of 0.3%, and it means that last quarter was the U.S. economy’s best in two years.

What about for Q4? That’s hard to say just yet, but we had strong income and spending reports for October. On Wednesday, the government said that personal income rose 0.6% during October. Consumer spending rose by 0.3%, and the figure for September was revised up to 0.7%. The Atlanta Fed now projects that the economy will grow by 2.9% in Q4. Again, I want to be cautious. The economic news is looking better, but we still have a long way to go.

I also have to mention that surprising OPEC news. Apparently, the oil cartel isn’t dead just yet. The always-bickering members actually agreed on a production cut. I was pretty impressed they were able to do that. Of course, who knows how long it will last, or if the members will abide by it?

Still, they’re all smiles now, and the price of oil jumped to $51 per barrel. (To be fair, it’s merely back to where it was a few weeks ago.) Energy stocks, in particular, loved the news. From May 2014 to January 2016, the Energy Sector (XLE) dropped in half. It’s now made back about half of what it lost.

The long end of the bond market has been in rough shape, as yields have climbed steadily higher. In fact, Thursday’s closing yield for some points of the yield curve was the highest in years. The five-year had its highest closing yield (1.90%) since 2011. For the three-year (1.45%), it was the highest since 2010.

Mostly this is a good thing, since it’s shaking money from the bond market, and that money is finding a new home in the stock market. I don’t expect yields to rise too high. The Fed will almost certainly raise interest rates again later this month. After that, they’ll probably hold off for a while. Prices still seem quite tame.

Overall, this is an ideal time to be a stock investor. The economy is getting stronger. Inflation is low. Rates are only beginning to move higher. The earnings picture is getting much better. My advice to investors is to remain concentrated in a portfolio of high-quality stocks such as those you’ll find on our Buy List. They don’t get much more high-quality than our favorite Spam maker and its amazing dividend streak.

Hormel Raised Its Dividend for the 51st Year in a Row

Last week, Hormel Foods (HRL) reported fiscal Q4 earnings of 45 cents per share, which matched Wall Street’s consensus. That’s a nice 22% increase over last, and quarterly revenues rose 9% to $2.63 billion, beating estimates.

“We had a strong finish to fiscal 2016, achieving record earnings for the fourteenth consecutive quarter,” said Jim Snee, president and chief executive officer. “Three of our five business segments delivered sales, volume, and earnings growth, again demonstrating our balanced business model. Refrigerated Foods and Jennie-O Turkey Store both had excellent quarters, with growth coming from value-added, branded products and improved market conditions. Grocery Products enjoyed a strong quarter aided by the inclusion of the JUSTIN’S® specialty nut butter business in addition to strong results from SPAM® luncheon meat and SKIPPY® peanut butter,” Snee said.

“Specialty Foods sales declined, primarily due to the divestiture of Diamond Crystal Brands in May, while sales of MUSCLE MILK® protein products were strong,” mentioned Snee. “Specialty Foods earnings decreased primarily due to increased advertising. Our International segment had a tough quarter as the team continues to work through challenging market conditions in China.”

The Spam maker wrapped up a great year. For 2016, Hormel earned $1.64 per share, compared with $1.32 last year. Hormel also gave 2017 guidance of $1.68 to $1.74 per share. Wall Street had been expecting $1.68 per share.

Hormel also raised its quarterly dividend by 17% to 17 cents per share. That brings its full-year dividend to 68 cents per share. Based on Thursday’s close, that gives the stock a yield of just over 2%. This is Hormel’s 51st annual dividend increase. That’s one of the longest streaks around.

Like other consumer staples, Hormel has been a bit weak lately, but that doesn’t concern me. This week, I’m going to lower my Buy Below on Hormel to $37 per share.

Buy List Updates

Earlier this week, Elliott Management sent a letter to Cognizant Technology Solutions (CTSH) outlining how the company can boost its stock. Elliott said Cognizant could be between $80 and $90 per share by the end of next year. That’s up from $54 right now. You can read the full letter here.

For now, I’ll reserve comment on Elliott’s letter. I will note that many of their criticisms strike me as compliments. They think the company too conservative, with too much cash and too little debt. As I read their letter, I kept thinking to myself, “exactly, that’s why I like CTSH!”

At least the letter gave a nice shot to the share. Cognizant remains a buy up to $57 per share.

Wabtec (WAB) finally completed its merger with Faiveley Transport. The deal cost $1.7 billion. Faiveley has annual sales of $1.2 billion.

Raymond T. Betler, Wabtec’s president and chief executive officer, said: “Our combination with Faiveley Transport brings Wabtec many complementary products, a strong presence in the European and Asia Pacific transit industries, and solid relationships with blue-chip, global customers. Together, we will be a more efficient global competitor, with a focus on technology, quality and customer service, and a singular mission: to help customers improve their safety, productivity, and efficiency.”

Wabtec also updated its guidance. Excluding charges, the company expects to have earnings of $3.95 to $4 per share for 2016. For 2017, WAB expects earnings growth of 8%, excluding charges. Wabtec is a good example of a good company that’s operating well in a terrible environment. I still like this stock a lot. I’m lifting my Buy Below on Wabtec to $90 per share.

Shares of Ford Motor (F) jumped nearly 4% on Thursday after a good sales report for November. At one point, Ford was up 7% on the day. The automaker saw its sales rise 5.2% last month. Ford sold 197,574 vehicles, including more than 72,00 trucks. Higher oil prices could help Ford since the shift to aluminum bodies was designed to be more fuel efficient. Ford remains a buy up to $13 per share.

We only have two Buy List earnings reports this month. HEICO (HEI) is due to report on December 13. Bed Bath & Beyond (BBBY) will report on December 21.

That’s all for now. The November jobs report is due out later this morning, but it won’t have any impact on the Fed’s plans for later this month. Next week will be fairly quiet as far as economic reports are concerned. The productivity report comes out on Tuesday. Consumer credit is on Wednesday. Perhaps the biggest news next week will be the European Central Bank meeting on December 8. The ECB will decide on more stimulus. A lot of folks will be watching this closely. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

P.S. Here’s a video of my appearance on CNBC’s “Halftime Report.”

-

Morning News: December 2, 2016

Eddy Elfenbein, December 2nd, 2016 at 7:04 amRussia Says Foreign Spy Agencies Preparing Cyberattacks on Banks

Offshore Yuan Heads for Best Week Since January as Rates Climb

Italian Assets Show Little Panic Before Vote

With Presidency in Play, Can France Embrace Economic Change?

Brazil’s Braskem Close to Leniency Deal in U.S., Brazil

Trump Threatens ‘Consequences’ For U.S. Firms That Relocate Offshore

Fed May Face Unnerving Shake-Up Under Trump Administration

Aixtron Tumbles as Obama Said Poised to Block Chinese Takeover

Howard Schultz Stepping Down As Starbucks CEO

Wells Fargo to Keep Commissions-Based Retirement Accounts Under Fiduciary Rule

`Never Say Never’: Why A Beloved Silicon Valley Website Sold For $20 Million

Johnson & Johnson Just Got Hit With a $1 Billion Verdict Over Faulty Hip Implants

A Few Billionaires Are Turning Medical Philanthropy on Its Head

Jeff Miller: Stock Exchange: Model Picks Teach Us to Manage Risk

Cullen Roche: Why The US Government Should NOT Refinance the National Debt with Longer Bonds

Be sure to follow me on Twitter.

-

The Rotation to Cyclicals Continues

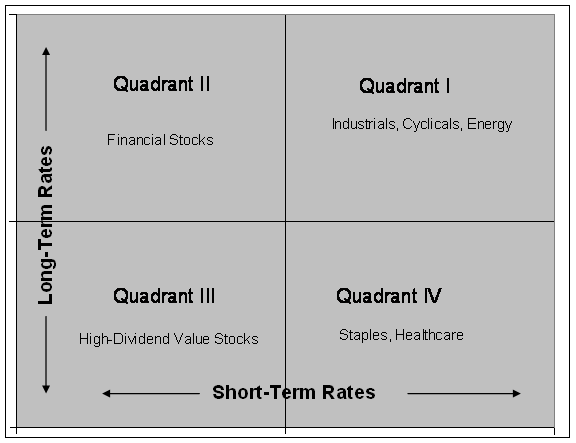

Eddy Elfenbein, December 1st, 2016 at 2:50 pmThe market is still digesting the OPEC news. Banks and energy stocks are up today while tech and income stocks are down. If you recall the “Elfenbein Theory to Explain the Entire Stock Market,” today is a classic Quadrant I & II day.

Bonds are doing poorly and stocks are rotating to cyclical areas.

Ford reported that November was a good month for sales:

Ford’s sales increased 5.2% for the month to 197,574 vehicles, easily beating expectations. That included a 10% increase in retail sales, bolstering the bottom line. The company’s flagship Ford brand was up 4.6%. Its luxury Lincoln brand continued its hot streak, rising 19.1%.

This morning, we also learned that the ISM Manufacturing Index rose to 53.2 last month from 51.9 in October.

-

Morning News: December 1, 2016

Eddy Elfenbein, December 1st, 2016 at 6:57 amGlobal Bonds Suffer Worst Monthly Meltdown as $1.7 Trillion Lost

Euro-Area Manufacturing Picks Up as Weaker Euro Bolsters Exports

Eurozone Unemployment Lowest Since Mid 2009

China Stands to Gain From OPEC Deal

China’s New Tax Could Hurt Ferrari, Aston Martin, and Rolls-Royce

Delinquencies Rise on Growing Volume of Subprime Auto Loans

Wall Street Wins Again as Trump Picks Bankers, Billionaires

Trump’s Treasury Pick Says US Should Get Out of Freddie Mac and Fannie Mae

How Trump Plans to Keep Jobs in America: Pressure and Promises

Court Rules IRS Can Seek Information on Bitcoin Customers

Though Awash in Fakes, China Rethinks Counterfeit Hunters

Netflix Allows Subscribers to Binge-Watch Shows Offline

ChemChina Setting Up $5 Billion Fund to Help Finance Syngenta Bid

Jeff Carter: If You Are A Bitcoin Developer, Don’t Walk, Run To Chicago

Be sure to follow me on Twitter.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His