Archive for January, 2017

-

Volatility Now Versus the Summer

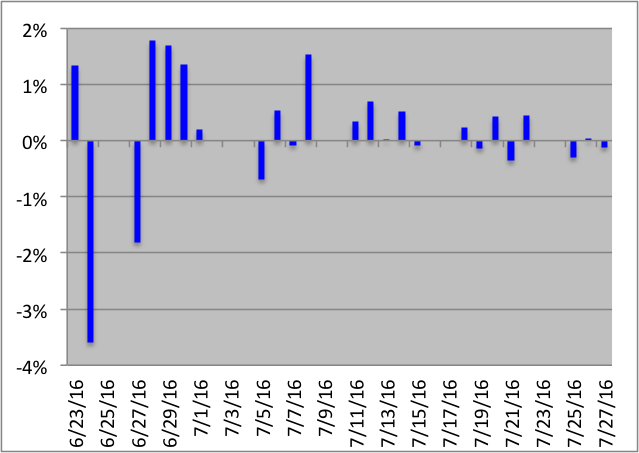

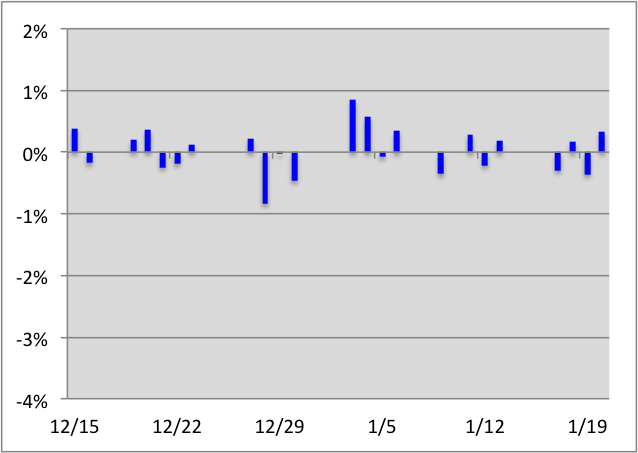

Eddy Elfenbein, January 23rd, 2017 at 11:32 amIt’s hard to describe how low the market’s volatility is. Here’s another way to see it. This is the daily changes of the S&P 500 over the last 24 days compared with a 24-day stretch from the middle of last year. I’ve used the same vertical axes.

Here’s last summer:

And this is now:

-

FLOTUS and AFLAC

Eddy Elfenbein, January 23rd, 2017 at 11:18 amHere’s an ad from one of our Buy List stocks featuring the new First Lady of the United States:

-

Morning News: January 23, 2017

Eddy Elfenbein, January 23rd, 2017 at 7:04 amChinese Banks Told To Issue Dollar-Denominated Debt-Sources

Japan’s PM Says Will Keep Seeking Trump’s Understanding on TPP

OPEC and Friends Agree on Way to Monitor Oil Cut to End Glut

Kuwait State Oil Company Says Onshore Oil Leak Contained

Chevron Slams Canadian Backdoor in $9.5 Billion Pollution Fight

The Rising Risk of Central Bank Instability

HUD Suspends FHA Mortgage Insurance Rate Cut An Hour After Trump Takes Office

Retail Malaise Puts Pressure on Chains to Shutter More Stores

AIG to Pay Buffett’s Berkshire About $10 Billion In Insurance Deal

Xiaomi, Chinese Phone Maker, Losing Its Global Face as Hugo Barra Exits

Apple-Supplier Foxconn Weighs $7 Billion U.S. Display Plant

Japan’s First Jet Delayed Again Raising Concerns About New Sales

Snapchat Discover Takes a Hard Line on Misleading and Explicit Images

Jeff Miller: Will Policy Uncertainty Increase Stock Volatility?

Howard Lindzon: Post Alt Fact World

Be sure to follow me on Twitter.

-

CWS Market Review – January 20, 2017

Eddy Elfenbein, January 20th, 2017 at 7:08 am“Obama’s Radicalism Is Killing the Dow” – WSJ, 13,000 Dow Points Ago

Dear Lord, this has been a dull, dull, dull market. The S&P 500 has now gone six weeks without having a single daily move, up or down, of more than 1%. Compare that to last summer, when we had six straight days of moves greater than 1%.

The Trump Rally has apparently given way to the Ambien market. Folks, Wall Street is fast asleep. Here’s a stat for you: Since December 12, the Dow has closed every single day within a range of 230 points. That’s a little over 1%. You can expect that kind of range for one day, but over a month?

Things may change soon. Fourth-quarter earnings season is under way, and we’ve already had our first Buy List earnings report. Signature Bank beat consensus estimates by two cents per share. This bank has had a phenomenal rally since the election, but, like everybody else, it’s chilled out. I’ll go over the earnings report in a bit.

I’ll also preview the five earnings reports coming our way next week. But first, let’s look at why the Ambien market may not last, and why I’m cautious about stocks over the next few weeks.

Expect a Rougher Market This Winter

The new president is going to be sworn in in a few hours. Whenever there’s a new president, you’ll hear lots of breathless commentary about how he’ll ruin or save Wall Street. I tend to shy away from these predictions (see this week’s epigram). As Warren Buffett said, forecasts tell you more about the forecaster than they do about the future.

Having said that, I think the market is looking tired right now. The Dow ran into 20,000 and could go no further. Let me be clear: I’m hardly forecasting doom. Rather, I think some minor pullbacks are in order over the next few weeks. Nothing to be too concerned about. In fact, I would expect our stocks to weather any storm better than the overall market.

This is a key moment for the economy. Next week, we’re going to get our first look at the fourth-quarter GDP report, and I think it will be a good one. The report for Q3 was 3.5%, but here’s the thing—the U.S. economy has had a difficult time stringing together two or three good quarters in a row. I think this is our best chance to break that.

This week, for example, we learned that industrial production grew by 0.8% last month. That’s quite good. That beat expectations, and it was the biggest increase in more than two years.

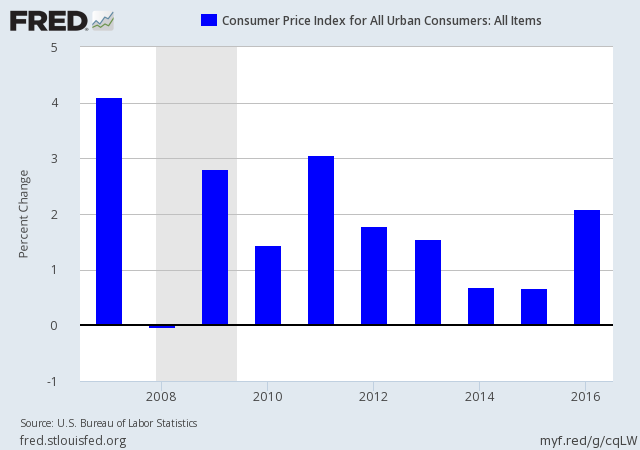

We also got another CPI report telling us that inflation is well contained. The news reports noted that inflation rose by 2.1% last year, which was the largest increase in five years. Well, yes, that’s correct, but it glides over the fact that we came close to deflation over those five years. So this year, inflation has climbed all the way to “low.” This is another reason I doubt the Fed will raise interest rates three times this year.

This week’s Fed’s Beige Book said that labor markets are getting “tight.” That’s econo-talk for “workers want more money.” They may get it. The initial claims report came within a whisker of touching its lowest point since the Nixon administration. Plus, last Friday, the Census Bureau released a decent retail-sales report for December. On Wednesday, Janet Yellen said the economy is close to full employment.

I prefer to listen to the market’s opinion over that of economists, and I’m pleased to see the bond market pull back some. It shouldn’t be too easy for bond investors to outpace stock investors. The bond folks need to be kept on their toes. The 10-year yield got up to 2.5% this week. That’s about double the yield from six months ago. This is part of an ongoing rotation as money leaves safe assets and is gradually finding a home in riskier ones. That could be a major theme this year.

Now let’s look at our first Buy List earnings report for Q4.

Signature Bank Earned $2.11 Per Share

On Thursday, before the opening bell, Signature Bank (SBNY) reported Q4 earnings of $2.11 per share. That was two cents more than Wall Street’s consensus. Overall, this was another good quarter for Signature.

For the year, the bank earned $7.37 per share. That was only 10 cents more than 2015’s total, but remember that they took a 70-cent charge in Q3 related to their medallion loans. Still, they were to top 2015’s result, which made 2016 their ninth record year in a row. The numbers for last year were pretty impressive. Total deposits grew 19% on the year. The key stat I like to watch is net interest margin, and that came in at 3.30%. That’s quite good.

I was also pleased to see Signature improve its fiscal condition this year by raising money from the capital markets. They had a common stock offering that brought in $320 million, plus a debt offering that took in $260 million.

Signature Bank Chairman of the Board Scott A. Shay, noted: “Signature Bank has produced yet another record year of earnings and solid financial performance. We are proud that — even from the depths of the financial crisis — we maintained a rapid growth pace while remaining a pillar of strength for our clients during those uncertain times.

“As the Bank continues to grow, we retain our strong discipline and follow the hedgehog theory of business – doing a few things, but doing each of them very well. In our case, that means maintaining our unrelenting commitment to depositor safety and service and conservative lending posture. We look forward to the New Year and to embracing many opportunities as we have built a platform poised to serve an expanding roster of clients,” Shay concluded.

Shares of SBNY weren’t doing much until the election. Then, out of the blue, the stock jumped 21% in four days. It’s always interesting how stocks can suddenly rally right about when you’ve given them up for dead. Once SBNY got to $150 per share, the rally started to peter out, and that’s about where the stock is today. I continue to rate Signature a buy up to $165 per share.

Next Week’s Buy List Earnings Reports

Stryker (SYK) is due to report its Q4 earnings on Tuesday, January 24. The orthopedics company had a good earnings report in October. In fact, they felt confident enough to raise the low-end of their full-year guidance by five cents per share. Stryker now expects 2016 earnings to range between $5.75 and $5.80 per share. That translates to Q4 results of $1.73 to $1.78 per share.

I’ll be curious to hear their forecast for 2017. Wall Street expects $6.39 per share. I suspect Stryker will offer conservative guidance.

Just a reminder that one year ago, Stryker said to expect 2016 earnings of $5.50 and $5.70 per share, and they’ll clear that with room to spare. This is why we like high-quality stocks. Here’s the annual EPS trend for Stryker: $2.95, $3.33, $3.72, $4.07, $4.23, $4.73, $5.12, and $5.75 to $5.80 for last year. That’s very impressive.

On Tuesday of this week, Alliance Data Systems (ADS) said it stands by its 2016 FY forecast of $16.90 per share in core earnings on revenue of $7.2 billion. That translates to Q4 guidance of $1.9 billion in revenue and core EPS of $4.64. My numbers say that sounds about right. ADS will report its earnings on Thursday, January 26.

CR Bard (BCR) has enjoyed a few upgrades recently from Wall Street. I started to get very bullish on this stock during the fall. On CNBC, they asked me for a candidate to beat earnings for Q3, and I said CR Bard. The company gave guidance of $2.51 to $2.55 per share, and I said that was too low. I was right. Bard made $2.64 per share, but the stock didn’t start to rally until last month.

Bard also increased their 2016 EPS range to $10.23 – $10.28 per share. That implies Q4 earnings of $2.70 to $2.75 per share. Keep an eye on my $230 Buy Below price. Don’t chase BCR. I’ll raise my Buy Below if the numbers are strong.

Microsoft (MSFT) also reports on Thursday. Not much to add about the software giant. The company has been churning out very good earnings. They beat the Street three months ago by eight cents per share. The consensus on Wall Street is for 78 cents per share. The stock has had a very good run over the last six months.

Sherwin-Williams (SHW) is one of our new stocks this year. The company gave a Q4 range of $2.13 to $2.23 per share; Wall Street expects $2.21.

Buy List Updates

Good news for Moody’s (MCO). The credit-ratings agency has agreed to pay $864 million to settle with the government over its ratings leading up to the financial crisis. The agreement calls for Moody’s to pay $437.5 million to DOJ and $426.3 million to the states. The news helped the stock bounce above $100 per share, despite being downgraded by UBS and Barclays last week.

Barclays struck again. This time, they downgraded Cerner (CERN). Interestingly, Cerner was one of our worst-performing stocks last year, and it’s our best so far this year. Weird how that happens! Earnings are due out on February 9.

SunTrust initiated coverage on HEICO (HEI) with a buy rating and a price target of $85. Also, Institutional Investors named HEICO’s CEO, Laurans Mendelson, the best CEO in defense/aerospace.

Deutsche Bank initiated coverage on Danaher (DHR) with a Buy rating. They gave the stock a price target of $88 per share.

That’s all for now. The news next week will probably be dominated by earnings news, but there will be some key economic reports. The most important will be the first look at Q4 GDP. Growth for Q3 was 3.5%, but we’ve had a lot of difficulty getting two good quarters back to back. Let’s see if we can do it this time. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: January 20, 2017

Eddy Elfenbein, January 20th, 2017 at 6:00 amDavos Elites See an `Abyss’: The Populist Surge Upending the Status Quo

China’s Growth in 2016 Slumps as Trump Trade Struggle Looms

Yellen Backs Gradual Rate Rises as Fed Not Behind the Curve

Steven Mnuchin, Treasury Nominee, Failed to Disclose $100 Million in Assets

Soros Says Markets to Slump With Trump, EU Faces Disintegration

IBM Posts Earnings Beat In Q4 And Raises Guidance For 2017, But Stock Plunges

Netflix Beats Subscriber Count Target By 36% As Growth Strategy Pays Off

Uber to Pay $20 Million to Settle FTC Charges on Earnings Claims for Drivers

Heineken in Discussions With Kirin to Double Down in Brazil

Telecommunications Company Avaya Files for Bankruptcy

Robot Crop Pickers Limit Loss of U.S. Farm Workers to Trump Wall

ChemChina Seeks U.S. Anti-Trust Approval for Syngenta Deal

Josh Brown: QOTD: Bob Shiller on the Trump Illusion

Jeff Carter: Venture Capital Is The Red Headed Stepchild, But It Shouldn’t Be

Be sure to follow me on Twitter.

-

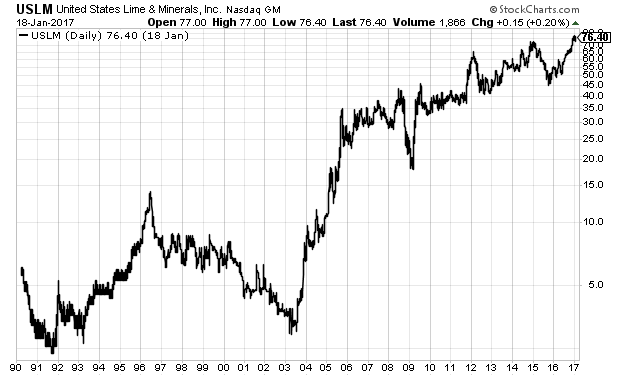

United States Lime & Minerals

Eddy Elfenbein, January 19th, 2017 at 12:35 pmIf you’ve followed me for some time, you know that I have a soft spot for small, not well-known stocks that have performed very well.

Here’s another good example—United States Lime & Minerals (USLM).

Fourteen years ago, USLM was going for $3 per share. Today it’s at $77. So how many analysts follow it? Zero.

The stock has a market cap of $425 million. I also have to say that I love that name.

So what do they do? From their website:

United States Lime & Minerals, Inc. (“US Lime”) is a public company traded on the NASDAQ Global Market® under the symbol USLM and conducts its business through two segments:

Lime and Limestone Operations and Natural Gas Interests.

The Lime and Limestone Operations manufactures lime and limestone products, supplying primarily the construction (including highway, road and parking lot contractors), metals (including steel producers), environmental (including municipal sanitation and water treatement facilities and flue gas treatment), oil and gas services, industrial (including paper and glass manufacturers), roof shingle and agriculture (including poultry and cattle feed producers) industries. The company is headquartered in Dallas, Texas, and primarily serves markets in the Central United States and consists of open-pit quarries and an underground mine, plants and distributions facilities owned by US Lime’s wholly owned subsidiaries: Arkansas Lime Company, Colorado Lime Company, Texas Lime Company, U.S. Lime Company, U.S. Lime Company — Shreveport, U.S. Lime Company — St. Clair and U.S. Lime Company — Transportation.

Through its wholly owned subsidiary, U.S. Lime Company — O & G, LLC (“U.S. Lime O & G”), under a lease agreement (the “O & G Lease”), US Lime has royalty interests ranging from 15.4% to 20% and a 20% non-operating working interest, resulting in an overall average revenue interest of 34.8%, with respect to oil and gas rights in wells drilled on approximately 3,800 acres of land located in Johnson County, Texas, in the Barnett Shale Formation. Through U. S. Lime O & G, US Lime also has a drillsite and production facility lease agreement and subsurface easement (the “Drillsite Agreement”) relating to approximately 538 acres of land contiguous to Johnson County, Texas, property. Pursuant to the Drillsite Agreement, US Lime receives a 3% royalty interest and a 12.5% non-operating working interest in any wells drilled from two pad sites located on the property.

Not too sexy, but they make money. Don’t expect to hear a lot about this one on TV or in the newspapers. USLM is about as dull as they get. About the only time they make news is when they release their quarterly earnings, and no one seems to pay too much attention to that.

-

Signature Bank Earned $2.11 Per Share for Q4

Eddy Elfenbein, January 19th, 2017 at 11:57 amThis morning, Signature Bank (SBNY) reported Q4 earnings of $2.11 per share. That was two cents more than Wall Street’s consensus. Overall, this was another good quarter for Signature.

The bank earned $7.37 per share for the year. That was only 10 cents more than 2015’s total, but remember they took a 70-cent charge related to their medallion loans. Still, they were to top 2015’s result which made 2016 their ninth record year in a row. Total deposits grew 19% on the year. The key stat is net interest margin and that came in at 3.30%. That’s quite good.

The bank also improved its fiscal condition this year by raising money from the capital markets. They had a common stock offering that brought in $320 million, plus a debt offering that took in $260 million.

Signature Bank Chairman of the Board Scott A. Shay, noted: “Signature Bank has produced yet another record year of earnings and solid financial performance. We are proud that — even from the depths of the financial crisis — we maintained a rapid growth pace while remaining a pillar of strength for our clients during those uncertain times.

“As the Bank continues to grow, we retain our strong disciplines and follow the hedgehog theory of business – doing a few things but doing each of them very well. In our case, that means maintaining our unrelenting commitment to depositor safety and service and conservative lending posture. We look forward to the New Year and to embracing many opportunities as we have built a platform poised to serve an expanding roster of clients,” Shay concluded.

Shares of SBNY weren’t doing much until the election. Then the stock jumped 21% in four days. The rally started to peter out once SBNY got to $150 per share, and that’s about where the stock is today.

-

Morning News: January 19, 2017

Eddy Elfenbein, January 19th, 2017 at 6:51 amChina Says Can Resolve Trade Disputes With New U.S. Government

As E.C.B. Meets, Monetary Policy Faces Complications Worldwide

May’s Speech to the 2017 World Economic Forum

Treasury Yields Rise on Yellen’s Hawkish Tone

A Border Adjustment Tax Threatens Disruption For U.S. And Its Neighbors

Safran to Buy Zodiac for $10 Billion in All-French Aero Deal

Goldman Exodus Isn’t Just About Trump

How Deutsche Bank Made −€367 Million Disappear

Here’s Why Netflix’s Share Price Just Hit a New All-Time High

Australia to Welcome Back Vegemite, a Surprisingly American-Owned Spread

JPMorgan Hit With Pair of Bias Claims in Obama’s Final Hours

Mallinckrodt Will Pay $100 Million to Settle Price-Hike Suit

Student Loan Collector Cheated Millions, Lawsuits Say

Jeff Miller: Neglected Investment Ideas

Roger Nusbaum: Tweets & Press Conferences

Be sure to follow me on Twitter.

-

Industrial Production and Inflation

Eddy Elfenbein, January 18th, 2017 at 3:24 pmTwo econ reports to pass along.

The first is that the Fed said that industrial production rose by 0.8% in December. That’s a strong number. It was the best in two years.

Manufacturing output, the biggest component of industrial production, climbed 0.2% in December, led by gains for primary metals and autos.

Factory activity had been stagnant for much of 2016 but appears to have perked up a little in the final month of 2016. Still, a long stretch of lackluster growth left December output only 0.2% ahead of the same month a year ago.

A separate gauge of manufacturing finished 2016 at its highest mark in two years. The Institute for Supply Management earlier this month said its purchasing managers index rose amid stronger household demand for goods and a brighter consumer outlook following November’s presidential election.

This caused some pain for the long-end of the bond market, and I think that’s a good thing. A month ago, the 10-year yield broke above 2.6%. It’s now back around 2.4% but I’d like to see it rise again.

At the shorter end, inflation continues to be quite tame. The government said that the CPI rose by 0.3% last month while the core rate rose by just 0.2%. For the year, the CPI rose by 2.1%. That’s the highest rate since 2011, but that’s because the other years were so low.

With today’s CPI report we have some final numbers for 2016:

S&P 500 +9.54%

S&P 500 Total Return Index +11.96%

CPI +2.07%

Real S&P 500 +7.31%

Real Total Return Index +9.68% -

Morning News: January 18, 2017

Eddy Elfenbein, January 18th, 2017 at 5:47 amThe Risks of ‘Brexit Means Brexit’

Loonie in Hottest Streak Since 1970 as U.S. Dollar Retrenches

Brainard Joins Fed Chorus Warning About Fiscal Stimulus Risks

Why Trump’s Tariff Threats Get Taken So Seriously

Treasury Pick Steven Mnuchin, Like His Would-Be Boss Donald Trump, Followed His Own Rules

Land Rush in Permian Basin, Where Oil Is Stacked Like a Layer Cake

Reynolds Board Accepts Increased BAT Offer of $49.4 Billion

HPE to Acquire Data-Storage Startup SimpliVity for $650 Million in Cash

Deutsche Bank CEO Looks to Future After Mortgages Settlement

Restaurant Chain Chuck E. Cheese Prepares IPO

Sears Clings to Catalog Thinking in an Online World

Bad Behavior Database Aims to Stop Rogue Traders Before They Act

Jeff Carter: If You Don’t Understand Blockchain Or Think It Won’t Apply To You; Read This

Howard Lindzon: The Dumb Multitasker?

Be sure to follow me on Twitter.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His