Archive for April, 2017

-

Express Scripts CEO Defends PBMs

Eddy Elfenbein, April 11th, 2017 at 1:03 pmHere’s a brief clip of the CEO of Express Scripts (ESRX) defending PBMs from the allegation that they’re responsible for high drug prices.

-

When Europe Leads, Here’s What Happens

Eddy Elfenbein, April 11th, 2017 at 12:55 pm -

Oppenheimer Knocks Alliance Data Systems

Eddy Elfenbein, April 11th, 2017 at 11:39 amThis morning, Oppenheimer initiated coverage on Alliance Data Systems (ADS) with an underperform rating. That seems to have knocked the shares down more than 4%. (I’m not aware of any other news that would have impacted the stock.)

The company is due to report earnings on April 20. Wall Street expects earnings of $3.89 per share.

-

JFK Attacks the Steel Industry

Eddy Elfenbein, April 11th, 2017 at 10:25 amFifty-five years ago tomorrow, President Kennedy attacked the steel industry. Gary Alexander explains the fallout.

Fifty-five years ago this week, on April 12, 1962, President John Kennedy held a special press conference to demand that the executives of U.S. Steel (and many other domestic steel companies) roll back their recently-announced $6 per ton price increase. He accused steel executives of being virtually traitorous in their “pursuit of private power and profit.” He said that the Department of Defense would only order steel from the firms that rolled back prices. Steel companies quickly complied, rolling back prices the next day.

By the next day, Friday the 13th of April 1962, the nation’s eight biggest steel companies surrendered to the President’s demands in quick succession: At 3:05 pm, Kaiser Steel was the first domino, followed by Bethlehem Steel at 3:21. U.S. Steel bowed at 5:25, followed by Republic Steel (5:57), Pittsburgh Steel (6:26), Jones & Laughlin (6:37), National Steel (7:33), and finally Youngstown Sheet & Tube (at 9:09).

That did not end the war of words. When it came time to announce U.S. Steel’s disappointing first-quarter 1962 earnings on May 7, CEO Roger Blough told his shareholders: “This concept is incomprehensible to me – the belief that Government can ever serve the national interest in peacetime by seeking to control prices in competitive American business, directly or indirectly, through force of law or otherwise.”

All through May of 1962, stocks kept falling. From its December 1961 peak at 741, the Dow fell by 29% in six months, to 525 by late June, 1962. It turned out to be the worst bear market to befall America in the 32-year expansion between 1942 and 1974. May 28, 1962 was the worst day on Wall Street since the 1929 crash. On that day, steel stocks dropped to 50% of their 1960 levels, as part of a long, long decline.

Steel companies weren’t price-gouging. Profits at U.S. Steel fell 61% from 1958 to 1963, with the biggest drop coming in 1962. The industry lost over 100,000 jobs from 1958 to 1960, including 70,000 jobs lost at U.S. Steel alone. Their profit margin was cut in half. While salaries in the steel industry rose 13% from 1958 to 1961, profits fell, as 85% of U.S. Steel’s 1961 profits were paid out in shareholder dividends.

In 1958, U.S. Steel was #4 in the Fortune 500, and Bethlehem Steel was #9. By 1985, U.S. Steel was in the process of changing its mix of businesses, emerging as USX Corp. The only pure steel company in the Fortune 100 in 1985 was Bethlehem Steel, ranked #68. Clearly, the U.S. steel industry was slowly dying.

The President killed an already-dying industry. By July 1962, the steel industry was working at just 55% capacity, vs. 70% in April, when the President attacked them. Very soon, Japan began to dominate the steel market, which was already beset by competition from non-steel construction products made from plastics, aluminum, cement, or glass. While the normal challenges of business are always present, the President’s attack contributed greatly to the decline of the U.S. steel industry over the next few decades.

As history shows, Presidents possess great powers to inspire or destroy when they propose to take any particular industry to the woodshed. Chances are, market forces are already disciplining those companies.

-

Morning News: April 11, 2017

Eddy Elfenbein, April 11th, 2017 at 7:07 amChina Is Playing a $9 Trillion Game of Chicken With Savers

Yellen Signals Shift From Stimulating Economy to Sustaining Growth

Trump Takes Credit for Planned $1.33 Billion Toyota Spending

Google is Fighting The Labor Department About Equal Pay For Women, And Both Can’t Be Right

AT&T Bets On 5G With Straight Path Communications Buy For $1.25 Billion

Seven Wells Fargo Managers in Board’s Review—and Their Fates

Toshiba Files Earnings Without Auditor Endorsement, Delisting Risk Rises

Toshiba Casts Doubt on Its Ability to Stay In Business

G.M. Takes a Back Seat to Tesla as America’s Most Valued Carmaker

Whole Foods’ Shareholder Battle Sets Up a Clash of Foodie Gurus

Vizio’s $2-Billion Sale to LeEco Called Off Over ‘Regulatory Headwinds’

Why Delta Air Lines Paid Me $11,000 Not To Fly To Florida This Weekend

Scammers Used SeekingAlpha for Bogus Stock Promotions, SEC Says

Roger Nusbaum: Blame It On The Rain

Josh Brown: Some Questions for the Bank CEOs

Be sure to follow me on Twitter.

-

The Best Retail Stocks to Buy Now

Eddy Elfenbein, April 10th, 2017 at 7:54 pm -

Tesla Surges on Upgrade

Eddy Elfenbein, April 10th, 2017 at 5:52 pm -

Morning News: April 10, 2017

Eddy Elfenbein, April 10th, 2017 at 6:54 amChina Insurance Probe Won’t Halt Firms’ Overseas Urge

Oil Surplus or Scarcity? Shale Makes It Even Harder to Predict

Geopolitics From France to Korea Keep Investors Cautious

Impressive Market Resilience Shouldn’t Be Taken for Granted

Trump-Taxes: President Scraps Tax Plan, Timetable Threatened

FCC Chief Ajit Pai Develops Plans to Roll Back Net Neutrality Rules

Battle of Billionaires: Son Set to Clash With Bezos in India

How Steven Colbert Finally Found His Elusive Groove

Women At Google Face ‘Extreme, Systemic’ Wage Gap, According To Labor Dept. Suit

Fox News Troubles Heighten Scrutiny of Rupert Murdoch’s Plan to Acquire Sky

LIBOR: Bank of England Implicated in Secret Recording

Barclays Reprimands Chief Executive For Trying To Identify Whistleblower

Jeff Miller: Will an Earnings Surge Revive the Stock Rally?

Howard Lindzon: The Insurance Boom in Fintech, Street Contxt and Bloomberg Terminal Rivals

Be sure to follow me on Twitter.

-

March 2017 NFP = 98,000

Eddy Elfenbein, April 7th, 2017 at 8:31 amThe March jobs report is out. The U.S. economy created 98,000 net new jobs last month. That’s well below expectations of 180,000, but the unemployment rate fell to 4.5%.

Manufacturing gained 11,000 jobs, but retail lost nearly 30,000 jobs.

For me, the key number is average hourly earnings. That rose by 0.2% in March. In the last year, AHE is up 2.7%.

Here’s a chart of NFP.

The unemployment rate is lower now than at anytime between March 1970 and April 1998.

12-month gain average hourly earnings.

-

CWS Market Review – April 7, 2017

Eddy Elfenbein, April 7th, 2017 at 7:08 am“The stock market is designed to transfer money from the active to the patient.”

– Warren BuffettThe stock market has apparently reverted to its tame ways. For the last eight days in a row, the S&P 500 has closed between 2,352 and 2,369. That’s a fairly narrow range. Last week, I thought we might see some action when the S&P 500 briefly dipped below its 50-day moving average. That hadn’t happened since November, but the index failed to close below this crucial technical support level.

So the boring market has continued.

Even though the stock market peaked over a month ago, there hasn’t been much momentum in either direction. But there was some interesting news from Washington this week. We learned that the Federal Reserve is finally considering ways to reduce its gargantuan balance sheet. This could be an important issue later this year. I’ll tell you what it means.

Now we’re in April and first-quarter earnings season is about to begin. This could be one of the better quarters in recent years. I’ll tell you what to expect. I’ll also discuss this week’s earnings report from RPM Inc., plus I have some other Buy List updates for you. But first, let’s look at what the Fed has planned in order to unwind its gigantic balance sheet.

Don’t Panic Over the Fed’s Balance Sheet

On Wednesday, the Federal Reserve released the minutes from last month’s policy meeting. This is the one where the Fed decided once again to raise interest rates. This was a notable increase because it wasn’t foreseen a month beforehand. By the time it happened, it wasn’t a surprise. But for those key weeks, the expectations completely changed. I think Wall Street was surprised by how forceful and direct the Yellen Fed could be.

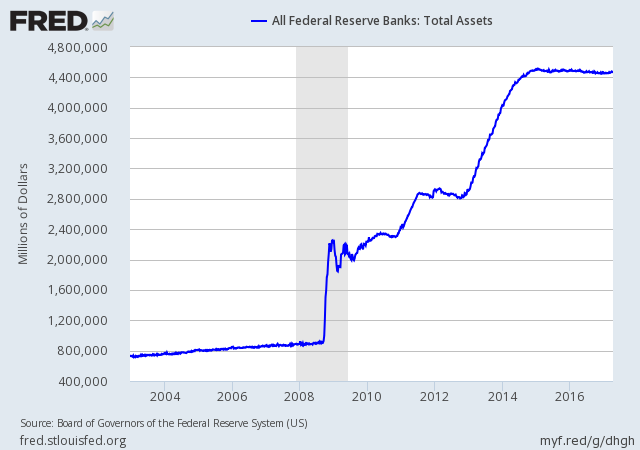

The Fed has become pretty good at conveying its intentions to Wall Street. But that’s regarding interest rates. What about the Fed’s balance sheet? Before the world economy went kablooey nine years ago, the Fed’s balance was less than $1 trillion. Then the Fed got busy. Very, very busy. Today, the balance sheet is $4.5 trillion.

As you might expect, this is a wee bit disconcerting for investors and folks inside the government. The problem is that if the Fed moves too quickly and dumps its holdings, that could cause long-term interest rates to rise. The Fed has been reinvesting the proceeds of its securities, but that could end soon. According to the minutes from the March meeting, “Provided that the economy continued to perform about as expected, most participants anticipated that gradual increases in the federal funds rate would continue and judged that a change to the Committee’s reinvestment policy would likely be appropriate later this year.”

As always, I apologize for quoting Fed officials. Despite their dull writing, this is actually a big honking deal. First off, let’s make the important point that the Fed will keep using interest-rate adjustments as its main policy tool. For its balance sheet, almost certainly, the plan will be to deflate it slowly and quietly. We don’t want a repeat of Wall Street’s “Taper Tantrum” in 2013. My guess is that the first step will be a decision to end reinvestment of agency debt, not Treasury debt.

As we know, the bond market is notoriously ornery. Yes, they’ll scream and holler every step of the way. But ultimately, I doubt the Fed’s plans will have a sizeable impact on long-term rates. There’s simply too much demand from investors all over the world to hold U.S. debt. Plus, there’s no hurry for the Fed to lower its holdings. If need be, they can wait out a storm.

Instead, my fear is that the Fed will raise rates too much too fast. Looking at the data, there’s not a great need for higher rates. Later today, we’ll get the jobs report for March. We’ll see more job gains. I hope we’ll see more improvement in wages, but we have a long way to go. Inflation is still not a problem. While oil has moved up recently, it’s down for the year.

Eric Rosengren, the top dog at the Boston Fed, recently said he thinks the Fed needs four hikes this year. I’m sorry, but I just don’t get it. Maybe one more raise this year. Outside chance of two more. The problem, of course, is that just because it’s a bad idea doesn’t mean the Fed won’t do it.

In the last year, long-term rates have gapped up significantly, and I’m starting to question how much of that is truly justified. I wouldn’t be surprised to see the yield on the 10-year Treasury fall back below 2%. Of course, much of this outlook is dependent on where the economy goes from here. Very soon, we’re going to get a slew of earnings reports. Let’s take a closer look at what Q1 earnings season has in store.

Preview of Q1 Earnings Season

According to the latest estimates, Wall Street expects earnings growth of 9.1% for Q1. What helps that figure is the comparison against weak numbers from a year ago. Still, if the forecast is correct, that would be the fastest growth rate since Q4 of 2011. Bank of America Merrill Lynch noticed a fascinating factoid. In company earnings calls for Q4, 52% of companies used the word “optimistic.” That’s the highest ever in data going back to 2003.

Another welcome change is that earnings estimates haven’t been slashed as they’ve been in previous quarters. It’s the norm to expect Wall Street’s forecasts to be pared back as earnings season approaches, but it’s been far more muted this time.

This earnings season will also be different because we’ll see better results from energy companies. The downturn in oil was brutal for many earnings stocks, but prices have rebounded. Typically, the big banks report early on in the earnings season. That often sets the tone for the rest of the earnings. Our own Signature Bank (SBNY) is due to report on April 17.

We’re also seeing decent topline growth. The early part of the bull market was often criticized for being driven by cost-cutting. Companies were growing their profits but not growing their firms. They were just laying off people. At some point, we needed to see more customers come in and buy more things. We’re now seeing more jobs leading to more spending leading to higher revenue. Wall Street currently expects Q1 revenue growth of 7.1%. That will be a five-year high. Not surprisingly, we recently saw consumer confidence touch a 16-year high.

We’re also somewhat safer now from an issue in previous quarters, namely the strong U.S. dollar. The greenback soared after the election, but it has pulled back since the start of the year. Last year, you may recall how often companies stressed that their “currency-adjusted” profits were doing just fine.

I’m particularly looking forward to the earnings report from Microsoft (MSFT). Wall Street currently expects earnings of 70 cents per share from the software giant. They should have little trouble topping that. Now let’s look at the only Buy List earnings report we’ve had in five weeks.

RPM Inc. Is a Buy Up to $55 Per Share

On Thursday, RPM Inc. (RPM) reported fiscal third-quarter earnings of nine cents per share. That result, however, includes five cents per share related to the company’s “Restore intangible impairment and the European facility closure.” Looking past that, RPM made 14 cents per share, which was three cents better than estimates.

I should explain that RPM is on the February/May/August/November reporting cycle. As such, they’re one of our few Buy List earnings reports over the last several weeks. Since most of our stocks (and most stocks in general) ended their last quarter in March, we’ll see a flurry of earnings reports soon.

RPM’s earnings report is a bit unusual because only a very small portion of its annual profit comes during their fiscal Q3. By my rough estimate, Q3 makes up about 5% to 7% of RPM’s full-year haul. The company expects full-year earnings to range between $2.57 and $2.67 per share. That’s a reduction of five cents per share from their previous forecast due to charges I mentioned before. Quarterly revenue rose to $1.02 billion, which was just shy of estimates of $1.04 billion.

“Our businesses serving the U.S. commercial construction market again experienced solid organic growth. Most businesses in Europe were up in the low- to mid-single-digit range in local currencies, and current-year acquisitions contributed nicely to the segment’s overall sales growth. We were very pleased with the strong EBIT leverage achieved on solid top-line sales,” stated Sullivan.

RPM is a good example of a solid company that’s having a sluggish year. The key takeaway is that profits will be about the same as last year. There’s no reason to run. The shares pulled back 3.6% on Thursday. This week, I’m dropping my Buy Below down to $55 per share.

Buy List Updates

I also want to change a few Buy Below prices. Shares of Cerner (CERN) have been doing quite well recently. I’m going to bump our Buy Below up to $62 per share. It’s our top-performing stock this year, and it was one of our worst last year.

Shares of JM Smucker (SJM) have been trending downward over the past month. I’m lowering my Buy Below to $138 per share. Fiscal Q4 earnings are due out in early June.

I’m also going to raise the Buy Below on HEICO (HEI) to $90 per share, ahead of the stock’s split later this month. HEICO will be split 5-for-4, which means shareholders will be getting 25% more shares but the share price will fall about 20%.

That’s all for now. The March jobs report will be out later this morning. I expect to see more gains in non-farm payrolls, but I’m especially curious to see any gains in earnings. There’s been some improvement here. There will be a few early earnings reports next week, but none from our Buy List. The stock market will be closed next Friday for Good Friday. This is the one day of the year when the market is shuttered and most government offices are open. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His