Archive for September, 2017

-

CWS Market Review – September 15, 2017

Eddy Elfenbein, September 15th, 2017 at 7:08 am“Fear is an emotion, not a stock indicator.” – Coreen T. Sol

After eight and a half years, the stock market is still hitting fresh all-time highs. The Dow, S&P 500 and Nasdaq all broke out to new highs this week. Here’s a cool stat: since the election, the S&P 500 has added $2 trillion in market value, and half of that is due solely to the tech sector. The much-hated rally marches ever onward.

The S&P 500 even came close to breaking through 2,500 for the first time in its history. Thursday’s intra-day high was 2,498.43. For some context, the S&P 500 first broke 25 in 1929, and it smashed 250 in 1986.

The historically-minded observer may have noticed that those milestones came just before some unpleasantness. I still think we’re pretty safe from any nasty downturns. Inflation, interest rates and unemployment are low, and the economy continues to hum along.

In this week’s CWS Market Review, I want to focus on a key aspect that’s been helping the market this year: the weak U.S. dollar. This is a crucial factor, and it’s not widely understood. The currency markets can have a big impact on the stock market, and I want to explain what’s happening. Later on, I’ll update you on some of our Buy List stocks. Cerner became our first stock to be up 50% for this year. I hope there will be more. Before we get to that, though, let’s see why the falling greenback has been our secret helper this year.

The Weak-Dollar Rally

The U.S. dollar has not been in a good way this year, and that’s actually a good thing. Look at some of the numbers. Earlier this year, a British pound was worth $1.20. Now it’s going for $1.34. The euro’s gone from $1.05 to $1.19. The euro rally may have further room to run. The Financial Times recently reported that “speculators were holding the biggest net long position on the euro against the dollar since May 2011.”

This is important to understanding what’s happening in today’s market. Despite a good year for stocks, both the Dow and S&P 500 would be down for the year if they were priced in euros. The slumping dollar has not only helped us rally, but it’s affected the nature of the rally. Let’s dig into this some more.

Right now, the economy of the United States is out of sync with much of the developed world, especially Europe. The economy in Europe is basically where we were two or three years ago. Only now are things starting to look up for the Old World. This week, we learned that the British unemployment rate dropped to a 42-year low. Unemployment in Germany is the lowest since reunification. Even France is improving.

As a result, there’s a growing belief that Mario Draghi and the European Central Bank will pull back on their “kitchen sink” strategy for monetary policy. On top of that, the plan for more rate hikes in the U.S. seems to have faded. Capital naturally flows to where it’s treated best, and lately, that’s been away from the USA.

A good example of the dollar’s impact can be seen at AFLAC (AFL), one of our Buy List favorites. The duck stock does a huge amount of business in Japan. As a result, the stock tends to be affected by the dollar/yen exchange rate. A few years ago, the strong dollar routinely dinged several cents per share out of each quarterly earnings report. Now that’s changed. As the yen has crept higher this year versus the dollar, it’s been good for shares of AFL. Recently, AFL jumped above $82. Compare that with the early part of last year, when AFL was going for $55 per share.

No doubt, AFLAC is a good company. But we have to agree that the currency market has given the stock a nice boost.

Now here’s where it gets complicated. Normally when we see the dollar slump, it often means that commodity prices are rising. In turn, that’s good for commodity stocks. Indeed, that’s been the case, as the S&P 500 Materials ETF (XLB) has done quite well this year, especially in the last six months. Did you know that Alcoa is up nearly 60% this year? That’s more than Apple, Facebook, Google or Amazon.

But what’s interesting is that energy stocks haven’t joined in the rally. The energy sector got slammed in 2014-15. While last year saw a modest recovery, this year has been more of nothing. OPEC is even talking about extending its production cuts. Exxon and Chevron are both down for the year. Fortunately, our Buy List doesn’t have any oil stocks.

Normally, we see materials and energy stocks behaving somewhat alike. Not this year. Why? That’s hard to say. It may reflect an emerging global recovery that’s skipped over the energy patch. Nearly every kind of metal has been booming. Zinc recently touched a 10-year high. Copper’s had a strong year as well (except for a nasty correction in the past week). Aluminum is up as well. And for the goldbugs, gold is up smartly this year.

This tells me that there’s demand for industrial metals, which means there’s a demand for industry. For example, the homebuilders are having a good year. The materials trend filters down to Buy List stocks such as Sherwin-Williams (SHW) and Axalta Coating Systems (AXTA).

We’re seeing a similar effect happening in defensive stocks. Healthcare and consumer staples normally tack each other fairly well, but not this year. It’s been a good year for healthcare stocks. On our Buy List, Stryker (SYK) is up more than 20% for us this year. But the consumer staples stocks have lagged, sometimes badly. On our Buy List, Hormel Foods (HRL) and Smucker (SJM) are both in the red.

Especially weak lately has been the financial sector. Typically, financial stocks rally when short-term interest rates rise. Or, more accurately, the hope for higher short rates rises. Financial stocks soared after last year’s election but haven’t done much of anything since then. August was an especially bad month for financials. Later on, I’m going to highlight Signature Bank (SBNY), which I think has finally fallen to a very good price point.

The tech sector has also been very strong this year. The S&P 500 Tech Sector ETF (XLK) is now up 22% this year. On our Buy List, we’ve seen the tech effect with Microsoft (MSFT), which is a 20% winner YTD. Many of the tech stocks have a global reach, so the weak dollar is a positive.

The weak dollar has also followed the small-cap sector lower. Both peaked after the election late last year, and both have drifted lower this year. This may be having an effect on the market’s appetite for risk. With volatility so low, there’s not much room for action for excitable day traders. As a result, this may be pushing them towards more extreme markets like bitcoin. I can’t be positive, but there may be a direct relationship between the stock market’s calmness and bitcoin’s frenzy. The virtual currency is down by one-third in the last 12 days.

What to do now: Wall Street is largely in a state of limbo until Q3 earnings season begins in another month. The recent economic numbers look good. The Fed may even be leaning towards a December rate hike. (I hope not, but it’s possible.)

It’s important for investors not to be scared out of this market. The fundamentals are strong, but the market is always vulnerable to a near-term hit. I also think it’s possible that a dollar rally could cause an internal market rotation.

As always, I like the stocks on our Buy List. Stocks like Ross Stores (ROST), Intercontinental Exchange (ICE) and Signature Bank (SBNY) look especially good here. Now let’s look at some updates to our Buy List stocks.

Buy List Updates

I had wanted to wait a bit before I updated some of our Buy Below prices, but now that we’re in the quiet period of September, I think this is a good opportunity for us to make some adjustments.

Cerner (CERN) continues to be a very strong performer. Cerner is now up 52% on the year for us. It’s our #1 performer. Last year, it was our #2 worst stock. Funny how that happens. In July, the healthcare-IT company had another solid earnings report. Cerner also narrowed its full-year EPS guidance from $2.44 to $2.56, to $2.46 to $2.54.

The next earnings report should come out in late October. The company expects Q3 earnings between 61 and 63 cents per share. This week, I’m raising my Buy Below on Cerner to $76 per share.

Look for Microsoft (MSFT) to raise its dividend next week. The current quarterly payout is 39 cents per share. I’m expecting 42 cents, maybe 43 cents per share. In the last seven years, the software giant has tripled its dividend. Too many investors look past dividends. This is a mistake. Consider this stat: If MSFT goes to 43 cents, that means an investor who got the stock at the start of the bull market would be yielding 11.6% based on their purchase price. Not too bad. I’m keeping my Buy Below for Microsoft at $76 per share.

I previously said I wanted to hold off on raising my Buy Below price for Continental Building Products (CBPX), but I’ve been impressed with the stock’s resiliency. The shares got a boost after Hurricane Harvey. I’m going to lift my Buy Below on CBPX to $26 per share.

Signature Bank (SBNY) has been a very frustrating stock to watch. It soared after last year’s election. The shares gained 21% in just four days. But it’s been a wreck ever since, especially since June. Lately, SBNY seems to go down every single day. On Thursday, the shares dropped below $120. The next earnings report should be out around mid-October. I’m lowering my Buy Below on Signature to $130 per share.

That’s all for now. The Federal Reserve gets together on Tuesday and Wednesday of next week. I don’t expect them to make any interest-rate moves, but there could be signals about their plans for December. The Fed’s policy statement will come out at 2 pm ET on Wednesday. After that, Fed Chairwoman Janet Yellen will answer questions at a press conference. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: September 15, 2017

Eddy Elfenbein, September 15th, 2017 at 7:05 amBitcoin Sinks as China Is Said to Order Exchange Halt This Month

Why the U.S. Government is Moving to Ban This Russian Software Company

Nestlé Targets High-End Coffee by Taking Majority Stake in Blue Bottle

Nissan, Renault, Mitsubishi Deepen Alliance in Electric Push

China Green Car Pivot Will Need State Support, GM Chief Says

Softbank Reportedly Wants a Big Discount for Uber Investment

Alphabet Considers Lyft Investment of About $1 Billion

‘Angry Birds’ Maker Rovio Is Not Worth What People Expected

Verizon Hints at Another Acquisition in Battle Against Google, Facebook

Google and Facebook Fret Over Anti-Prostitution Bill’s Fallout

Who’s Warren Buffett’s Successor? JPMorgan Thinks It’s Greg Abel

Equifax Breach Prompts Scrutiny, But New Rules May Not Follow

In Amish Country, The Future Is Calling

Joshua Brown: ESG Links: Allocating With Purpose

Jeff Miller: Stock Exchange: Do Your Trades Fit Your Style?

Be sure to follow me on Twitter.

-

Inflation Heated Up in August

Eddy Elfenbein, September 14th, 2017 at 10:52 amThe government released the August inflation report this morning, and for the first time in several months, inflation actually came in higher than expected. The headline rate rose by 0.4% which was 0.1% higher than economists had been expecting.

Obviously, Hurricane Harvey impacted some of that. Gasoline prices were up 30 cents last month. But even the “core rate,” which excludes food and energy prices, was up 0.2% last month.

I still don’t think the Fed will hike rates in December, but the futures market is now about 50-50 on that.

Here’s the headline rate:

Here’s the core rate:

-

Morning News: September 14, 2017

Eddy Elfenbein, September 14th, 2017 at 7:06 am`False Peace’ For Markets? A Trader Is Betting Millions On It

U.K. Subjects Murdoch’s Fox to Wider Probe Over Sky Takeover Bid

Trump Blocks China-Backed Bid to Buy U.S. Chip Maker

This Is the Crazy Tax Math Trump Must Master, Fast

Thank You for Calling Equifax. Your Business Is Not Important to Us

Equifax’s Mega-Breach Was Made Possible by a Website Flaw It Could Have Fixed

Tesla To Unveil Electric Semi Truck That Elon Musk Calls A ‘Beast’

Ford’s Push For Driverless Vehicles Includes a Man Pretending To Be a Car Seat

To Fight Amazon, This Startup Offers Retailers Their Own Mini-Me

Munich Re Says It May Miss Profit Target on Irma, Harvey

Target Is Hiring Way More People for the Holidays This Year

Deutsche Börse to Pay $12.5 Million in Fines in Insider Trading Inquiry

Jeff Carter: The Chicago Bitcoin Summit

Be sure to follow me on Twitter.

-

Morning News: September 13, 2017

Eddy Elfenbein, September 13th, 2017 at 7:06 amIn China’s Hinterlands, Workers Mine Bitcoin For A Digital Fortune

Getting High On Your Own Bitcoin Supply

Act or Wait? Fed Debate Heats Up After Inflation Misses Target

Department Of Transportation Rolls Out New Guidelines For Self-Driving Cars

Mnuchin: It Might Not Be Possible to Reach 15% Corporate Tax Rate

Finance Industry’s Deregulation Drive Faces New Threat With Equifax

DowDuPont Revises Breakup Plan Opposed by Activist Investors

Seadrill Files for Chapter 11 Bankruptcy Protection in Texas

Toshiba Says It Favors Bain Group’s Bid for Microchip Business

Apple Bets on Augmented Reality to Sell Its Most Expensive Phone

Emails Show How the Food Industry Uses ‘Science’ to Push Soda

The Food Court Matures Into the Food Hall

Ben Carlson: Markets Are Hard: Seth Klarman Edition

Cullen Roche: There’s No Such Thing as a “Sin Stock”

Michael Batnick: A Few Charts and a Few Thoughts at All-Time Highs

Be sure to follow me on Twitter.

-

Morning News: September 12, 2017

Eddy Elfenbein, September 12th, 2017 at 7:07 amDollar Sports Heavier Tone As Yesterday’s Bounce Runs Out Of Steam

Bitcoin Diehards Are Undeterred by China

Theresa May Pleads With Donald Trump to Protect Thousands of Jobs in Britain

A $150 Billion Misfire: How Forecasters Got Irma Damage So Wrong

The Real Outrage Isn’t Equifax’s Arbitration Clause — It’s All The Others

How Cities Can Win the Fight for Amazon’s HQ2

Nordstrom Slides After Announcing Plans of a Smaller Store Concept With No Merchandise

SoFi Chief Executive to Step Down

GM, Cruise Unveil Self-Driving Car Ready For Mass Production

Volkswagen to ‘Electrify’ All 300 of Its Cars and SUVs by 2030

Tesla is Adding Charging Stations in City Centers

DowDuPont Alters Post-Merger Breakup Plan

Apple Set to Unveil Anniversary iPhone in Major Product Launch

Howard Lindzon: Momentum Monday – Sipping Avocado Juice and Shooting Fish in a Barrel in China

Joshua Brown: You Can Practically Smell It In The Air

Be sure to follow me on Twitter.

-

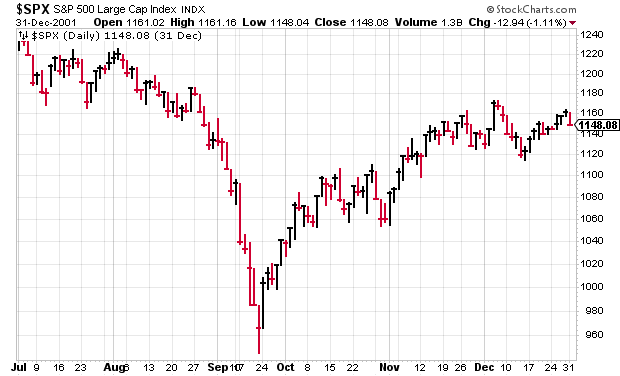

Crossing Wall Street 16 Years Ago

Eddy Elfenbein, September 11th, 2017 at 7:33 am

It’s been 16 years since 9/11. Since then, the stock market’s total return index has more than tripled. However, nearly all of that came in the second eight years. The first eight years came to nothing.

Here’s what the S&P 500 looked like during the second half of 2001. The market has been sliding going into September 11.

-

Morning News: September 11, 2017

Eddy Elfenbein, September 11th, 2017 at 7:07 amGlobal Shares Return to Record High as Irma Loses Strength

Cruise Lines Send Ships to Caribbean on Hurricane Rescue Mission

Insurers Ache for Qualified Inspectors After U.S. Hurricanes

India Swaps Cheaper LNG for More Volume in 2nd Reworked Deal

Here’s Who China’s Bitcoin Exchange Ban Reportedly Won’t Affect

As China Moves In, Serbia Reaps Benefits, With Strings Attached

Electric Cars Reach a Tipping Point

Teva Picks Lundbeck’s Schultz to Revive Israeli Drugmaker

Canadian Mining Firm Threatens to Suspend Greece Investment

Amazon’s Surprise Plan for HQ2 is a Bold Experiment

What to Expect at Apple’s Biggest Event in Years

U.S. Solar Bracing for First Decline as Rooftop Demand Slumps

Jeff Miller: Have the Odds Improved for a Market-Friendly Policy Agenda?

Michael Batnick: These Are The Goods

Roger Nusbaum: Barron’s on Health Savings Accounts

Be sure to follow me on Twitter.

-

CWS Market Review – September 8, 2017

Eddy Elfenbein, September 8th, 2017 at 7:08 am“Investing without research is like playing stud poker and never looking at the cards.” – Peter Lynch

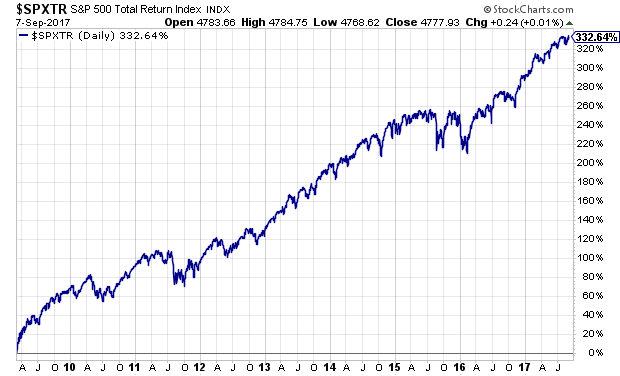

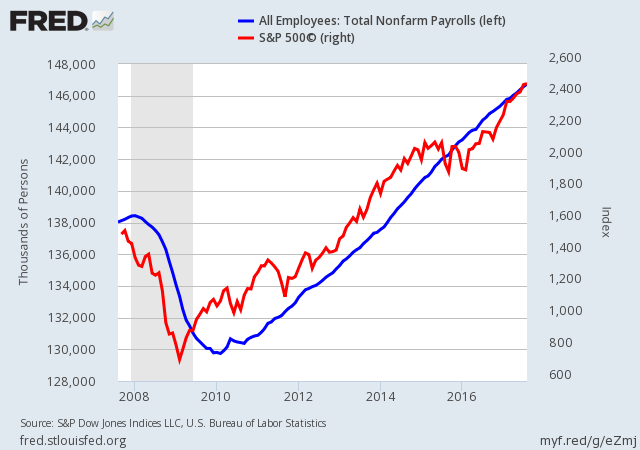

Tomorrow will mark 8-1/2 years of the great bull market. On March 9, 2009, the S&P 500 reached its closing low of 676.53. The previous Friday, March 6, the index touched its sinister-sounding intra-day low of 666.79. To give you an idea of how bleak things were, that morning the government reported that the unemployment rate touched a 25-year high, and the non-farm payrolls report for February came in at -651,000. Yikes!

Things are quite different today. Going by Thursday’s close, the S&P 500 Total Return Index has gained 332.64% in this bull market. That’s enough to turn every $1 into $4.32. This has been one of the longest and strongest bull markets in history, but what’s fascinating is how hated it’s been. Some people just can’t stand to see the indexes rise higher and higher.

We’re constantly told that it’s a reckless bubble that’s all about to crash. Or it’s all due to manipulation from the Fed, and it’s all about to crash. Please. Predicting that the world is about to end is one of the favorite pastimes on Wall Street. Still, the bull marches on. In fact, this year may turn out to be the lowest year on record for the stock market’s volatility.

If there’s a golden rule for long-term investing, it’s that betting on disaster is always overpriced, and betting on “it’ll all work itself out” is always a bargain. In this week’s CWS Market Review, we’ll look at some of the recent economic news. I’ll update you on some Buy List stocks. First, we’ll survey what’s in store for the Federal Reserve. Soon, the Fed will be down to just three members left on the seven-member board.

What’s Next for the Federal Reserve?

Stanley Fischer, the vice-chair of the Federal Reserve, announced this week that he’s stepping down next month. This brings us to an unusual moment for the Fed since there will be four vacancies on the Federal Reserve Board. By law, the FRB has seven slots. By my math, this means that the labor force participation rate for Fed governors is only 43%.

It will soon go even lower since Janet Yellen’s term as Fed chair ends in February. This gives President Trump a big opportunity to put his stamp on the Fed. Officially, Trump has not ruled out reappointing Janet Yellen to another term as Fed chair, but that probably won’t happen. She recently defended some of the post-crisis financial regulations which Trump has promised to repeal.

Quick side note: The appointments to the Fed and of the Fed chair are separate presidential appointments. So if President Trump doesn’t reappoint Yellen as chair, she would still be a Fed member. However, it’s generally assumed she would resign if she were no longer Fed chair.

Fed watchers had assumed that Gary Cohn was Trump’s top choice to replace Janet Yellen. But this week, the Dow Jones reported that it’s “unlikely” Cohn will get the nod due to his criticisms of the president’s response to the terrible events in Charlottesville. Jake Tapper tweeted that one White House source said that Cohn was more likely to get the electric chair than the Fed chair. Ouch.

GOP source close to WH tells me: Cohn "more likely to get electric chair than Fed Chair" https://t.co/5IGR0Db1wU

— Jake Tapper (@jaketapper) September 6, 2017

So who’s next for the position of Fed Poobah? A few names have been thrown around. I would guess that John Taylor at Stanford would be a front runner. He’s widely known for the “Taylor Rule,” which is a guideline for determining where interest rates should be. Frankly, I’m a skeptic on these rules. They’re great in theory, but I’m not sure how they work in real time. But there’s no doubt that Taylor is a highly-qualified choice. Some other contenders are Kevin Warsh, Glenn Hubbard and Jerome Powell.

President Trump has described himself as a “low-interest-rate person,” but I doubt he’s very ideological on monetary matters. This is an important time for the Fed. The central bank wants to unwind its gigantic balance sheet at the same time it’s looking to raise interest rates. It’s not an easy task. With low rates, that weakens the dollar. The euro is near a 33-month high versus the greenback.

I’ve been critical of the Fed lately because I think they’ve moved too quickly on rates. Lately, however, I think the Fed is coming around to my side (more on that in a bit). I think the Fed will remain on a pragmatic and accommodative course over the next few years, and that’s good for investors.

The U.S. Economy Is Gaining Strength

Speaking of the Fed, last Friday we got the August jobs report. It was on the weak side, but nothing too dramatic. Last month, the U.S. economy created 156,000 net new jobs. The numbers for June and July were revised downward. The unemployment rate ticked up to 4.4%, but it’s still near a 16-year low. For the most part, the U.S. economy has created an average of 200,000 jobs a month every month for the last seven years. The numbers haven’t deviated very far from that trend.

While this report wasn’t that bad, I think it finally clued in the bond market that the Fed isn’t going to move on interest rates anytime soon. The equation is simple. When someone asks, “Are stocks cheap?,” the answer is always, “Compared with what?” (Yes, we answer questions with questions.) That’s why interest rates are so important to equity valuations.

Last Thursday, the government released personal-income and spending numbers for July. That report includes the PCE price index, which is the Fed’s preferred measure for tracking inflation. The core PCE number for July rose by just 0.1%. It was the same in June. For the past year, core PCE is up 1.4%. In other words, inflation is hardly a problem. Next week, we’ll get the CPI report for August, and I expect to see much of the same.

With so little happening with inflation the Fed may be convinced to back down. The FOMC is set to meet again on September 20, and I strongly doubt they’ll do anything. The futures market thinks there’s only a 26% chance the Fed will raise rates before the end of the year. I’d say that’s about 20% too high. The Fed funds futures are now priced to show a 54% chance of no rate hike in the next 12 months. That’s a stunning reversal of sentiment. Late last year, the Fed was calling for three hikes this year, plus three more in 2018 and three more in 2019. All that’s gone now.

One potential roadblock for the economy could be the impact of Harvey and Irma. We don’t know yet the full measure of these events. On Thursday, we got our first glimpse of what Harvey could mean. Initial jobless claims soared to 298,000. That’s a rise of 62,000. As a metric, initial jobless claims have the benefit of being early, but that’s at the expense of being noisy. We saw similar jumps with previous storms.

The recent economic numbers look quite good. Q2 GDP came in at 3%. Last week, we learned that personal income rose by 0.4% in July while personal spending rose by 0.3%. That’s quite good. Also, Friday’s ISM report was the best in six years. This suggests the economy got off to a strong start for Q3. The Atlanta Fed’s GDPNow model now says that Q3 GDP grew by 3.3%. I’m wary of such models, but I hope that number is right.

Buy List Updates

Cinemark (CNK) got trashed for a 5% loss on Thursday. What happened? Disney came out with details on its streaming service. Marvel and Star Wars will be exclusive to Disney and not on Netflix. This was a rough summer for the movie biz, but as far as earnings go, Cinemark is doing well. They missed earnings last quarter by one penny per share, yet the stock has been hammered. Cinemark is now going for less than 14 times next year’s estimate. As of now, there’s no evidence that the recent news is hurting CNK’s business. I’m looking for a turnaround for shares of CNK.

Cerner (CERN) broke out to a new 52-week high this week. CERN is still shy of its all-time high of $75 from two years ago. The stock is having a great year for us (+45.7%). I’m going to hold off raising my $68 Buy Below price for now. Cerner could turn into a big winner for us.

I’m ready to declare Signature Bank (SBNY) a very good bargain. The shares are now down to $122. The bank has basically erased nearly everything it gained in the post-election boom. Yes, SBNY has its issues, but the numbers have been solid. I think it’s possible SBNY can earn $10 per share next year.

That’s all for now. There’s not much in the way of economic news next week. I’ll be keeping an eye out for Wednesday’s report on the Federal Budget. The deficit is shaping up to be worse than originally thought. This comes after years of decreasing deficits. On Thursday, we’ll get the CPI report for August. Inflation has been quite tame for the last few months. Let’s see if that trend continues. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: September 8, 2017

Eddy Elfenbein, September 8th, 2017 at 7:01 amWhy Europe’s Central Bank Shouldn’t Worry About the Euro

Will Saudi Aramco Deliver World Record Profit For Next Year’s IPO?

Oil Steady as Irma Heads For Florida, Saudi Arabia Cuts Supply

In World of Supposed Bubbles Here’s What Investors Fear Most

Equifax Says Cyberattack May Have Affected 143 Million Customers

Amazon Plans Second Headquarters, Opening a Bidding War Among Cities

Who Will Win the Great Airfare War of 2017?

F.D.A. Accuses EpPen Maker of Failing to Investigate Malfunctions

Amazon Shoppers Complain of Price-Gouging During Hurricane Irma

Comcast Stock Plunges On Video Subscriber Losses, Hurricane Impact

Using Silicon Valley Tactics, LinkedIn’s Founder Is Working to Blunt Trump

Hedge Fund Wannabes Busted for Trading on Illegal Amazon Tips

Howard Lindzon: Identity…Here We Go Again

Jeff Miller: Are You Trying To Win Every Trade?

Cullen Roche: Yes, Getting Rid of the Debt Ceiling is Smart

Be sure to follow me on Twitter.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His