Archive for September, 2017

-

The Impact of Harvey

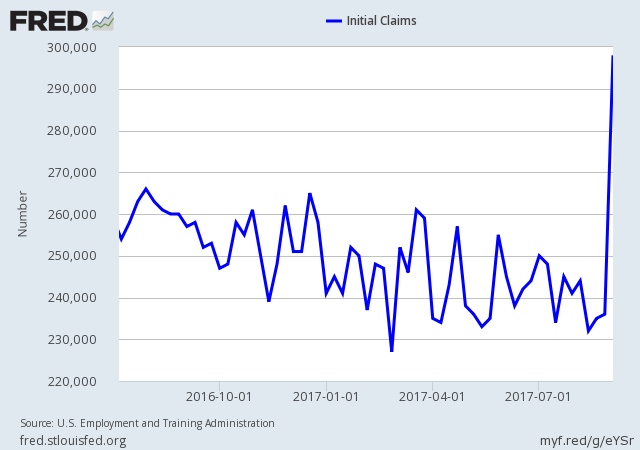

Eddy Elfenbein, September 7th, 2017 at 11:03 amThere’s been a lot of talk about the economic impact of Hurricane Harvey. Much of this we simply don’t know yet. This morning, we got one of our first looks. Notice the jump in initial jobless claims.

Jobless claims came in at 298,000. That’s enough to keep our sub-300,000 streak going. The last time jobless claims printed over 300,000 was in February 2015.

-

Morning News: September 7, 2017

Eddy Elfenbein, September 7th, 2017 at 7:10 amIt’s Time for Draghi to Talk About the Elephant in the Room

Self-Driving Cars’ Prospects Rise With Vote by House

Nuclear Plants in Irma’s Path Plan Shutdowns Ahead of Storm

Amid Preparations For Hurricane Irma, Amazon Draws Scrutiny For Price Increases

Amazon is Building a $5 Billion Secondary U.S. HQ and Wants Local Governments to Submit Proposals

IBM Invests $240 Million Into AI Research Lab With MIT As It Struggles In AI Battle

Kohl’s Enlists Amazon as Ally in Bid to Drive Store Traffic

Toys `R’ Us Is Said to Hire Advisers to Help Weigh Bankruptcy

From Software to Staffers, Tesla and SpaceX Share More Than Musk

We’re Going to Need More Lithium

Football Champs and CEOs Alike Sidestep Taxes With Private Jets

Ben Carlson: How Stocks Took Over Asset Allocation

Jeff Carter: Should Google Be Broken Up?

Be sure to follow me on Twitter.

-

Morning News: September 6, 2017

Eddy Elfenbein, September 6th, 2017 at 6:59 amSimmering Korea Tensions Hit Global Stocks and Dollar

What the ECB Will and Won’t Do This Week

Nafta Talks Lurch Ahead Without Signs of Major Progress

This Bond’s Rollercoaster Ride is Far From Over

Chief Executives See a `Sad Day’ After Trump’s DACA Decision

Intel Wins Boost in Fight Over $1.26 Billion Antitrust Fine

Lego Will Cut 1,400 Jobs as Profit Dips, Despite Big-Screen Heroics

Wells Fargo Scandal: Banks Tap Watson To Monitor Employee Activity

The World’s Largest Chocolate Maker Is Committing $1 Billion to Fight Climate Change

Coupa Software Narrows Fiscal Q2 Loss, Revenue Tops Views

Toshiba Board Reaches No Verdict on New Western Digital Chip Proposal

Nissan Aims to Double Sales of the Leaf With New Features

Joshua Brown: When The Hedge Is Worse Than The Thing Being Hedged

Roger Nusbaum: August Was Complicated But Markets Took It In Stride

Be sure to follow me on Twitter.

-

The Worst Time of the Year for Stocks

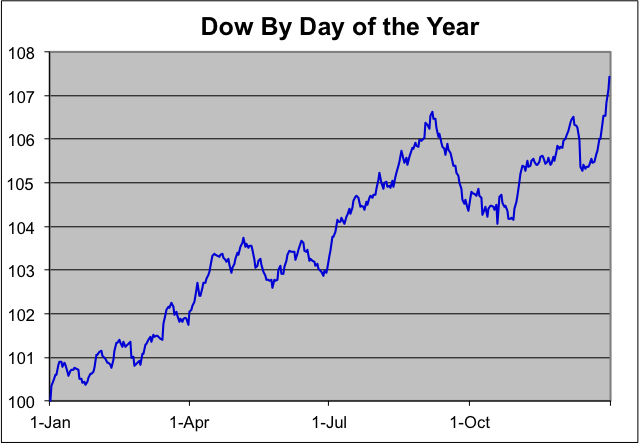

Eddy Elfenbein, September 5th, 2017 at 2:51 pmI’ve crunched the entire history of the Dow Jones Industrial Average and come up with the average year for the index. As it turns out, we’re about to start what has been the worst time of the year historically for stocks.

The historic Dow reaches a peak on September 6 and falls 2.31% by October 29. For any one year, that’s not a big fall, but it’s equivalent to nearly one-third of the Dow’s average annual return. Here’s what the Dow’s average year looks like:

To be clear, I would never make an investment decision based on this kind of analysis. I just think it’s interesting.

-

Morning News: September 5, 2017

Eddy Elfenbein, September 5th, 2017 at 6:36 amUK Economy Losing Momentum As Brexit Worries Weigh

Trump’s South Korea Trade Talk Is Just That

Chill, Bitcoin’s Still Cool. What’s That Burning?

`Too Big to Fail’ Label May Shrink for Some Firms Under Trump

Airlines’ $10 Billion August Swoon Keeps Wall Street on Edge

United Tech Forges Aerospace Giant With $23 Billion Rockwell Buy

Lego Cuts Jobs as Profit Declines Amid Change of Leadership

Novartis Calls the Doctor to Push Breakthrough Drugs Forward

Amazon Fears Sink Blackstone’s $2.8 Billion Australian Mall Sale

An `Angry Birds’ Empire: Games, Toys, Movies and Now an I.P.O.

Lilium, a Flying Car Start-up, Raises $90 Million

Noble Group in Talks to Extend $2 Billion Credit Facility Deadline

Howard Lindzon: Momentum Monday on Tuesday…Moore’s Law and Quantum Computing

Michael Batnick: These Are The Goods

Ben Carlson: An Alternative Solution to the Retirement Crisis

Be sure to follow me on Twitter.

-

Morning News: September 4, 2017

Eddy Elfenbein, September 4th, 2017 at 7:05 amXi Calls for BRICS to Play a Bigger Role in World Governance

Beijing’s Coin Offerings Clampdown Could Hit 105,000 Investors in China

Kim Can Disturb Japan’s Zen, Not Yen

Investor With 30% in Cash Says North Korea Selloff Will Come

Trump Shifts Labor Policy Focus From Worker to Entrepreneur

Texas Edges Closer to Recovery After Harvey as Key Pipeline Restarts

Hurricane Harvey’s Massive Flooding Also Destroyed Hundreds of Thousands of Cars

To Understand Rising Inequality, Consider the Janitors at Two Top Companies, Then and Now

Novartis CEO Jimenez to Quit, Giving Reins to Harvard Doctor

Fiat Chrysler Set for Parts-Unit Separation as Big Deal on Hold

Latest Air Berlin Bidder Looks to Focus on Holiday Routes

Why Drugs Cost Less in the U.K. Than in the U.S.

Jeff Miller: Time to Ask What Could Go Wrong?

Jeff Carter: Driverless Will Affect Everything

Be sure to follow me on Twitter.

-

August NFP +156k, Unemployment 4.4%

Eddy Elfenbein, September 1st, 2017 at 10:37 amThe August jobs report is out. The U.S. economy created 156,000 net new jobs last month, although there were downward revisions to June and July. The unemployment rate ticked up to 4.4%. Average hourly earnings rose just three cents to $26.39. That’s up 2.5% in the last year.

“Growth was slower in August, but that’s because there were fewer gains in growing industries, not because we’re seeing more losses in shrinking industries,” said Jed Kolko, chief economist at Indeed.com. “We’re actually at a point of unusual stability.”

The report does not include any impact from Hurricane Harvey and the devastation it unleashed in Texas, as the collection of the data used for the report was completed before the storm struck.

Employees also worked a bit less in August, with the average workweek falling .3 percent to 34.4 hours.

I think we can forget about the Fed raising rates again this year — and probably not for the first half of next year.

-

CWS Market Review – September 1, 2017

Eddy Elfenbein, September 1st, 2017 at 7:08 am“The race is not always to the swift, nor the battle to the strong, but that’s how the smart money bets.” – Damon Runyon

Like many of you, I’ve been distraught by the scenes of destruction caused by Hurricane Harvey in Texas. It always feels a bit improper to discuss the financial impact of such terrible events, yet it’s an important subject. For these areas to rebuild, they need investment, and that’s what we talk about around here.

Fortunately, the financial disruption from Harvey, while serious, appears to be contained at this point. That’s a relief, especially considering the sheer amount of rain brought on by the storm. The stock market has been calm, as it was before the hurricane. The Nasdaq Composite (see below) just closed at an all-time high, and the S&P 500 Total Return has now closed higher for the tenth month in a row.

Houston is, of course, a crucial city for the energy industry. Right now, one-fifth of the nation’s refinery capacity has been shut down. At the moment, 3.6 million barrels per day are offline. That costs money. According to GasBuddy, the retail price for gasoline is up 11 cents per gallon in the past week. There simply isn’t enough fuel to fill the pipelines to supply other areas of the country. Gasoline futures just touched a two-year high.

In this week’s issue, I’ll discuss what it all means for us and our portfolios. We’ll also look at interest rates. Remember all those forecasts from the Fed for higher and higher interest rates? Well, that seems to be off the table. Later on, I’ll examine how some of our Buy List stocks are reacting. But first, let’s take a broader look at where we are now.

The Disruptions from Harvey Won’t Last Long

On Thursday, the Nasdaq Composite closed at an all-time high, and the S&P 500 is less than 0.4% from its all-time high close. So despite the terrible destruction from Harvey, investors continue to be optimistic. The S&P 500 hasn’t posted a weekly decline of more than 2% in nearly a year.

This week, unlike in weeks past, we don’t have any earnings reports to discuss, or upcoming earnings to preview. Earnings season is past us. The summer is over, and we’re coming up on what’s historically been the rough time of the year for the stock market.

I tend not to place a great deal of faith in these kinds of trends, but I’ll note that September 6th has historically been a peak for the market. From September 6th to October 29th, the Dow has lost an average of 2.3%. Of course, that’s the average for 120 years, so we can’t say too much about any one particular year.

When looking at the impact of an event such as Harvey, it’s important to remember how dynamic markets are. For example, if people can’t get oil from Houston, then foreign suppliers rush in to fill the void. In the near term, I expect to see gasoline prices rise, which normally happens at this time of year anyway.

We’ll also see a drop in employment and a rise in consumer prices, but I expect both will be short-lived. This also happened during other recent natural disasters. While the cost of Harvey is in the tens of billions, overall U.S. GDP is close to $20 trillion, so we need to maintain our perspective. I assume that many planned new car purchases have been delayed, but we’ll see a rise in car buying soon. I would also expect that in the post-Harvey environment, lawmakers are much less inclined to see a government shutdown. At least, I hope they are.

So far, insurance stocks are holding up fairly well. On our Buy List, shares of AFLAC (AFL) have broken out to a new all-time high. I’ll have more on AFL later. One of the more surprising reactions to Harvey is the surge in shares of Continental Building Products (CBPX). Of course, since the company specializes in gypsum wallboard, the rally makes sense, but I certainly didn’t see the uptick coming.

One month ago, CBPX reported a three-cent earnings miss; still, the shares jumped after the earnings report. I suspect traders were expecting even worse news. The problem is that product costs have been rising, but Continental hasn’t been able to pass that along to their customers. That may soon change.

This has been a very good week for Continental. On Monday, shares of CBPX rose 3.6%, followed by a 0.4% gain on Tuesday and a jump of 7% on Wednesday (see above). It’s now in the black for us this year. Three weeks ago, I dropped my Buy Below from $26 to $23 per share. I probably moved to soon, but I want to hold off raising it for now. The recent rally is due to expectations of more business, and I’d prefer to see proof. This is a good example of the effects of a natural disaster that you might not expect.

You Can Forget About That Parade of Rate Hikes

On Wednesday, the government updated its report on Q2 GDP growth. The initial report in July said the economy grew in real, annualized terms by 2.6%. This week, that was raised to 3.0%. That’s the best quarter for the economy for the past nine quarters.

From the 60s until the last recession, the U.S. economy tended to grow in real terms by about 3%. Since then, the economy has grown in slower terms, around 2%. While the last GDP was encouraging, I doubt it’s the beginning of a growth resurgence. The Atlanta Fed has a model that tries to predict the GDP numbers. For Q3, the model currently says 3.3%. That would be very good.

Later today, the government will release the employment report for August. The numbers recently have been pretty solid. Unemployment is currently at 4.3%, which is tied for a 16-year low. The economy has added an average of 200,000 jobs every month for the last seven years.

For our purposes, what’s been most interesting has been the lack of inflation. Traditional economics (don’t laugh) suggests that prices should rise as we get close to full employment. If anything, inflation has been going down as more people are working. The Fed likes to watch the PCE price index. That rose by just 1.4% in July.

Last December, the Fed said it sees raising interest rates three times in 2017, 2018 and 2019. I wrote, “Not to put too fine a point on it, but that’s nuts.” It looks like I was right. While the Fed has already raised rates twice this year, a third hike doesn’t look to be happening. In fact, the futures market doesn’t see another hike coming until June 2018.

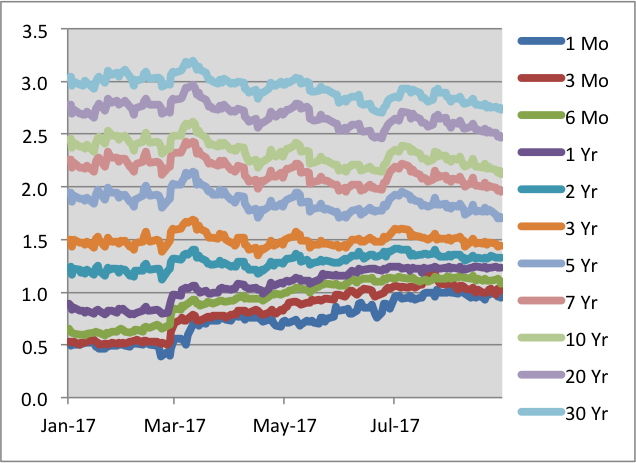

What’s been interesting is the behavior of the bond market. Long-term yields have been trending lower while short-term yields have been climbing higher. The three-year note is the dividing line. Anything longer than that means yields are going down. Shorter than that, they’ve been rising (see colorful chart below). This means that the yield curve is getting flatter. Traditionally, a flat yield curve is a warning sign for the stock market and the economy. While the yield curve is indeed getting flatter, we’re still a long way from the danger zone.

The 10-year inflation-protected bond still yields you a measly 0.4%. A few years ago, I ran some numbers and said that the stock market does well until TIPs yield 2.4%. That shows you how much room we have. Of course, five years ago, 10-year TIPs were yielding -0.90%.

I also wanted to touch on another interesting phenomenon: divergence between energy stocks and materials stocks. These two sectors tend to be decently correlated, but the connection is far from perfect. This year, however, they’re moving in different directions. This represents a major trend of 2017: metal prices are going higher, while energy prices, oil and natural gas, are going down. There’s no rule that extraction industries need to run parallel, but they generally have.

Copper, for example, is now at a three-year high. Gold and silver have been coming to life recently as well. This may suggest that the global economy is getting back on its feet despite a sluggish energy patch. This may also explain the weak dollar this year. In fact, the Dow is actually down this year, if it were priced in euros. Overall, I think the financial markets are in a healthy state, and hopefully, the Houston area will be back as strong as ever. Now let’s look at some news from our Buy List.

Buy List Updates

On Thursday, shares of Microsoft (MSFT) closed at another all-time high. The stock is now a 20% winner for us this year. We added MSFT to our Buy List in 2014. It was almost exactly four years ago when Steve Ballmer announced his retirement. Shares of MSFT jumped 7.3% on the news. Just as a rule of thumb, if the company you lead gains $20 billion in market value on the news that you’ll be out the door, then the relationship probably wasn’t meant to be. Since the day of Ballmer’s announcement, shares of MSFT have gained more than 150%.

Last earnings season, which was their fiscal Q4, Microsoft had another solid report. They beat Wall Street’s consensus by four cents per share. The software giant also gave upbeat guidance for the current quarter. The company said it expects Intelligent Cloud revenue to rise by between 8% and 11%. They also see Productivity and Business Processes revenue rising by 21% to 24%.

I also expect to see a dividend increase fairly soon. In the past, the company has announced dividend increases toward the middle of September. They’ve been pretty generous as well. Over the last seven years, Microsoft has tripled its dividend. The company now pays out a quarterly dividend of 39 cents per share. Going by Thursday’s close, that works out to a yield of 2.1%. My guess is that Microsoft will soon bump up its dividend to 42 cents per share. Microsoft is a buy up to $76 per share.

AFLAC (AFL) is one of two stocks left that have been on our Buy List all 12 years. The other is Fiserv. Shares of the duck stock have come to life in the past few weeks. Keeping with the animal theme, AFLAC is one of the stocks that acts like a rabbit. It will sit and sit and sit and then suddenly start hopping like mad.

Seven months ago, AFLAC bombed its Q4 2016 earnings report. They missed by 17 cents per share. The stock dropped 4% that day. In the CWS Market Review from February 3rd, I wrote, “Let me be clear: I’m not at all worried about AFLAC. This is a very well-run firm, and the stock is going for just over 10 times this year’s earnings estimate.” The shares are up 23% since then. This week, I’m going to raise my Buy Below on AFLAC to $86 per share.

That’s all for now. The August jobs report will be coming out later this morning. We may see a fresh 16-year low in the unemployment rate. The stock market will be closed on Monday for Labor Day. Next week, we’ll get the factory orders report on Tuesday. The important Beige Book comes out on Wednesday. Then on Thursday, we’ll get a look at the productivity report. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: September 1, 2017

Eddy Elfenbein, September 1st, 2017 at 7:05 amGreek Economy Expands for Second Straight Quarter

U.K. Manufacturing Unexpectedly Accelerates to Four-Month High

Mnuchin Says Trump Administration, Congress to Release Tax Plan Details in Coming Weeks

Spaghetti-Like Pipeline System Falls Short as Gulf Supplies Slow

Uber Needs a Tim Cook. Can Its New CEO Deliver?

Wells Fargo’s Testimony Left Some Feeling Shortchanged

Amazon Puts Bond Traders on Edge in Once-Quiet Corner of Market

Campbell Plunges as Bleak Outlook Follows Blow From Buffett

Check Out This $1 Million Bet Warren Buffett Looks About to Win

Just Smile: In KFC China Store, Diners Have New Way To Pay

Car Makers Offer Scrappage Deals For New Customers

Why the Dismissed Uber ‘Hell’ Program Lawsuit Could Come Back

Michael Batnick: Today in Market History, The First Index Fund

Howard Lindzon: Mein Volatility…Is Germany in Trouble? and Should You Care?

Joshua Brown: An Amazing Lesson From Warren Buffett On His Cake Day

Be sure to follow me on Twitter.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His