CWS Market Review – December 1, 2017

“Time is on your side when you own shares of superior companies.” – Peter Lynch

The month of November has come to a close, and it was another good one for stocks. In fact, this was the 13th month in a row of gains for the S&P 500 Total Return Index.

Not only is the bull still running, but he’s getting stronger. On Thursday, for the first time ever, the Dow closed above 24,000. The S&P 500 is now up 18.26% for the year. Our Buy List is also doing quite well. Since August 28, it’s beating the S&P 500 by a margin of 11.37% to 8.32% (not including dividends), and it’s been happening despite some unsettling headlines.

"Stocks Soar to All-Time High on Threat of Nuclear Annihilation"

— Eddy Elfenbein (@EddyElfenbein) November 28, 2017

Even though daily volatility remains quite low, there’s been a lot of drama in our Buy List. This is especially true for Axalta Coating Systems, a company which is playing a billion-dollar version of “hard to get.” I’ll go over the details in a bit.

Just before Thanksgiving, we got a very nice earnings report from Hormel Foods. The Spam stock is up over 20% in the last month. It also looks like Cerner is partnering with Amazon. That was enough to give the stock a jolt. Also, Express Scripts is looking a lot like a company that’s putting itself up for sale. I’ll explain it all. Plus, I have some new Buy Below prices for our Buy List. Before we get to that, let’s look at the soap opera that’s better known as Axalta Coating Systems.

High Drama at Axalta

The WSJ recently ran an article titled, “Who Knew the Paint Industry Could Be this Exciting?” Man, oh man, I have to echo those thoughts when discussing the wild ride for Axalta Coating Systems (AXTA).

Let’s start at the beginning with the initial news that Axalta said they were in merger talks with Akzo Nobel. I was careful to say that they were simply talking and that no deal had been accepted. The market responded by shooting up shares of AXTA by 17% in one day. That was the good news.

Let me explain. What’s going on is a global rush to consolidate in the paint industry, and AXTA finds itself in the middle of all this. Later, on the Wednesday before Thanksgiving, we got the news that Axalta and Akzo Nobel had broken off their merger talks. (Oh no!) This news came after the market had closed. In the after-hours market, AXTA was down 17%.

Moments later, we got the news that the reason they had ended merger talks is that they had received another offer from Nippon Paint, a Japanese company. One difference was this offer was all in cash. Thought we don’t have proof, I think we can infer that Nippon’s offer was higher than Akzo Nobel’s. Then in the after-hours market, AXTA did a massive U-turn and made back everything it lost. (By the way, this is a good reason why I’m leery of using stop-losses. You can find yourself tossed out of good stocks just because everyone freaks the hell out. Take note of this week’s epigraph.)

That brings us to Thursday. Shares of AXTA were halted when we learned that Axalta had rejected Nippon’s offer. According to reports, the deal on the table was for $37 per share. Some analysts think AXTA could have gotten $40, maybe more.

I think this was a big mistake for Axalta not to accept. In my mind, it doesn’t make sense to walk away from a very good deal in hopes of getting an amazing deal. I would have especially granted Nippon some latitude since they were offering all cash.

When trading resumed around 1 p.m., AXTA had crashed to $30 per share. It eventually closed Thursday at $31.66. That’s a drop of $15.69% from Wednesday’s close. That hurts, but I suspect other companies will give Axalta a look. Maybe even our own Sherwin-Williams (SHW) will do so.

What to do now? Nothing. Let’s just wait this out. I suspect more news will be forthcoming.

The Recent Economic News Has Been…Not Bad

I like to joke that nothing upsets some people as much as good economic news. Yet it’s true: the sky is not always falling. Over the past few days, we’ve gotten some encouraging economic news.

Let’s start with the GDP report. The government revised higher its estimates for Q3 GDP growth. They now say the economy grew in real terms by 3.3% last quarter. This comes on the heels of 3.1% growth in Q2.

During this recovery, the economy has had a hard time stringing together more than three quarters in a row of robust growth. Q4 might do it for us. The Atlanta Fed currently expects Q4 growth to come in at 3.4%.

On Monday, the existing-home sales report came out, and it was the best in ten years. Then on Tuesday, the Conference Board reported that consumer confidence is at a 17-year high. (My preference is to report consumer humility as being at a 17-year low.)

Next Friday, we’ll get the jobs report for November, and I expect to see more job growth. The unemployment rate is currently at 4.1%, and it could drop below 4% for the first time since 2000.

The Federal Reserve will be getting together again on December 12-13. This will be one of their two-day meetings, which will be followed by a press conference by Janet Yellen. This will be her final presser before Jay Powell takes over early next year. The Fed will also update its economic projections, also known as the blue dots for the scatterplots.

The Fed seems almost certain to raise rates at this meeting. The futures market has it pegged at 100%, which is pretty darn certain. As I’ve said before, I think this would be a mistake, but I can’t say it’s a gigantic mistake.

After December, the outlook gets a little muddy. The futures market expects another rate hike in March, but that’s by a close margin. A hike by June is seen as much more probable (81%). That would be followed by another hike by September (55.7%).

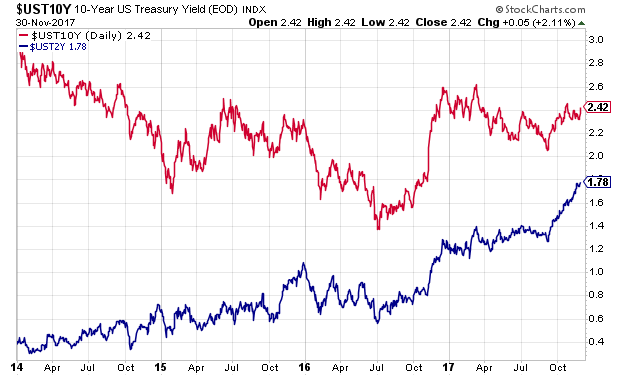

My fear is that the Fed is moving too fast too soon. There’s very little evidence of inflation. I’m also concerned that long-term bond yields are still rather low. To me, this suggests the Fed has a lower “ceiling” for rate hikes than it may realize. I want to be clear that this isn’t a problem yet, but it could be one in the coming months.

The spread between the 2- and 10-year Treasuries recently dropped as low as 58 basis points. That means the yield curve could invert with just a few more rate hikes. I just don’t see the need for that. Now let’s look at the good earnings news from Hormel.

Hormel Foods Earns 41 Cents per Share

Last Wednesday, Hormel Foods (HRL) reported fiscal Q4 earnings of 41 cents per share. That beat the Street by a penny. I was very relieved to see this report because it’s a big improvement over their previous earnings report.

This was not an easy year for the Spam people. For the year, Hormel made $1.57 per share which was down from $1.64 in 2016. The company had sales of $2.5 billion, which was down 5%, although organic net sales were up 5%. Cash flow from operations totaled $499 million. That’s up 34%. Operating margins were 13.2%.

For fiscal 2018, Hormel sees earnings between $1.60 and $1.70 per share.

“Fiscal 2018 represents a return to growth with the addition of three strategic acquisitions and contributions from innovative new items such as HORMEL® BACON 1TM fully cooked bacon and SKIPPY® PB BITES,” said Jim Snee, chairman of the board, president and chief executive officer. “The earnings power we are creating with acquisitions, major capital investments in value-added capacity, a supply chain reorganization, the union of the Grocery Products and Specialty Products segments, and an intense focus on strategic cost management sets us up for renewed earnings growth in 2018 and beyond.”

“We expect Refrigerated Foods, Grocery Products and International to drive growth as Jennie-O Turkey Store continues to navigate difficult industry conditions,” Snee said.

Net-Sales Guidance (in billions)

$9.40 – $9.80

Earnings-per-Share Guidance

$1.60 – $1.70Fiscal 2018 net-sales and earnings-per-share guidance exclude the pending acquisition of Columbus Craft Meats, which is expected to close in December. Total sales are approximately $300 million, and the transaction is expected to be 2-3 cents per share accretive to earnings in fiscal 2018.

Hormel responded very favorably to the earnings news. The stock gapped up the day before the earnings report and then pulled back only to gap up even higher. HRL is now a 4.7% winner on the year for us. Sure, that’s not great for this market, but remember that at one point, HRL was a 14% loser for the year. Thanks to the recent rally, I’m raising my Buy Below on Hormel Foods to $39 per share.

Update on Cerner and Express Scripts

I also wanted to update you on two fast-moving stories. I’ll say up front that we don’t know all the details just yet. Let’s start with Cerner (CERN). Shares of CERN got a big lift last Wednesday on the news of a potential partnership with Amazon (AMZN). The Bezos Behemoth is so big that any hint of news can move a stock.

We don’t know much about their partnership, but it appears that Amazon Web Services will be involved with Cerner’s HealtheIntent. This is a product that helps analysts predict outcomes within a certain population. I think of it as the marriage of Big Data and healthcare. We’ll get more details soon.

The other news comes from Express Scripts (ESRX). The stock has rebounded some in recent weeks as the company appears to be readying itself for a buyout. I don’t know if they’re talking with anyone (Amazon?), but they’re certainly acting like they’re on the market. Express has been selling off different units and subsidiaries that would probably be sold in any merger.

With CVS hitching up with Aetna, the writing’s on the wall for this industry: make a move, and do it soon. On top of that, Express is still reeling from the loss of Anthem. I wish I had more news at the moment, but we simply don’t know. It appears that something is going to happen, at some point.

Before I go, I want to raise our Buy Below prices on three of our stocks (in addition to Hormel). This week, I’m raising the Buy Below on Signature Bank (SBNY) to $150 per share. I’m also raising Ross Stores (ROST) to $81 per share. Finally, I’m raising Snap-on (SNA) to $181 per share.

That’s all for now. There are some key economic reports next week. On Monday, the factory-orders report comes out. On Wednesday, we’ll get a look at the ADP payroll report. That’s often a preview for the official jobs report. Speaking of which, the November jobs report will come out on Friday morning. The report for October showed an increase of 261,000. The unemployment rate fell to 4.1%, which is a 17-year low. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on December 1st, 2017 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His