CWS Market Review – February 23, 2018

“I made my first investment at age eleven. I was wasting my life up until then.”

– Warren Buffett

John Maynard Keynes famously described the irrational behavior of financial markets as being the result of “animal spirits.” Given the market’s behavior during much of 2017, the animals in question must have been snails, wombats, turtles and sloths.

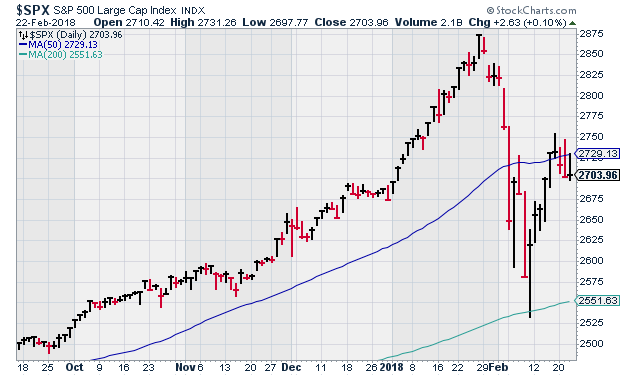

That all changed a few weeks ago when the stock market had one of its sharpest corrections in decades. Since then, things seem to have gotten back to normal. I’m not so sure.

The S&P 500 is still below its 50-day moving average, and I think there’s a good chance we will soon see more dips. In this week’s CWS Market Review, I’ll explain what I think is really going on. I’ll also highlight some good earnings reports from our Buy List stocks. Smucker beat earnings and raised guidance. Hormel raised guidance as well. Over the last two weeks, Wabtec has given us a very nice rally, and Fiserv just announced a stock split. Before we get to that, let’s look at how higher interest rates are impacting the stock market.

How the Market Is Stuck in the Middle with You

Unlike previous market breaks, the recent one was more serious. Not solely because it was steeper and sharper, but because there are more fundamental concerns driving it. Brexit or the election or hurricanes can pass quickly, but rising yields are a more pressing threat. I don’t mean to say that the market is ready to take a plunge, but I want to stress that the investing climate will become more challenging this year.

Let’s start with the basics. Interest rates are going up. This week, the one-year Treasury broke 2% for the first time in nearly a decade. The 20-year bond recently broke 3%, and the 10-year won’t be far behind. The yield curve is also starting to flatten out at the long end. This means that yields level off after about seven years. Not completely, but it’s a big change from where we’ve been.

One metric I like to follow is the spread between the 20- and 30-year Treasuries (see below). In June 2016, the spread was 46 basis points. Lately, it’s been as low as 11. What I’m describing is happening at the long end of the curve, but it will soon spread to the short end. Currently, the difference between the three-month Treasury yield and the two-year yield is greater than the difference between the five-year and 30-year.

If this sounds like mumbo-jumbo, I’ll boil it down. Rates are going up, and that puts the squeeze on stock valuations. This week, the Fed released the minutes from its last meeting, and the members appear quite confident that rates need to go higher.

The futures market currently sees an 83% chance of a Fed hike next month. There’s a 66% chance of another rate hike in June and a 65% chance of a third hike in December. (There’s also a distant bet of four hikes by December. Yikes!)

The odd thing about the higher yields is that they’re due to a good thing: the improving economy. The unemployment rate is still low. This has been a very good earnings season for Wall Street. The “beat rate” is the highest since 2006. Economists expect more good numbers for Q1. Americans’ expectations for the economy are the second-highest since 2002.

What’s happening is that two counteracting forces are at play. The strong economy is boosting profits. In response, the rising economy is lifting interest rates. Stock valuations tend to move in a contrary direction to interest rates. In other words, the P/E Ratio is going lower while the “E” part of the equation is getting bigger. This means the “P” part, the prices, is kinda stuck in the middle.

It’s hard to fight a market with falling valuations. Those of you who have been with us for a while may remember Medtronic (MDT), which was on our Buy List from 2006 through 2014. While we had it, the company churned out good earnings. We were right about that. The problem was that earnings multiples seemed to sink lower every year which weighed on the stock’s performance. We were right on the big picture, but we got a lousy entry price. Lesson learned.

I want to be clear that I’m not predicting doom. Hardly. Instead, I’m saying that things are going to be different. The important takeaway for investors is that the stock market has been a lot more willing to shoulder risk. That normally happens with higher yields. If the one-year Treasury pays 0.1%, who cares? But now that it’s at 2%, you have to put in a little more effort at getting profits. I think it’s interesting that safe sectors like Utilities and Consumer Staples have been having a rough time.

You’ll notice that our Buy List has exposure to safe Consumer Staples along with deep Cyclicals like Wabtec (WAB) and Snap-on (SNA). We also have value plays like Carriage Systems (CSV) plus some more aggressive picks like Cognizant (CTSH). Make sure your portfolio is spread out like that. Now let’s look at our recent earnings reports.

Smucker Beats and Raises Guidance

Last Friday, JM Smucker (SJM) released fiscal Q3 earnings and they were quite good. The jelly folks earned $2.50 per share, but 35 cents was due to tax reform. Wall Street had been looking for $2.12 per share, so in real terms, we’re talking about a three-cent beat.

CEO Mark Smucker said:

“We had a strong third quarter, with sales growth for key brands in every business and strong earnings per share growth fueled by the benefits of U.S. income tax reform and ongoing cost discipline,” said Mark Smucker, Chief Executive Officer. “These results reflect our commitment to delivering top and bottom line growth and supporting our portfolio of iconic and emerging brands. In addition, the benefits of income tax reform provide incremental fuel to invest in our growth initiatives and support our employees and communities as well as opportunities to increase cash returned to shareholders.”

Thanks to tax reform, Smucker increased its full-year guidance. The company now sees adjusted EPS for this year ranging between $8.20 and $8.30 per share. That’s a big increase from the previous guidance of $7.75 to $7.90 per share. Smucker also gave a one-time bonus of $1,000 to nearly 5,000 employees. That’s good to see. We should never forget the people who are behind the great results.

Smucker has four divisions. Here’s a quick rundown. Their coffee group, which is the largest, saw profit growth of 6%. Consumer foods was up 2%. Pet food was down 7%. International was up 16% thanks to forex.

Initially, the shares dropped below $120 after the earnings report but have since gained ground. SJM closed Thursday at $122.84 per share. Going by the revised guidance, that’s less than 15 times earnings. A lot of these consumer staples are looking cheap. For now, I’m keeping our Buy Below on SJM at $130 per share.

Wabtec Rallies 16% in Two Weeks

On Tuesday, Wabtec (WAB) reported Q4 earnings of 90 cents per share. That’s not much of a surprise since that’s what they had told us to expect. For the year, the rail-services company made $3.43 per share.

Last year was a tough one for Wabtec, but it was also promising considering the integration of Faiveley.

Raymond T. Betler, Wabtec’s president and chief executive officer, said: “After a year of transition in 2017, during which we made excellent progress on the Faiveley integration and continued to invest in our worldwide growth opportunities, we are confident the company is positioned for improved performance in 2018. We have a record backlog, we’re seeing improvements in the freight aftermarket, and our Wabtec Excellence Program provides the fuel to increase margins over time. We are committed to achieving our 2018 plan and excited about Wabtec’s long-term growth prospects.”

For 2018, Wabtec expects sales to be about $4.1 billion and adjusted EPS to be about $3.80. They said they expect Q1 to be about the same as Q4, meaning 90 cents per share. Things are looking a lot better for Wabtec. The stock has rallied eight times in the last nine sessions. In the last two weeks, WAB is up 16%. This could be the start of an extended rally.

On Thursday, Hormel Foods (HRL) reported fiscal Q1 earnings of 56 cents per share. Of that, 12 cents was due to tax reform, so in practical terms, they made 44 cents per share in terms of continuing operations. That matched Wall Street’s consensus.

Hormel raised its FY 2018 guidance to a range of $1.81 to $1.95 per share. The previous range was $1.62 to $1.72 per share. The company is also raising its starting wage from $13 to $14 per share. In November, Hormel increased its dividend from 17 cents to 18.75 cents per share. That marked their 52nd annual dividend increase. That’s a lot of Spam.

Hormel has had a tough year so far. It’s our worst-performing stock (-9.3% YTD). As I said, these consumer staples have lagged badly. Still, the outlook for HRL is pretty good. This week, I’m lowering my Buy Below on Hormel to $36 per share.

Continental Beats and Fiserv Announces a 2-for-1 Split

Also on Thursday, Continental Building Products (CBPX) reported very good earnings for Q4. I was really impressed by these numbers. Sales rose 11.1% to $131.4 million. Wallboard sales volume increased from 666 to 725 million square feet. Earnings jumped 28% to 41 cents per share. Wall Street had been expecting 33 cents per share (my guess was 35 cents per share). EBITDA increased 10.1% to $37.2 million.

Like many other Buy List companies, tax reform had a big impact in Q4. For the year, sales were up 6%, and EPS rose 12.7% to $1.33. Continental also expanded its buyback program from $200 million to $300 million. All the numbers are moving in the right direction.

I know wallboard sounds like the most boring business imaginable, but it can be a profitable one as well. Continental is doing very well at the moment, and I think the shares are undervalued. The company offers guidance on several metrics except earnings, but I think they can hit $1.60 per share this year. Stick with this one.

We’re now entering the quiet period for Buy List earnings reports. Over the next seven weeks, we’ll only have three earnings reports. Ross Stores (ROST) is due to report on March 6. We then have two Buy List stocks with quarters ending in February; Factset Research Systems (FDS) will probably report in mid-to-late March, and RPM International (RPM) will report sometime in early April. After that, we won’t see anything until Q1 earnings season starts up in mid-April.

We also had another Buy List stock split. First it was AFLAC; now it’s Fiserv’s turn. Fiserv (FISV) announced on Thursday that it will split its stock 2-for-1. If you own FISV, you’ll get twice as many shares and the stock price will drop in half. Shareholders at the close of business on March 5 will get additional shares on March 19. This is Fiserv’s first split since 2013.

Before I go, I wanted to clarify a point I didn’t properly make. In the February 2 issue, I mentioned that AFLAC (AFL) raised its quarterly dividend from 45 to 52 cents per share. That’s correct, but I should have added that that’s on top of the two-cent dividend hike from October. AFLAC’s dividend is up 21% from a year ago. I’m lifting my Buy Below on AFLAC to $94 per share.

That’s all for now. Next Tuesday, we’ll get the latest durable goods report. On Wednesday, the government will update its report on Q4 GDP. Last month, the initial report said the economy grew by 2.6% in the last three months of the year. On Thursday, we’ll get the personal-income and spending data for January. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Syndication Partners

I’ve teamed up with Investors Alley to feature some of their content. I think they have really good stuff. Check it out!

Sell These Healthcare Middlemen About to Get Amazoned

A few weeks ago, I told you about the announcement from Amazon.com (Nasdaq: AMZN) that it was joining forces with JPMorgan and Warren Buffett’s Berkshire Hathaway to disrupt the healthcare industry. More specifically, the venture is being aimed at the many middlemen in the U.S. healthcare industry including insurance companies and pharmacy benefit management companies.

The focus on healthcare supplies is a smart move by Amazon since many hospital systems have been buying up medical practices as they move into the rapidly growing outpatient care market. However, most hospital distribution systems have not kept up and are still focused on just servicing the main hospital. Amazon can modernize their distribution system.

It’s also a savvy move because it doesn’t involve getting complex regulatory approvals. Many states don’t require a license at all to sell low-tech medical supplies. It’s the lowest-hanging ‘fruit’ in the very big healthcare market.

And once Amazon understands how to keep the shelves stocked with band aids and gauze, it shouldn’t be much of a stretch that it would move up the supply chain (while obtaining regulatory approvals) and begin to provide healthcare systems with medicines and high-tech medical devices.

The healthcare supply chain is a huge opportunity for a disruptive company like Amazon. The Wall Street Journal cited a November research report by Citigroup Global Markets Inc. that found fees, administration, marketing and shipping costs account for an estimated 20% to 30% of healthcare supply costs. As Rob Austin of Navigant Consulting said to the WSJ, “There’s a lot of people with fingers in the pie.”

In other words, more middlemen that are driving up the cost of healthcare for you and me and everyone else in the country. Middlemen that are just begging to be Amazoned. As Jeff Bezos famously said, “Your margin is my opportunity.”

So what middlemen companies are in the sights of Amazon in the healthcare supply chain? Check out my report.

3 REIT Dividend Increases Coming in March

As a dividend focused stock analyst, I put less emphasis on short term share price fluctuations and more on dividend yields and dividend growth prospects. When the market turns volatile, such as what we have experienced in the last several weeks, it is good to go back to the basics of dividend investing, which for me is dividend growth. A growing payout should, over time result in a higher share price. One nice way to get a quick start to capital gains from dividend growth is to buy shares just before an announced dividend increase.

I maintain a database of about 130 REITs, which I use to track yields and dividend growth. The typical REIT increases its dividend rate once a year, at about the same time each year. Across the REIT universe, the dividend increase announcements come in almost every month of the year. Each month I like to cover the REITs on my list that have historically increased their payouts in the following month. You can use this information to establish longer term positions in stocks with growing dividends or try for the short-term capital gain that often occurs when a dividend increase is announced. Here are three potential REIT dividend increases for March.

Posted by Eddy Elfenbein on February 23rd, 2018 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His