CWS Market Review – March 16, 2018

“Individuals who cannot master their emotions are ill-suited to profit from the investment process.” – Benjamin Graham

In recent issues, I’ve struck a cautious note to investors. After the brief correction of a few weeks ago, the market rebounded very quickly. Perhaps too quickly.

I still think there’s danger out there. The S&P 500 has now fallen for four days in a row. That’s hardly a disaster, but I’m noticing a few troubling trends just below the surface. I’ll explain more in a bit.

The economic news continues to be mostly positive. We got a very good jobs report last Friday. This week’s inflation report was quite tame, which is reassuring after the surprise from last month.

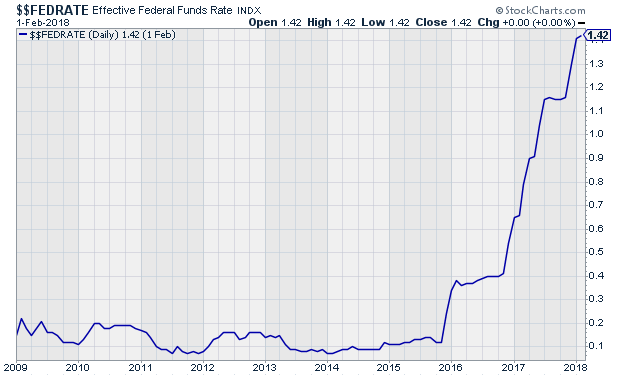

The big issue ahead is next week’s Fed meeting. The consensus is that the Fed will raise interest rates again. This would be the sixth rate hike of this cycle. But what comes next? That’s not so clear. I’ll lay out what it means for us, but first, let’s look at some of the cracks showing up in the bull market’s foundation.

Tech Has Dominated This Market and It Can’t Last

I have to be up front. This is going to be a rather slim issue because, well…there’s not much going on in the market right now. But that will change very soon.

What has me concerned recently is the divergence between growth stocks and value stocks. The expected relationship is that growth leads value during a bull market, and value grabs the upper hand during a bear market. This time, growth has been giving value a super-atomic wedgie almost nonstop since the middle of 2007.

Value shone briefly in late 2016, after the election. But since the beginning of 2017, growth has been tearing up value. We can see this effect in a few other areas. For example, while the S&P 500 is still well below its all-time high from January, the NASDAQ Composite recently powered its way to a seven-day winning streak and it struck a few new all-time highs.

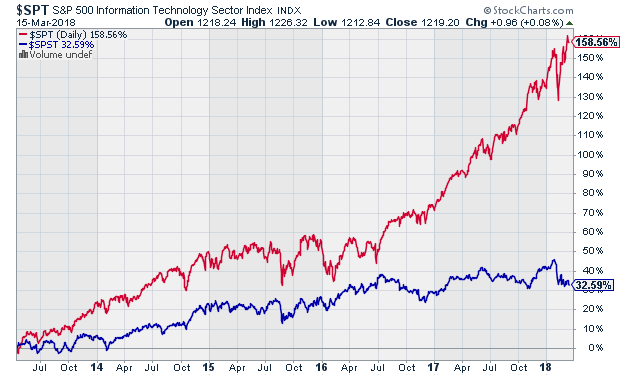

When we look at classic safe-haven sectors like Utilities, REITs and Consumer Staples, they’ve been left behind. On our Buy List, we can see this in the performance of stocks like Hormel Foods (HRL) and Ingredion (INGR). Meanwhile, the Tech Sector ETF (XLK) seems like it never goes down. Don’t be lured in (note today’s epigraph). Tech has done much of the heavy lifting for this market. The chart below shows the tech sector in red and the consumer staples in blue. Excluding a few high-profile stocks, the overall rally hasn’t been as impressive as it appears.

This trend can’t last. I don’t know when it will end, but we’re closer to the end than to the beginning. I’m not predicting a crash or market blowup, but I do think we may soon see a change in market leadership.

What to do now? Investors should continue to focus on high-quality stocks. On our Buy List, I especially like some of the names that have lagged recently. Ross Stores (ROST) looks quite good especially after its earnings report and dividend hike. JM Smucker (SJM) is going for less than 14 times next year’s earnings. That’s a good deal. Another Buy List stock that’s looking good here is Alliance Data Systems (ADS). In January, ADS creamed earnings, raised guidance and hiked its dividend.

About technology, I was also struck by two key news stories this week. The first is that the government blocked Broadcom’s attempt to buy Qualcomm. Let’s skip over the debate over whether it made business sense or if it’s the right government policy. The fact is that they did it, and this is a big change. Twenty years ago, this kind of merger would have barely raised an eyebrow. Those days are gone.

The other news was that President Trump is planning to impose tariffs on up to $60 billion worth of Chinese imports. I’m not sure how firm the administration is on these plans. I know some people think this is the president’s “opening bid” in an effort to gain concessions later on.

I highlight these stories because I think they quietly signal the end of the post-war consensus on economic issues. For over 25 years, the global economy has moved toward free trade and relaxed regulations. Sure, there have been bumps and bruises along the way, but the free-market orthodoxy has held the higher ground. These two events of this week show that the old conventional wisdom no longer holds.

Preview of Next Week’s Fed Meeting

The Federal Reserve meets again next week. This will be the first meeting with Jay Powell as chairman. The central bank is expected to raise interest rates again. However, what comes next is the big question.

Powell will hold a post-meeting press conference, and the Fed will release updated economic projections. This is what I’m most interested in. In previous projections, the Fed has said it will raise interest rates three times this year. Wall Street seems to buy that. However, there’s a growing belief that they may raise rates a fourth time before the end of the year. That’s quite extraordinary.

Personally, I think the chances of four hikes are remote, but the futures markets currently put the odds at 33%. Seven months ago, the odds were at 0.05%. There are a few factors driving this thesis. The first is that inflation might heat up. There was some concern that the inflation report for January might come in hot. Fortunately, this week’s CPI report showed that inflation was much more subdued in February. I still don’t think inflation is an issue.

There’s also a chance that the economy could be revising up, and that may require elevated rates. It’s possible, but I don’t see the hard evidence just yet. I should note that last Friday’s jobs report (+313,000) was quite good.

There’s also a concern that the budget deficits are unusually high for this point in the cycle. That’s certainly true, but foreign investors seem quite happy to finance our spending. I had a little concern this week when investors weren’t particularly enthusiastic about the recent Treasury auctions. In the bond market, they like to watch the “bid to cover ratio.” That’s simply how much interest there is in the Treasury auction. This week’s auction had some of the weakest ratios in years.

I think of this as an early test of the Trump administration’s fiscal policy. If China, Japan and other countries still gobble up our bonds, then it’s no problem. If not, that’s going to mean higher interest rates. In turn, that means tougher competition for the stock market. It’s not a major issue now, but there’s a chance it could become one down the road.

There hasn’t been much in the way of Buy List news recently. Our next Buy List earnings report will come from FactSet Research Systems (FDS) on March 27. The one after that is RPM International (RPM) on April 5.

We also have two stock splits coming up. AFLAC (AFL) will split 2-for-1 on March 16, and Fiserv (FISV) splits 2-for-1 on March 19. So don’t be alarmed when you see the lower share prices. Our Buy Below prices will split as well.

I should also mention that on Tuesday, AFLAC made a new all-time high. If you recall, the shares plunged 7.4% on January 12 after a negative article appeared. As usual, the long term works to the advantage of superior companies.

That’s all for now. The big news next week will be the Federal Reserve meeting. This will be a two-day affair (Tuesday and Wednesday). Also on Wednesday, we’ll get the latest report on existing-home sales. Then on Friday, the government reports on durable goods. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Syndication Partners

I’ve teamed up with Investors Alley to feature some of their content. I think they have really good stuff. Check it out!

Sell These 3 Stocks as Amazon Takes Over Banking

Executives across the world are asking themselves the same question: is there no end to the ambitions of Jeff Bezos and Amazon.com (Nasdaq: AMZN)?

A good question since it looks like the company nicknamed the “Death Star” (after the moon-sized, planet-killing weapon from Star Wars) is set to take aim at another industry. Just recently, Amazon seemed to be setting its sights on the freight delivery industry then on the healthcare industry and now its seems to be getting ready to target the financial industry. Although as with healthcare, Amazon is in talks with possible established partners in the sector.

Now Amazon has its sights set on the banking industry. Find out what three financial stocks you need to sell right now to avoid the wrath of the Death Star!

3 REITs Increasing Dividends in April

With a pending interest rate increase from the Fed, I have been receiving questions on whether REIT values will be hurt by rising interest rates. It is a widely held – but inaccurate – belief that REIT values must fall if interest rates continue to increase. The fact that many REITs increase their dividends over time tells us that these are businesses with the potential for growing dividends and share values even in a rising rate environment.

Recently, I read an article that looked at the history of REIT values and interest rates. Since 1995, there has been 15 periods of significantly rising interest rates. Out of those 15, REIT values increased 12, or 75% of the time. In the period from June 2004 through August 2006 the Fed increased rates 16 times. During that period REITs outperformed the S&P 500, 59% to 22%.

The fact is that REIT results are driven more by economic conditions, rising commercial real estate values, and the ability of REITs to increase the rental rates on their properties. We can monitor how well a REIT is performing from its history of dividend growth. Most REITs announce any dividend increases once a year, in the same month each year.

Across the sector there are increase announcements in almost every month in the calendar. You can often get a nice share price gain by buying shares before a dividend increase announcement hits the news wires. I maintain a database that covers about 140 REITs. I use the database to track dividend rates, yields and increases. Of the 140, about 90 have histories of regular dividend increases. Here are three REITs that should announce a dividend increase in April.

Posted by Eddy Elfenbein on March 16th, 2018 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Tweets by @EddyElfenbein

-

-

Archives

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His