Archive for April, 2018

-

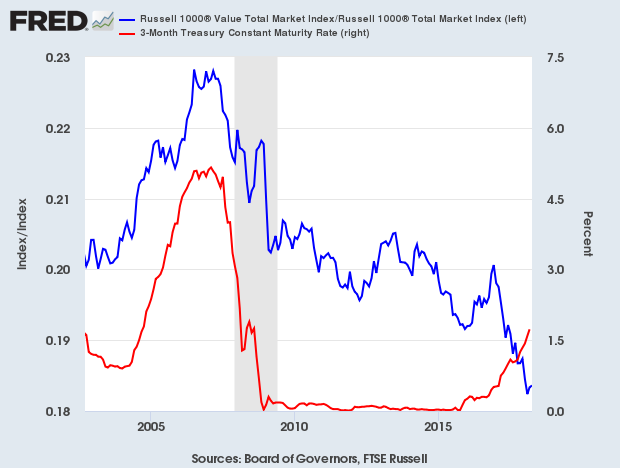

Is Value No Longer Value?

Eddy Elfenbein, April 30th, 2018 at 1:33 pmThis weekend’s Barron’s had an interesting article touting the turn for value. They may be right, but it’s been a rough time for value. The Russell 1000 Value Index peaked against the regular Russell 1000 in August 2006. In other words, Value has been lagging the market for nearly 12 years.

What’s interesting is that Value tends to lead when short-term rates are rising. But since the Fed started hiking rates, Value has continued to trail. Check out the last part of this chart:

What’s going on? Is Value about to catch up, or is the relationship broken. In finance, whenever I see a relationship diverge, I try to not blame the market. Instead, it’s likely that whatever drove the previous relationship has broken down.

-

Personal Income and Spending for March

Eddy Elfenbein, April 30th, 2018 at 10:12 amThis morning, we got reports on personal income and spending for March. Personal spending rose by 0.4% which matched estimates. Personal income rose by 0.4% which was 0.1% below estimates.

Here are both series for the last 15 years:

-

Does Sell in May Really Work?

Eddy Elfenbein, April 30th, 2018 at 10:03 amThere’s an old saying on Wall Street to “sell in May and go away.” And to be very formal, one can add, “don’t come back till St. Leger day.”

So…is this true? The answer is “historically, yes.”

I took all the numbers of the Dow Jones Industrial Average from its first day of trading in 1896 until the end of 2017. Here’s how it works out. From May 6 through October 29, the DJIA has had an average gain of 0.49%. The rest of the year, the index has averaged 7.11%. (Note that these numbers don’t include dividends.)

In other words, for half the year, the Dow has been flat, and the entire historic gain has come during the other half of the year.

But what does this mean for investors? The answer is nothing. It’s interesting how market returns have worked out over a very long period, but it tells us nothing about a coherent investing strategy. To go in and out of the market will bring up fees and taxes, among other headaches.

Ryan Detrick noted that if you sold in May during the past six years, you lost out on five up Mays. The average gain was 4.8%. The one down year was just 0.3%.

-

Morning News: April 30, 2018

Eddy Elfenbein, April 30th, 2018 at 7:07 amU.S. Allies Brace for Trade War as Tariff Negotiations Stall

China Prepares a Hard-Line Stance on Trump’s Trade Demands

SoftBank’s Prodigal Son Makes a Costly Flip-Flop

T-Mobile Agrees to Buy Sprint in $26 Billion Deal

Marathon to Buy Andeavor in $23.3 Billion Oil-Refining Deal

In Age of Amazon, a Warehouse Powerhouse Is Getting Even Bigger

Netflix And Amazon Join The Battle Against Kodi Pirates

Walmart Sheds Grow-Everywhere Plan in Refining Global Strategy

Apple Results to Show iPhone Growth Problem and Cook’s Plan to Fix It

AT&T Court Fight With U.S. Justice Department Heads Into Closing Arguments

Top Performing Global Junk Bond Fund Is Moving Out of Junk

4 Mistakes That’ll Slash Your Social Security Benefits

Jeff Miller: Will Strong Economic Data Send Interest Rates Higher?

Joshua Brown: World’s First AI-Driven Finance Columnist Proves Its Mettle

Howard Lindzon: Buy in May Go Away

Be sure to follow me on Twitter.

-

Moody’s Earned $2.02 per Share

Eddy Elfenbein, April 27th, 2018 at 12:00 pmThis morning, Moody’s (MCO) reported Q1 earnings of $2.02 per share. Revenue rose 16% to $1.1 billion. The company also reaffirmed full-year earnings of $7.65 to $7.85 per share.

Moody’s record first quarter revenue reflects a strong contribution from Bureau van Dijk and solid organic growth from Moody’s Analytics, as well as strength in rated structured finance volumes in Moody’s Investors Service,” said Raymond McDaniel, President and Chief Executive Officer of Moody’s. “Our business remains well-positioned to benefit from continued global economic expansion in 2018, and as such we are affirming our full year 2018 guidance of $7.20 to $7.40 for diluted EPS and $7.65 to $7.85 for adjusted diluted EPS.

(…)

Operating expenses totaled $635.9 million, up 20% from the prior-year period, including 12 percentage points attributable to Bureau van Dijk operating expenses, amortization of acquired intangible assets, as well as non-recurring acquisition and integration expenses associated with the Bureau van Dijk acquisition (“Acquisition-Related Expenses”).

Operating income was $490.8 million, up 10% from the first quarter of 2017. Adjusted operating income, which excludes depreciation and amortization, as well as Acquisition-Related Expenses, was $540.7 million, up 13% from the prior-year period. Operating margin for the first quarter was 43.6% and the adjusted operating margin was 48.0%.

Diluted EPS of $1.92 was up 8% from the first quarter of 2017. Adjusted diluted EPS of $2.02 was up 35%. First quarter 2018 adjusted diluted EPS excludes $0.10 per share related to amortization of acquired intangible assets and Acquisition-Related Expenses. First quarter 2017 adjusted diluted EPS primarily excludes a $0.31 per share non-cash, non-taxable gain from a strategic realignment and expansion involving Moody’s China affiliate China Cheng Xin International Credit Rating Co. Ltd. (“CCXI Gain”). Both first quarter 2018 diluted EPS and adjusted diluted EPS include a $0.15 per share tax benefit related to the adoption of accounting standard update ASU 2016-09, “Improvements to Employee Share-Based Payment Accounting,” compared to a $0.10 per share tax benefit in the first quarter of 2017.

-

Q1 GDP Grew by 2.3%

Eddy Elfenbein, April 27th, 2018 at 11:51 amThis morning, the government said the economy grew by 2.3% in Q1. Economists has been expecting growth of 1.8%. Spending by consumers rose by just 1.1%.

The economy grew at a 2.9 percent pace in the fourth quarter. Economists polled by Reuters had forecast output rising at a 2.0 percent rate in the January-March period.

The first-quarter growth pace is, however, probably not a true reflection of the economy, despite the weakness in consumer spending. First-quarter GDP tends to be sluggish because of a seasonal quirk. The labor market is near full employment and both business and consumer confidence are strong.

Economists expect growth will accelerate in the second quarter as households start to feel the impact of the Trump administration’s $1.5 trillion income tax package on their paychecks. The tax cuts came into effect in January.

Lower corporate and individual tax rates as well as increased government spending will likely lift annual economic growth to the administration’s 3 percent target, despite the weak start to the year.

Here’s quarterly growth in real GDP:

Here’s a look at rolling NGDP growth. It’s been close to 4% for several years.

-

CWS Market Review – April 27, 2018

Eddy Elfenbein, April 27th, 2018 at 7:08 am“If you have trouble imagining a 20% loss in the stock market, you shouldn’t be in stocks.” – Jack Bogle

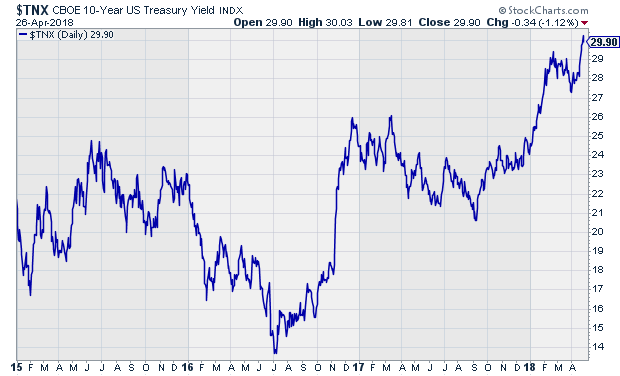

On Tuesday, the yield on the 10-year Treasury bond broke above 3% for the first time since 2014. Less than two years ago, the 10-year was going for a measly 1.37%. The increase isn’t surprising; the economy is getting better and the Federal Reserve has been raising interest rates.

But it does remind us that the investing climate is changing. For a long time, bond yields were so low that the financial markets were practically begging you to buy stocks. Investors responded. In less than nine years, the Dow quadrupled.

Now things are different. Bonds are much tougher competition. As a result, the stock market has become far more discerning. We’re currently in earnings season, and we can see how swiftly the market gods have rewarded or punished stocks. So far, every Buy List stock has beaten Wall Street’s earnings estimate. We’re 11-0. But not all of our stocks have performed well following their earnings.

In this week’s CWS Market Review, I’ll run down our earnings reports from this week. I’ll also preview seven more coming next week. It’s been a busy week and there’s a lot to get to, so let’s jump into this week’s earnings. Don’t forget, you can always see our complete Earnings Calendar.

This Week’s Buy List Earnings

On Tuesday, three of our stocks reported. Let’s start with Wabtec (WAB), the freight services company. Wabtec reported Q1 earnings of 92 cents per share which beat estimates by two cents per share.

The good news is that Wabtec reaffirmed their full-year guidance. They expect revenue of $4.1 billion and earnings of “about” $3.80 per share, excluding restructuring costs.

The CEO said:

Our first-quarter results exceeded our expectations slightly and represent a solid start to the year. With a record backlog and the positive indicators we’re seeing in our core markets, we are well positioned to meet our financial targets in 2018.

It’s now an open secret on Wall Street that GE may sell their transportation business to WAB. This would be a huge deal. Expect more details soon. Fortunately for us, the stock has been behaving much better recently. WAB gapped up 2.6% on Tuesday to touch a nine-month high. This was a good earnings report. This week, I’m lifting my Buy Below price on Wabtec to $93 per share.

Sherwin-Williams (SHW) also reported earnings on Tuesday, but their report is a bit complicated. The company had Q1 earnings of $3.57 per share, which beat expectations by 41 cents per share, but there are some accounting issues related to the Valspar acquisition.

The $3.57 figure includes 24 cents per share in transaction costs and 71 cents per share in “accounting impact” costs. On the plus side, Valspar added $1.08 per share in net income. The net debt charge from Valspar was 40 cents per share.

Thanks to that 40-cent charge, Sherwin reduced its full-year guidance by 40 cents per share. The company now expects full-year EPS of $18.35 to $18.95 (excluding any Valspar issues). Wall Street had been expecting $19.14 per share.

I apologize if this sounds confusing – I’ll try to summarize as briefly as I can. Sherwin’s business is going well. Very well, in fact. However, they’re having more trouble than expected with the Valspar merger. In the long run this deal should pay off for us, but for now, I’m dropping my Buy Below down to $400.

After the bell on Tuesday, Carriage Services (CSV) posted Q1 earnings of 59 cents per share. Only two analysts follow the stock, so it’s not completely accurate to call it a consensus. For my part, I was expecting something around 50 to 52 cents per share. The CEO, Mel Payne, said, “We got off to a good start in 2018 by setting numerous historical first quarter performance records.”

Revenue rose 7.7% to $73.4 million, and EBITDA was up 5.8%. The downside is that they’re lowering their guidance. They gave three reasons for the lower guidance: an acquisition that didn’t close in Q4 as expected, rising interest costs on their floating rate debt, and a higher share count related to convertible debt and recent increase in share price.

For the rolling four quarters ending in March 2019, Carriage expects revenue of $274 to $277 million and earnings of $1.80 to $1.85 per share. That’s a decrease of 20 cents per share at both ends. The decrease in the midpoint of the revenue range is just 2.5%. The stock pulled back after the report, but the current valuation is pretty low. Don’t let this glitch worry you. Carriage remains a buy up to $28 per share.

On Wednesday morning, Check Point Software (CHKP) had a decent earnings report, but the stock took a hit after they lowered guidance. The details aren’t quite as bad as the stock action suggests.

The issue is that Check Point has been shifting their business towards a greater reliance on subscription revenue. The problem is that these subscriptions boost results in higher deferred revenue. It’s also been taking CHKP a long time to close deals for their new Infinity Total Protection product.

Let’s dig into the numbers. For Q1, Check Point reported earnings of $1.30 per share. That was two cents better than estimates. Revenue rose 4% to $452 million, and cash flow from operations increased by 18% to $419 million. They had previously given Q1 guidance for earnings between $1.25 and $1.30 per share and revenues of $440 to $460 million.

Now we get to the disappointing news, which is the weak guidance. For Q2, Check Point expects revenue to range between $445 and $475 million. Wall Street had been expecting $477 million. For Q2 EPS, their range is $1.25 to $1.35. Wall Street had been expecting $1.35 per share.

Check Point also cut their full-year earnings range. The previous guidance was $5.50 to $5.90 per share. The new range is $5.45 to $5.75 per share. They also lowered their full-year revenue forecast from $1.9 billion – $2 billion to $1.85 billion – $1.93 billion.

In Wednesday’s trading, shares of CHKP fell 6.4%. Don’t give up on Check Point; this is a strong company. I’m cutting my Buy Below on CHKP to $105 per share.

Also on Wednesday, AFLAC (AFL) reported Q1 operating earnings of $1.05 per share. Favorable forex boosted that figure by three cents per share. Wall Street had been expecting 97 cents per share.

The duck stock is standing by its earnings forecast for full-year earnings of $3.72 to $3.88 per share (remember, the stock recently split 2 for 1). For Q2, AFLAC expects earnings to range between 91 cents and $1.05 per share. Wall Street had been expecting 99 cents per share. AFLAC’s guidance assumes the yen averages between ¥100 and ¥110 to the dollar. Lately, it’s been creeping up to about ¥109.

This is basically what I expected. On Thursday, the shares touched a new all-time high. I’m lifting our Buy Below to $50 per share.

Stryker (SYK) reported after the close on Thursday, and it was a good one. For Q1, they earned $1.68 per share which was eight cents above the Street. Previously, the company had given a forecast range of $1.57 to $1.62 per share.

CEO Kevin Lobo said, “We had an excellent start to 2018 with strong organic sales growth, operating margin and adjusted EPS in the first quarter.” For Q1, their quarterly operating margin was 25%. That’s very good.

Stryker also raised their full-year forecast. Their initial range was $7.07 to $7.17 per share. Now they see 2018 coming in between $7.18 and $7.25 per share. It seems they’re basically adjusting for the eight-cent beat. For Q2, Stryker expects $1.70 to $1.75 per share. Wall Street had been expecting $1.70 per share. This was a very good quarter for Stryker.

Moody’s (MCO) will be reporting later today. They’re looking for 2018 earnings of $7.65 to $7.85 per share. They made $6.07 per share in 2017. For Q1, Wall Street expects earnings of $1.80 per share.

Seven Earnings Reports Next Week

We have seven more Buy List earnings reports next week.

Fiserv (FISV) will kick things off on Tuesday, May 1. Last year was their 32nd year in a row of double-digit earnings growth. There’s a very good chance that 2018 will be year #33. Fiserv expects earnings this year of $6.05 to $6.30 per share. Wall Street expects Q1 earnings of 73 cents per share. I think Fiserv will beat that.

Cerner (CERN) has been a bit of a flop for us this year which is surprising. The company missed earnings for Q4. I’m not worried just yet but I want to see signs of improvement. The company is due to report on Wednesday, May 2. Cerner expects Q1 earnings of 57 to 59 cents per share and 2018 earnings of $2.57 to $2.73 per share.

We have a very busy day planned for next Thursday, May 3. Five of our Buy List stocks are due to report.

Becton, Dickinson (BDX) had a very good report for Q4, and the company continues to be optimistic about the CR Bard acquisition. This has been a great opportunity for us. For 2018, Becton is looking for earnings to range between $10.85 and $11.00 per share. That’s a very good range, and it’s surprisingly narrow for a full-year forecast. For Q1, Wall Street is looking for $2.63 per share.

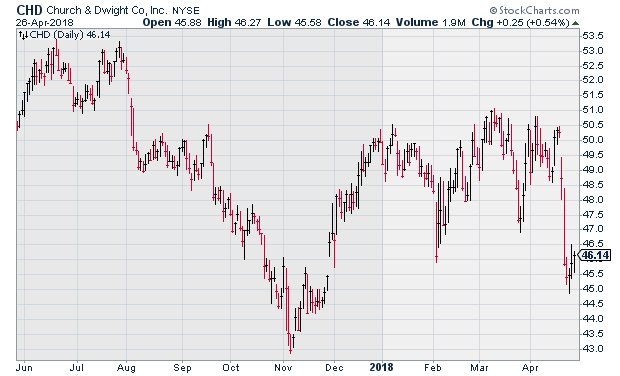

Church & Dwight (CHD) has been pretty weak lately. The stock dipped last week after some big-name consumer staples posted disappointing results. This is puzzling to me. CHD’s CEO recently said “they’re hitting on all cylinders.” For 2018, they expect EPS to range between $2.24 and $2.28. That’s growth of 16% to 18%. For Q1, Church & Dwight expects earnings of 61 cents per share on organic sales growth of 2%.

On the surface, Continental Building Products (CBPX) is a boring wallboard company. Actually, they’re the same below the surface as well, but they’re a very good business. Continental offers guidance on several metrics except earnings, but I think they can hit $1.60 per share this year. The consensus for Q1 is for 36 cents per share. I think they can beat that.

Ingredion (INGR) is another Buy List stock that’s been off to a poor start this year. The plant-food company missed Q4 earnings by two cents per share. The stock is going for a good value here. For 2018, Ingredion said they see EPS ranging between $8.10 and $8.50. That means the stock is going for around 15 times earnings.

Last is Intercontinental Exchange (ICE). I like the stock-exchange operator a lot but for several weeks, the stock has been stuck in a range between $70 and $75. The company recently sealed a deal to buy the Chicago Stock Exchange. That was a good move. The consensus for Q1 is for 88 cents per share. I’m expecting a beat.

That’s all for now. Earnings season will continue to dominate the news next week. On Tuesday and Wednesday, the Federal Reserve meets again. Don’t expect any action from the Fed. The policy statement will come out at 2 pm on Wednesday. Then on Friday, the April jobs report comes out. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Syndication Partners

I’ve teamed up with Investors Alley to feature some of their content. I think they have really good stuff. Check it out!

3 Cloud Computing Companies Racing to Push Cloud Computing Aside

The technology research firm Forrester Research says that the Internet of Things – and the coming deluge of sensors and data – make a good bit of cloud computing passé. It will be more practical and efficient to process all of this data right on the spot where it is being collected.

In other words, data will be processed not in a centralized cloud, but at the edge of the network. Thus you get the term ‘edge computing’.

In October 2017, the IT research firm Gartner estimated that by 2022, half of all data generated by businesses will come from smart edge devices – IoT sensors as well as smartphones and PCs – rather than from the cloud or their own data centers.

This new reality in computing suggests to me the best way to invest in edge computing, while still keeping exposure to cloud computing, is through certain stocks.

3 High-Yield Energy Stocks to Buy as Crude Oil Continues to Climb

After two-and-a-half years of giving income investors false hopes of a recovery, the energy infrastructure sector is now ready to stage a sustained positive price trend. Investors are renewing interest in these sectors. Now is the time to buy into these companies for attractive current yields, dividend growth and price appreciation.

Energy infrastructure (also called energy midstream) companies provide the assets and services which move energy commodities (crude oil, natural gas, refined products and natural gas liquids, also referred to as NGLs) from the production areas to the end users. The assets in the sector include pipelines, storage facilities, processing facilities, and all kinds of terminals.

Prior to 2015, the master limited partnership (MLP) was the prevailing business structure for energy midstream companies. Now the sector is close to a balanced mix of MLPs and corporations. At the present time, the higher yields come from the MLPs. This means these companies have more upside price potential has yields between them and the corporate shares become similar for companies with comparable business results. Most MLPs report tax information on what’s called a Schedule K-1. For my Dividend Hunter subscribers, I search out Form 1099 reporting energy infrastructure investments.

Here are three midstream companies with high current yields, continuing dividend growth, and strong business prospects.

-

Morning News: April 27, 2018

Eddy Elfenbein, April 27th, 2018 at 6:59 amU.K.’s Worst Growth Since 2012 Sinks Pound on Rate Hike Doubts

G.D.P. Report on Friday Morning: An Early Read on 2018

Being Jeff Bezos Means Never Apologizing About Profits

It Seems A Pretty Big Deal Ford’s New Focus Won’t Have A Focus

Intel’s Higher Profit Shows Firm Shaking Off Chip Flaws

T-Mobile, Sprint Make Progress in Talks, Aim For Deal Next Week

Facebook May Look Bulletproof, But It’s Bracing Investors For Bad News

UPS’s Balancing Act: More Packages, Less Spending

Pepsi and Coke Are Fighting to Get You to Drink Soda Again

Daimler Edges Up Profit Forecast as Luxury Cars Offset Spending

Microsoft Sales Top Estimates, Fueled by Strong Cloud Demand

Jury Awards Neighbors of North Carolina Hog Farm $50 Million In Nuisance Case

Ben Carlson: 50 Ways the World is Getting Better

Blue Harbinger: Ominous Vomiting Camel Formation

Michael Batnick: Animal Spirits: The Collaborative Podcast

Be sure to follow me on Twitter.

-

Recent Buy List News

Eddy Elfenbein, April 26th, 2018 at 6:27 pmEarnings news has been dominating the scene for the past several days but I wanted to pass along some other news items impacting our stocks.

GE Rebuffed Danaher Bid to Buy Life-Sciences Unit

Hormel Mulls Bid for $600 Million Chinese Wasabi Maker

GE Is Said in Talks to Unload Rail Unit in Deal With Wabtec

Fiserv Technology Will Enable Voice Banking on Amazon Alexa This Year

-

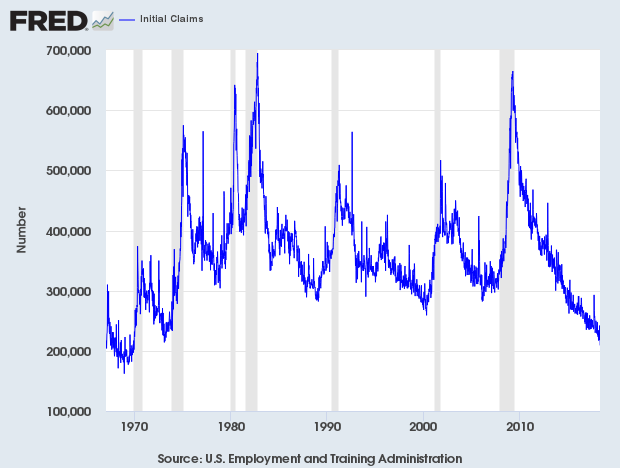

Initial Claims Lowest Since Altamont

Eddy Elfenbein, April 26th, 2018 at 11:03 amToday’s initial claims report was just 209,000. That’s the lowest number since December 6, 1969, which was the same day as the Altamont concert.

Also this morning, the durable goods report for March showed an increase of 2.6%, but much of that was due to a big batch of orders for Boeing. Orders for non-defense capital goods excluding aircraft fell by 0.1% last month.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His