CWS Market Review – April 20, 2018

“To achieve satisfactory investment results is easier than most people realize; to achieve superior results is harder than it looks.” – Benjamin Graham

Earnings season is upon us, and so far, things are looking good. We’ve had five Buy List earnings reports this week, and all five beat Wall Street’s consensus. You can always check out our latest Earnings Calendar.

In this issue, I’ll run though all of our reports. I’ll also profile seven more earnings reports coming our way next week. Remember, things can get much more volatile for individual stocks after their earnings reports, so don’t be scared by a little more action.

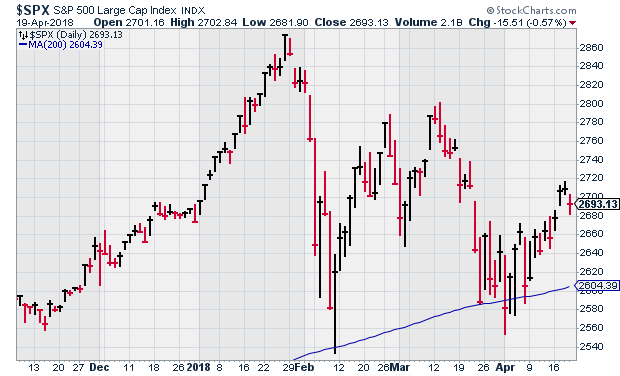

Fortunately, the stock market has been more buoyant recently. At one point, the S&P 500 rallied eight times in 11 sessions, and on Wednesday, the index closed at a four-week high. But don’t be complacent. I still think there’s a good chance the market will test the lows.

If you’re into numbers, I can remind you that the closing low from February 8 was 2,581.00, and the one from April 2 was 2,581.88. That’s how close we came to a new low. This tells me that the bears haven’t been scared off. More on that later. For now, let’s look at some earnings.

This Week’s Five Buy List Earnings Reports

We had five of our Buy List stocks report earnings this week. I’m happy to say that all five beat estimates. However, not all five got a lift from the news. Let’s run through the reports.

Torchmark (TMK) led off earnings season for us after the bell on Wednesday. The insurance company reported Q1 earnings of $1.47 per share. That was two cents more than estimates. For last year’s Q1, Torchmark made $1.15 per share. This one is as steady as they come.

One of the key stats for Torchmark is Return on Equity that excludes unrealized gains on fixed income. That’s kind of a mouthful, but it’s one of the best ways to measure the company’s performance. For Q1, this metric came in at 14.6%, which is quite good. The company is experiencing healthy growth across its different business units.

In the earnings release, Torchmark said they see 2018 EPS coming in between $5.93 and $6.07 per share. That’s probably a tad low. I think TMK can hit $6.10 per share, but I won’t quibble with their guidance; we’re still early in the year. The guidance implies the stock is going for a decent valuation. Shares of TMK gained 1.8% in Thursday’s trading. I’m pleased with this news, and I’m raising our Buy Below on Torchmark to $91 per share.

On Thursday morning, we got four more Buy List earnings reports. I had been a little nervous coming into the earnings report for Alliance Data Systems (ADS). The stock has plunged since the last earnings report. Alliance reported Q1 core earnings of $4.44 per share. The good news is that that easily topped Wall Street’s estimate of $4.23 per share. The bad news is that the estimate had been severely pared back over the last several weeks. Not too long ago, the Street had been expecting over $5.10 per share for Q1. Quarterly revenue rose to $1.88 billion which was a little bit below forecasts.

Alliance’s CEO, Ed Heffernan, said, “This quarter’s pro-forma revenue growth of 4 percent and core EPS growth of 13 percent should reflect our softest quarter of the year. Specifically, higher reserve levels required to cover the transitory impacts of the internal recovery investment was an approximate $0.60 hit to core EPS for the first quarter. Moving forward, recovery rates should move in our favor.”

ADS reiterated its full-year guidance of $22.50 to $23 per share with revenue of $8.35 billion. I was pleased to see that. Still, the shares dropped 4.5% at Thursday’s open, but then they regained their composure later in the day and only closed off by 0.9%. Just to be safe, I’m dropping my Buy Below down to $232 per share.

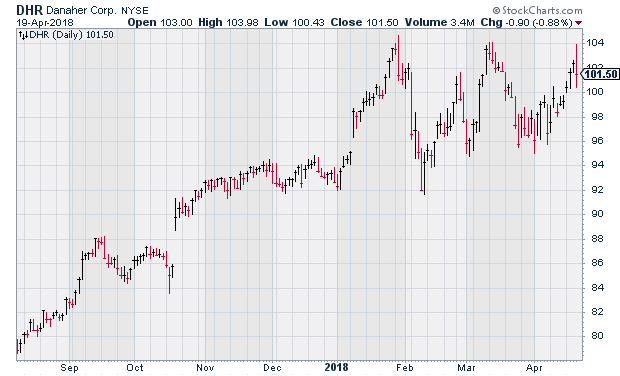

Danaher (DHR) had a very good report for Q1. The company made 99 cents per share. If you recall, they initially provided Q1 guidance of 90 to 93 cents per share. DHR later said they’ll beat that thanks to strong results from their Life Sciences and Diagnostics platforms, “specifically at Cepheid.”

For Q2, Danaher sees earnings of $1.07 to $1.10 per share. Wall Street had been expecting $1.08 per share. The best news is that Danaher raised its full-year guidance. The old range was $4.25 to $4.35 per share. The new range is $4.38 to $4.45. Last year, DHR made $4.03 per share. Danaher remains a buy up to $105 per share.

Also on Thursday, Signature Bank (SBNY) reported Q1 earnings of $2.69 per share. That was two cents better than estimates. Signature’s results for Q1 are a bit distorted because they took a big write-down for their taxi medallion loans.

Let’s look at some metrics. Deposits rose 4.1% to $34.82 billion. Net interest margin was 3.01%. Thanks to the medallion loans, Signature’s efficiency ratio rose to 42.2%. This measures a bank’s net interest expense as a share of its total income. The lower, the better.

Excluding the medallion loans, Signature is doing just fine. The problem for the last few quarters was that that’s a hard thing to exclude. Fortunately, SBNY is moving beyond that. I still think SBNY can earn $11 per share this year. The shares lost 3.1% on Thursday. I still like SBNY. This week, I’m dropping my Buy Below to $142 per share.

Our big winner this week is Snap-on (SNA). On Thursday, the company reported Q1 earnings of $2.79 per share. I’ve been concerned by weakness in their tool group, and that’s still an issue. For Q1, organic sales rose by just 0.8%. The good news is that their other business units are picking up the slack.

I think this is a case of Wall Street expecting the worst. When the worst didn’t come, the stock rallied. By the closing bell, shares of SNA had gained 6.2%. It was the second-best performer in the S&P 500 for the day. I’m keeping our Buy Below at $167 per share. Now let’s take a look at some of next week’s reports.

Seven Buy List Earnings Reports Next Week

Next week is going to be another crowded week for earnings. Here’s a rundown.

On Tuesday, April 24, three Buy List stocks are ready to report. Carriage Services (CSV) may be a dark-horse winner for us this year. The stock is already our third-best performer so far. The funeral-home company had a rough year in 2017, but things seem to have turned the corner. The last earnings report was a good one. Carriage also increased its earnings guidance.

Only two analysts on Wall Street follow the stock, so I really can’t say there’s an earnings consensus. I’m expecting Q1 earnings around 50 to 52 cents per share. The stock is going for an attractive valuation.

For Q4, Sherwin-Williams (SHW) gave us an earnings dud. I’m hoping this won’t become a habit. The problem is that they’re still adjusting to their big merger with Valspar. Some headaches are to be expected. In the long run, this deal should pay off. For 2018, Sherwin expects earnings in the range of $16.05 to $16.45 per share. Wall Street is looking for $3.16 per share for Q1.

Wabtec (WAB) had a strange time during its last earnings report. The shares dropped when the company released preliminary results, but then they snapped back just before the actual results. For Q1, Wabtec said they’re expecting similar results as Q4. Since they made 90 cents per share for Q4, I’m assuming 90 cents or so for Q1. For all of 2018, Wabtec is looking for earnings of “about” $3.80 per share. The stock has been acting better in recent weeks.

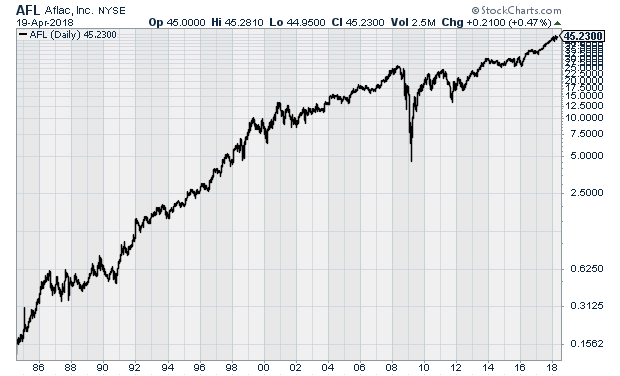

On Wednesday, AFLAC (AFL) is due to report Q1 earnings. I’m a big fan of the duck stock. Check out this 34-year log chart of AFLAC.

For 2018, AFLAC is looking for earnings to range between $3.73 and $3.88 per share ($7.45 and $7.75 pre-split). That assumes a yen/dollar rate of 112.16 which was the average for 2017. For Q1, Wall Street is looking for earnings of 97 cents per share.

Also on Wednesday, Check Point Software (CHKP) is due to report. The company had a very good report three months ago. For Q1, Check Point sees earnings between $1.25 and $1.30 per share on revenues of $440 to $460 million. For the full year, they see EPS of $5.50 to $5.90 on revenue of $1.9 to $2.0 billion.

On Thursday, Stryker (SYK) will report earnings. They previously said they expect Q1 earnings between $1.57 and $1.62 per share. For the full year, Stryker expects earnings of $7.07 to $7.17 per share. The stock has been holding up well. SYK is within 3% of its all-time high. The company has raised its dividend every year since 1993.

Moody’s (MCO) is set to report on Friday, April 27. The credit-ratings agency is our second-best performer this year with a gain of 12.3%. I like this company a lot. They’re looking for 2018 earnings of $7.65 to $7.85 per share. They made $6.07 per share in 2017. For Q1, Wall Street expects earnings of $1.80 per share.

That’s all for now. Still more earnings reports are to come next week. We’ll also get a few key economic reports. On Monday will be existing-home sales. Then on Tuesday, we’ll see new-home sales. On Friday, we’ll get our first look at Q1 GDP. The last three quarters have been close to 3% growth. Let’s see if that trend continues. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Syndication Partners

I’ve teamed up with Investors Alley to feature some of their content. I think they have really good stuff. Check it out!

3 Stocks for Profits from People Playing Video Games All Day

According to PricewaterhouseCooper (PwC), the global e-sports market was worth $327 million in 2016. One reason for its smallish size compared to say the NFL is that e-sports is a collection of different game titles across different game genres, with different intellectual property holders that, to date, have not bargained together for TV (and streaming) rights and sponsorship deals.

But now e-sports is moving into the ‘major league’ of sports. They will be added as a medal event in the 2022 Asian Games. That’s not surprising considering that South Korea is the hot spot for these sports, with other Asian countries also joining in. The backers of e-sports are pushing too for it to be added as an official event in future Olympics too.

Any future Olympics boost will only add to the growth already occurring. PwC estimates that the e-sports market will expand at a compound annual growth rate (CAGR) of 21.7% through 2021 into an $874 million market. Other forecasts are even more bullish. For example, the Dutch research firm Newzoo says e-sports will be a $1.6 billion industry by 2021.

Whatever forecast you believe, the bottom line is that the e-sports industry is growing in leaps and bounds. Here are three to stocks to buy from companies profiting off people playing video games all day.

Buy These 2 Stocks Benefitting from Trump’s Tax Reform Law

With this year’s tax filing deadline date just past, it’s a good as time as any to take a look at a few special situations whose stock prices were hit because of recent changes in tax policies.

The first company I want to tell you about is one that has become a real life example of the law of unintended consequences…

Congress changed the way American corporations are taxed on their overseas earnings. Previously, firms were taxed at the 35% rate. But most companies avoided that by booking their income overseas and then keeping the money there.

So Congress came up with GILTI (Global Intangible Low-Taxed Income), which was set at 10.5%. Its main target was the tech and pharma companies that transferred their trademarks and patents overseas to avoid paying tax on them.

But this new tax intended to tax overseas income earned by U.S. technology and pharmaceutical firms and their trademarks and patents has hit closer to home. Click here to see which stocks are impacted.

Posted by Eddy Elfenbein on April 20th, 2018 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His