Archive for July, 2018

-

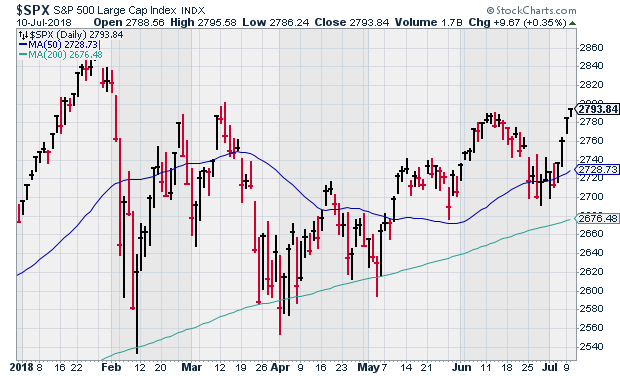

Four-Month High

Eddy Elfenbein, July 10th, 2018 at 4:39 pmThe S&P 500 closed today at 2,793.84. That’s the highest close since February 1.

-

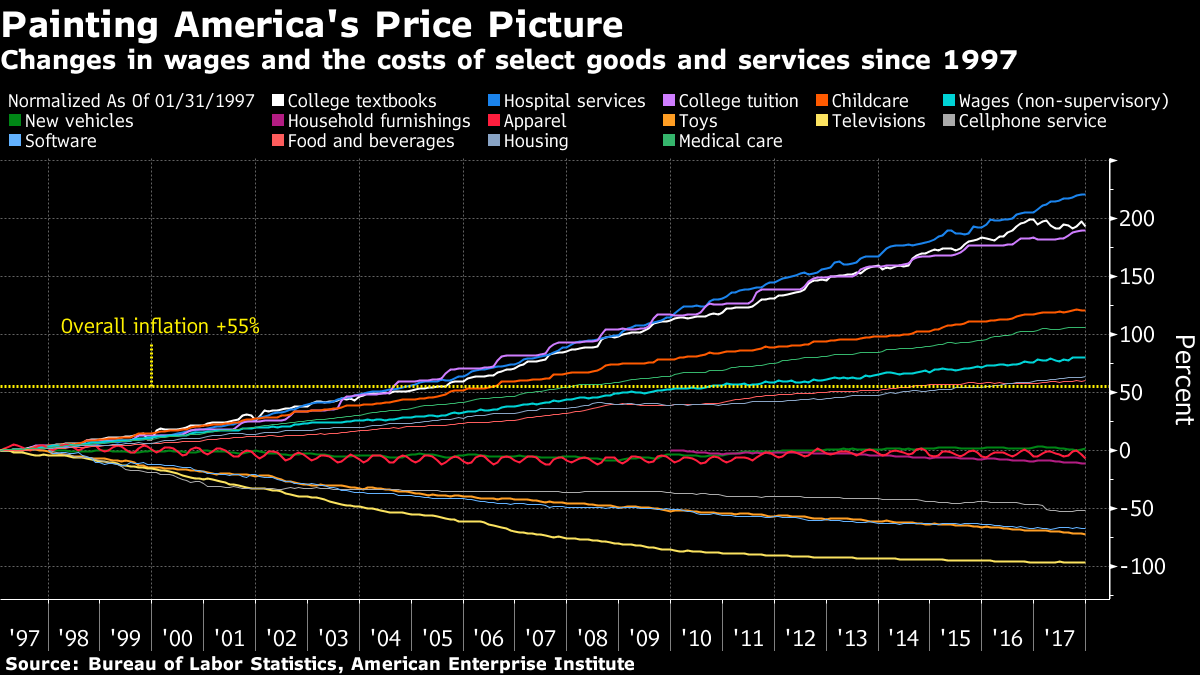

The Inflation Divide

Eddy Elfenbein, July 10th, 2018 at 1:03 pmEconomist Mark Perry has created a fascinating chart. It shows the increase in prices in several sectors of the economy. In the areas that are subject to foreign competition, prices have collapsed. But in areas protected from foreign competition, prices have soared.

Globalism has created winners and losers. The problem is that it’s hard to see the victories. People come to see goods are correctly priced, not as far below what they would have been in another scenario.

Just as globalization has been a headwind holding back inflation, its unraveling could end up being a tailwind in the years ahead, pushing costs higher as countries and companies retreat from the international marketplace. That would be on top of the one-time effect that Trump’s tariffs will have on prices of selected imports, putting pressure on the Fed to raise interest rates at a faster pace than the gradual path it has currently mapped out.

The president has already imposed import duties on a wide range of products, from steel and aluminum to washing machines and farm equipment. He’s taken particular aim at shipments from China, levying $34 billion in tariffs on goods from that country last week. China, Canada and some of the other nations affected have responded in kind.

Administration officials argue that Trump’s tariffs are designed to convince other countries to dismantle trade barriers, not erect new ones. Yet experts are skeptical, pointing to the president’s focus on getting rid of America’s bilateral deficits and his repeated attacks on the North American Free Trade Agreement, which eliminated many tariffs among the U.S., Canada and Mexico.

-

One Upgrade and One Downgrade

Eddy Elfenbein, July 10th, 2018 at 11:50 amI usually don’t pay much attention to analyst moves on our Buy List stocks, but today we had two that are noteworthy.

Check Point Software (CHKP) was upgraded by BTIG analyst Joel Fishbein who upgraded the stock to buy from neutral. He wrote, “After three quarters of stagnant stock performance and four quarters of disappointing guidance from Check Point, we believe it is now time to get constructive on the name again.”

The other move was that Evercore ISI downgraded Cerner (CERN) from inline to underperform. They lowered their price target from $75 to $55.

-

Morning News: July 10, 2018

Eddy Elfenbein, July 10th, 2018 at 7:09 amJapan’s Takeda Gains U.S. Approval for $62 Billion Shire Buy

Son Has a Plan for Yahoo Japan. It Begins With D.

BMW Finalizes Accord to Start Producing Electric Minis in China

Tesla Drops Reservation System, Opens Model 3 Orders to Anyone With $3,500. (No Refunds.)

Tesla Hikes Prices in China as Trade War Hits Carmakers

Nissan Falsifies Exhaust Emission Data in New Issue for Saikawa

Xiaomi Gains $6 Billion in a Rebound From Weak Hong Kong Debut

AT&T’s Big Plan for HBO Is to Fill It With More Random Trash Like Netflix

IHOP Has Officially Changed its Name Back from IHOb and is Slashing the Price of Pancakes

Trump Slams Pfizer, Other Drug Companies, for Raising Prices, Vows Government Response

Starbucks: Goodbye, Plastic Straws

States Want Fast Food Chains to Allow Employee Poaching

Lawrence Hamtil: A Cautionary Tale for Index-only Investors

Cullen Roche: Who Are the Greatest Investors of All-Time?

Joshua Brown: The Nine Essential Conditions to Commit Massive Fraud

Be sure to follow me on Twitter.

-

Smucker Ditches the Doughboy

Eddy Elfenbein, July 9th, 2018 at 4:30 pmJM Smucker (SJM) announced today that it’s selling its Pillsbury baking division. This was hardly a surprise. We knew this move was coming for some time.

J.M. Smucker is selling its U.S. baking business to a private-equity firm for $375 million, including debt, mirroring moves by other food companies to divest decades-old brands whose sales are in decline because of changing consumer tastes.

Smucker said Monday that Greenwich, Conn.-based Brynwood Partners would buy Funfetti and Pillsbury baking mixes and Hungry Jack pancakes, among other brands. Smucker put the baking business, which generated 5% of its revenues, up for sale in April.

While the fluffy, white Pillsbury’s Doughboy wearing a chef’s hat charmed Americans into buying the brand for decades after his 1965 debut, his effectiveness has waned.

Mark Smucker, chief executive of the Orrville, Ohio company, said in February that he hadn’t invested much in Pillsbury over the prior year because it would have hurt profit. “We consciously chose not to go deep,” he said on an earnings call.

This was the right move for Smucker, and they’ll get some cash from the deal.

-

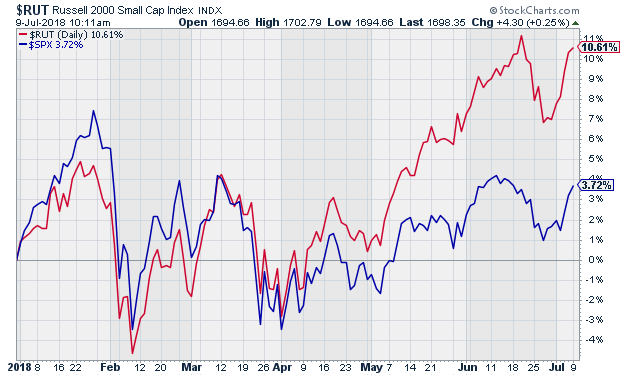

Small-Caps Near All-Time High

Eddy Elfenbein, July 9th, 2018 at 10:15 amAfter lagging for the first part of this year, small-cap stocks have been popular lately. Here’s a chart showing the S&P 500 (blue) along with the Russell 2000 (red). The Russell is close to hitting a new all-time high today.

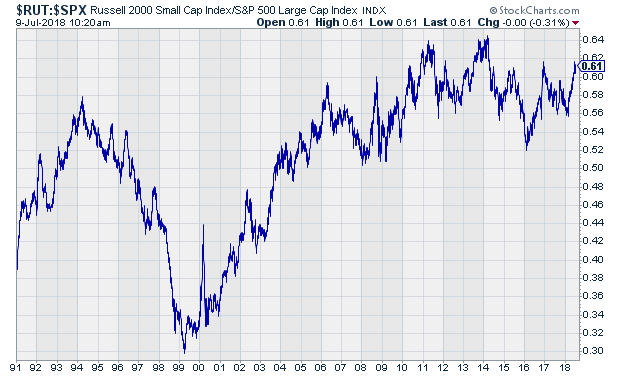

Even though the Russell is near a new high while the S&P 500 is not, the Russell has still lagged the S&P 500 over the past few years. The Russell/S&P Ratio peaked on March 4, 2014. That ended 15 years of outperformance.

-

Stock Buybacks Soar While Stocks Haven’t

Eddy Elfenbein, July 9th, 2018 at 9:31 amShare buybacks seem to be one of those topics, along with the Fed, that many investors are determined to not understand. There’s nothing underhanded about them. The issue I have with them is that they can be swallowed up in normal volatility. While buybacks continue to rise, share prices haven’t kept up.

U.S. companies are buying back record amounts of stock this year, but their shares aren’t getting the boost they bargained for.

S&P 500 companies are on track to repurchase as much as $800 billion in stock this year, a record that would eclipse 2007’s buyback bonanza. Among the biggest buyers are companies like Oracle Corp. , Bank of America Corp. and JPMorgan Chase & Co.

But 57% of the more than 350 companies in the S&P 500 that bought back shares so far this year are trailing the index’s 3.2% increase. That is the highest percentage of companies to fall short of the benchmark’s gain since the onset of the financial crisis in 2008, according to a Wall Street Journal analysis of share buyback and performance data from FactSet.

Most companies are not very good market-timers. As a result, a lot of firms are paying too much for their own shares.

The S&P 500 Buyback index, which tracks the share performance of the 100 biggest stock repurchasers, has gained just 1.3% this year, well underperforming the S&P 500.

-

Morning News: July 9, 2018

Eddy Elfenbein, July 9th, 2018 at 7:08 amLegal Marijuana Is Coming to Canada. Investors Catch the Buzz.

Trump’s And China’s Tariffs Could Do Permanent Damage To Soybean Farmers

U.S. Exporters Will Be a Surprise Loser From Tariff Fight

Ford: Potential Impact From Lower Global Auto Tariffs

Xiaomi, a Chinese Technology Darling, Slumps After I.P.O.

Tencent’s U.S. Music IPO Reflects More Upbeat Recording Industry

China’s Cosco Gets U.S. Security Clearance to Purchase Shipping Rival

HBO Must Get Bigger and Broader, Says Its New Overseer

Dreams of Goldman Doing Big Takeover Meet Stress Test’s Reality

Inside China’s Dystopian Dreams: A.I., Shame and Lots of Cameras

Takeaway From the New Billionaires Ranking: Zuckerberg and Bezos Don’t Give Away Enough Money

Jeff Miller: Inflation on the Horizon?

Roger Nusbaum: Sharpening The Pencil On Factor Funds

Michael Batnick: These Are the Goods

Be sure to follow me on Twitter.

-

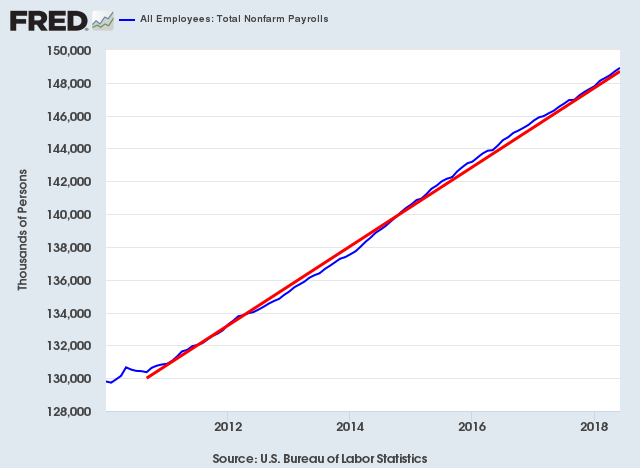

June NFP = +213K

Eddy Elfenbein, July 6th, 2018 at 12:03 pmThe June jobs report is out, and the numbers are pretty good. The U.S. economy created 213,000 net new jobs last month.

The unemployment rate ticked up from 3.8% to 4.0%. Actually, I dug into the decimals and the increase was closer to 0.3%. That’s the largest monthly increase in the unemployment rate since November 2010.

Part of the effect is more workers joining the labor pool. That can create the oxymoron of more jobs leading to a higher unemployment rate. After nine years of economic expansion, the jobs-to-population ratio is still lower than at any point from 1987 to 2008.

Here’s the growth of NFP along with a trend line that increases by 201,000 each month. They seem quite similar.

-

Morningstar on Check Point

Eddy Elfenbein, July 6th, 2018 at 9:58 amCheck Out Check Point

Check Point Software Technologies (CHKP), an Israel-based network security incumbent, has adapted its product portfolio in recent years to strategically position itself as enterprises migrate toward hybrid cloud environments. Its expertise in software-defined security environments, relative to peers’ reliance on physical infrastructure, should result in margin expansion.

As mobile and cloud become more important for customers, the potential vectors of attack become increasingly serpentine, which we think could expand Check Point’s market opportunity. Check Point excels because of its large-enterprise-focused model and a broad product portfolio, yielding high renewal rates and a growing recurring revenue base. Further, we think the company’s ability to churn out new offerings allows it to meet the rapidly evolving technological needs of its client base. Check Point continues to earn exemplary marks in its threat detection rates from independent reviews. We estimate that nearly 70% of the company’s revenue is recurring, and we see switching costs from its mission-critical security offerings for sprawling enterprise clients whose demands necessitate a vendor with ubiquitous solutions like Check Point. The company’s focus on software blade subscriptions (suites of integrable software products that can be selected or deselected based on the client’s preference) sold into the enterprise allows Check Point to extract respectable pricing from clients and post outstanding gross and operating margins.

Check Point’s Infinity product represents the next iteration of its management console. We think clients are in a consolidation phase as they limit security subscriptions to a single vendor, which should benefit Check Point based on its reputation and expansive product portfolio.

Check Point is a market leader, but secular trends such as the growth in cloud computing, the Internet of Things, and artificial intelligence remain on the periphery. We see these themes as potential avenues for disruption, but because each spawns added threats to Check Point’s client base, they create additional vectors for Check Point to secure.

Robust Switching Costs Result in Narrow Moat

We believe that the mountainous undertaking of deploying a large enterprise network firewall, coupled with the macro trend of cybersecurity product consolidation, benefits Check Point’s relatively diverse ecosystem of available offerings and creates a robust degree of switching costs, resulting in a narrow economic moat. Typically, the rapidly evolving nature of the cybersecurity industry has made it difficult to construct a moat, particularly as malicious actors have shown a propensity to outpace the ability of security providers to detect, protect against, and respond to new malevolent threats. However, we believe Check Point is in a league of its own because of its operational reputation, the fairly high attach rate of its core firewall business, and its comprehensive suite of integrable software subscriptions. These factors yield unparalleled margins and returns on invested capital among the security vendors we cover. Check Point’s many services, which include supplying firewall, endpoint, and mobile protection, among many others, become embedded in the IT infrastructure of large organizations. We believe any potential benefit of switching to a competitor would pale in comparison with the costs of implementation and training required when deploying a new solution, not to mention the risks of a potential breach allowed by technology from a less reputable vendor.Check Point originally established itself as a pre-eminent supplier of network firewall technology. A company’s IT security teams would install a firewall to limit the access into internal IT environments. Check Point was well positioned to build share in large enterprises thanks to its long record of reliability, innovation, and an international presence. We believe firewalls benefit from a multiyear refresh life cycle. Recently, the industry has undergone a metamorphosis as network security has become increasingly complex, with organizations moving away from the data center. Software as a service, endpoint protection, mobile, and the hybrid cloud have all made the IT environments increasingly byzantine. As Check Point has built subscription-based software offerings to meet the protection needs of its customers across each of these potential penetration vectors, switching costs have become entrenched.

Check Point offers a plethora of solutions, including small and midsize and enterprise firewalls, endpoint protection, mobile security, malware protection, advanced threat protection for public, private, and mobile cloud environments. We see this as a more complete solution set than certain rivals have. We conclude that with each subsequent product or subscription a customer purchases from Check Point, the stickier the relationship becomes. Many current clients began using Check Point’s firewall product and added a software blade product as their businesses grew. Given the Internet of Things, whereupon a customer’s light, lock, or thermostat may eventually need protection at the enterprise level, we believe complexity will only increase.

We believe there is evidence of product consolidation, with clients now wanting all their applications managed in one place, by a single vendor. In the past, the cybersecurity market was characterized by companies that specialized in one niche. Today, however, for many businesses it no longer makes sense to have separate cybersecurity vendors for each area. Thus, as enterprises and small and midsize businesses consolidate under one platform, we believe Check Point will benefit as it arguably has the most comprehensive suite of subscription-based offerings. Threats to its customers can be managed under one console. Check Point anticipated this trend, as it expanded its software blade offerings to cater to a multitude of clients, allowing customers to mix and match subscriptions to fit their needs as their respective businesses scale. We believe the recently launched Infinity product cements this trend; as clients use several of Check Point’s offerings in this single console, switching costs increase.

Large and New Competitors a Concern

One concern for Check Point remains the secular shift away from the data center to public cloud infrastructure vendors such as Amazon (AMZN) and Microsoft (MSFT). While AWS and Azure provide basic security features, we believe they lack the cohesive offerings and functionality that incumbent firewall vendors like Check Point can provide, in addition to what security-conscious enterprises have historically shown they have needed. Amazon, Microsoft, and Google (GOOG) could conceivably build out their respective software offerings, which could be supported by their scale and marketing power as enterprises migrate to the cloud.Newer voracious competitors such as Palo Alto Networks (PANW) and Fortinet (FTNT) have adopted an aggressive go-to-market strategy, with Palo Alto spending 50% of its revenue on sales and marketing (compared with Check Point’s 23% in 2017). These competitors have attempted to disrupt incumbents such as Check Point, Cisco (CSCO), and Juniper Networks (JNPR). The firewall space was disrupted by Palo Alto’s launch of its next-generation firewall, demonstrating that a competitor can take share with an innovative offering. We can’t rule out the threat of other innovative startups over time. Check Point may need to respond to this intense competition with renewed investment in sales and marketing, potentially weighing on margins. Finally, we think Check Point has been marred by execution issues with regard to relaying the breadth and depth of its product portfolio to clients and shedding its reputation as an “old world” firewall vendor.

Check Point is in exemplary financial health. It now has $4 billion in cash and marketable securities on its balance sheet. We expect the company to perennially buy back its own stock. Check Point has historically been opportunistic in its acquisitions, only buying businesses that it believed to be well below fair value or in instances where management believed it could not build the product internally. Given the cash balance and decelerating growth, we would be amenable to bolt-on acquisitions to move the company into high-growth areas.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His