Archive for November, 2018

-

Q3 2018 Earnings Calendar

Eddy Elfenbein, November 8th, 2018 at 9:10 amEarnings season is winding down with 20 of our 25 Buy List stocks now having reported Q3 earnings. Here’s a list of reporting dates, Wall Street’s consensus estimates and actual reported results.

Company Ticker Date Estimate Result Alliance Data Systems ADS 18-Oct $6.20 $6.26 Danaher DHR 18-Oct $1.08 $1.10 Signature Bank SBNY 18-Oct $2.83 $2.84 Snap-On SNA 18-Oct $2.86 $2.88 AFLAC AFL 24-Oct $0.99 $1.03 Check Point Software CHKP 24-Oct $1.36 $1.38 Torchmark TMK 24-Oct $1.53 $1.59 Cerner CERN 25-Oct $0.63 $0.63 Sherwin-Williams SHW 25-Oct $5.75 $5.68 Stryker SYK 25-Oct $1.68 $1.69 Moody’s MCO 26-Oct $1.78 $1.69 Cognizant Technology Solutions CTSH 30-Oct $1.13 $1.19 Wabtec WAB 30-Oct $0.95 $0.95 Carriage Services CSV 31-Oct $0.22 $0.14 Fiserv FISV 31-Oct $0.77 $0.75 Intercontinental Exchange ICE 31-Oct $0.80 $0.85 Church & Dwight CHD 1-Nov $0.54 $0.58 Ingredion INGR 1-Nov $1.70 $1.70 Becton, Dickinson BDX 6-Nov $2.93 $2.93 Continental Building Products CBPX 8-Nov $0.48 $0.51 Morning News: November 8, 2018

Eddy Elfenbein, November 8th, 2018 at 7:09 amStrong Dollar Hits China’s Foreign-Exchange Reserves

Respect Our Choices, China’s Xi Says Ahead of Trump G20 Meeting

‘Fed Is in Denial’: How a $4 Trillion Dilemma Could Get Ugly

Why Corporate America Is Content With the Midterms

What Democratic Control of the House Could Mean for Your Wallet

Tesla Names New Chair As Elon Musk Steps Down

Google Plans Large New York City Expansion

Two Hong Kong Companies in Lose More Than 75% of Value

Why the Google Walkout Was a Watershed Moment in Tech

UBS Faces New Legal Battle in U.S. Over Mortgage Securities

Roku Stock Falls Late Despite Beating Third-Quarter Estimates

Berkshire Hathaway’s Profits Are Not What You Think They Are

Michael Batnick: I Remember When

Blue Harbinger: Do You Trade Binary Events?

Be sure to follow me on Twitter.

Morning News: November 7, 2018

Eddy Elfenbein, November 7th, 2018 at 7:16 amMarkets Got the Midterms Right. Now What Happens?

What the Election Results Mean for Business

Job Openings Outnumbered Unemployed Americans by More Than One Million in September

Looking for Higher Yields? Try Lending Money

Russian Trolls Were at It Again Before Midterms, Facebook Says

A $240-Billion-a-Day Market Is Leaving London Ahead of Brexit

Shanghai Is Being Thrust Into the High-Stakes Tech I.P.O. Race

How Apple Is Losing Its Grip on India

Ahold Ups Stakes in U.S. Grocery War With Mini-‘Robot Supermarkets’

CVS Lays Out Vision for Future as Aetna Merger Looms

Dish Revenue Falls 5% as Satellite Subscribers Drop

Nick Maggiulli: The McRib Effect

Jeff Carter: Was It The Banks Fault?

Cullen Roche: Three Things I Think I Think – What In the Hell is Going On Out There?

Be sure to follow me on Twitter.

The Math Hustle

Eddy Elfenbein, November 6th, 2018 at 10:23 pmInstitutional Investor has a very good article on Wall Street’s abuse of math. Let me explain. Financial economics has an inferiority complex. As a result, the field needlessly uses fancy math to justify itself. This seeps into money management.

The financial industry uses mathematics in a manner that would be mortifying to any other field of science. Academic literature and industry research are rife with pseudo-mathematical nonsense. You don’t have to look far to see where the motivation lies: Many of the authors are either employed by or retained by richly paid investment management and consulting firms. Faced with soaring investor interest in algorithm-powered investment strategies, the habit — indeed, the requirement — today is for firms to use scientific language and notation to nourish the idea that they’ve proved mathematically that there’s a way to systematically beat the market.

They haven’t.

It’s not surprising that more is claimed by their suggestive language than they actually “prove” because the field suffers from a subtle corruption. There is a pattern developing of publishing a semi-quantitative paper and using it as the basis to establish an investment advisory firm, become the seller of an investment product “relying only on math,” and go off on a globe-circling marketing bender. The fastest-growing asset management firms are purveyors of investment products that draw upon mathematical finance research, so theories ridden with poorly specified mathematics and wildly exaggerated results abound.

Becton, Dickinson Earns $2.93 per Share

Eddy Elfenbein, November 6th, 2018 at 7:37 amThis morning, Becton, Dickinson (BDX) reported fiscal Q4 earnings of $2.93 per share. That matched Wall Street’s estimates. It was also a nice increase from $2.40 per share one year ago. This was a big year for BDX because it was the first year they’ve operated after absorbing CR Bard. For the year, Becton made $11.01 per share. Adjusting for the acquisition, revenues were 5.8% for the fiscal year.

“Fiscal 2018 was a historic year for BD with the successful completion of the acquisition of C. R. Bard. We are extremely proud of our strong fourth quarter and fiscal year results, which demonstrate how agile we can be as an organization while executing concurrently on two transformative acquisitions,” said Vincent A. Forlenza, Chairman and CEO. “We enter fiscal 2019 with continued strong momentum and confidence in our ability to execute on our strategy, deliver on our commitments and create value for our shareholders.”

In fiscal 2017, Becton made $9.48 per share. Last November, the company originally pegged EPS for fiscal 2018 at $10.55 to $10.65. In February, they bumped the range up to $10.85 – $11 per share. In May, they raised the range again to $10.90 – $11.05 per share. Then in August, it went to $10.95 – $11.05 per share. Ultimately, they made $11.01 per share.

For the current fiscal year, BDX expects earnings between $12.05 and $12.15 per share. They’re looking for adjusted revenue to rise by 5% to 6%.

Morning News: November 6, 2018

Eddy Elfenbein, November 6th, 2018 at 6:51 amItaly Gets a Warning From the 14th Century

Iran Sanctions and Oil Prices: Who’ll Feel the Pain?

China’s Trade Olive Branch Can’t Dispel Fears of Clash With U.S.

Amazon Plans to Split HQ2 Evenly Between Two Cities

Crazy Work Hours and Lots of Cameras: Silicon Valley Goes to China

Apple’s Asia Suppliers Fall on Report iPhone XR Production Boost Canceled

Ford Goes Local in India, Aims for Bigger Slice of Competitive Market

Boeing, Airbus Fret Over Trade War as China Displays Aviation Ambitions

Verizon to Break Up Wireless Unit in Reorganization

Drugmaker Lilly’s Third-Quarter Profit More than Doubles

How Bill Gates Aims to Save $233 Billion by Reinventing the Toilet

Joshua Brown: Will the Stock Market Celebrate Gridlock?

Howard Lindzon: Momentum Monday…The FANG/FAANG Blues and Mood Matters

Be sure to follow me on Twitter.

RIP: Evelyn Y. Davis

Eddy Elfenbein, November 5th, 2018 at 11:04 amEvelyn Y. Davis, one of Wall Street’s true characters, has passed on, aged 89. She was known as the original shareholder activist, which is a polite way of saying she grilled CEOs at shareholder meetings.

It’s a basic rule of our free enterprise system that if you own shares in a company, you are the owner. As a result, you’re fully within your right to question management. And question, Ms. Davis did.

For more than five decades, the Netherlands-born Ms. Davis attended annual meetings of Bank of America, Ford Motor Co. and Goldman Sachs Group Inc., among many other companies, to offer advice and demand changes. She advocated lower pay for executives and term limits for directors. Sometimes she advised CEOs to resign or commented on their looks.

At a Goldman Sachs annual meeting in 2011, when the investment bank was still facing regulatory and legal fallout from the 2008 financial crisis, she advised the CEO, Lloyd Blankfein, to step down. “I want people to know I have nothing against you personally,” she told Mr. Blankfein. “And you are not a bad-looking guy.”

Mr. Blankfein replied that he had no plans to resign.

She held stock in more than 80 companies and published an annual newsletter, Highlights and Lowlights, to recount her tussles with top executives. She charged $600 an issue and insisted that companies buy at least two copies.

Morning News: November 5, 2018

Eddy Elfenbein, November 5th, 2018 at 7:04 amBig Short’s Eisman Is Shorting Two U.K. Banks on Brexit

Despite Killing, SoftBank Chief Sees ‘Responsibility’ to Invest in Saudi Arabia

Iran Says It Will Resist ‘Economic War’ as U.S. Revives Curbs

Xi’s Swipes at Trump Show China Standing Its Ground in Trade War

China Seeks Allies as Trump’s Trade War Mounts. It Won’t Be Easy.

Fading Hopes for U.S.-China Trade Truce Hit Markets

Their Soybeans Piling Up, Farmers Hope Trade War Ends Before Beans Rot

Jack Ma Says the Trade War Is the ‘Most Stupid Thing’

Amazon Drops Free Shipping Minimum in Tussle for Holiday Sales

Should You Buy Or Sell Apple For No Longer Disclosing iPhone Sales Numbers?

How Hyundai Motor, Once a Rising Star, Lost its Shine

Fewer Stars to Rise at Goldman Sachs as Partnership Class Shrinks

Ben Carlson: Tiny Improvements, Big Results

Cullen Roche: No, The Government Didn’t Cause Unemployment

Be sure to follow me on Twitter.

October NFP = +250K; Unemployment = 3.7%

Eddy Elfenbein, November 2nd, 2018 at 9:03 amThe October jobs report is out! The US economy created 250,000 net new jobs last month. Wall Street had been expecting 190,000. The unemployment rate stayed at 3.7%.

The ranks of the employed rose to a fresh record 156.6 million and the employment-to-population ratio increased to 60.6 percent, the highest level since December 2008, according to the department’s household survey. That headline jobless number stayed level even amid a two-tenths of a percentage point rise in the labor force participation rate to 62.9 percent.

Those counted as outside the labor force tumbled by 487,000 to 95.9 million.

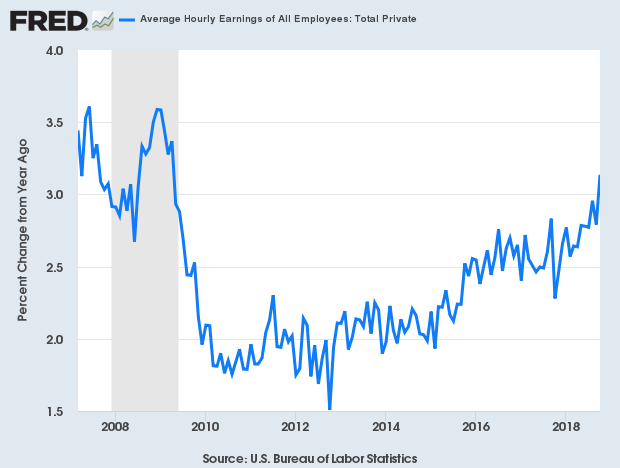

But the bigger story may be wage growth, which has been the missing piece of the economic recovery. Average hourly earnings increased by 5 cents an hour for the month and 83 cents year over year, representing a 3.1 percent gain. The annual increase in wages was the best since 2009.

That number is being watched closely by Federal Reserve, which has increased its benchmark interest rate three times this year and is on track for a fourth quarter-point hike in December. Higher wage growth feeds into the central bank’s desire to raise rates to keep inflation under control.

Here’s the year-over-year increase in average hourly earnings. It finally topped 3%.

U-6, which is a broader measure of unemployment, fell to 7.4%. The futures market is indicating a strong open.

Health care showed some of the biggest gains for the month, adding 36,000. Manufacturing contributed 32,000, thanks to a gain in durable goods and in particular transportation equipment, which added 10,000.

Construction also rose sharply, with an increase of 30,000 while transportation and warehousing jumped by 42,000.

In addition, leisure and hospitality was a strong contributor, with 42,000 new positions after being unchanged in September, due likely to Hurricane Florence, the government report said.

Professional and business services increased by 35,000, bringing its 12-month total gain to 516,000, and mining added 5,000.

Job growth skewed by full-time positions, which rose by 318,000, while part-time jobs increased by 242,000, according to the household survey.

Another closely watched internal metric, the average work week, increased 0.1 hour to 34.5 hours.

CWS Market Review – November 2, 2018

Eddy Elfenbein, November 2nd, 2018 at 7:08 am“It’s waiting that helps you as an investor, and a lot of people just can’t stand to wait.” – Charlie Munger

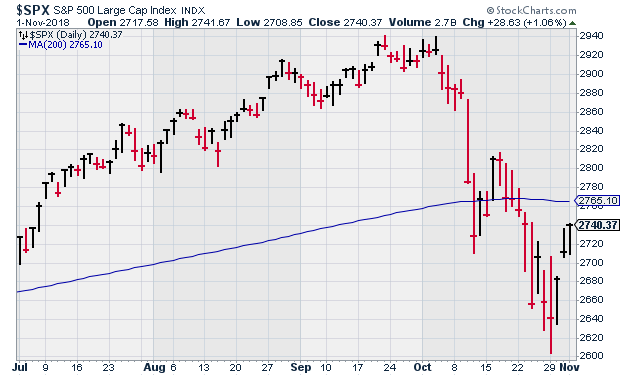

October has mercifully come to an end. The S&P 500 shed nearly 7% during the month making it the worst month for stocks in seven years. The Nasdaq suffered even more. The tech-heavy index was down over 9% for the month.

The good news is that there’s been some relief lately. The S&P 500 has rallied more than 1% for the last three days. That hasn’t happened in more than two years, but don’t think the storm has passed. As long we’re below the 200-day moving average—and we are—then there’s a threat that we’ll move lower. The market loves to “test” its low once or twice before making its next move.

In this month’s issue we have several Buy List earnings reports to cover. Some were good (Church & Dwight), others were not (Carriage Services). I’ll sort it out for you. We also have two more earnings reports next week that will be our final reports for this season. Now let’s take a closer look at the broad market.

The End of Red October

October was a very bad month for stocks. The major event came on October 3 when Fed Chairman Jay Powell said that we’re a “long way” from neutral. The markets took the clue. Later this month, we learned that mortgage rates touched a seven-year high. After that, we got a bad housing report which spooked the bulls even more.

I think the market has forgotten that housing can have a bad year. Not every slowdown means a global bust-up like we had ten years ago. But lately, just about any stock related to housing has felt the pain. With the general market wooziness, some tech stocks have been caught up in the selling, but most of the damage has been related to anything involved in construction. The S&P 500 Materials Sectors dropped 16% in a little over one month.

The market had a dramatic turnaround this week. From Monday’s low to Thursday’s close, the Dow gained more than 1,250 points. I tend to be wary of such strong “contra-trend” moves, especially when there’s so little to justify it. On Monday, the stock market had a pronounced reversal. A morning rally was wiped out. The difference between Monday’s high and low was over 900 points. On Monday, the S&P 500 got as low as 2,603.54. That’s 11.5% below the intra-day high from September 21.

The key for investors is the 200-day moving average. Historically, volatility is much higher below the 200-DMA than above it. Even with this week’s nice bounce, the S&P 500 is still about 1% below its 200-DMA. But a short burst is not a convincing move. Expect to see the S&P 500 back below 2,650 soon. Until then, make sure you have a well-diversified portfolio of high-quality stocks. Now let’s take a look at a busy week of earnings reports.

Eight Buy List Earnings Reports

We had another big batch of earnings this week (here’s our earnings calendar). Let’s start with Moody’s (MCO) which reported last Friday. For Q3, the company earned $1.69 per share, an eight-cent miss. That’s unusual for Moody’s. The company said that non-financial corporate debt issuance slowed down last quarter.

Even though this was an earnings miss, Moody’s earnings were still up 11% from a year ago. The company lowered its full-year range to $7.50 – $7.65 per share. That implies a Q4 range of $1.74 to $1.89 per share. On Friday, shares of Moody’s dropped nearly 9%. Fortunately, the stock made up a lot of lost ground this week. MCO gained more than 3% on Wednesday and then another 3% on Thursday. I’m dropping my Buy Below on Moody’s to $162 per share.

On Tuesday, we had two more reports. First up is Cognizant Technology Solutions (CTSH). For Q3, the IT outsourcer earned $1.19 per share. That beat estimates by six cents per share. The company had told us to expect earnings of at least $1.13 per share. Revenue rose 8.3% to $4.88 billion.

For Q4, Cognizant sees earnings of at least $1.05 per share and full-year earnings of at least $4.50 per share. That’s a bit light. The Street had been expecting $1.14 for Q3 and $4.53 for the year. Cognizant sees Q4 revenue between $4.09 billion and $4.13 billion.

The stock fell close to 4% on Tuesday, but it gained nearly all of it back on Wednesday. Cognizant is doing just fine. This week, I’m lowering our Buy Below to $74 per share.

Also on Tuesday morning, Wabtec (WAB) said they made 95 cents per share for Q3 which matched estimates. This is a crucial time for WAB with the big merger coming. Frankly, any merger news probably outweighs earnings news at this point.

Wabtec said they now expect full-year 2018 earnings of $3.85 per share which excludes merger costs. The company is aiming for a 13% operating margin and $200 million in cash flow. The CEO said he expects a strong Q4 and that the freight business continues to show strong growth. The merger with GE Transportation is expected to happen in early 2019. There will be a special shareholder meeting to vote on the deal on November 14.

I wasn’t as disappointed with this report as traders seemed to be. Shares of WAB dropped about 9% over Tuesday and Wednesday, but rallied some on Thursday. I still like this stock, but I’m dropping our Buy Below to $91 per share.

Earnings from ICE, Fiserv and Carriage

We had three earnings reports on Wednesday. Before the bell, Intercontinental Exchange (ICE) reported Q3 earnings of 85 cents per share. That was five cents ahead of expectations. Total revenue, excluding transaction-based expenses, rose 4.7% to $1.2 billion. Also, the board of directors authorized a new share-buyback program of $2 billion.

This was a good quarter for ICE. The company noted that it was the 22nd quarter in a row of year-over-year revenue growth. ICE didn’t offer any financial guidance. The company is also in the midst of a regulatory battle on the future of data fees. This is a very profitable business for ICE and the other exchanges, but the fight over regulations will probably wind up in the courts. The stock jumped 5.4% on Wednesday. ICE remains a solid buy up to $79 per share.

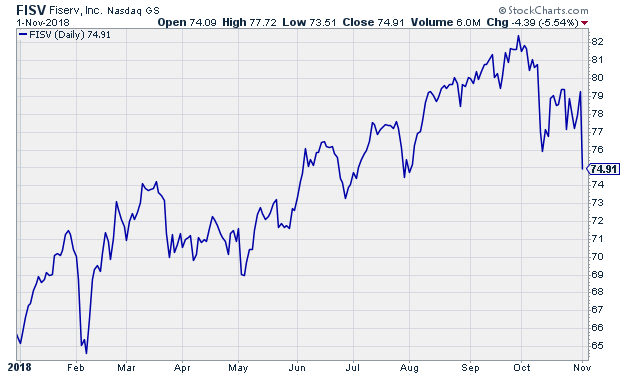

After the closing bell on Wednesday, Fiserv (FISV), “a leading global provider of financial-services technology solutions,” reported third-quarter earnings of 75 cents per share. That was two cents below estimates. In last week’s issue, I said I had been expecting an earnings beat from Fiserv.

Despite the earnings miss, Fiserv is having a generally good year. For the first nine months of this year, Fiserv has made $2.26 per share. Operating margin dipped to 31.6%, but that’s still quite good.

Fiserv also raised the lower end of its full-year guidance. The range had been $3.02 to $3.15 per share. Now it’s $3.10 to $3.15 per share. That represents growth over last year of 25% to 27%. That also translates to a Q4 range of 84 to 89 cents per share. Wall Street had been expecting 86 cents per share. This year looks to be Fiserv’s 33rd year in a row of double-digit earnings growth. The stock took a 5.5% bath on Thursday, but don’t let the earnings miss scare you. Fiserv is a buy up to $81 per share.

The report from Carriage Services (CSV) was a disaster. There’s no way to put a positive spin on this one. The stock plunged 21.5% on Thursday. When the weak Q2 report came out, management said the issues were temporary, and that they will experience “broadly higher performance during the latter part of the second half of the year.” That was wrong.

I took management’s word, and that was a big mistake. For Q3, Carriage earned 14 cents per share which was far below consensus of 22 cents per share. That’s down from 25 cents per share one year ago. I’m dropping my Buy Below down to $14 per share. You’ll notice that I’m not much bothered by a small earnings miss from companies like Fiserv because I have faith in the company’s management. Not so with Carriage. I apologize for this one.

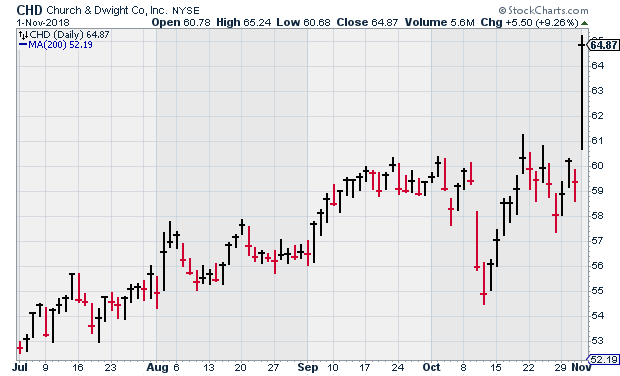

Church & Dwight and Ingredion

Church & Dwight (CHD) may be our star pupil this earning season. On Thursday, the consumer-brand powerhouse reported Q3 earnings of 58 cents per share. That beat estimates by four cents per share. Net sales rose 7.2% to $1.04 billion.

Consumer Domestic, which is CHD’s largest unit, saw net sales growth of 7.6%. Business growth was led by Arm & Hammer. I was pleased to see the company raise its estimate for full-year organic revenue growth from 3.5% to 4.0%.

For Q4, CHD expects earnings of 57 cents per share which makes the full-year total $2.27 per share. The stock jumped over 9% on Thursday. Church & Dwight qualified as my only Buy Below price increase this week. I’m lifting our Buy Below on CHD to $70 per share.

Last week, Ingredion (INGR) warned that Q3 earnings would be about $1.70 per share which was 26 cents less than what Wall Street had been expecting. The company also lowered its full-year guidance from a range of $7.50 to $7.80 per share to a new range of $6.80 to $7.05 per share. The company blamed weak currencies in developing markets plus power outages in North America. Ingredion said it will require more than one quarter to recover.

On Thursday, Ingredion confirmed that they did, in fact, make $1.70 per share last quarter. The company didn’t offer much more in specifics outside what we already know. The plan is to invest more in its specialties portfolio. I afraid I’m skeptical about Ingredion’s plans. I had been expecting to hear more concrete plans from them.

Two More Buy List Earnings Reports Next Week

We have our final two earnings reports next week. Becton, Dickinson (BDX) had a strange reaction to its last earnings report. The stock initially dropped but then regained its composure and proceeded to rally strongly to a new high. The good times ended in October when the stock pulled back sharply. I actually don’t mind seeing BDX at a discounted price.

The next BDX earnings report is scheduled for Tuesday, November 6. In August, BDX reported $2.19 per share for Q2. That beat the Street by three cents, and it was up 18.3% over last year. Becton also raised their revenue guidance for this year. Plus, they bumped up the low end of their full-year forecast. Becton now sees full-year EPS of $10.95 to $11.05 from a previous range of $10.90 to $11.05. For Q3, the consensus on Wall Street is for $2.93 per share.

Continental Building Materials (CBPX) is due to report on Thursday, November 8. Continental was our worst-performing stock last month. For October, CBPX shed more than one-quarter its value. At one point during the summer, we had nearly a 40% YTD gain in Continental. A few days ago, it was negative on the year for us. More remarkably, we didn’t hear anything from the company. As a wallboard stock, it’s certainly tied to the housing sector.

The last earnings report in August was quite good. CBPX made 59 cents per share which was 14 cents more than estimates. Net sales were up 15.5%, while EBITDA rose more than 21%. Gross margins improved to 29.4% from 25.5%. It’s not just about price increases; wallboard sales volume rose from 647 million square feet last year to 722 million square feet this year. The consensus on Wall Street is for earnings of 48 cents per share.

That’s all for now. The big news next week will be the mid-term U.S. elections on Tuesday. There will also be another Federal Reserve meeting on Wednesday and Thursday. Don’t expect to see any move on interest rates. The policy statement will come out on Thursday at 2 pm ET. I’m also curious to see Monday’s ISM Non-Manufacturing Index. The last report was the highest since the index was created ten yeas ago. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Syndication Partners

I’ve teamed up with Investors Alley to feature some of their content. I think they have really good stuff. Check it out!

Can This Tech Stock Save Your Portfolio from the Market Crash?

Buy These 3 High-Yield Stocks to Protect Your Portfolio

Make This Easy Trade to Profit from Stalled Real Estate Prices

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His