Archive for April, 2019

-

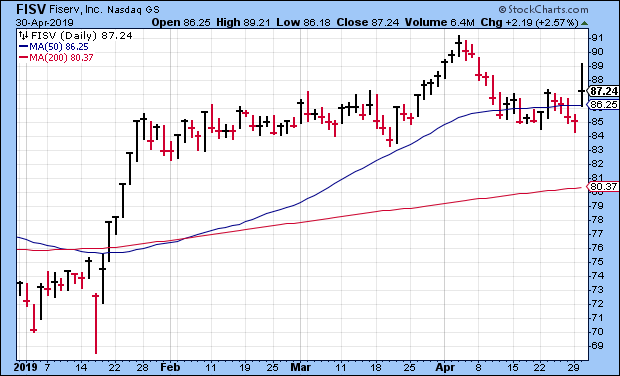

Fiserv Earned 84 Cents per Share

Eddy Elfenbein, April 30th, 2019 at 4:05 pmAfter the bell on Tuesday, Fiserv (FISV) released a pretty good earnings report. This is a relief because the Q4 report wasn’t so hot. For Q1, the company made 84 cents per share. That’s an increase of 12% over last year. It also beat expectations by two cents per share. Quarterly revenues rose 5% to $1.43 billion. Free cash flow was $302 million, and adjusted operating margin came in at 31.9%. Those are nice numbers.

“We are off to a strong start to the year, with first quarter internal revenue growth and sales ahead of our initial expectations,” said Jeffery Yabuki, President and Chief Executive Officer of Fiserv. “In addition to strong financial performance, we are well into integration planning and looking forward to completing the First Data acquisition in the second half of the year.”

In January, Fiserv said it’s going to merge with First Data in a major deal. The plans are moving ahead. The company sees the deal being completed in the second half of this year. Due to the pending merger, Fiserv has suspended all stock buybacks. Fiserv reiterated its full-year earnings range of $3.39 to $3.52 per share.

Update: From Fiserv’s earnings call, this is what Jeffery W. Yabuki has to say about Q2.

Although we don’t provide quarterly guidance, it’s important to remind you that we had very high periodic revenue in last year’s Q2, which will create a difficult compare this year. As such, we anticipate the second quarter will be the low watermark for both internal revenue and adjusted EPS growth with strong acceleration into the back half of the year

-

Morning News: April 30, 2019

Eddy Elfenbein, April 30th, 2019 at 7:08 amBoxed In: $1 Billion of Iranian Crude Sits at China’s Dalian Port

The Fed Has a Problem at the Heart of Its Battle to Spark Inflation

Labor Dept. Says Workers at a Gig Company Are Contractors

GE Swings to Quarterly Profit as It Shrinks

Marriott to Take On Airbnb in Booming Home-Rental Market

Vegan Burger Maker Beyond Meat Raises Price Range in Upsized IPO

Chevron May Have to Up the Ante to Beat Occidental in the Fight for Anadarko Petroleum

Tesla Looks to Regain Its Luster in Solar Energy by Slashing Prices

Another Setback for Samsung as Profit Misses Estimates

Vodaphone Found Hidden Back Doors in Huawei Equipment

Chase Bank Tried to Be Relatable on Twitter and Got Absolutely Dunked On

Cullen Roche: How Will The Fee Structure of Financial Advisory Change in the Future?

Roger Nusbaum: It Turns Out Retirement Planning Is Complicated

Be sure to follow me on Twitter.

-

Disney’s Best Month in 32 Years

Eddy Elfenbein, April 29th, 2019 at 7:41 pmI had been expecting a modest pop from shares of Disney (DIS) this morning thanks to the release of the Avengers movie which, I take it, has been somewhat popular this weekend.

The movie smashed all box office records. For the weekend, the Avengers brought in $350 million domestically and $1.2 billion worldwide. That’s about one-quarter of what Disney paid for Marvel ten years ago. Disney now has nine of the ten largest opening weekends in movie history.

The shares did gap up to a high of $142.37 shortly after the open. Later in the day, however, DIS retreated and closed just below $140 per share. The stock is headed for its best month in 32 years.

Earnings are due out on May 8.

-

Morning News: April 29, 2019

Eddy Elfenbein, April 29th, 2019 at 7:16 amWhat Oil at $100 a Barrel Would Mean for the World Economy

Canadian Farm Exports Run Into Chinese Wall Amid Diplomatic Dispute

U.S.-China Talks to Resume With Significant Issues Unresolved

Mnuchin Says Trade Negotiations With China Are in ‘the Final Laps’

‘Avengers: Endgame’ Shows Movie Theaters Can Still Be on Top of the World

Spotify Tops Estimates With 100 Million Paid Users

Apple Cracks Down on Apps That Fight iPhone Addiction

One in Seven Homes in Japan Is Empty

Boeing CEO Faces Shareholders for First Time Since 737 MAX Crashes

Anadarko to Pursue Deal Talks with Occidental Petroleum

This Elon Musk Comment Should Terrify Tesla Investors

In Washington, Juul Vows to Curb Youth Vaping. Its Lobbying in States Runs Counter to That Pledge.

Jeff Miller: Weighing the Week Ahead: How to Watch the Information Avalanche

Michael Batnick: These Rallies Aren’t Holding & Are Annuities So Terrible?

Howard Lindzon: Momentum Monday – Software, Software, Software!

Be sure to follow me on Twitter.

-

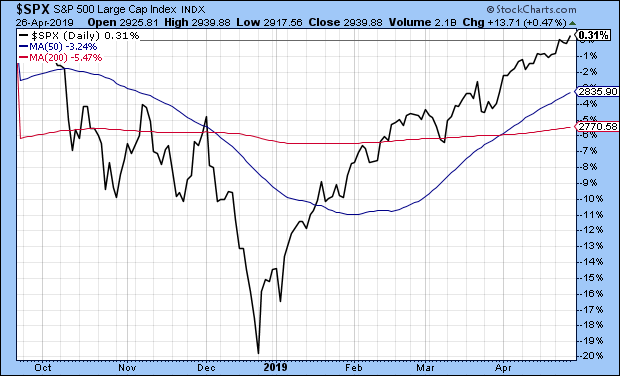

New All-Time High

Eddy Elfenbein, April 28th, 2019 at 7:59 pmOn Friday, the S&P 500 closed at its high for the day which was also its all-time high close. The index was just shy of the intra-day high from last September. Since the all-time high from September, the S&P 500 has gained 0.31%.

Here’s the chart:

It took more than seven months but we made back everything we lost.

-

Q1 GDP Grew by 3.2%

Eddy Elfenbein, April 26th, 2019 at 8:47 amThe initial report on Q1 GDP showed that the U.S. economy grew by 3.2% in real terms during the first quarter.

The U.S. economy expanded at a 3.2% annual pace in the first three months of 2019, the government said Friday.

The gain was well above forecasts. Economists polled by MarketWatch had forecast a 2.3% increase in gross domestic product. The economy grew at a 2.2% rate in the final three months of 2018.

Inflation moderated a bit in the first quarter.

What happened: One unexpected factor behind the acceleration in GDP growth in the first quarter was a sharp upturn in state and local government spending.

Spending at this level jumped 3.9% after a 1.3% drop in the prior three months. This was the fastest gain in three years. Spending by local governments likely picked up due to the partial federal government shutdown.

Also fueling the stronger GDP growth were stronger inventory building and trade. These factors are volatile and could reverse this quarter.

Final sales to domestic purchasers, which excludes trade and inventory behavior, rose 2.3% in the first quarter, the smallest gain in three years, but still well above what economists were expecting.

The value of inventories, which adds to GDP, increased to $128.4 billion from $96.8 billion.

The trade sector added a little more than 1% to growth in the first quarter. Exports rose 3.7%, while imports dropped by the same amount, leading to a smaller trade deficit.

Offsetting these gains, Consumer spending decelerated to a 1.2% gain, the slowest increase in a year.

Business fixed investment decelerated to a relatively slow 2.7% gain, down from a 5.4% gain in the prior quarter. Investment in structures fell 0.8%, the third straight decline.

Investment in new housing was another weak spot. Residential investment dropped 2.8%, the fifth straight quarterly decline.

Headline inflation, as measured by the personal consumption expenditure price index, fell to a 1.4% annual rate in the first quarter from 1.9% in the prior three-month period. The decline in core PCE inflation was less pronounced, slipping to 1.7% from 1.9%. The monthly inflation numbers will be released on Monday.

Big picture: The acceleration in growth in the first quarter is all the more remarkable considering the doom and gloom that surrounded the first quarter outlook in December. Before the new year began, the Atlanta Fed’s “nowcast” model projected 0.5% growth and the flattening of the yield curve was fueling talk of recession. The partial government shutdown, which limited economic data, added to unease.

Instead, the economic data improved steadily as the quarter progressed. Economists think the strong gain in retail sales in March bodes well for second-quarter growth.

The Federal Reserve is not expected to change its patient approach to interest-rate policy despite the strong report. Officials are expected to wait to see how the economy fares in the second quarter before making any decisions. The solid performance in the first quarter may quell some of the chatter that the next Fed move will be a rate cut.

U.S. central bank officials will meet next week to discuss the outlook. Reporters will get a chance to ask Fed Chairman Jerome Powell about the GDP data at his press conference on Wednesday.

-

CWS Market Review – April 26, 2019

Eddy Elfenbein, April 26th, 2019 at 7:08 am“Every day, I assume every position I have is wrong.” – Paul Tudor Jones

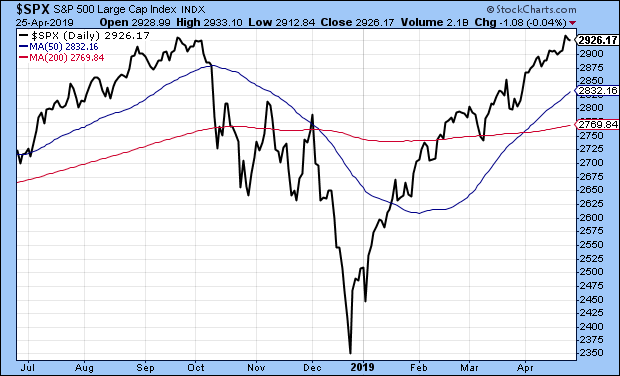

Now that earnings season is in full swing, Wall Street is in its happy place. Truthfully, earnings really aren’t that great this season, but they’re better than they could have been. At least traders are happy. On Tuesday, the S&P 500 closed at a fresh all-time high. This means that we made back everything we lost in a nasty correction that lasted from late September to late December.

We had lots of Buy List earnings reports this week. Moody’s jumped 3% on a very good report. It’s now a 38% winner on the year for us. Hershey beat estimates and gapped 5% to a new high. Cerner raised guidance. Stryker beat and raised guidance. Raytheon creamed estimates, and AFLAC beat as well. Sherwin-Williams shook off a tepid earnings report. I’ll go over all our earnings reports from this week. I’ll also preview a slew of Buy List earnings reports headed our way next week.

Here’s our updated Earnings Calendar:

Twenty of our 25 Buy List stocks are reporting their Q1 earnings this cycle. Here’s a list of reporting dates, Wall Street’s consensus estimates and actual reported results.

Company Ticker Date Estimate Result Eagle Bancorp EGBN 17-Apr $1.12 $1.11 Signature Bank SBNY 17-Apr $2.77 $2.65 Torchmark TMK 17-Apr $1.59 $1.64 Check Point Software CHKP 18-Apr $1.31 $1.32 Danaher DHR 18-Apr $1.01 $1.07 Sherwin-Williams SHW 23-Apr $3.69 $3.60 Stryker SYK 23-Apr $1.84 $1.88 Moody’s MCO 24-Apr $1.93 $2.07 AFLAC AFL 25-Apr $1.06 $1.13 Cerner CERN 25-Apr $0.61 $0.61 Hershey HSY 25-Apr $1.46 $1.59 Raytheon RTN 25-Apr $2.47 $2.77 Fiserv FISV 30-Apr $0.82 Church & Dwight CHD 2-May $0.66 Cognizant Technology Solutions CTSH 2-May $1.04 Continental Building Products CBPX 2-May $0.34 Intercontinental Exchange ICE 2-May $0.90 Broadridge Financial BR 7-May $1.50 Disney DIS 8-May $1.55 Becton, Dickinson BDX 9-May $2.58 There’s a lot to get to this week, so let’s jump right in.

Earnings from Stryker and Sherwin-Williams

We had two earnings reports on Tuesday. Before the opening bell, Sherwin-Williams (SHW) reported Q1 earnings of $3.60 per share. That was below estimates of $3.69 per share. Sales rose 1.9% to $4.04 billion.

Here’s the important fact for investors: The company didn’t alter its full-year outlook of $20.40 to $21.40 per share (that excludes acquisition costs). That compares with $18.53 per share a year ago. For Q2, Sherwin expects sales to rise by 2% to 5%. For the full year, they expect sales to rise by 4% to 7%. This isn’t terrible news.

Here’s what the CEO had to say:

Commenting on the first quarter, John G. Morikis, Chairman and Chief Executive Officer, said, “We made good progress on our pricing initiatives across all segments during the quarter and effectively managed SG&A spending, but volumes fell short of expectations due to a slower start to the architectural painting season in North America and continued challenging conditions in many end markets outside North America. Despite the volume shortfall and higher year-over-year raw material costs, consolidated Company adjusted gross margin, which excludes acquisition-related costs, improved sequentially and was flat year-over-year. We expect the positive trend in gross margin and operating expense control to continue as the year progresses, and volume growth should also improve over the balance of the year, particularly in the back half.

“Looking at our performance by segment, in The Americas Group, despite a strong backlog and project pipeline reported by many of our professional customers, volume growth in the quarter was slower than expected. We continued to invest by opening 15 net new store locations in The Americas Group during the quarter. In our Consumer Brands Group, most of the softness in demand in the quarter was in markets outside North America. Consumer Brands Group adjusted segment operating margin in the first quarter expanded sequentially and year-over-year, and we are very well positioned across all North American retail channels heading into the important spring selling season. Performance Coatings Group achieved modest sales growth and increased adjusted segment operating margin in the quarter against year-over-year raw material pressure.”

Sherwin is fundamentally sound. I think the weakness they had in Q4 is behind them. Reaffirming guidance is a key move. I’m lifting my Buy Below on Sherwin to $460 per share.

Last week, I told you Stryker (SYK) had a good shot at beating expectations, and I was right. The company reported Q1 earnings of $1.88 per share, which beat the Street by four cents per share. That’s an increase of 11.9% over last year. Net sales rose 8.5% to $3.5 billion, and organic net sales increased by 7.3%. For the quarter, Stryker’s adjusted operating margin was 25.1%.

Now for guidance. For Q2, Stryker expects earnings between $1.90 and $1.95 per share. Wall Street had been expecting $1.96 per share. For the full year, Stryker sees earnings between $8.05 and $8.20 per share. That’s an increase of five cents per share to the low end. Wall Street was at $8.13 per share.

This is a really good stock. Stryker remains a buy up to $192 per share.

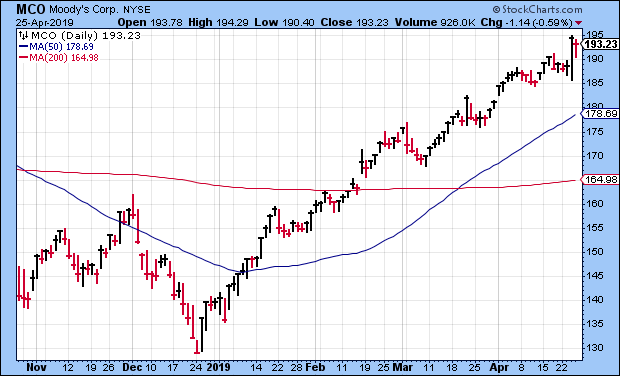

Moody’s Is a Buy Up to $200 per Share

On Wednesday, Moody’s (MCO) released a very good earnings report. The credit-ratings agency reported Q1 earnings of $2.07 per share. That beat estimates by 14 cents per share. The stock gapped up 3% on Wednesday.

Revenue at Moody’s Analytics rose 16%. The company stood by its full-year forecast of $7.85 to $8.10 per share. Moody’s is our top-performing stock this year with a YTD gain of 38%. I’m lifting my Buy Below on Moody’s to $200 per share.

Earnings from AFLAC, Hershey, Cerner and Raytheon

On Thursday, we had four more Buy List earnings reports. Let’s start with AFLAC (AFL). The duck stock had another good quarter. For Q1, AFLAC had adjusted operating earnings, not including currency, of $1.13 per share. That beat estimates by seven cents per share.

The supplemental insurer expects to buy back between $1.3 billion and $1.7 billion in shares this year. AFLAC recently raised its dividend for the 36th year in a row. For 2019, AFLAC is standing by its previous guidance for earnings of $4.10 to $4.30 per share. That assumes the yen trades at ¥110.39 to the dollar.

This means AFLAC is currently going for about 12 times this year’s earnings. Buy up to $50 per share.

Last quarter, Cerner (CERN) did what I pretty much expected. The healthcare-IT folks earned 61 cents per share. That was in the center of their guidance. Sales rose 8% to $1.39 billion.

For Q1, Cerner had operating cash flow of $317.1 million and free cash flow of $123.5 million. For Q2, Cerner expects earnings of 63 to 65 cents per share on revenue of $1.41 to $1.46 billion.

For all of 2019, Cerner sees earnings of $2.64 to $2.72 per share. That’s up from the previous guidance of $2.57 to $2.67 per share. Cerner recently said it had reached an agreement with Starboard Value to start paying a dividend and increase its buyback authorization by $1.5 billion. Cerner is a solid stock. Buy up to $66 per share.

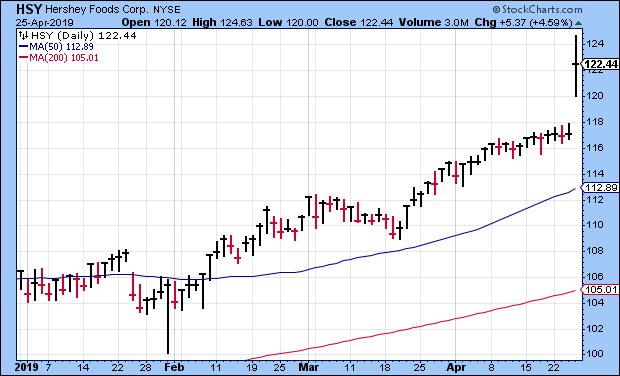

Hershey (HSY) rebounded well after the disappointment from Q4. For Q1, the chocolatier had adjusted Q1 earnings of $1.59 per share. That’s an increase of 12.8% over last year. It also beat Wall Street’s consensus by 13 cents per share.

Hershey reiterated its full-year guidance of $5.63 to $5.74 per share. The shares jumped 4.6% on Thursday and broke out to a new 52-week high. Notice how good companies always bounce back. I’m raising my Buy Below on Hershey to $126 per share.

Raytheon (RTN) shot a tomahawk missile at its earnings estimates. For Q1, the company made $2.77 per share which was 30 cents more than expectations. Wow! Raytheon made $2.20 per share for last year’s Q1.

The company is doing especially well with cyber-security and its intelligence and information unit. Despite the impressive earnings beat, Raytheon didn’t change its full-year earnings guidance of $11.40 to $11.60 per share and sales guidance of $28.6 billion to $29.1 billion. I think that disconcerted some traders, and the shares pulled back 4.4% on Thursday.

Last month, Raytheon hiked its dividend by 8.6%. That was its 15th annual dividend increase in a row. Raytheon remains a buy up to $190 per share.

Five Buy List Earnings Reports Next Week

We have five more Buy List earnings reports next week. Let’s start with Fiserv (FISV), which reports on April 30. Three months ago, the company had an uncharacteristically underwhelming earnings report. They missed the Street by two cents per share, and earnings came in at the low end of their guidance.

Am I worried? Not at all. Despite the earnings miss, Fiserv had Q4 earnings growth of 24%, and operating margin came in at 33.4%. For the year, Fiserv made $3.10 per share. This was their 33rd year in a row of double-digit earnings growth. On top of that, Fortune named Fiserv to their list of most-admired companies for the sixth year in a row.

For 2019, Fiserv expects earnings to range between $3.39 and $3.52 per share. They’ll need to get above $3.41 to extend their double-digit streak. Fiserv also said they expect the First Data deal to close in the second half of 2019. For Q1, Wall Street expects 82 cents per share.

We have four more earnings reports on May 2.

Three months ago, Church & Dwight (CHD) missed Q4 estimates by a penny per share. The stock got clobbered, but I wasn’t too worried. The CEO noted that they were hitting 2019 “with momentum,” and that they have price increases on the way. Wall Street expects Q1 earnings of 66 cents per share.

The big news at Cognizant Technology Solutions (CTSH) is that Brian Humphries has taken over as CEO on April 1 from Francisco D’Souza, who has been CEO since 2007. D’Souza has done a great job, and he’ll remain a member of the board.

For 2019, Cognizant sees earnings of at least $4.40 per share. Wall Street had been expecting $4.45 per share. The company didn’t provide EPS guidance for Q1, but they said sales growth should be between 7.5% and 8.5%. Wall Street expects $1.04 per share, which sounds about right.

Continental Building Products (CBPX) may be our most dramatic stock. In February, the wallboard company soared 8% after its Q4 earnings report matched expectations. Of course, that makes you wonder what expectations really were. I suspect Wall Street has been secretly expecting much worse.

Yet after the initial surge, Continental turned around and gave it all back. The company gives guidance on several metrics but not EPS. For 2019, Continental sees SG&A of $40 million to $42 million and capital expenditures of $28 million to $32 million. Cost-of-goods-sold inflation per unit compared with 2018 is expected to be 4.5% to 6.5%. For Q1, Wall Street expects 34 cents per share.

Last year was Intercontinental Exchange (ICE)’s 13th straight year of record revenues. I think they have a good chance of making this year number 14. For 2018, ICE made $3.59 per share. That’s up 21% over 2017. ICE’s operating margin was an impressive 58%. ICE provides guidance for several metrics except EPS. For Q1, Wall Street expects 90 cents per share, which should be beatable.

That’s all for now. Next week will have it all—more earnings, the April jobs report, the new ISM report, and if that’s not enough, there’s a Fed meeting as well. On Monday, we get personal income. The Federal Reserve meets on Tuesday and Wednesday. The policy statement will come out on Wednesday at 2 pm. Don’t expect any change on rates. Then on Friday, the government releases the April jobs report. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Morning News: April 26, 2019

Eddy Elfenbein, April 26th, 2019 at 7:01 amIn China Stocks, a $2.3 Trillion Rebound Is Giving Way to Gloom

China Retools Vast Global Building Push Criticized as Bloated and Predatory

Exports, Inventories Seen Boosting U.S. First-Quarter Growth

Regulators Around the World are Circling Facebook

Microsoft Touches $1 Trillion Value, Signaling Big Tech’s Stock Market Comeback

Uber Aims to Top $80 Billion Valuation in Year’s Largest IPO

Falling Mercedes Sales Hits Daimler

Germany’s Troubled Banking Giants Decide Against a Merger

PepsiCo is Suing Farmers in India for Growing the Potatoes it Uses in Lays Chips

Renault to Propose Joint Holding Company with Nissan

Joshua Brown: Three Reasons You’re Never Satisfied & Is a Volatility Tsunami Imminent?

Cullen Roche: Having a Printing Press Doesn’t Mean Money is Infinite

Roger Nusbaum: Beware The Bitcoin Charlatans & Asset Allocation Don’ts

Ben Carlson: How Hard is it to Become a 401(k) Millionaire? & The 3 Levels of Wealth

Be sure to follow me on Twitter.

Morning News: April 25, 2019

Eddy Elfenbein, April 25th, 2019 at 7:06 amChina Seeks to Allay Fears Over Belt and Road Debt Risks

Venezuela’s Trade Scheme With Turkey Is Enriching a Mysterious Maduro Crony

Souvenirs From Europe You Can’t Sneak Through Customs

Facebook Expects to Be Fined Up to $5 Billion by F.T.C. Over Privacy Issues

Deutsche Bank, Commerzbank Merger Talks Hit Stumbling Blocks

Occidental Seeks to Buy Anadarko for $38 Billion, Topping Chevron’s Offer

Amazon’s Spending Is Key as Investors Fixate on Profits

Tesla Posts Big Quarterly Loss as Its Electric-Car Sales Lag

Boeing Reports Slide in Earnings and Admits Future Is Hazy

Nissan Warns Investors of a 45 Percent Drop in Profit

Comcast First Quarter Profit Beats Wall Street, Misses on Revenue

Unsold Luxury Homes Are Piling Up in the Hamptons

Jeff Miller: Do You Make Up False Market Narratives?

Michael Batnick: Being Wrong and Changing Your Mind

Jeff Carter: There Is No Quick Easy Money; Unless It’s A Bad Deal or a Scam

Be sure to follow me on Twitter.

Moody’s Earned $2.07 per Share

Eddy Elfenbein, April 24th, 2019 at 7:19 am1Q19 revenue of $1.1 billion up 1% from 1Q18

1Q19 diluted EPS of $1.93 up 1%; adjusted diluted EPS of $2.07 up 2% from 1Q181; both aided by a lower effective tax rate

Record 1Q19 Moody’s Analytics revenue of $472.0 million up 16%, with double-digit growth across all business lines

Affirming FY 2019 diluted EPS and adjusted diluted EPS guidance ranges of $7.30 to $7.55 and $7.85 to $8.10, respectivelyMoody’s Corporation (MCO) today announced results for the first quarter of 2019, as well as provided its current outlook for full year 2019.

“Moody’s first quarter revenue reflected robust performance in Moody’s Analytics across all business lines. This strength was largely offset by an expected decline in Moody’s Investors Service’s revenue as the business faced challenging year-over-year debt issuance comparisons,” said Raymond McDaniel, President and Chief Executive Officer of Moody’s. “We are affirming our full year 2019 guidance of $7.30 to $7.55 for diluted EPS and $7.85 to $8.10 for adjusted diluted EPS.”

MCO FIRST QUARTER REVENUE UP 1%

Moody’s Corporation reported revenue of $1.1 billion for the three months ended March 31, 2019, up 1% from the prior-year period.

U.S. revenue was $612.1 million, up 2%, and non-U.S. revenue was $530.0 million, approximately flat to the prior-year period. Revenue generated outside the U.S. constituted 46% of total revenue, down from 47% in the prior-year period. Foreign currency translation unfavorably impacted Moody’s revenue by 2%.

Moody’s Investors Service (MIS) First Quarter Revenue Down 7%

Revenue for MIS for the first quarter of 2019 was $670.1 million, down 7% from the prior-year period, compared to a 14% decline in issuance activity2. U.S. revenue was $411.2 million, down 5%, and non-U.S. revenue was $258.9 million, down 10%. Foreign currency translation unfavorably impacted MIS revenue by 2%. The MIS adjusted operating margin was 54.9%.

Corporate finance revenue was $355.4 million, down 9% from the prior-year period. This result was primarily driven by a decline in global bank loan issuance, partially offset by increased U.S. and EMEA investment grade bond activity. U.S. and non-U.S. corporate finance revenues were down 6% and 15%, respectively.

Structured finance revenue was $100.7 million, down 15% from the prior-year period. This result primarily reflected lower U.S. and EMEA collateralized loan obligation (CLO) refinancing activity. U.S. and non-U.S. structured finance revenues were down 16% and 12%, respectively.

Financial institutions revenue was $115.8 million, up 1% from the prior-year period. U.S. financial institutions revenue was down 5%, while non-U.S. revenue was up 6%.

Public, project and infrastructure finance revenue was $92.7 million, down 1% from the prior-year period. This result reflected a slow start to the year in non-U.S. infrastructure finance issuance, principally in EMEA, largely offset by higher U.S. municipal issuance against a low prior-year comparable. U.S. public, project and infrastructure finance revenue was up 13%, while non-U.S. revenue was down 18%.

Moody’s Analytics (MA) First Quarter Revenue Up 16%

Revenue for MA for the first quarter of 2019 was $472.0 million, up 16% from the prior-year period. U.S. revenue was $200.9 million, up 22%, and non-U.S. revenue was $271.1 million, up 12%. Foreign currency translation unfavorably impacted MA revenue by 3%. Organic MA revenue for the first quarter of 2019, which excluded Reis and Omega Performance revenues, was $460.6 million, up 13% from the prior-year period. The MA adjusted operating margin was 28.1%.

Research, data and analytics (RD&A) revenue was $307.7 million, up 15% from the prior-year period. U.S. and non-U.S. RD&A revenues were up 20% and 12%, respectively. Organic RD&A revenue, which excluded Reis revenue, was $298.8 million, up 12%, driven by strong sales growth at Bureau van Dijk in the second half of 2018, as well as sales of credit research and ratings data feeds.

Enterprise risk solutions (ERS) revenue was $121.9 million, up 19% from the prior-year period. This result reflected growth in fourth quarter 2018 and first quarter 2019 subscription sales, and the business continued to successfully execute on the transition toward a software-as-a-service model. U.S. and non-U.S. ERS revenues were up 26% and 15%, respectively.

Professional services revenue was $42.4 million, up 13% from the prior-year period. U.S. and non-U.S. professional services revenues were up 34% and 2%, respectively. Organic professional services revenue, which excluded Omega Performance revenue, was $39.9 million, up 6% from the prior-year period.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His