Archive for May, 2019

-

Becton, Dickinson’s Fiscal Q2 Results

Eddy Elfenbein, May 9th, 2019 at 6:18 amAs reported, revenues of $4.195 billion decreased 0.6 percent.

– On a comparable, currency-neutral basis, revenues increased 3.4 percent.

– As reported, diluted earnings per share of $(0.07) increased 63.2 percent.

– As adjusted, diluted earnings per share of $2.59 decreased 2.3 percent, and increased 7.2 percent on a currency-neutral basis.

– The company reaffirmed its full fiscal year 2019 comparable, currency-neutral revenue guidance, and updated its adjusted diluted earnings per share guidance.BD (Becton, Dickinson and Company) (NYSE: BDX), a leading global medical technology company, today reported quarterly revenues of $4.195 billion for the second fiscal quarter ended March 31, 2019. This represents a decrease of 0.6 percent from the prior-year period. On a comparable, currency-neutral basis, revenues increased 3.4 percent over the prior-year period.

“Through the second quarter we have delivered solid revenue growth and operating performance,” said Vincent A. Forlenza, chairman and CEO. “Our revised fiscal year 2019 outlook reflects recent, near-term regulatory and market pressures related to paclitaxel-coated devices and foreign currency, which will affect our EPS guidance range. We remain confident that our business is strong, fundamentals are in-tact, and we will continue to deliver value to our shareholders and customers around the world.”

Second Quarter and Six-Month Fiscal 2019 Operating Results

As reported, diluted earnings per share for the second quarter were $(0.07), compared with $(0.19) in the prior-year period. This represents an increase of 63.2 percent. Adjusted diluted earnings per share were $2.59, compared with $2.65 in the prior-year period. This represents a decrease in adjusted diluted earnings per share of 2.3 percent, or an increase of 7.2 percent on a currency-neutral basis.

For the six-month period ended March 31, 2019, as reported, diluted earnings per share were $1.98, compared with $(0.90) in the prior-year period. This represents an increase of 320.0 percent. Adjusted diluted earnings per share were $5.29, compared with $5.15 in the prior-year period. This represents an increase in adjusted diluted earnings per share of 2.7 percent, or 10.5 percent on a currency-neutral basis.

Current period adjusted results exclude, among other items, charges to record product liability reserves of $331 million and the estimated cost of a product recall of $65 million.

Segment Results

In the BD Medical segment, as reported, worldwide revenues for the quarter of $2.180 billion increased 0.4 percent over the prior-year period, or 3.8 percent on a comparable, currency-neutral basis. The segment’s results were driven by performance in the Medication Management Solutions, Diabetes Care and Pharmaceutical Systems units. Performance in the Medication Delivery Solutions unit reflects a tough comparison to the prior year, as well as distributor inventory adjustments during the quarter in the United States.

For the six-month period ended March 31, 2019, BD Medical revenues were $4.316 billion as reported, which represents an increase of 7.2 percent over the prior-year period. On a comparable, currency-neutral basis, BD Medical revenues increased 4.5 percent.

In the BD Life Sciences segment, as reported, worldwide revenues for the quarter of $1.052 billion decreased 4.2 percent from the prior-year period. On a comparable, currency-neutral basis, revenues increased 2.7 percent. Revenue growth was driven by performance in the Biosciences and Preanalytical Systems units. Growth in the Diagnostic Systems unit reflects a tough comparison to the strong flu season in the prior-year period.

For the six-month period ended March 31, 2019, BD Life Sciences revenues were $2.108 billion as reported, which represents a decrease of 1.6 percent from the prior-year period. On a comparable, currency-neutral basis, BD Life Sciences revenues of $2.099 billion increased 3.7 percent.

In the BD Interventional segment, as reported, worldwide revenues for the quarter of $0.963 billion increased 1.1 percent over the prior-year period, or 3.5 percent on a comparable, currency-neutral basis. The segment’s results were driven by performance in the Urology and Critical Care and Peripheral Intervention units. Growth in the Surgery unit reflects a tough comparison to the prior-year period.

For the six-month period ended March 31, 2019, BD Interventional revenues were $1.932 billion as reported, which represents an increase of 70.2 percent over the prior-year period. On a comparable, currency-neutral basis, BD Interventional revenues increased 4.6 percent.

Geographic Results

As reported, second quarter revenues in the U.S. of $2.341 billion increased 0.7 percent from the prior-year period. On a comparable basis, U.S. revenues increased 2.2 percent over the prior-year period. Growth in the U.S. was driven by performance in the BD Medical and BD Interventional segments. BD Life Sciences’ growth in the U.S. reflects the aforementioned comparison to a strong flu season in the prior year in the Diagnostic Systems unit.

As reported, revenues outside of the U.S. of $1.854 billion decreased 2.3 percent from the prior-year period. On a comparable, currency-neutral basis, revenues outside of the U.S. increased 4.9 percent over the prior-year period. International revenue growth was driven by strong performance in China and EMA.

For the six-month period ended March 31, 2019, U.S. revenues were $4.728 billion as reported, which represents an increase of 18.7 percent over the prior-year period. On a comparable basis, U.S. revenues of $4.724 billion grew 4.1 percent over the prior-year period. As reported, revenues outside of the U.S. of $3.628 billion grew 9.2 percent over the prior-year period. On a comparable, currency-neutral basis, revenues outside the U.S. of $3.623 billion grew 4.5 percent over the prior-year period.

Fiscal 2019 Outlook for Full Year

As reported, the company expects full fiscal year 2019 revenues to increase 8.0 to 9.0 percent, compared to 8.5 to 9.5 percent previously communicated, due to the estimated additional negative impact from foreign currency. The company continues to estimate full fiscal year 2019 revenues will increase 5.0 to 6.0 percent on a comparable, currency-neutral basis.

The company expects adjusted diluted earnings per share to be between $11.65 and $11.75, resulting in growth of approximately 12.0 percent on a currency-neutral basis. This is a decrease from previously issued guidance of approximately 13.0 to 14.0 percent growth, and is due to recent regulatory and market pressures related to paclitaxel-coated devices. Including the estimated additional unfavorable impact of foreign currency, adjusted diluted earnings per share are expected to grow approximately 6.0 to 7.0 percent over fiscal 2018 adjusted diluted earnings per share of $11.01.

Estimated adjusted diluted earnings per share for fiscal 2019 excludes potential charges or gains that may be recorded during the fiscal year, such as, among other things, the non-cash amortization of intangible assets, acquisition-related charges, and certain tax matters. BD does not attempt to provide reconciliations of forward-looking non-GAAP earnings guidance to the comparable GAAP measure because the impact and timing of these potential charges or gains is inherently uncertain and difficult to predict and is unavailable without unreasonable efforts. In addition, the company believes such reconciliations would imply a degree of precision and certainty that could be confusing to investors. Such items could have a substantial impact on GAAP measures of BD’s financial performance.

-

“Cerner Controls a Quarter of Electronic Medical Records Market”

Eddy Elfenbein, May 9th, 2019 at 5:53 amFrom the Kansas City Business Journal:

Cerner Corp., along with its competitor Epic Systems Corp., ruled the electronic health record (EHR) market in 2018, with a combined 85 percent market share in the large, 500-plus-bed hospital space, according to KLAS Research reports cited in Healthcare Dive. Epic holds a 58 percent share, while Cerner holds 27 percent.

The split is closer when it comes to all acute care hospitals in the U.S. In this larger market, Epic has a 28 percent market share and North Kansas City-based Cerner (Nasdaq: CERN) claims 26 percent of the market.

Although fewer large hospitals and health systems are buying EHRs — 80 percent of all doctors will be working at a facility that uses an EHR system by the end of this year according to Business Insider — Cerner signed the most new hospitals last year. This is due, in part, to a 10-year, $10 billion contract with the U.S. Department of Veterans Affairs. The contract, won in May 2018, includes 147 acute care and 20 specialty contracts.

In February, the VA terminated a $624 million 2015 contract with Epic and Leidos Holdings Inc. (NYSE: LDOS) so that it could adopt Cerner’s patient scheduling system, Millennium. It’s unclear how much Cerner’s new contract is worth.

In contrast, Cerner lost 65 Millennium EHR customers in the private hospital sector, including 52 from a single health system.

EHR purchases in 2018 were higher than previous years, with the continued consolidation of the health care market helping to drive those 445 deals. Since 2014, a fifth of all EHR switches at acute care hospitals have stemmed from mergers and acquisitions, according to KLAS.

-

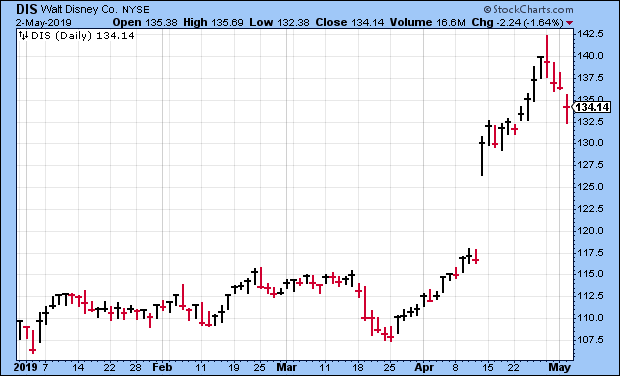

Disney Beats Earnings

Eddy Elfenbein, May 8th, 2019 at 6:32 pmAfter the bell, Disney (DIS) earned $1.61 per share. That was three cents better than estimates. The stock is up a bit after hours.

Walt Disney Co’s theme parks lifted quarterly earnings past Wall Street targets on Wednesday, helping offset big investments to support the media and entertainment company’s bid to draw audiences to streaming media.

Shares of Disney rose 1.5 percent to $137 in after-hours trading.

“Avengers: Endgame”, the end of a decade-long superhero series with $2.2 billion in box office sales worldwide, will stream exclusively on Disney+ starting Dec. 11, the company announced.

Growth at Disney parks in the United States boosted results above analyst expectations. From January to March, Disney reported adjusted earnings per share of $1.61, ahead of analyst estimates of $1.58, according to IBES data from Refinitiv. Heavy investment accounted for a 13 percent drop from a year ago by that measure.

Revenue rose 3 percent to $14.92 billion. Analysts had been expecting a small decline.

Disney is trying to transform from a cable TV leader to a streaming media powerhouse that, like Netflix Inc, sells subscriptions directly to consumers. Costs to build digital services will weigh on profits for several years, the company has said.

Its biggest streaming bet, the family-oriented Disney+, is set to launch in November. The company told analysts in April that it expects Disney+ to achieve profitability in fiscal 2024.

The just-ended quarter reflected the purchase of film and TV assets from 21st Century Fox, which brought Disney more content for its streaming future.

For the quarter, the direct-to-consumer and international unit recorded a loss of $393 million from streaming costs.

Disney also recorded a $353 impairment charge from its ownership stake in media startup Vice.

In the theme park unit, net income hit $1.5 billion as more visitors showed up at Walt Disney World in Florida and at Hong Kong Disneyland, and occupied hotel nights increased.

“Increased ticket prices haven’t put visitors off, and hotels continue to be a major driver of additional spending,” said Nicholas Hyett, equity analyst at Hargreaves Lansdown. “It’s easy to get caught up in the hype surrounding new films … but it’s the less glamorous Media Networks and Parks that pay the lion’s share of the bills.”

Overall net income jumped 85 percent, to $5.4 billion, thanks to Disney’s acquisition of a controlling stake in Hulu through the Fox acquisition.

Media networks, a division that includes ESPN and ABC, reported $2.2 billion in operating income for the quarter.

The movie studio reported profit of $534 million, lifted by “Captain Marvel,” which was a global hit but did not reach the level of “Black Panther” and “Star Wars: The Last Jedi” a year earlier.

-

Morning News: May 8, 2019

Eddy Elfenbein, May 8th, 2019 at 7:09 amChina Defaults Hit Record in 2018. 2019 Pace Is Triple That

Tariff War Renewed? How the U.S.-China Talks Could Play Out

Are Trump’s Tariffs Bolstering the U.S. Economy? Nope.

Eyeing IPO Riches, Uber Drivers Go On Strike in UK Ahead of U.S. Action

Google Says It Has Found Religion on Privacy

Lyft’s First Results After I.P.O. Show $1.14 Billion Quarterly Loss

JPMorgan Poised to Be First Foreigner to Get Majority in China Fund Venture

Bristol-Myers Sells $19 Billion of Bonds to Fund Celgene Purchase

McDonald’s Joins the Meatless Burger Trend in One of Its Biggest Markets

Amazon’s Latest Store Proves the Cashless Dream is Dead

GM Stock Could Be Undervaluing the Cruise Division

Nick Maggiulli: When Does Market Timing Work?

Jeff Carter: The Liquidity Premium

Be sure to follow me on Twitter.

-

Broadridge Earns $1.59 per Share

Eddy Elfenbein, May 7th, 2019 at 7:30 amReaffirming Fiscal Year 2019 Guidance for Recurring Revenue Growth

Reaffirming Fiscal Year 2019 Guidance for Double-Digit EPS Growth

Raising Fiscal Year 2019 Closed Sales Guidance with Year-to-Date at Record $161 million

Broadridge Financial Solutions (BR) today reported financial results for the third quarter and nine months ended March 31, 2019 of its fiscal year 2019. Results for the three and nine months ended March 31, 2019 compared with the same period last year were as follows:

“After a solid third quarter, Broadridge is very well-positioned to deliver strong full-year results. In addition, we continue to make progress on key growth initiatives including next generation regulatory communications and adding clients to our industry-leading technology platforms,” said Tim Gokey, Broadridge’s President and Chief Executive Officer. “Our sales pipeline remains strong which, combined with our sales over the first three quarters of the year, positions us well for future growth.

“We are raising our full-year Closed sales guidance and reaffirming our fiscal year 2019 guidance for recurring revenue growth and EPS growth. Our ability to deliver double-digit adjusted EPS growth reflects the strength of the Broadridge business model and the growth of our recurring revenue. As we close out fiscal year 2019, we remain confident that we are on track to deliver long-term growth and achieve the three year objectives we laid out at our 2017 Investor Day,” Mr. Gokey added.

Net Earnings and Earnings per Share

For the third quarter of fiscal year 2019:

Net earnings increased 58% to $172 million, compared to $109 million for the prior year period.

Adjusted Net earnings increased 56% to $189 million, compared to $121 million for the prior year period.

Diluted earnings per share increased 61% to $1.45, compared to $0.90 for the prior year period.

Adjusted earnings per share increased 59% to $1.59, compared to $1.00 for the prior year period.“After a solid third quarter, Broadridge is very well-positioned to deliver strong full-year results. In addition, we continue to make progress on key growth initiatives including next generation regulatory communications and adding clients to our industry-leading technology platforms,” said Tim Gokey, Broadridge’s President and Chief Executive Officer. “Our sales pipeline remains strong which, combined with our sales over the first three quarters of the year, positions us well for future growth.

“We are raising our full-year Closed sales guidance and reaffirming our fiscal year 2019 guidance for recurring revenue growth and EPS growth. Our ability to deliver double-digit adjusted EPS growth reflects the strength of the Broadridge business model and the growth of our recurring revenue. As we close out fiscal year 2019, we remain confident that we are on track to deliver long-term growth and achieve the three year objectives we laid out at our 2017 Investor Day,” Mr. Gokey added.

-

Morning News: May 7, 2019

Eddy Elfenbein, May 7th, 2019 at 7:16 amA $400 Billion Wave of Japanese Cash May Be Heading Overseas

How the Rise of Developing Countries Has Disrupted Global Trade

Lagarde Issues New Trade Warning Amid ‘Unfavorable’ Trump Tweets

Trade Talks Are Foundering on Mistrust and Arrogance

Federal Reserve Warns as Risky Corporate Debt Exceeds Peak Crisis Levels

Anadarko Says It Now Favors Occidental Bid Over Chevron

Silicon Valley Is Coming For Your House

As IPO Looms, Uber Clings to Hard-Knuckled Tactics in Pursuit of Growth

BMW Profit Slumps on Weaker Markets, $1.6 Billion Provision

Vodafone Steps Up Fight for Liberty Deal With German Access Offer

Tyson Says Hog Disease Impact to Linger for Years

Kraft Heinz to Restate Financial Results Following Investigation

Joshua Brown: Charlie Munger on Commission-Based Brokers and Bankers

Cullen Roche: Three Things I Think I Think – Berkshire, Jobby Jobs and Chase Tweets

Roger Nusbaum: It’ OK To Be Skeptical & Is The Harvard Endowment Making A Huge Mistake?

Be sure to follow me on Twitter.

-

Good Day for Our Buy List

Eddy Elfenbein, May 7th, 2019 at 5:06 amThis will probably jinx us, but Monday was a very good day for our Buy List. While the S&P 500 fell 0.45%, our Buy List gained 0.41%. That’s a big outperformance for one day.

Our biggest winner was Continental Building Products (CBPX), which gained 6.6%. Our wallboard stock is an unusual one because its results have been good but the share price hasn’t done much. It’s almost like Disney up until a month ago.

Except for CBPX, there weren’t any outstanding gains on Monday. Instead, it seems like there was an unusual number of stocks that gained 1% to 2% for us. FactSet (FDS), Moody’s (MCO) and Smucker (SJM) all made new 52-week highs.

-

Morning News: May 6, 2019

Eddy Elfenbein, May 6th, 2019 at 7:02 amEurope Is Reining In Tech Giants. But Some Say It’s Going Too Far.

Stocks Tumble as Trump Trade Threat Reverberates

Trump’s Tariff Threat Leaves Beijing Stalling on Next Talks

Fed Faces Tough Sell on Inflation Framework

Why A 60-65% Market Loss Would Be Run-Of-The-Mill

Occidental Ups Its Cash Offer for Anadarko

Warren Buffett’s Case for Capitalism

5 Insights from the 2019 Berkshire Hathaway Annual Meeting

Boeing Believed a 737 Max Warning Light Was Standard. It Wasn’t.

Facebook ‘Labels’ Posts By Hand, Posing Privacy Questions

SoftBank Has a Big Sprint Problem on Its Hands Without T-Mobile

Boeing Did Not Disclose 737 MAX Alert Issue to FAA for 13 Months

Michael Batnick: Animal Spirits, Re-Kindled: The Big Short

Jeff Carter: Does Culture Eat Strategy For Lunch?

Ben Carlson: How Compounding Works in the Stock Market, Investing Lessons from the Reigning Jeopardy Champ & 4 Overlooked Investment Decisions

Be sure to follow me on Twitter.

-

April 2019 NFP = +263K

Eddy Elfenbein, May 3rd, 2019 at 8:37 amThe April jobs report is out, and it’s a good one. The U.S. economy created 263,000 net new jobs last month. The report for February was revised higher by 23,000, and March was revised upward by 16,000.

The unemployment rate fell to 3.6%. That’s the lowest unemployment rate since December 1969. It’s the lowest peacetime jobless rate in 70 years.

Nonfarm payroll growth easily beat Wall Street expectations of 190,000 and a 3.8% jobless rate.

Average hourly earnings growth held at 3.2% over the past year, a notch below Dow Jones estimates of 3.3%. The monthly gain was 0.2%, below the expected 0.3% increase, bringing the average to $27.77. The average work week also dropped 0.1 hours to 34.4 hours.

Unemployment was last this low in December 1969 when it hit 3.5%. At a time when many economists see a tight labor market, big job growth continues as the economic expansion is just a few months away from being the longest in history.

-

CWS Market Review – May 3, 2019

Eddy Elfenbein, May 3rd, 2019 at 7:08 am“Successful investing is anticipating the anticipations of others.” – J.M. Keynes

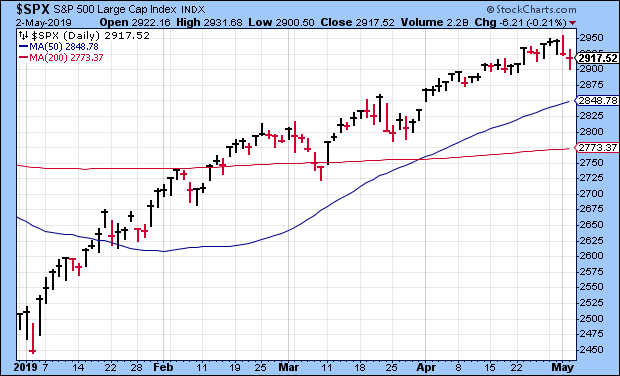

On Tuesday, the S&P 500 closed at yet another all-time high. The same day, our Buy List closed at a YTD high. We now have six stocks that are up more than 28% this year, including Disney, which just had its best month in nearly 20 years.

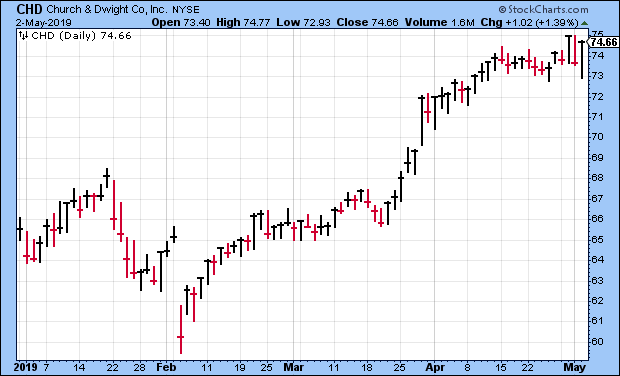

We had more Buy List earnings reports this week, and they were quite good. Fiserv beat by two cents. So did Intercontinental Exchange. Church & Dwight beat by four cents and rallied to a new high. Continental Building topped estimates by 24%.

Our one dud (and there’s always one each earnings season) was Cognizant Technology Solutions. The IT-outsourcer missed earnings and cut guidance, and the shares took a nasty fall. I’ll have all the details in a bit. But first, let’s survey some recent economic data.

We May Have Avoided an Earnings Recession

If all the earnings news wasn’t enough, the Federal Reserve got together this week and decided against changing interest rates. This wasn’t much of a surprise. In fact, the Fed may not be touching rates at all in the next few months. In the policy statement, the Fed kept the language saying the central bank will be “patient” regarding future rate increases.

In the post-meeting press conference, Chairman Jerome Powell was optimistic. He said, “Our outlook, and my outlook, is a positive one, is a healthy one, for the U.S. economy for the rest of this year.” I have to explain that in central-banker talk, that’s a jump for joy. Most central bankers are born dour, and it goes down from there.

I want to highlight some recent economic data because they back up Powell’s view. Last week, we got the initial report for Q1 GDP growth, and it came in at 3.2%. That’s pretty good. Over the last nine quarters, GDP has grown at its fastest pace in 12 years. We’ll get another CPI report next week, but the latest figures (through March) show that core inflation is running at 1.6%. That’s hardly a problem.

The April jobs report is due out later today. It may be out by the time you’re reading this. The other jobs numbers are encouraging. Jobless claims are up a bit, but that’s after hitting 50-year lows. Wednesday’s ADP payroll report showed a gain of 275,000 private payrolls last month. (I don’t place a high degree of faith in ADP’s figures, but it’s interesting to note.)

Earlier this week, we learned that the ISM Manufacturing report for April fell to 52.8. While that’s down, it still indicates that the factory sector is growing. Most importantly for us, this earnings season isn’t as bad as some folks had expected. About 75% of companies are beating expectations. We don’t have the full numbers in yet, but Credit Suisse had been expecting a Q1 earnings decline of 2.5%. Now they expect to see an earnings gain of 2.5% to 3%.

The takeaway is clear. All the doomsayers of a few months ago were overstating the case. The economy is still expanding, and markets are responding. Now let’s look at this week’s Buy List earnings.

Fiserv Earned 84 Cents per Share

After the bell on Tuesday, Fiserv (FISV) released a pretty good earnings report. This was a relief because the Q4 report wasn’t so hot. For Q1, the company made 84 cents per share. That’s an increase of 12% over last year. It also beat expectations by two cents per share. Quarterly revenues rose 5% to $1.43 billion. Free cash flow was $302 million, and adjusted operating margin came in at 31.9%. Those are nice numbers.

“We are off to a strong start to the year, with first-quarter internal revenue growth and sales ahead of our initial expectations,” said Jeffery Yabuki, President and Chief Executive Officer of Fiserv. “In addition to strong financial performance, we are well into integration planning and looking forward to completing the First Data acquisition in the second half of the year.”

In January, Fiserv said it’s going to merge with First Data in a major deal. The plans are moving ahead. The company sees the deal being completed in the second half of this year. On the earnings call, this is what Yabuki had to say about Q2.

Although we don’t provide quarterly guidance, it’s important to remind you that we had very high periodic revenue in last year’s Q2, which will create a difficult compare this year. As such, we anticipate the second quarter will be the low watermark for both internal revenue and adjusted EPS growth with strong acceleration into the back half of the year.

Due to the pending merger, Fiserv has suspended all stock buybacks. Fiserv reiterated its full-year earnings range of $3.39 to $3.52 per share. Fiserv is a buy up to $92 per share.

Four Buy List Earnings Reports on Thursday

We had four more Buy List earnings reports on Thursday, May 2. Let’s start with Church & Dwight (CHD), which reported before the opening bell. For Q1, CHD earned 70 cents per share, which was four cents better than Wall Street’s estimates, as well as CHD’s own guidance.

Q1 net sales rose 3.8% to $1.0447 billion. Organic sales rose by 4.5%. Global consumer products were up 5.2%. Of that, 2.7% was from volume while pricing added 2.5%.

First-quarter net sales grew 3.8% to $1,044.7 million. Organic sales grew 4.5% driven by global consumer-products growth of 5.2%, which was driven by volume growth of 2.7% and positive product mix and pricing of 2.5%. This was CHD’s fourth quarter in a row of organic sales growth topping 4%.

I was pleased to see gross margins increase by 20 basis points to 45.1%. Operating margins rose 120 basis points to 23.1%. The company reiterated its full-year EPS guidance of $2.43 to $2.47. That’s an increase of 7% to 9% over last year. For Q2, CHD expects earnings of 52 cents per share, which matches the Street. Church & Dwight remains a buy up to $75 per share.

Also on Thursday, Intercontinental Exchange (ICE) had a very good earnings report. (We love those pseudo monopolies!) For Q1, the NYSE owner made 92 cents per share. That was two cents more than Wall Street had been expecting. Their adjusted operating margin was 58%.

Q1 revenues were up 4% to $1.3 billion. The breakdown is that revenue for data and listings was $657 million. Revenue for trading and clearing was $613 million. Operating cash flow was $654 million. That’s up 14% from last year’s Q1. The company also noted that the blowup in bitcoin and other cryptos helped ICE acquire discounted assets in order to build its Bakkt platform.

Shares of ICE got off to a relatively slow start this year, but the stock has picked up over the past few weeks. The stock isn’t far from its all-time high, reached in December. Thanks to this week’s earnings report, I think there’s a good chance ICE can break out to a new high. I’m raising my Buy Below on ICE to $86 per share.

“Cognizant’s growth and performance in the quarter leaves room for improvement,” said Brian Humphries, Cognizant Technology’s CEO. Well, I’ll give him points for understated brevity. There’s no easy way to put it. Cognizant Technology Solutions (CTSH) had a terrible Q1.

Let’s look at the damage. For the first three months of this year, Cognizant made 91 cents per share. That was well below Wall Street’s forecast of $1.04 per share. The earnings report came out shortly before the closing bell, and the stock lost 7.7% in Thursday’s session.

Cognizant also cut its full-year forecast. Previously, the company expected EPS this year to be at least $4.40. Now they see it ranging between $3.87 and $3.95.

Where was the weakness? Apparently, the banking sector hasn’t been spending as much. The company’s Financial Services division, which makes up about one-third of its revenue, posted a sales decline of 1.7%. Karen McLoughlin, the company’s CFO, said, “Our revised full-year outlook reflects the first-quarter underperformance and expectations of slower growth in Financial Services and Healthcare for the remainder of 2019.”

I feel confident that Cognizant can manage its way through a difficult environment, but it will take some cost-cutting. For now, I’m dropping my Buy Below on Cognizant Technology Solutions to $70 per share.

After the bell on Thursday, Continental Building Products (CBPX) reported Q1 earnings of 42 cents per share. Expectations were for 34 cents per share. Net sales rose 4.5% to $122 million, and wallboard volume increased by 5.5% to 649 million square feet. We want to see that the company isn’t merely profiting from higher product prices but that they’re selling more units as well.

Continental’s profits were up 16.7% from a year ago. Operating income was up 11.3%. Earlier this year, the company had a malfunction at its Buchanan plant, which went offline for several weeks. That’s now been resolved.

These results are good news for a stock that hasn’t done well over the past few weeks. In fact, the last two earnings reports have been pretty good, but it hasn’t had much impact on the stock price. That may change soon. Buy up to $26 per share.

Three Buy List Earnings Reports Next Week

We have our final three Buy List earnings reports next week. You can see the complete Earnings Calendar. Three months ago, Broadridge Financial Services (BR) bombed its earnings report. For Q2, BR made 56 cents per share, which was 15 cents below estimates. Total revenues fell 6% to $953 million.

For its part, Broadridge didn’t alter its fiscal 2019 guidance. BR sees revenue growth of 3% to 5%, operating margins at 16.5% and EPS growth of 9% to 13%.

For Q3, the company sees revenue between $1.195 billion and $1.245 billion and earnings of $1.40 to $1.56 per share. Wall Street expects $1.50 per share.

At this point, Disney’s (DIS) earnings report seems anti-climatic. The stock just finished up its best month in nearly two decades. The Avengers movie blew up at the box office. For the opening weekend, the movie did $1.2 billion. On top of that, the Disney+ announcement was very well received. For Q1, Wall Street expects earnings of $1.59 per share.

Shares of Becton, Dickinson (BDX) have been uncharacteristically weak lately. The stock lost more than 10% over a four-day period in mid-April. The next earnings report is due out on Thursday, May 9. For 2019, Becton expects revenues to grow by 5% to 6%, and they see EPS ranging between $12.05 and $12.15. For Q1, Wall Street expects earnings of $2.58 per share.

Before I go, I wanted to make two Buy Below adjustments. I’m raising my Buy Below on FactSet (FDS) to $287 per share. The stock has been doing very well for us lately. We’re now +37.2% in FDS this year. Earnings are due out in June. I’m also raising Cerner’s (CERN) Buy Below to $71 per share. The stock just touched a new 52-week high.

That’s all for now. Heads up: I’ll be hitting the road, so next week’s issue will be out on Sunday, May 12. There’s not much in the way of economic reports. Earnings reports will start to taper off. On Thursday, I’ll be on the lookout for the jobless-claims report. Then on Friday, the April CPI report is due out. I expect to see more signs of subdued inflation. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His