Crossing Wall Street – October 11, 2019

“The expectation of an event creates a much deeper impression on the exchange than the event itself.” – Jose de la Vega, 1688

Third-quarter earnings season is finally here! This is like Judgement Day for Wall Street. If you do well, your shares can be richly rewarded. However, if you disappoint the market gods, they show little mercy.

This could the first quarterly earnings decline for the S&P 500 in three years. If I had to guess, I’d say that we’ll narrowly avert a decline, but it will be close. Still, earnings expectations have come down a lot. Since January 1, the estimates for Q3 earnings have been pared back by 8%. The typical Wall Street game is to lower expectations just low enough that companies can beat them by a few percentage points. Then, of course, they declare victory.

In this week’s issue, we’ll look at some of our Buy List stocks that are due to report earnings next week. But first, last week we learned that the unemployment rate fell to a 50-year low, yet the Federal Reserve has been cutting rates, and will likely do so again soon. What gives? I’ll share my thoughts.

It’s a Weird, Weird World

The current state of the economic world is weird. At least, it is to me. All the standards that I learned and had become used to, it seems, have been thrown out the window.

I never thought that bonds with negative yields were possible, yet here we are. There’s several trillion dollars’ worth of them to tell me I’m wrong, so I’ll believe them.

I didn’t think the Federal Reserve could lower interest rates to 0%. Or keep them there for years. Or see other central banks go even lower. Yet it happened.

I didn’t think the U.S. economy could expand at a tepid yet steady pace for ten years. Again, it happened.

Nor did I think the economy could create so many jobs so consistently, yet not see much in the way of wage increases. But we saw it.

It seems to me that the natural interest rate has dropped to near 0%. That’s so bizarre to me, but I suspect it’s true.

All of these trends baffle me, and I can’t explain what’s happening. Sure, I have some ideas. But the point is that the current economic models for the world aren’t very useful right now. The financial crisis broke economics, and no one’s put it back together yet. At some point, I imagine we’ll see some brilliant young professor who will tie all the pieces together. But until then, I’m pretty stumped.

You’ll notice that the conflict I’m describing isn’t so much between me and someone else. It’s really between me and me—what I see going on and what I’ve been taught. I’m not alone.

Here’s the important point for us. You don’t need to have the world figured out to be a good investor. All you really need is discipline and time. I’d also add a suppleness of mind that allows you take in discordant evidence. Most people, when presented with evidence that conflicts with their belief, simply dismiss the evidence. Dogmas offer comfort.

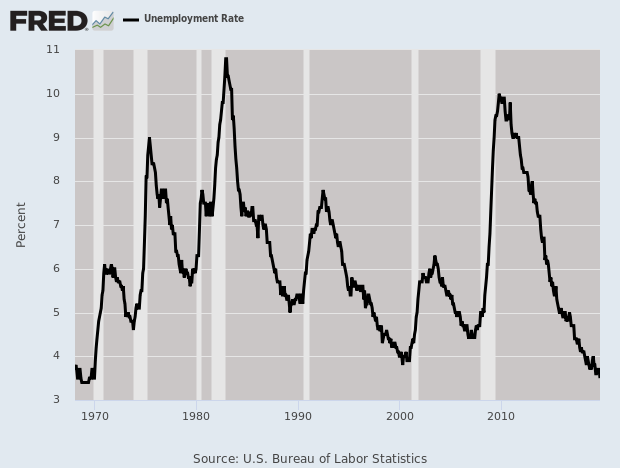

Now let me apologize for that brief bit of navel-gazing, and we’ll turn to last week’s labor report. On Friday, the government said that the economy created 136,000 net new jobs last month. The previous month’s figures were revised a bit higher.

The unemployment rate ticked down to 3.5%. That’s the lowest in 50 years. It’s also the lowest peacetime rate in more than 70 years. (Some folks on Twitter took me to task for calling this peacetime. Sorry, but I stand by my claim. In terms of mobilization, the current deployments are nowhere close to the numbers we saw in Korea and Vietnam. Not to mention that there was a draft.)

Despite the unemployment rate’s being so low, there’s still not much in the way of inflation. This week’s inflation report showed no change for September. The core rate rose by 0.1%. That’s good to hear since the three months prior to that all saw increases of 0.3%. If there was any threat of higher prices, that fear seems to have passed.

This means the Federal Reserve will almost certainly cut interest rates again when they meet on October 30. Another cut will bring the Fed’s target for the Fed funds rate to 1.5% to 1.75%. There’s a chance that the yield curve could revert soon. The spread between the three-month and 10-year yields is down to one basis point. A few weeks ago, the spread was over 50 basis points.

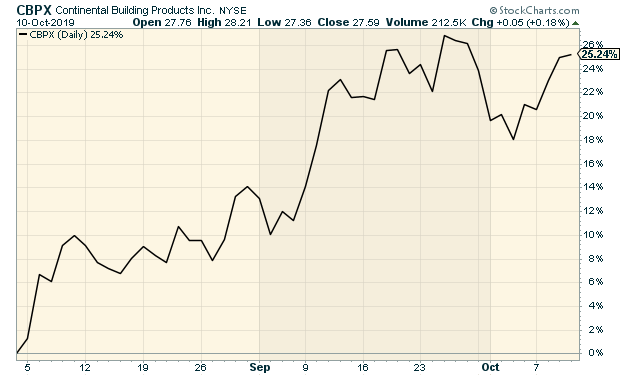

What about after that? I think the Fed might take it easy after that. Lower rates will help the mortgage market, and that will filter down to the housing sector. Have you noticed that Continental Building Products (CBPX), our wayward wallboard stock, is up more than 25% since early August? Sherwin-Williams (SHW), the paint people, just touched a new 52-week high. About this time last year, SHW was getting crushed by the market. As Jesse Livermore said, “It never was my thinking that made the big money for me. It always was my sitting.”

Now let’s turn to earnings season.

Earnings Preview for Eagle Bank and Signature Bank

Earnings season kicks off for us next week when Eagle Bank and Signature Bank are due to report. Actually, I’m guessing that Signature will report on October 17. They haven’t said so yet, but I’m guessing that based on previous years. Eagle has said they’ll report on October 16.

Let’s start with Eagle Bancorp (EGBN) because their last earnings report caused so much trouble. In July, Eagle said they made $1.08 per share for their Q2. That was pretty good. It was four cents more than expectations.

The problem is that Eagle also said their legal bill has soared due to “investigations and related document requests and subpoenas from government agencies.”

A few key points. The bank made it clear that this will not “materially impact its results.” Also, the bank isn’t under any regulatory restrictions. The problem is that Eagle isn’t allowed to talk about what’s happening. I suspect this is connected to local Washington, D.C. political scandals. On July 18, the shares dropped almost 27%.

For Q3, Wall Street expects earnings of $1.07 per share. Eagle is trading for less than 10 times this year’s earnings estimate.

Three months ago, Signature Bank (SBNY) reported earnings of $2.72 per share. That beat expectations by one penny.

Net interest margin came in at 2.75%. That’s down 20 basis points from a year ago. That’s not great, but it’s certainly respectable for this environment.

I’m happy to say that Signature is almost done with its taxi-medallion mess. The bank went into this in a big way, but then thanks to ride-sharing apps, the medallions plunged in price. That left the bank holding a bunch of bum loans.

In Q2, Signature sold off $46.4 million in medallion loans. That leaves them with $18.8 million in non-performing medallion loans plus $43.8 million in repo-ed medallions. It was a costly mistake, but the issue is basically behind them.

For Q3, Wall Street expects Signature to earn $2.70 per share.

Hormel Foods Updates Guidance

This week, Hormel Foods (HRL) hosted an investor day. The Spam folks narrowed their full-year guidance by a tiny bit. Hormel now sees full-year earnings ranging between $1.76 and $1.80 per share. The previous guidance was $1.71 to $1.85 per share.

The shares pulled back some on the news. Q4 results will come out on November 26. Hormel remains a buy up to $46 per share.

That’s all for now. Earnings reports will probably dominate the headlines next week. The bond market will be closed on Monday for Columbus Day, but the stock market will be open. On Wednesday, the retail-sales report comes out. This should give us a good look at consumer spending which had been doing well. Then on Thursday, we’ll get the report on industrial production. There will also be reports on housing starts and building permits. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on October 11th, 2019 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His