CWS Market Review – October 4, 2019

“Investing is where you find a few great companies and then sit on your ass.” – Charlie Munger

So true, Charlie. Too many investors overthink this game.

The S&P 500 wrapped up the third quarter with a small gain. This was the index’s 14th quarterly gain in the last 16 quarters.

Wall Street finally a got a little action this week. The S&P 500 fell by more than 1% on back-to-back days. That was the first time that happened all year. In fact, it looked like Thursday was going to be the third in a row, but a rally saved us. The index is now firmly nestled between its 50- and 200-day moving averages. Wednesday was the market’s worst day in five weeks. The second-worst day was the day before.

If you think that’s bad, for the second quarter of 1932, the market fell more than 1% on each of its first seven trading days!

What gave Wall Street the shakes this week? Some of the economic news was on the light side. As usual, whenever there’s any hint of danger, traders will storm the lifeboats. It’s really not that big of a deal. I’ll break it all down for you in a bit.

I’ll also cover this week’s earnings report from RPM International. This may be one of the quietest stocks on the Buy List, but don’t overlook it. Its shares have been in rally mode over the past three months. RPM also announced its 46th consecutive dividend hike. There aren’t many companies like that. I’ll have all the details in a bit. But first, let’s look at what upset Wall Street this week.

Weak Economic News Rattles the Market

The new month and quarter began this week. With the turn of the month, we typically get several important economic reports. The ISM Manufacturing Index usually comes out on the first day of the month.

I like the ISM report because the data is current. It’s a survey rather than hard data. On Tuesday, I wasn’t expecting to see a good report. We already knew that the manufacturing sector has been struggling. Still, the ISM came in at 47.8 which is worse than I expected. It’s the lowest number in more than 10 years.

Any number below 50 means that the factory sector of the U.S. economy is shrinking. This was the second sub-50 number in a row. To give you an idea of how things have changed, a year ago, ISM reached a 14-year high. The details of the report aren’t encouraging.

The group said just three of 18 industries reported growth in September, the lowest total since April 2009. Contracting industries were led by apparel, leather and allied products; printing and related support activities; and wood products. The only expansions were in miscellaneous manufacturing; food, beverage and tobacco products; and chemical products.

ISM’s measure of new orders, considered a leading indicator of downturns, edged up slightly to 47.3 from an August reading that matched the weakest of this expansion. The production index declined to 47.3, while the inventories gauge fell to 46.9, the lowest since late 2016.

The ISM Manufacturing Report also has a decent track record of lining up with recessions, but we’re still above the danger zone. Generally, recessions happen when the ISM drops below 45. So, we’re not in a recession, but growth may be slowing down.

I should add that this is simply for the manufacturing sector of the economy. The economy has had periods of strong growth with soggy ISMs. The 1990s is a good example.

The problem is that on Thursday, we got the ISM Non-Manufacturing Report, and it was also below expectations. The reading was 52.6 which was the lowest in three years. Wall Street had been expecting 55. Since it’s above 50, we know that the Non-Manufacturing sector is still expanding, but it challenges the theory on Wall Street that the consumer is holding up the economy while the factory sector is in a recession.

Until this week, it had been popular to believe that the Fed might not be in such a hurry to cut rates again. They’ve already done so twice, but would a third be necessary? There were three dissents at the last meeting. Charles Evans, the top guy at the Chicago Fed, said that the latest numbers haven’t convinced him to cut rates again. The Atlanta Fed now estimates that the economy grew by 1.8% for Q3.

The FOMC meets again at the end of this month. At the start of the week, the futures markets thought there was a 40% chance of a Fed cut in October. Thanks to this week’s news, the odds of a rate cut are now up to 88%.

The big news for this week will be the jobs report which is due out later this morning. The consensus is that the economy created 146,000 net new jobs. On Wednesday, we got the ADP payroll report which is an imperfect preview of the government’s official report.

ADP said that the U.S. economy added 135,000 private jobs last month. That was 10,000 more than expected. That’s the good news. The bad news is that the numbers for August were revised lower. The economy is still creating jobs, but the rate of increase is slowing.

On Thursday, the initial jobless claims report fell to 219,000. That’s still quite good. In fact, jobless claims have been mostly in a range between 210,000 and 230,000 for much of the last eight months.

After Thursday morning’s initial drop, stocks rallied. Forgive me if this sounds bizarre, but stocks rallied on the bad news. Not because of the bad news itself, but because the bad news would spur the Fed to act, and that’s good news. I feel like we need Abbott and Costello to sort this out.

This week, the World Trade Organization cut its forecast for trade growth for this year and next. The big worry is that the trade spat between the U.S. and China could push the global economy into a recession. In that case, there’s not much that the Fed can do with rate cuts. It would be like pouring gasoline into a car that doesn’t have any wheels.

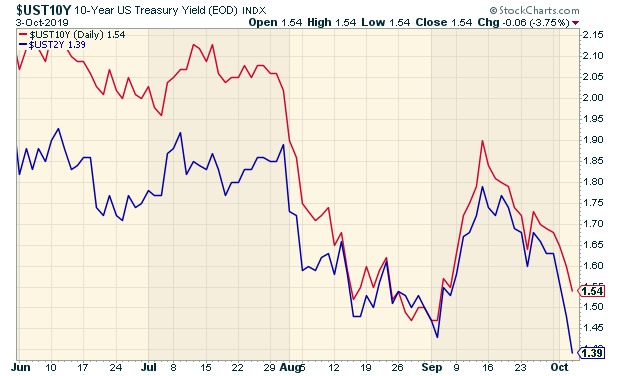

The bond market is feeling the pressure as well. In early September, the 10-year yield was going for less than 1.5%. By September 13, the yield had shot up to 1.90%. But the bond market made a U-turn and yields are plunging again. On Thursday, the 10-year yield closed at 1.54%.

The difference this time is that the yield curve has re-inverted. By that, I mean that even though the 10-year yield is down, the two-year yield has fallen even faster. Much faster. This week, the two-year yield fell to its lowest level since October 2017. As a result, the spread between the two and the ten is the widest it’s been since early August.

Remember how in August everyone freaked out about the Great Yield Curve Inversion of 2019? Well, that lasted for about one week. (See Charlie Munger’s words in this week’s epigraph.)

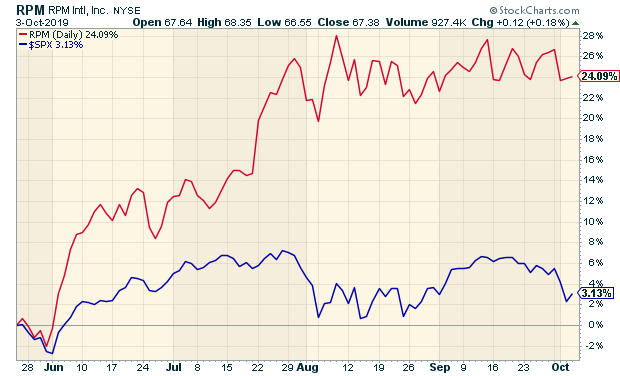

RPM International Beats by Three Cents per Share

On Wednesday, RPM International (RPM) released its fiscal Q1 earnings report, and the news was mixed. Let’s start with the good news. For the first three months of its fiscal year, RPM earned 95 cents per share. That was three cents more than expectations. Net sales were $1.47 billion compared to $1.46 billion for last year.

“We continued to experience the benefits of the plant rationalization, manufacturing improvements and center-led procurement initiatives of our 2020 MAP to Growth operating improvement plan during the quarter. These actions resulted in adjusted EBIT and EPS performance that met our projections despite modest top-line sales growth,” stated RPM chairman and CEO Frank C. Sullivan. “As we anticipated in July, sales growth was modest as a result of an extremely wet June that slowed painting and construction activity in North America and unfavorable foreign exchange. We were encouraged to see our restructuring program drive significant EBIT margin improvement across all of our segments. On a consolidated basis, our adjusted EBIT margin improved 260 basis points.”

RPM’s guidance wasn’t terrible, but it could have been better. For Q2, RPM expects sales to rise by 2% to 3% and EPS to be in the “low- to mid-70-cent range.” Let’s say that’s 72 to 75 cents per share. Wall Street had been expecting Q2 earnings of 76 cents per share.

RPM is reaffirming its previous guidance for the full year; however, the company now expects revenue growth to be at the low end of its range of 2.5% to 4%. RPM is standing by its projected adjusted EBIT growth, which is between 20% and 24%. For 2020 EPS, RPM still sees earnings ranging between $3.30 and $3.42 per share.

The important thing is that RPM did not cut its EPS guidance. The shares initially dropped on Wednesday but eventually rallied and closed a little bit higher, while the rest of the market was down. RPM closed higher on Thursday as well.

On Thursday, RPM increased its dividend for the 46th year in a row. The quarterly payout will rise from 35 to 36 cents per share. Only 41 companies have longer dividend-hike streaks. Based on Thursday’s closing price, RPM now yields 2.14%.

Since late May, RPM has rallied 24.1% for us, while the S&P 500 is up just 3.1%. I’m keeping my Buy Below prices at $71 per share.

Before I go, I want to make two minor changes to our Buy Below prices. This week, I’m lowering our Buy Below on Cognizant Technology Solutions (CTSH) to $64 per share. I’m also lowering our Buy Below on Cerner (CERN) to $71 per share. Nothing is wrong with either company. I’m just updating these numbers to reflect the current market.

That’s all for now. Third-quarter earnings seasons is set to begin soon. There are a few key economic reports to look forward to next week. On Wednesday, the Fed will release the minutes of their last meeting. This was an important meeting because the Fed cut rates and there were three dissensions. That’s unusual. Then on Thursday, the CPI report for September is due out. I’ll be curious about what it has to say, because core inflation has been running hot. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on October 4th, 2019 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His