Archive for December, 2019

-

Danaher Announces Final Results Of Envista Exchange Offer

Eddy Elfenbein, December 18th, 2019 at 9:15 amDanaher Corporation (NYSE: DHR) announced today the final results of its previously announced offer to holders of shares of Danaher common stock to exchange their shares of Danaher common stock for shares of common stock of Envista Holdings Corporation (NYSE: NVST) owned by Danaher. The exchange offer expired at 12:00 midnight, New York City time, at the end of the day on December 13, 2019.

Based on the final count by the exchange agent, Computershare Trust Company, N.A., the final results of the exchange offer are as follows:

Total number of shares of Danaher common stock validly tendered and not validly withdrawn: 304,607,504

Shares validly tendered that were subject to proration: 303,682,229

“Odd-lot” shares validly tendered that were not subject to proration: 925,275

Total number of shares of Danaher common stock accepted: 22,921,984

Today, Danaher accepted 22,921,984 of the tendered shares in exchange for the 127,868,000 shares of Envista common stock owned by Danaher. Because the exchange offer was oversubscribed, Danaher accepted only a portion of the shares of its common stock that were validly tendered and not validly withdrawn, on a pro rata basis in proportion to the number of shares tendered. Stockholders who owned fewer than 100 shares of Danaher common stock, or an “odd-lot,” who validly tendered all of their shares, were not subject to proration, in accordance with the terms of the exchange offer. All shares validly tendered by eligible “odd-lot” stockholders have been accepted. The final proration factor of 7.2433% had been applied to all other validly tendered shares of Danaher common stock to determine the number of such shares that were accepted.Shares of Danaher common stock tendered but not accepted for exchange will be returned to the tendering stockholders in book-entry form promptly. In addition, the exchange agent will promptly credit shares of Envista common stock for distribution in the exchange offer in book-entry form to accounts maintained by the Envista transfer agent for tendering stockholders whose shares of Danaher common stock were accepted in the exchange offer. Checks in lieu of fractional shares of Envista common stock will be delivered after the exchange agent has aggregated all fractional shares and sold them in the open market.

Goldman Sachs & Co. LLC and J.P. Morgan Securities LLC served as the dealer managers for the exchange offer. Evercore served as an advisor to Danaher for the exchange offer.

-

Morning News: December 18, 2019

Eddy Elfenbein, December 18th, 2019 at 7:28 amU.S. Concedes Defeat on Gas Pipeline It Sees as Russian Threat

Trump’s Trade Deals Raise, Rather Than Remove, Economic Barriers

PG&E Reaches $1.7 Billion Deal With Regulators

Fiat Chrysler, Peugeot Owner Agree to Binding $50 Billion Merger Deal

Boeing 737 MAX Freeze Divides Suppliers Into Haves and Have-Nots

Apollo and Blackstone Are Stealing Wall Street’s Loans Business

H&M’s Different Kind of Click Bait

With Promotion Of New CMO, Coca-Cola Revisits Previously Retired Role

Bed Bath & Beyond’s New CEO Just Blew Up His Executive Circle — In the Midst of the Holiday Season

How the Immigrant Dream Died in an Automotive Shantytown

SoftBank Vision Fund Employees Depict a Culture of Recklessness

Nick Maggiulli: Climbing the Wealth Ladder

Howard Lindzon: The Rarest Of Years and Decades for Markets

Joshua Brown: The Top Performing Stocks of the Decade & Why Apple Is The Most Emblematic Stock of 2019

Be sure to follow me on Twitter.

-

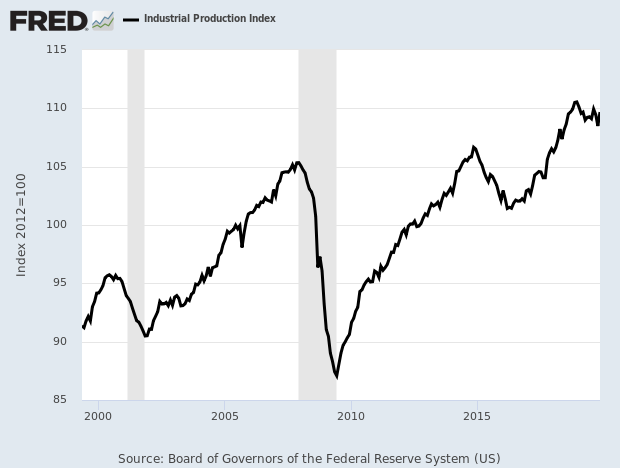

Rebound in Industrial Production

Eddy Elfenbein, December 17th, 2019 at 2:34 pmThe market is up again this morning, and again, not by much. This could be the fifth daily gain in a row for the S&P 500.

We also finally got some good production news. This morning, the industrial production report for November showed an increase of 1.1%. That’s pretty good. Wall Street had been expecting an increase of 0.7%. Some of this was due to the end of the GM strike.

The Fed’s measure of the industrial sector comprises manufacturing, mining, and electric and gas utilities.

There was a 12.4% jump in the production of motor vehicles and parts in November. Overall, production rose 2.1% for consumer goods and 1.7% for business equipment, the Fed said.

Utilities output increased 2.9% compared to a decline of 2.4% in the previous month.

The manufacturing sector, which makes up about 11% of the U.S. economy, has been weakened by a 17-month trade war between the United States and China.

Last Friday, the world’s two largest economies announced a “Phase one” agreement that reduces some U.S. tariffs in exchange for increased Chinese purchases of American farm goods.

-

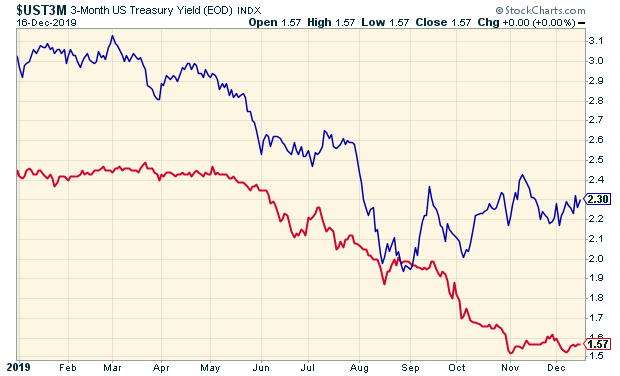

Chart of the Year

Eddy Elfenbein, December 17th, 2019 at 2:30 pmThe Fed’s recent cuts have impacted the mortgage market. The average rate on a 30-year fixed-rate mortgage in the U.S. is 3.73%. Mortgage rates are already 1% below where they were one year ago, and I think it is very likely that interest rates will stay low. That’s good for the economy and the housing sector.

This is really the culmination of a dramatic yield curve story that played out all year. Let’s take a look at one of my top candidates for Chart of the Year.

The chart above shows the yield on the three-month Treasury (in red) along with the 30-year Treasury (in blue). You can see how both were trending downward during the first half of this year. However, starting in the summer, the gap between the two narrowed dramatically. By August, the ten-year yield briefly dipped below the three-month yield. That was the dreaded inverted yield curve that made headlines for about 36 hours.

It was almost like a cry for help from the bond market. The Federal Reserve heard the pleas and moved to act. The Fed slashed rates three times in three months.

At the time, a lot of folks on Wall Street, especially the bears, thought this was the beginning of a rate-cutting cycle. The Fed said that their moves were merely mid-cycle adjustments. The Fed held firm and it appears that Jerome Powell and his friends on the FOMC have prevailed again the bond market.

What makes me say that? Notice how the 10-year yield (the blue line) has started to stabilize in recent weeks. The yield is actually above the lows from a three months ago. This probably hints at a re-accelerating economy. Also, inflation continues to remain low.

-

Morning News: December 17, 2019

Eddy Elfenbein, December 17th, 2019 at 6:49 amChina May Buy Ethanol, Divert Hong Kong Trade to Hit U.S. Pledge

Mortgage Rates Below 1% Put Europe on Alert for Housing Bubble

Liquor Taxes Could Go Up 400%, Thanks to Congressional Dysfunction

Fed Alumni Fear Crisis Risk in Simultaneous Cuts to Rules, Rates

Boeing to Temporarily Shut Down 737 Max Production

Boeing’s Production Pause Will Not End 737 Max Cash Burn

Roche to Complete $4.3 Billion Spark Deal as Regulators Give All Clear

Disney Bets on Nostalgia to Pull ‘Star Wars’ Saga Out of Decline

Amazon Blocks Sellers From Using FedEx Ground for Prime Shipments

Two Men Admit to Working on Illegal Streaming Sites that Rivaled the Size of Netflix and Hulu

Visa Warning: Hackers Ramp Up Card Stealing Attacks At Gas Stations

Cullen Roche: Intangible Returns

Michael Batnick: The Twitter Types

Jeff Miller: Stock Exchange: Intuition or Intu Wishing?

Ben Carlson: Jimmy Hoffa & General Motors: When Labor Ruled the World & Talk Your Book: The Case For Tactical Equity

Be sure to follow me on Twitter.

-

Homebuilder Confidence Hits 20-Year High

Eddy Elfenbein, December 16th, 2019 at 1:11 pmA stronger economy and a severe housing shortage have the nation’s homebuilders feeling better than they have in two decades.

Builder confidence in the newly built, single-family home market jumped 5 points in December to 76, the highest reading since June 1999, according to the National Association of Home Builders/Wells Fargo Housing Market Index. Anything above 50 is considered positive.

November’s reading was also revised higher by 1 point. The index stood at 56 last December. At the worst of the housing crash, in 2009, builder sentiment hit a low of just 8.

“Builders are continuing to see the housing rebound that began in the spring, supported by a low supply of existing homes, low mortgage rates and a strong labor market,” said NAHB Chairman Greg Ugalde, a homebuilder and developer from Torrington, Conn.

Builders’ confidence is clearly based on what they’re seeing in their showrooms. Of the index’s three components, current sales conditions rose 7 points to 84, sales expectations in the next six months rose 1 point to 79 and buyer traffic increased 4 points to 58.

All, however, is not perfect in the homebuilding market. Builders could likely be doing even better if they didn’t face so many headwinds.

“While we are seeing near-term positive market conditions with a 50-year low for the unemployment rate and increased wage growth, we are still underbuilding due to supply-side constraints like labor and land availability,” said NAHB chief economist Robert Dietz. “Higher development costs are hurting affordability and dampening more robust construction growth.”

-

Morning News: December 16, 2019

Eddy Elfenbein, December 16th, 2019 at 6:51 amU.S. Top Trade Negotiator Praises Deal, China Remains Cautious

U.S. Economy Shakes Free of Recession Fears in Striking Turnaround Since August

There Are Economic Warning Signs for Trump in the Midwest

Market Primed for First Quarter ‘Melt-Up,’ Says Bank of America

A Third of America’s Economy Is Concentrated in Just 31 Counties

IFF Wins DuPont Nutrition Unit Over Kerry in $26.2 Billion Deal

Netflix Shuns Commercials, but It’s Cozying Up to Brands

Cineworld Tops North American Box Office With Cineplex Deal

From Zero to 4, Before the End of the Driveway

Europe’s Richest Man Earns $39 Billion in 2019

Joshua Brown: My Favorite Expense

Jeff Carter: Being Competitive and Grinding

Roger Nusbaum: Ultimately It Comes Down To Accountability & How Lifting Weights Can Improve Your Retirement Planning

Be sure to follow me on Twitter.

-

Cerner Increases Share Repurchase Program

Eddy Elfenbein, December 13th, 2019 at 2:16 pmCerner Corporation (CERN), a global health care technology company, today announced that its Board of Directors declared a cash dividend to stockholders of $0.18 per issued and outstanding share. The cash dividend will be payable on Jan. 9, 2020, to shareholders of record as of the close of business on Dec. 27, 2019.

Cerner intends to pay regular quarterly cash dividends, with future declarations subject to approval by its Board of Directors and their determination that the declaration of dividends remains in the best interests of Cerner and its shareholders. The decision of whether to pay future dividends and the amount of any such dividends will be based on the company’s financial position, results of operations, cash flows, capital requirements, the requirements of applicable law and any other factors the Board of Directors may deem relevant.

Cerner also announced that its Board has approved an amendment to its stock repurchase program, authorizing the repurchase of an additional $1.5 billion of its common stock. Cerner has repurchased $1.3 billion of its shares in 2019 and had $0.2 billion of available authorization remaining prior to the increase announced today. The total authorized amount available for repurchase is now $1.7 billion.

Cerner plans to repurchase shares in the open market, by block purchase, in privately negotiated transactions or possibly through other transactions managed by broker-dealers. No time limit was set for completion of the program, and the timing and amount of repurchases will depend on how much funding is used for other purposes, such as acquisitions. The Company intends to fund its capital allocation program, including share repurchases, dividend payments and other uses, with cash from operations and debt.

“The Board of Directors and our leadership team believe Cerner’s shares are an attractive investment, and our expanded repurchase program and quarterly dividend reflect our ongoing commitment to returning capital to shareholders and the company’s belief in Cerner’s long-term potential,” said Marc Naughton, executive vice president and chief financial officer. “We have a strong balance sheet and expect to continue generating strong cash flow that can support ongoing investments in growth and a balanced capital allocation strategy.”

-

CWS Market Review – December 13, 2019

Eddy Elfenbein, December 13th, 2019 at 7:08 am“The labor market remains strong and that economic activity has been rising at a moderate rate.” – This week’s FOMC policy statement

Wall Street is in a festive mood this holiday season. The S&P 500 just closed at another new all-time high. The index is now up 26.4% for the year. That’s the 27th time this year that the S&P 500 has broken records.

This week, the Federal Reserve decided against changing interest rates. In fact, the Fed’s outlook suggests they won’t touch rates during all of next year as well. Last week, we also had another strong jobs report. The unemployment rate is now down to a 50-year low. And it looks like we might finally get some sort of trade deal with China.

In this week’s CWS Market Review, we’ll take a closer look at what the Fed had to say. I also want to discuss how the U.S. economy is doing. Later on, I’ll preview next week’s earnings report from FactSet. (And don’t forget that on Christmas Day, I’ll be sending you the stocks for the 2020 Buy List.) But first, let’s look at last week’s jobs report.

The U.S. Economy Is Still Creating Jobs

Last Friday, the government released the November jobs report, and the numbers were quite good. The U.S. economy created 266,000 net new jobs last month. The forecast had been for 187,000. There were also positive revisions of 41,000 jobs (13,000 to September and 28,000 to October).

Manufacturing saw an increase of 54,000 jobs. Motor vehicles and parts rose by 41,000 thanks to the end of the GM strike. Healthcare, as well as leisure and hospitality, rose by 45,000.

The unemployment rate ticked down to 3.5%, which is a 50-year low. The U-6 Rate, which is a broader measure of joblessness, ticked down 0.1% to 6.9%. The labor-force participation rate is 63.2%. That also fell by 0.1%.

The jobs market is the best it’s been in a generation. The investment writer Gary Alexander notes some interesting stats. The number of Americans able to work but not actively seeking jobs fell by 432,000 (-27%) over the last year. Only one-fifth of the 3.5% jobless have been out of work for 27 weeks versus 45% of the jobless who were out of work that long in 2011. In Ames, Iowa, the unemployment rate is just 1.3%.

The weak point is still wages. For November, average hourly earnings rose seven cents to $28.29. In the last year, wages are up 3.1%. That’s actually an improvement, but we still need to see more. Wages eventually become revenue.

On Thursday, we got an unusually high jobless-claims report. It was the highest in more than two years. The number tends to be “noisy,” so I’m not concerned just yet, but it’s something to take note of.

Fortunately, inflation still isn’t a problem. On Wednesday, the government said that inflation rose 0.3% in November. That topped expectations by 0.1%. Part of the rise was due to gasoline prices. In the last 12 months, consumer prices are up 2.1%.

The core rate, which excludes food and energy, rose by 0.2% in November. In the last year, core prices rose by 2.3%. The important point is that the Fed is still below the inflation rate. This means that real rates are negative. They had been positive a few months ago. So where do rates go from here?

In this week’s Fed policy statement, the central bank had good things to say about the economy. The Fed said the labor market is strong and the economy is growing at a moderate rate. Household spending is rising at a strong pace, and inflation is tame. The Fed noted that two weak areas are business fixed investment and exports.

The Fed decided against raising rates, and the decision was unanimous. The Fed hasn’t had a one-sided vote in several months. Fed Chairman Jay Powell said that the recent rate cuts were merely mid-cycle adjustments. There were a lot of doubters, but it appears that Powell has prevailed.

The Fed also released its economic projections for the next few years. According to the median vote, the Fed doesn’t see itself changing rates all next year. Even in 2021, the Fed forecasts one rate change, and again, no changes in 2022.

Permit me one econo-nerdy point. In the Fed’s projections, they forecast a “long run” rate for different data series. They peg the long-run interest rate at 2.5% and the long-run inflation rate at 2.0%. Frankly, those are pretty meaningless, but with one exception. This implies that the Fed sees the neutral real rate at 0.5%.

For years, the neutral rate was assumed to be about 2%, give or take. If someone told you 10 or 15 years ago that the Fed would eventually see the neutral rate at 0.5%, they would have been stunned. The lower neutral rate has changed so many basic assumptions about the financial markets, and getting used to it has caused a lot of the doomsday crowd to miss a great stock market. Now let’s look at our Buy List earnings report for next week.

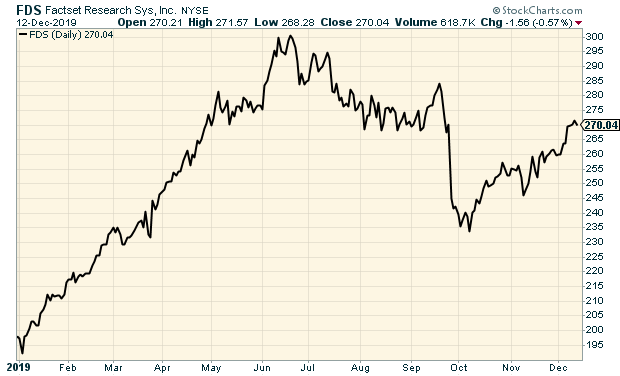

Earnings Preview for FactSet

FactSet (FDS) is due to report its fiscal Q1 earnings on Thursday, December 19. Three months ago, the company had a very good earnings report. The problem was that guidance was below expectations.

For its fiscal Q4, FactSet said that revenues rose 5.3% to $364.3 million. Annual Subscription Value, or ASV, rose to $1.48 billion. Quarterly earnings rose 18.6% to $2.61 per share. Wall Street had been expecting $2.47 per share.

This was FactSet’s 39th year in a row of revenue growth and 23rd year in a row of EPS growth. I was particularly glad to see FactSet’s operating margin come in at 33.9%. For the quarter, client count rose by 119 to 5,574. User count rose by 3,871 to 126,833. FactSet’s annual retention rate is running at 89%. The company now has 9,681 employees.

Now let’s look at guidance, and let’s bear in mind that FDS is being quite conservative. The company sees earnings for the current fiscal year (ending in August 2020) ranging between $9.85 and $10.15 per share. That’s basically no growth at all. The range is -1.5% to +1.5%. Wall Street had expected $10.52 per share.

FactSet sees revenues ranging between $1.49 billion and $1.50 billion. That’s up from $1.44 billion for the year that just ended.

Regarding guidance, I want to remind you that FactSet’s initial guidance for last year was $9.50 to $9.65 per share, and they ended up making $10.00 per share. That should tell you how they look to keep expectations low.

The shares took a big hit in September, but FDS has made back most of the lost ground.

Buy List Updates

Disney (DIS) has another big hit with Frozen 2. Elsa and her friends will soon top $1 billion at the box office. That will be Disney’s sixth billion-dollar release this year. Of course, that doesn’t include Star Wars, which is due out in a few days. All told, Disney has made $10 billion at the box office this year. The new streaming service, Disney+, has been downloaded 22 million times. Disney remains a buy up to $152 per share.

RPM International (RPM) said it will release its fiscal Q2 earnings before the bell on January 8. The consensus on Wall Street is for earnings of 73 cents per share.

Danaher (DHR) is giving its shareholders an option to buy shares of Envista (NVST) that DHR owns. Envista used to be Danaher’s dental business. Now it’s a stand-alone company with its own stock.

The deal works like this: You can get 5.5784 shares of NVST for each share of DHR you tender.

For Buy List purposes, we’re not taking the deal because it would violate our set-and-forget philosophy, but it’s not a bad one for shareholders. The ratio works out to a 4.5% discount for NVST based on Thursday’s close.

I’ll caution you that you might not get all the shares you want. That’s just how these deals work. Remember that as a DHR shareholder, you’ll still own some NVST indirectly. The deal expires at midnight tonight. I’m raising my Buy Below on Danaher to $155 per share.

I also want to raise my Buy Below prices on two more our Buy List stocks. This week, I’m lifting my Buy Below on Moody’s (MCO) to $245 per share, and I’m lifting Signature Bank (SBNY) to $141 per share.

That’s all for now. Next week will be rather light for economic news. On Tuesday, we’ll get the report on industrial production. On Thursday, the existing-home-sales report is due out. Then on Friday, we’ll get the second revision to the Q3 GDP report. The last revision showed growth of 2.1%. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: December 13, 2019

Eddy Elfenbein, December 13th, 2019 at 7:05 amJohnson Wins Crushing Majority in Election That Upends Britain

British Election, Advancing Brexit, Heralds End of a Global Trade Era

Brexit Once Meant a Weaker British Pound, but Not Anymore

Lagarde Wants an `Economic Ballet.’ It Could Be a Mosh Pit.

Trump’s China Deal Flirts With the Curse of a Phase One and Done

U.S. Sets China Trade Deal Terms, Sources Say, But Beijing Mum

How Ethanol Plant Shutdowns Deepen Pain for U.S. Corn Farmers

Saudi Aramco IPO is Latest Example of Why It’s Best to Wait to Invest in Newly Public Companies

Why the Fed May Need to Slash Rates to Zero Before the End of 2020

Bank Regulators Disagree on Changes to Rules for Poor Communities

Broker Group Warns of Investor Risks Posed by U.S. Direct Share-Listing Proposal

Oracle Won’t Return to Dual-CEO Structure

Ben Carlson: Raising the Best Kids You Can & Animal Spirits: Murder of the American Dream

Michael Batnick: The Rise and the Fall & Emotional Alchemy

Howard Lindzon: Domino’s The True Netflix and Chill Winner

Be sure to follow me on Twitter.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His