Archive for June, 2020

-

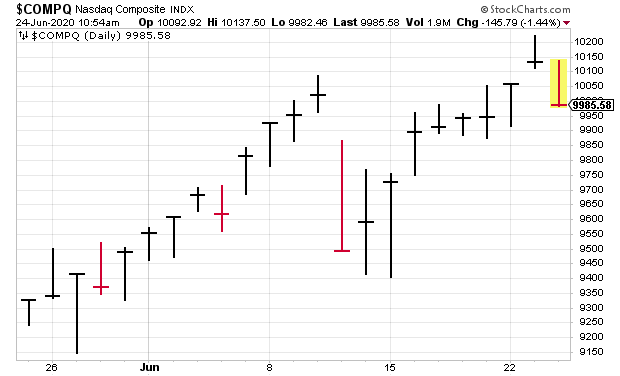

The Nasdaq’s Win Streak Looks to End

Eddy Elfenbein, June 24th, 2020 at 10:53 am

The stock market is down sharply today. At its low, the S&P 500 was down about 1.6%. The Nasdaq Composite looks to snap its eight-day win streak.

There are concerns about the growing numbers of coronavirus cases. The seven-day average of news cases is up 30% from a week ago. There’s even talk of reversing some of the recent re-openings.

So far, Energy and Financial stocks are down the most while Consumer Staples and Utilities are down the least. This suggests the market is concerned about the economy’s underlying strength. Sonos, the speaker-maker, said it’s going to cut 12% of its workforce due to the coronavirus.

There’s not much in the way of economic news today. Next week will be interesting because the stock market will be closed on Friday, July 3. That means that the jobs report will come out on Thursday. Also, the jobs report will come at the same time as the jobless claims report. It will be interesting to see if traders want to be net long going into the three-day weekend.

-

Morning News: June 24, 2020

Eddy Elfenbein, June 24th, 2020 at 6:31 amGold Shines As Coronavirus Surge Unnerves Investors

U.S. Eyes $3.1 Billion of EU, U.K. Imports for New Tariffs

The Pandemic’s Worst-Case Scenario Is Unfolding in Brazil

The Tiny Bank That Got Pandemic Aid to 100,000 Small Businesses

Can a Private-Equity Giant Invest in Oil While Saving the Planet?

TaskRabbit C.E.O. to Step Down, a Blow for Silicon Valley Diversity

The New Escapism: Isolationist Travel

Disney Exits Language School Business in China, Citing Coronavirus

Nick Maggiulli: Roth 401(k) vs. 401(k): Which is the Better Option?

Ben Carlson: Why Are Credit Card Interest Rates So High?

Michael Batnick: The Biggest Stock Market Rally Ever

Jeff Carter: Great Companies, Tough Times

Cullen Roche: Three Things I Think I Think – Market Bonanza!

Howard Lindzon: Keep It Simple and $QQQ Over $SPY

Joshua Brown: “The German Enron” & Why Public Banned Its Users From Trading in Hertz Shares

Be sure to follow me on Twitter.

-

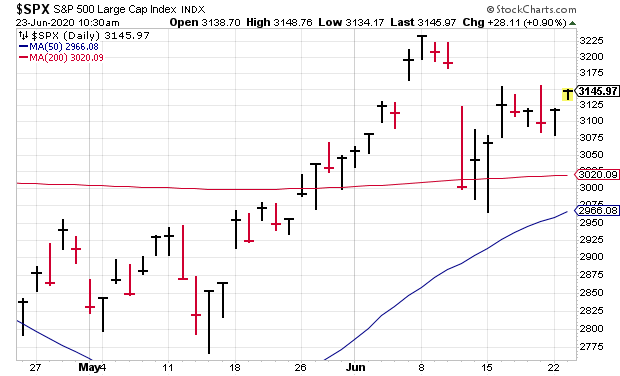

All-Time High for the Nasdaq

Eddy Elfenbein, June 23rd, 2020 at 10:31 am

The stock market is up nicely so far today. This could be our sixth gain in the last eight sessions. The S&P 500 may be able to close at its highest point in nearly two weeks.

The Nasdaq hit a record high today. Michael Batnick points out that the Big Five (Apple, Google, Amazon, Facebook and Microsoft) now account for 22% of the S&P 500. That’s over $6 trillion. Four of the five are at new highs today. Only Google is left out.

The markets were nervous overnight as there were concerns about a trade deal between the United States and China. I’m glad to see that’s gone.

This morning’s new-home sales report showed an increase to 676,000 (that’s the annualized figure). Wall Street had been expecting 640,000. The previous three months were revised down.

-

Morning News: June 23, 2020

Eddy Elfenbein, June 23rd, 2020 at 7:07 amDefying Dire Predictions, China Is the Bubble That Never Pops

Betraying Frustration with China, E.U. Leaders Press for Progress on Trade Talks

Thumping Data Drives Stocks And Oil Higher

ADNOC Inks $10 Billion Deal, Keeps Tight Control Of Costs Amid Market Downturn

Culture of Inflating Oil Reserves Helped Stoke U.S. Shale Boom

White House Adviser Navarro Walks Back On Comments China Trade Deal ‘Over’

Fearful Commuters on Trains, Buses Hold One Key to U.S. Recovery

A Multibillion-Dollar Opportunity: Virus-Proofing the New Office

Pandemic Travel Patterns Hint at Our Urban Future

Former Wirecard CEO Arrested On Suspicion Of Falsifying Revenue

Michael Batnick: A Small Update on the Giants

Howard Lindzon: Momentum Monday…Gold, Chinese Internet And Biotech Look Good

Joshua Brown: Something To Hate For Everyone

Be sure to follow me on Twitter.

-

NAR: Existing-Home Sales to Post “Strong Rebound”

Eddy Elfenbein, June 22nd, 2020 at 11:24 amThe stock market opened down a bit this morning but is now in positive territory. The Nasdaq is hovering right at 10,000.

This morning’s existing-home sales report showed a drop of 9.7% for May. The good news is that the National Association of Realtors expects a “strong rebound” in the coming months. There’s also been more talk of a surge in coronavirus cases, but for now, the markets don’t seem too worried.

On our Buy List, Sherwin-Williams (SHW) increased its sales guidance for the second quarter.

The Company now expects second quarter 2020 consolidated net sales to decrease by a mid-single-digit percentage compared to the second quarter of 2019. The Company’s prior guidance, issued April 29, 2020, was for second quarter 2020 consolidated net sales to decrease by a low to mid-teens percentage compared to the second quarter of 2019.

-

Sherwin-Williams Increases Second Quarter 2020 Sales Guidance

Eddy Elfenbein, June 22nd, 2020 at 7:42 amThe Sherwin-Williams Company (NYSE: SHW) today increased its net sales guidance for the second quarter of 2020. The Company now expects second quarter 2020 consolidated net sales to decrease by a mid-single-digit percentage compared to the second quarter of 2019. The Company’s prior guidance, issued April 29, 2020, was for second quarter 2020 consolidated net sales to decrease by a low to mid-teens percentage compared to the second quarter of 2019.

On a segment basis, second quarter net sales in The Americas Group are expected to be down by a high-single-digit percentage compared to the previous guidance of down by a low-double-digit to mid-teens percentage. Net sales in the Consumer Brands Group are expected to be significantly above the high end of the previous guidance of up by a high-single-digit to low-double-digit percentage. Net sales in the Performance Coatings Group are expected to be in line with the previous guidance of down by a high-teens percentage.

“Our employees have performed admirably during this challenging time to meet our customers’ needs,” said Chairman and Chief Executive Officer, John G. Morikis. “We are raising our second quarter sales guidance given our ability to capture and serve greater than expected demand in our North American architectural businesses.

“We are encouraged by the sequential improvement in all three of our business segments during the second quarter. In The Americas Group, we rapidly adapted to the pandemic by implementing curbside pickup in our stores, utilizing our fleet of over 3,000 delivery vehicles, and leveraging our e-commerce platform. We have gradually and safely reopened nearly all of our sales floors over the last month. DIY growth in our stores remains strong, while our residential repaint and new residential segments have improved at a faster rate than our property management, new commercial and protective and marine segments. In the Consumer Brands Group, the unprecedented demand from most of our retail partners has remained robust, driven by consumers who are nesting during the pandemic and focused on DIY projects. In the Performance Coatings Group, demand has been variable by end market and geography. Packaging remains our strongest performer, while demand in our coil business has been choppy following the slower reopening of many commercial construction projects. Our automotive refinish business remains under pressure as driving trends have not yet returned to pre-pandemic levels. Recovery remains sluggish in our general industrial and industrial wood businesses.

“Although uncertainties in the timing and pace of improvement in the U.S. and global operating environments continue, we remain confident in our ability to successfully manage through these challenging conditions while continuing to invest and execute on initiatives that will drive our long-term growth.”

The Company is scheduled to release second quarter 2020 financial results on July 28, 2020, at which time it will provide its outlook on third quarter sales and update its full year sales and earnings per share guidance.

-

Morning News: June 22, 2020

Eddy Elfenbein, June 22nd, 2020 at 7:09 amGlobal Dollar Crunch Appears Over As Central Banks Rely Less On Fed Backstop

Why Japan’s Jobless Rate Is Just 2.6% While the U.S.’s Has Soared

Hedge Funds Exploit CLO Weakness Laid Bare by Corporate Distress

Pandemic Propels Old-School Bond Traders Towards An Electronic Future

New Hope for White-Collar Job Seekers? It Depends on the Job

Eerie Calm Settles On Housing Market, Defying Doomsayers For Now

Apple To Update Developers, Possibly Signal Split From Intel

Wirecard Says Missing $2 Billion Never Existed. Its Stock Is Down 85% In 3 Days

Club of World’s 10 Richest People Finally Gets A Member from Asia

Michael Batnick: An Army of Day Traders

Roger Nusbaum: Health Insurance Dysfunction

Jeff Miller: Weighing the Week Ahead: Understanding a Mixed Message

Ben Carlson: How Rare is a Double Dip Recession? & The Air Conditioning Effect

Howard Lindzon: Shopify, Spotify and Now Snapchat? What Is With The S’s…?

Joshua Brown: Revamping the Podcast & “Inequality Is The Defining Feature Of Our Economy Today”

Be sure to follow me on Twitter.

-

Bloomberg on Trex

Eddy Elfenbein, June 19th, 2020 at 4:13 pmA nice profile from Bloomberg:

Last month, Trex Co. enticed homeowners cooped up during the pandemic with the siren song of sunshine and al fresco dining.

“Does staying inside have you yearning for the outside?” the maker of wood-plastic composite decking asked restless recluses in a Facebook post. “Us, too.”

The bait of fresh air appears to be working. Requests for product samples and designs picked up considerably since an April lull, Chief Executive Officer Bryan Fairbanks said. Like RH, the company is expected by analysts to be a beneficiary of the pandemic-fueled home improvement craze as residents remodel, a sector that accounts for the majority of demand for Trex.

“The outdoor living theme is resonating with consumers,” Jefferies analyst Philip Ng said in an interview.

Shares of Trex, which sells products crafted from 50% recycled polyethylene and 50% reclaimed wood, hit a record $128 in late May, more than doubling from a March low. So far this year, the stock has gained about 33%.

Trex’s product appeals to homeowners tired of sanding, staining and stepping on the occasional splinter. The company manufactures composite decking and railing sold at retailers including Lowe’s Cos. and Home Depot Inc. as well as lumberyards. The Winchester, Virginia-based company also has a commercial segment, but it’s the residential business that drives sales, contributing the most to revenue last year.

Fairbanks, 51, took the helm in late April after working at Trex for more than 15 years, most recently as financial chief. He’s CEO at a pivotal point, as homeowners have had downtime to ponder how to beautify their backyards and as the company adds capacity to plants in Nevada and Virginia.

Demand for home remodeling and repair is improving by the day, said Benchmark analyst Reuben Garner, who pumped up his price target to a Street-high matching $136 this week. Meanwhile, Google searches for “Trex decking” are at all-time highs, he added.

“We believe that this is evidence consumers are increasingly looking to make investments in their homes,” he said Thursday in an email. “Trex is the most recognizable consumer brand in the composite decking space, and the product is more ‘DIY’ in nature than I think most investors may realize.”

Trex aims to capture a larger slice of the decking and railing market. The company estimates that as of 2019, composites like those made by Trex only account for about 20% by volume. For Trex, that means the lion’s share of the decking and railing market is ripe for conversion. Their strategy: go after wood.

This market opportunity is “the biggest part of the story,” Berenberg analyst Alex Maroccia said in an interview.

Last year, Trex launched its re-engineered Enhance Basics and Naturals collection, the company’s most affordable offering. Jefferies’ Ng said that’s a big positive as the lower maintenance and more durable nature of composites was already a draw, but the price was a sticking point.

Trex is the largest player in composite decking by market share. The company competes with Azek Co. and Fiberon, which is owned by Fortune Brands Home & Security Inc. Azek, the second-largest player in the industry, made its public debut last week.

Some differentiating factors between Trex and Azek include margins and debt, according to Berenberg’s Maroccia. Azek’s TimberTech decks use less recycled content than Trex’s products, and that lower proportion results in more expensive raw materials, the analyst wrote in a recent note. Azek, whose top holder is PE firm Ares Management, is also more highly leveraged than Trex, he said.

“I think they view them as a competitor, but not a true threat for the foreseeable future,” Maroccia said in an interview, referring to Trex’s perception of Azek.

While Maroccia has a buy rating, the majority of analysts tracked by Bloomberg rate Trex at hold, including Ng at Jefferies. For him, the company’s valuation is a roadblock from turning more bullish. Trex warrants a bigger multiple, but it trades at “too large a premium” to its repair and remodel peers, Ng said in a recent note.

Other investors hold a downright bearish wager on Trex’s long-term outlook. In April, famed “Big Short” investor Steve Eisman said in a CNBC interview that he was short the decking materials manufacturer. Short interest has come down from a peak at the end of April but now sits around 15% of float, according to data compiled by financial analytics firm S3 Partners.

Trex is in the midst of a $200 million capital expenditure program that is set to increase capacity by about 70%. The ramp up of additional lines to the Nevada facility will be completed by the end of the second quarter, management said in May. Meanwhile, the construction of a building for the Virginia facility is on schedule.

Trex is moving full speed ahead, but the potential impact of a resurgence in Covid-19 remains a question mark, as cases in some states continue to climb.

Berenberg’s Maroccia said a second wave of coronavirus could pull forward demand for Trex’s products, with homeowners throwing in the towel on travel. However, Ng at Jefferies said it could hurt Trex alongside the broader market, even though the company’s business has shown it’s more resilient.

“We’re not going to try to convince you that they’re recession-proof or second wave-proof,” Ng said.

-

Barron’s on Ross Stores and Church & Dwight

Eddy Elfenbein, June 19th, 2020 at 10:57 amBarron’s featured two of our Buy List stocks today. Here’s the first in an article about discount retailers and Ross Stores (ROST):

Before the pandemic, one knock against off-price retail stores was they didn’t have much of a digital presence, because shifting inventory and low prices made e-commerce less economical for the group. Then the stars aligned to put this theory to the test, as coronavirus pushed all retailers online. Yet the discounters appear stronger than ever.

In a time of economic uncertainty, consumers are more focused on value than ever, and that’s been great for off-price retailers like TJX Cos. (ticker: TJX), Ross Stores (ROST), and Burlington Stores (BURL).

While these stores weren’t essential, and thus had to close when lockdown measures were in place in many areas, Covid-19 doesn’t appear to have dented their mojo. As Placer.ai notes, these retailers were seeing robust traffic going into the crisis, and the plunge in discretionary spending in March means that discounters have their pick of merchandise from full-line rivals.

Barrons also discussed the upgrade Credit Suisse gave to Church & Dwight (CHD).

Church & Dwight stock is rising on Thursday, helped by an upgrade from Credit Suisse, which argues that the maker of household and personal products can shine during uncertain economic times, thanks to its value-oriented brands and strong cash position.

Analyst Kaumil Gajrawala boosted his rating on Church & Dwight (ticker: CHD) to Outperform from Neutral, with an $85 price target. He writes that the company’s “operating model is designed to thrive in this environment: a value-oriented portfolio with a clean balance sheet and favorable M&A prospects meets a history of stability through difficult periods.”

He writes that while the stock’s valuation may look high—Church & Dwight has rallied nearly 10% in 2020—investors would do well to remember that the company has the highest return on capital and asset efficiency in the sector, which deserves a premium. Moreover, the stock’s valuation, at around 27 times forward earnings, is at a decade low versus the S&P 500.

Gajrawala highlights the fact that some 37% of the company’s portfolio comes from value-priced brands, a higher proportion than peers. He said Church & Dwight has “driven most of its growth through volume rather than pricing, which should serve it well through an economic downturn.”

The company is a serial acquirer, so declines in valuations among potential targets create opportunities for it. And it has a strong balance sheet, making it capable of doing deals.

-

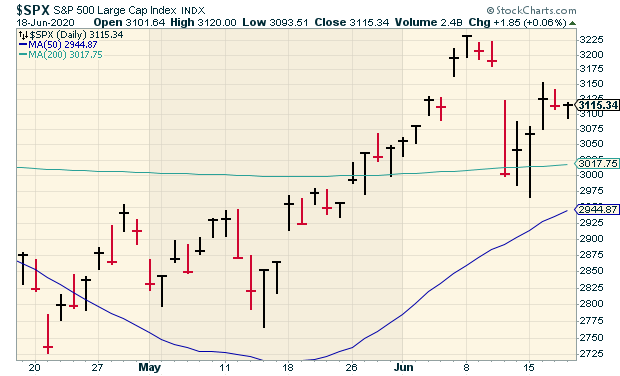

CWS Market Review – June 19, 2020

Eddy Elfenbein, June 19th, 2020 at 7:08 am“The expectation of an event creates a much deeper impression on the exchange than the event itself.” – Jose de la Vega, 1688

After last Thursday’s unpleasantness, when the S&P 500 plunged nearly 6%, the stock market has been much more relaxed this week. At one point on Monday, the S&P 500 was down 2.5% during the day. Yet by the closing bell, the index had eked out a small gain. That was only the third time in the last ten years that a 2.5% drop wound up being a day in the black.

So the bulls haven’t all been scared off. In this week’s issue, I want to cover some of the recent economic data, which hasn’t been good; it just hasn’t been quite as terrible as previous data. I’ll also preview next week’s earnings report from FactSet. The stock is having a good year for us. I also have some updated Buy Below prices for you. But first, let’s review some recent economic data.

Where the Economy Can Improve, It’s Improving

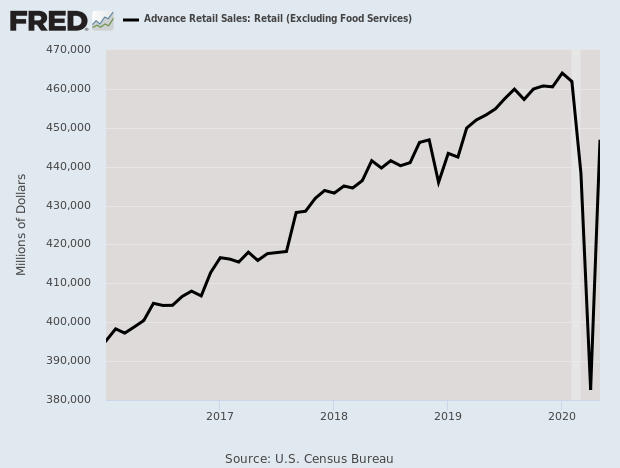

On Tuesday, the Census Bureau said that retail sales rose an amazing 17.7% last month. It’s not often you see a retail-sales report beat Wall Street’s consensus by 10%. Last month’s result was the best on record, by far.

Get used to seeing a lot of that. We saw lots of economic data recently that was among the worst on record. Now that some sectors have reopened, it’s only natural that we’re seeing a pronounced snap back.

So is the economy back on track? Not exactly. While the retail-sales report is good news, the government’s stimulus checks clearly played a role. We still have a long way to go till the economy is fully back on its feet. Much of that will be due to the course the coronavirus ends up taking. Gradually, more companies are getting back to normal.

Here’s the retail-sales chart. Sometimes the chart really does tell the story.

Disney World looks to start reopening on July 11. Disney World Hong Kong just reopened, and Shanghai Disneyland opened up in May. Speaking of Disney World, the NBA looks to finish off its regular season starting in late July. All games will be played at the ESPN Wide World of Sports Complex in Disney World.

Also on Tuesday, we learned that industrial production rose by 1.4% in May. Some factories are coming back online, albeit only partially. The economy is a long way from full capacity. Industrial production is still 15.4% below where it was in February.

In last week’s issue, I mentioned that the recession-dating committee officially declared that the recession had started. There’s a good chance that this could be one of the quickest recessions on record. There was a brief recession in 1980 that only lasted six months. We could see something like that. The difference is that this recession is much steeper.

This week, we learned that homebuilder confidence rose sharply in June. That’s a good sign. On Wednesday, the Commerce Department said that housing starts rose 4.3% in May. This was the first increase since January. Housing starts are still bad, but the increase is off the lowest reading in five years. This aligns with the previous report which tells us that the economy is in rough shape, but where it’s allowed to improve, it’s improving.

On Thursday, the jobless-claims report fell to 1.508 million. It’s odd to say that’s a good number, but it’s the tenth-straight improvement in a row. Continuing claims decreased slightly, from 20.606 million to 20.544 million.

Finding a Competitive Advantage

Since this is a fairly short issue, I wanted to talk a little more about proper stock selection and how to find superior investments. I’m often asked about this, and it’s an interesting but complex topic.

I’ll try to keep it simple. My basic plan is to find companies with a distinct competitive advantage. Here’s a good way to think about this (I’m heavily borrowing from our friends at Investopedia for this example).

Let’s say you have a lemonade stand and business is going well. You suddenly have an idea. Normally, your stand buys lemons each morning. Instead of doing that, you decide to buy a bunch of lemons at the beginning of the week. Your supplier gives you a bulk discount.

Let’s say, this cuts your cost of goods sold by 20%. In terms of economics, this is a huge deal. This means you can cut your prices by 20%, thereby gaining market share, and it will have zero impact on your gross profit margins. This is great news for you and your business.

As much as we love this, there’s one small problem. While it’s a great idea, it’s just an idea—and one that can be easily copied by your competitors. Once they discover the secret, your advantage is gone.

Now let’s say you come up with a second idea. You invent a revolutionary new lemon squeezer that’s so good, you get 20% more juice out of each lemon. Once again, this is a huge deal in terms of business economics. You’re effectively cutting your costs of goods sold by 20%, and again, you can pass those savings on to your customers with no impact on your gross margins.

But there’s a crucial difference between the first example and the second. In the second case, you can patent your lemon squeezer. That means you can line up state power to enforce your invention monopoly. The idea in the first example isn’t protected the same way.

The second example shows the kind of company I look for. I look for firms that do things that no one else can do. Several stocks on our Buy List have strong competitive advantages. In particular, I think of companies like Moody’s (MOC) or Fiserv (FISV).

With that said, how do you know if a company has a strong competitive advantage? There are a few characteristics that typically show up.

Oftentimes, the company we’re looking at has a consistent operating history. Sales and earnings edge higher nearly every year. There may be bad years, but the positive trend is clear.

This tells me a few things about the business. First and most obviously, it’s a growing enterprise with a steady demand for its products. It also tells me that management is probably on the ball. That’s because in a dynamic marketplace, you need to make a lot of small corrections to keep the ship moving.

A company with a consistent operating history also probably has a loyal customer base. Never overthink a business. You can make a lot of money selling the same thing to the same people. Ask Starbucks (SBUX).

Lastly, investing in companies with a consistent track record is an easy way of reducing risk. I’m not a fan of “oil well” stocks. These are companies that appear flat broke but are pinning all their hopes on some deal that may never come. There are too many of these stocks around. When in doubt, I always prefer a stock that grows its business each year.

A company should also have the ability to raise prices. This is a subtle rule, so let me explain what I mean.

You’ll notice that I didn’t say I look for companies that do raise their prices. Rather, the key is finding ones that, if the need arises, can raise their prices.

Think about the items in your home or office. Now imagine which ones you would still buy even if they raised their price by 10% or 15%. Some items you’d simply stop buying. But not all.

Why? Maybe you’re attached to it. Or maybe it’s an integral part of your day. I have friends who would make their daily Starbucks run no matter what.

Also, a company that has the ability to raise its prices most likely has a firm handle on its costs. That way, it can pass savings along to its customers, which builds customer loyalty

There’s a risk component as well. No company wants to raise prices, but it’s nice to be in a position where they can do so if need be.

Ability to raise prices is often a sign that a company has a dominant position in its market. I often think of Harley-Davidson (HOG), the legendary hog stock and former Buy List member.

I also like to see a company that is the dominant player in a niche market. A company doesn’t have to own the world to be successful. Owning the best autobody shop in town, or the best Thai restaurant in town, can be a great business.

Why? Because the firm is doing something no else can do. In business, there’s a term called “switching costs.” This refers to the cost for a consumer to change his or her preference. With toothpaste, folks aren’t so picky. With eating habits, people can be very picky.

For a business, you want to be the dominant player, even if it’s in a very narrowly-defined market. Think of the ratings agencies. If you want to float a bond, you pretty much have to deal with Moody’s or S&P.

Warren Buffett often tells the story that the perfect business to own is an unregulated toll road. The fixed costs are low, and drivers need to use it.

On our Buy List, we have Broadridge Financial Solutions (BR). This is the dominant player in share-voting proxies. This is the kind of business not one person in 20 ever thinks about, but it fills a concrete need.

You can spot a dominant player because it often has modest debt levels, wide operating margins and strong cash flow.

I hope that gives you a better idea of what I look for when selecting our Buy List stocks. I’ll have more details in upcoming issues. Now let’s look at next week’s earnings report.

FactSet Earnings Preview

FactSet (FDS) is due to report its earnings on Thursday, June 25, before the stock market opens. This will be for FactSet’s fiscal Q3 earnings, which ended on May 31.

I like this company a lot, and it’s one of the stocks that has a strong “moat,” meaning a strong position in its market. Three months ago, FactSet reported solid results from its fiscal Q2. The company earned $2.55 per share which beat consensus by six cents per share. Quarterly revenue rose 4.2% to $369.8 million. This was for the quarter that ended on February 29, so coronavirus didn’t have a noticeable impact on its operations.

For FactSet, the key stat to watch is Annual Subscription Value, or ASV. For Q2, that stood at $1.44 billion. ASV is growing at more than 4%. At the end of Q2, FactSet’s client count reached 5,699, and the user count is up to 128,896. Annual ASV retention is over 95%.

At the time of the Q2 report, FactSet stood by its full-year earnings estimate of $9.85 per share to $10.15 per share. Like nearly everybody else, FDS rallied nicely off its low, although the stock recently pulled back over 10% in four trading days.

Wall Street currently expects Q3 earnings of $2.43 per share. That sounds about right.

Updated Buy Below Prices

Before I go, I want to update a few of our Buy Below prices.

Ansys (ANSS), a new stock for us this year, has been doing well lately. The May earnings report was quite good. This week, I’m raising our Buy Below on Ansys to $300 per share.

Church & Dwight (CHD) has rallied for the last four days in a row. It’s now up 10.6% this year. The shares just hit a nine-month high on Thursday. I’m raising my Buy Below on CHD to $80 per share.

Danaher (DHR) has also been acting well lately. The stock hit another new high this week. It’s now a 14.7% winner for us this year. I’m lifting our Buy Below to $185 per share.

That’s all for now. Next week, we’ll get the existing-home sales report on Monday and the new-home sales report on Tuesday. Thursday morning will be busy, as the jobless claims report is due out. At the same time, the Q1 GDP revision comes out. This will be the second revision to Q1 GDP growth. As if that weren’t enough, we’ll also get the report on durable goods at the same time. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His