Whither the P/E?

Why is the P/E Ratio so darned high? That’s a question that’s bedeviled analysts for many years, not just now.

As a stock-picker, I generally avoid such arguments. The stock market doesn’t need to “make sense.” The market gods have their reasons for doing whatever it is they do, even if it’s not entirely clear to us mortals. The judgments of the markets are true and righteous altogether.

The market’s sanity has especially been called into question lately because the market has done well even though the economy has not. The disconnect between Wall Street and Main Street has become a popular talking point.

As I’ve noted before, this disconnect should not alarm anyone. The stock market and economy have little reason to be strongly linked in the near term. We’ve experienced many such disconnects. One popular idea is that President Trump and, of course, “his cronies” are propping up the market for the election. I’m curious where this cabal was during February and March.

In any event, Alan Reynolds, a senior fellow at the Cato Institute, is the latest to take on this question. I should add that since Dow 36,000, conservative pundits have not had a particularly stellar track record in discussing market valuations. (By the way, here’s a brilliant critique of Dow 36,000 written by, as it turns out, me.)

Reynolds writes:

The argument for stocks being greatly “overvalued” rests on the fact that the trailing P/E ratio rose significantly from May 1 to September 1. On January 1, the P/E ratio was 24.21 –about the same as two years before (24.87). Even after Covid-19 and lockdowns crushed the economy, the P/E ratio was still 23.74 on April 1. Stock prices and earnings had both collapsed in sync. The P/E ratio was 25.10 on May 1 after the Fed funds rate fell to nil and the $1,200 checks and PPP loans peaked. It then rose to 26.69 on June 1, 27.57 on July 1, 28.31 on August 1 and 30.32 on September 1.

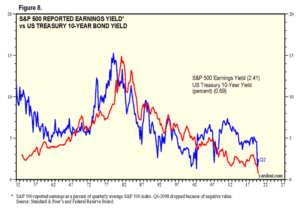

First, Reynolds points out that the inverse of the P/E Ratio, earnings over price, should generally follow bond yields. As bond yields have plunged, valuation should rise. Since the days of Alan Greenspan, this has often been called the Fed Model, though Reynolds believes he may have originally influenced the Maestro. They worked together on Reagan’s transition team.

Here’s a chart from Reynolds’s post:

Yes, they certainly do seem to match up. Reynolds also notes that the P/E Ratio falls when inflation rises. Therefore, he claims that Jerome Powell’s Jackson Hole speech, which outlined the Fed’s greater tolerance for inflation, could have been a negative for share prices.

While Reynolds says the lower bond yields justify the higher equity valuations, he says the Federal Reserve deserves zero credit since they were a laggard on lowering short-term rates.

The Federal Reserve can certainly crash the market (e.g., the double-dip recessions of 1980-82), but milder forms of Fed activism rarely explain bond yields or stock prices. The 10-year bond yield has at times risen 3.5 to 4 percentage points above the Fed funds rate, as in 1992, 2001-04 and 2010. Also, the S&P 500 stock index hovered at or below 2000 the last time the Fed kept the funds rate near zero in 2014-15, then rose 46% by July 2019 even as the Fed raised the funds target ten times to 2.5%.

Reynolds then gets to the key point that trailing P/E Ratios are higher but forward ratios may not be. We still don’t know.

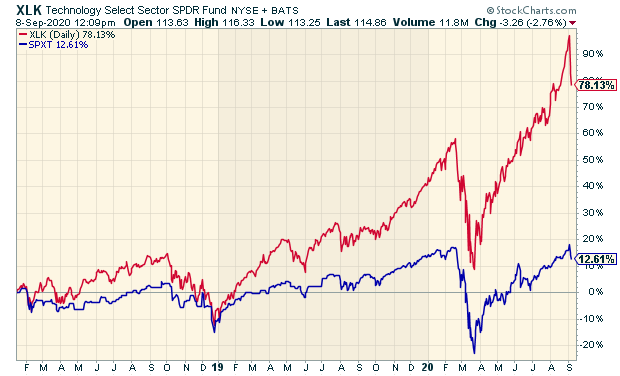

I believe Reynolds errs on two key points. One oversight is noting which stocks are rising. There’s a tendency to treat the S&P 500 as if it’s one giant stock. It’s not. The Big Outside of a small group of tech stocks, the stock rally hasn’t been particularly impressive.

Here’s the S&P 500 Tech Index (red) along with the S&P 500 except tech (in blue).

The other point is dividends which are a key component of stock returns. On this point, short-term rates from the Fed have an impact though it’s a limited effect.

Posted by Eddy Elfenbein on September 8th, 2020 at 11:54 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His