CWS Market Review – December 4, 2020

“There’s no shame in losing money on a stock. Everybody does it. What is shameful is to hold on to a stock, or worse, to buy more of it when the fundamentals are deteriorating.” – Peter Lynch

Before I get to today’s newsletter, I have a quick announcement. I’ll be unveiling next year’s Buy List three weeks from today, on December 25. The market is closed that day, but I’ll send you an email with the new portfolio. As usual, five stocks go in and five stocks go out, and twenty stocks will remain the same. This will be our 16th annual Buy List.

I announce the portfolio changes a bit early so that no one can claim I’m somehow rigging the track record. The new Buy List will go into effect on the first day of trading in the new year, which will be Monday, January 4, 2021. The 25 positions will be equally weighted based on the closing price on December 31. On January 1, I’ll send you another email with all the portfolio stats and a summary of our performance in 2020.

Now, onto this week’s newsletter.

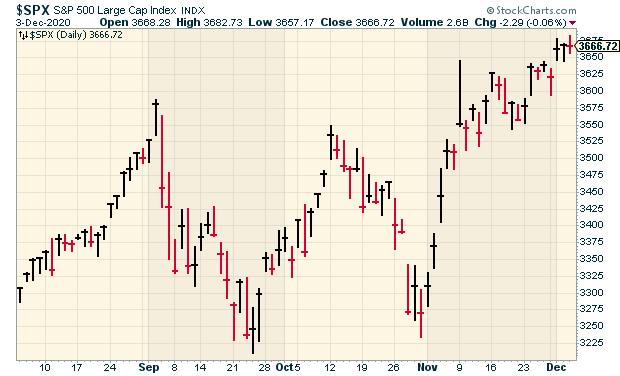

The Best November for the S&P 500 Ever

The stock market has been in the holiday spirit lately. The S&P 500 just came off its best November on record. The rally continued into December as the S&P 500 closed at an all-time high on Wednesday. Since the March 23 low, the S&P 500 has rallied more than 63%. I wonder how many people expected that eight months ago! I’m pleased to say that our 2020 Buy List has also enjoyed recent gains.

What’s the reason for the rally? That’s hard to say precisely, but my guess is that it’s two things. First, the positive news about a Covid vaccine. The FDA is currently reviewing two vaccine candidates for approval. If everything goes well, the next step will be rolling them out as quickly as possible. This is a difficult time as new coronavirus cases have soared across the U.S. Many states seem to be moving back to lockdown procedures.

The other reason for the market’s optimism is that Congress seems to be coming together to support a stimulus deal. Before the election, no one was interested in striking a deal. Now that the election has passed, the mood is quite different.

This week, a group of bipartisan legislators came together to support a $908 billion stimulus package. That probably won’t become law, but it may serve as a starting point for future negotiations. It seems very likely that some sort of deal will ultimately be reached before the end of the year. The details still haven’t been worked out, but the important point is that everybody wants a deal to be done before the end of the year. It’s in no one’s interest to let this drag on.

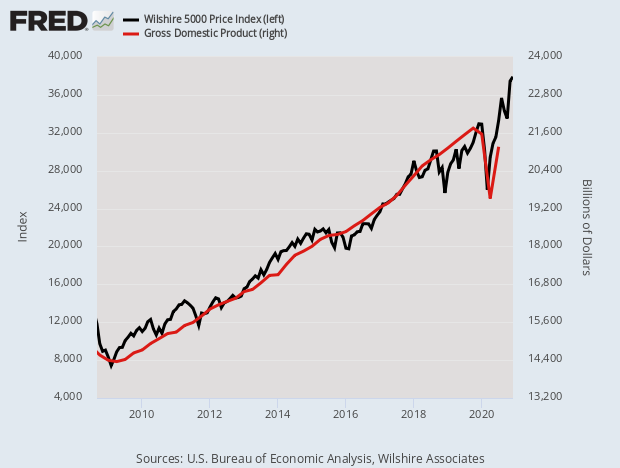

It’s true, the stock market isn’t the economy. But they are related. Here’s a long-term look at share prices and GDP:

The November jobs report is due out later this morning. The consensus on Wall Street is for a net gain of 500,000 jobs and for the jobless rate to fall to 6.7%. I haven’t seen the results yet, but there’s been some sogginess in the recent economic data. One exception was this week’s initial jobless claims report, which showed another pandemic low.

Most economists expect GDP growth for Q4 of around 4%. However, one outlier is the Atlanta Fed’s GDPNow, which sees Q4 GDP growth of 11.1%. That’s very good, and it’s well above expectations. What helped increase their forecast was this week’s ISM Manufacturing report, which came in at 57.5.

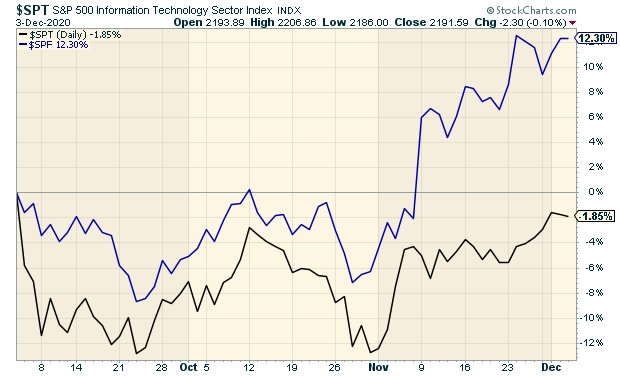

We’re continuing to see the trend I’ve talked about in recent issues. Value stocks are outpacing growth stocks. That’s not always the case in a rising market. The big drivers of value’s lead in recent weeks has been the performance of financial stocks and energy stocks. Of course, it’s not so much that these stocks are doing well. Rather, they’re bouncing back after terrible performances. Still, that counts.

Here’s a look at the performance of finance stocks (in blue) and tech stocks (in black):

This trend is still going strong. It also suggests that the Atlanta Fed may be right and that the outlook for the economy is improving. This has caused a seeming contradiction. At one end, coronavirus cases and hospitalizations are rising. Some healthcare systems may even be overwhelmed. At the same time, some vaccines may soon be ready, and that could mean life may get back to something like normal in 2021.

Hormel Misses by a Penny per Share

On November 24, Hormel Foods (HRL) reported earnings for its fiscal Q4, and the results were on the weak side. Hormel made 43 cents per share for the quarter, which was one penny per share below the Street’s forecast. This was for the three months ending October 25.

Wall Street wasn’t pleased, and frankly, neither was I. The shares dropped over 5% that day, and they had been falling going into the report.

Let’s look at some details:

• Volume of 1.2 billion lbs., down 2%; organic volume down 3%

• Net sales of $2.4 billion, down 3%; organic net sales down 4%

• Operating margin of 11.4%, compared to 12.8% last year

• Effective tax rate of 15.9%, compared to 21.0% last year

• Diluted earnings per share of $0.43, down 9% from $0.47

Those are some soggy numbers across the board. Here’s how the quarter broke down by Hormel’s different business units:

Refrigerated Foods

Volume down 4%; organic volume down 5%

Net sales down 5%; organic net sales down 7%

Segment profit down 17%

Grocery Products

Volume up 1%

Net sales down 1%

Segment profit up 1%

Jennie-O Turkey Store

Volume down 2%

Net sales down 6%

Segment profit down 21%

International & Other

Volume down 1%

Net sales up 8%

Segment profit up 55%

Not that great. Obviously, doing business in the world of the coronavirus is difficult. One silver lining is that business in China picked up a bit.

The balance sheet is still pretty clean, and Hormel has $1.7 billion in cash. For the year, Hormel made $1.66 per share. That’s down from $1.74 per share last year. I’ve not been pleased with Hormel’s performance this year.

Here’s an interesting chart. This is shares of Hormel divided by the S&P 500 ETF (SPY). You can see that HRL crushed the market during the panic in February and March. That’s exactly what defensive stocks are supposed to do. Since then, HRL has lagged, and the gap has only grown wider recently. This is the other side of the coin of cyclical stocks leading. Defensive stocks are lagging.

Buy List Updates

There’s been a lot of news impacting our stocks recently.

First, I have to comment on shares of Disney (DIS) making a new 52-week high. That’s astounding. The company has really suffered under the pandemic. The parks business has been squeezed. No one’s going to the movies. The cruise industry is in the docks, and pro sports is having a rough time.

Despite it all, the Mouse House continues to rally. Every day the company becomes more of a streaming business with a side business of amusement parks. I would guess that the pandemic caused Disney to do five years of evolution in less than one. I’m lifting our Buy Below on Disney to $160 per share.

I saw that Hershey (HSY) recently altered its famous Jingle Bells ad with Hershey Kisses. Apparently, this has outraged Hershey fans! As you might guess, they took to the Internet to express their displeasure. Some practically blamed the chocolatier for ruining Christmas. Mind you, Hershey merely altered the ad. Fortunately, Hershey finally caved and said it will run the classic version of the ad.

A lot of this is harmless fun, but there is a serious business point underneath it. It’s that we see a company that has very strong brand loyalty. The customers know and love the product, and they feel a sense of ownership. That’s very important. These facts don’t show up on a balance sheet, but they’re real.

We also had three of our Buy List stocks recently raise their dividends. They all extended long streaks of continuous dividend hikes.

Let’s start with Stryker (SYK). The company just bumped up its quarterly dividend from 57.5 cents to 63 cents per share. That’s an increase of 9.6%. This is Stryker’s 28th annual dividend increase.

Stryker’s last earnings report blew the doors off. For Q3, the orthopedics company earned $2.14 per share. That was up 12% over last year. Wall Street had been expecting earnings of $1.41 per share. I’m raising our Buy Below on Stryker to $240 per share.

Becton, Dickinson (BDX) raised its quarterly dividend from 79 to 83 cents per share. That’s an increase of 5.1%. This is their 49th annual dividend increase in a row.

The new dividend will be payable on December 31 to holders of record on December 10. The indicated annual dividend rate for next year is $3.32 per share.

Earlier I mentioned the earnings report from Hormel Foods (HRL). The company also raised its quarterly dividend from 23.25 cents to 24.5 cents per share. This is the 55th annual dividend increase in a row. Not bad for Spam!

The dividend will be paid on February 16 to stockholders of record at the close of business on January 11. Since becoming a public company in 1928, Hormel has paid a regular quarterly dividend without interruption.

Lastly, FactSet (FDS) said it will release its fiscal Q1 results on Monday, December 21. Wall Street expects earnings of $2.75 per share.

That’s all for now. The November jobs report is due out later today. For October, the jobless rate fell to 6.9%. There’s not much in the way of economic reports next week. On Tuesday, productivity growth for Q3 will be updated. The job-openings report comes out on Wednesday. On Thursday, the CPI report is due out along with the initial-jobless-claims report. So far, inflation has been relatively tame. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on December 4th, 2020 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Tweets by @EddyElfenbein

-

-

Archives

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His