CWS Market Review – March 26, 2021

“The great fortunes in stocks have not usually been made by people who give stop orders.” – Charles Dow

The stock market ran into some minor turbulence this week. The S&P 500 fell four times in five days before an impressive rebound and reversal on Thursday. Once again, the index’s 50-day moving average proved to be the key support level. This isn’t the first time. Over the last two months, the S&P 500 has dipped below its 50-DMA a few times, but not for long. Each time, stocks have rallied back.

I fear that investors are becoming overly reliant on minor drops quickly reversing themselves. On Wall Street, easy patterns work right until the moment they stop. The stock market has rallied fairly consistently over the last five months. We may be due for a dust up soon. I’m not predicting anything scary, but I am urging caution and patience.

Honestly, this is a fairly quiet time for Wall Street. The Fed just had its meeting, and the Q1 earnings season is still a few weeks away. Volatility is low, and the VIX is back below 20. This week, Federal Reserve Chairman Jay Powell and Treasury Secretary Janet Yellen testified on Capitol Hill about the economy. Both reiterated the position we’ve been making for a few weeks, which is that the economy is doing pretty well, and the higher bond yields are a reflection of that.

In this week’s issue I want to cover some of the recent economic news. It’s been a bit soggy, but nothing to worry about. I also want to preview what to expect when Q1 earnings season starts. Wall Street has a lot riding on this. I’ll also preview FactSet’s earnings report, which is due out on Tuesday. I also have some Buy List updates for you. But first, let’s take a closer look at some recent economic news.

February Was Tough, but the Economy Is Getting Better

On Thursday, the government said that jobless claims fell to 684,000. It’s odd saying that’s good news, but in the Age of the Coronavirus, that’s good news. That’s a post-pandemic low, yet it’s still higher than the highest claims number from 12 years ago. Context is everything.

This week, we got reports on new- and existing-home sales. Both reports were fairly weak, but harsh February weather probably held back those numbers. Overall, the housing market remains fairly strong. In fact, housing inventory is at very low levels. The CEO at Redfin said that lack of inventory was like a Soviet-era supermarket. Housing inventory usually runs around six months’ supply. Now it’s close to one or two months. This is happening in housing markets all across the country.

The durable-goods report was also below expectations. During the initial lockdown, the durable-goods numbers took a big hit, but they had been improving since then. That is, until February. Expectations were for an increase of 0.4%. Instead, durable goods declined by 1.1%.

Economists also like to look at “core” durable goods, which excludes aircraft. Core durable goods fell 0.8% last month. Again, weather was clearly a factor. But I think it points at the broader view that while the economy is improving, it’s not happening at an even pace.

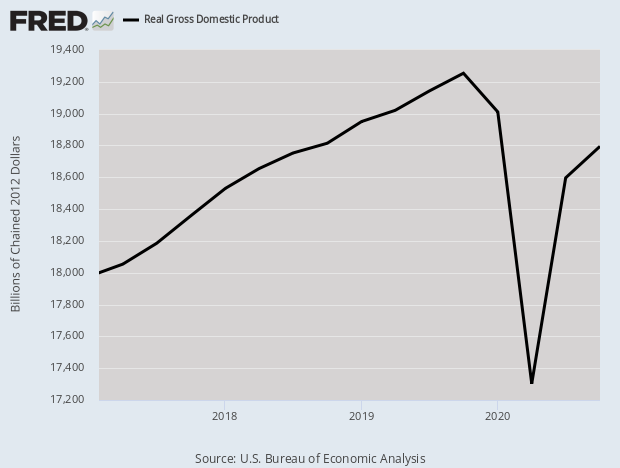

On Thursday, the government revised the Q4 GDP growth report up to 4.3%. That’s an annualized number, and it’s adjusted for inflation. The previous estimate was for growth of 4.1%. The economy is going through something like a V-shaped recovery, but we’re still well below the level we reached one year ago. Financial markets have improved, and that’s good for us, but for a lasting recovery, we need to see improvements in the real economy.

As I’ve said before, Covid news is now economic news. As soon as the economy can fully reopen, we will see much broader improvement. You can’t install drywall over Zoom.

In a few weeks we’ll get our first look at the Q1 GDP, and it could be very strong. Goldman Sachs is expecting growth of 8%. There’s talk of 10% growth. Even the Fed is optimistic, and they hate everything. Now let’s look at some numbers for Q1 earnings season.

Looking at the Numbers for Q1 Earnings Season

The Q1 earnings season will start in early- to mid-April. This is a crucial time for Wall Street. The economy has improved, and investors will want to see improved profits as well.

This is also important because Wall Street has gambled that things are getting better and will continue to get better. Right now, you may see a lot of scare items in the news media about how expensive the overall market is. Well, those valuation ratios are correct, but they’re missing the point in how unusual the current market is.

Investors are looking past the dismal numbers we’ve had. That’s why we have skyward valuations. Stock prices are forward-looking and earnings are backward looking. With such a gap between today and tomorrow, of course the valuation metrics look scary.

Actually, the Q4 earnings season was pretty good. In the S&P 500, 384 stocks beat guidance, 18 met expectations and 98 missed estimates. (No, it doesn’t add up to 500.) Regarding sales, 368 of 498 stocks beat on sales.

For Q4, the S&P 500 made $38.18 per share. That’s the index-adjusted figure. Before the pandemic hit, analysts had been expecting something close to $50 per share. Then everyone got scared. At one point, expectations fell all the way to $35 per share.

For Q1, Wall Street expects the S&P 500 to earn $38.99 per share. That’s almost exactly double last year’s Q1. If you recall, it was really the second half of Q1 (or the second eighth, if you prefer) that was impacted by the lockdowns.

The analyst community currently expects the S&P 500 to have full-year earnings of $172.43 per share. Going by today’s level, that means the S&P 500 is trading at 22.67 times this year’s expected earnings. That’s high, but it also needs to be put in context. The earnings yield (the inverse of the P/E Ratio) is 4.41%. That compares pretty favorably with the 10-year yield at 1.61%.

Going out even further, Wall Street analysts expect 2022 earnings of $200 per share. I’m leery of forecasts going out that far. Still, if a robust recovery is coming our way, I don’t believe equity prices are unreasonably high.

FactSet Earnings Preview

FactSet (FDS) is due to report its fiscal Q2 earnings report on Tuesday, March 30. The stock hasn’t done particularly well over the last several months. Shares of FDS reached their peak of $363 in August. Since then, they’ve gradually drifted lower.

For Q1, FactSet earned $2.88 per share. That beat Wall Street’s estimate of $2.75 per share. That was an improvement of 11.6% over last year’s Q1.

I was impressed with the details. Adjusted operating margin improved 0.4% to 34.3%. The key stat for FactSet is Annual Subscription Value or ASV. For its fiscal Q1, ASV plus professional services rose 5% to $1.56 billion. The company’s user count increased by 5,187 to 138,238. Annual ASV retention was greater than 95%. When expressed as a percentage of clients, annual retention was 90%.

For this year, FactSet expects earnings to range between $10.75 and $11.15 per share. (Their fiscal year ends on August 31.) That’s probably too low. The company also sees revenue coming in between $1.57 billion and $1.585 billion. FactSet expects operating margin between 32% and 33%. That’s very good, and it’s one of the key reasons why I like this stock.

Unfortunately, the company didn’t provide quarterly guidance, but Wall Street expects Q2 earnings of $2.74 per share. That sounds about right to me. There’s a decent chance the company will raise its full-year guidance.

FactSet is not a cheap stock, but it’s cheaper than it was, and its business has improved. I’m a big fan of FactSet.

Buy List Updates

Here are some updates on a few of our Buy List stocks.

First off, I had a typo in last week’s issue. Thanks to the many readers who caught this. The correct Buy Below for Danaher (DHR) is $230 per share. My apologies for the error. The shares have firmed up some recently.

Shares of Moody’s (MCO) have also been improving lately. The stock came close to touching a six-month high. I expect another solid earnings report in a few weeks. This week, I’m raising our Buy Below on Moody’s to $320 per share.

Sherwin-Williams (SHW) is due to split next week. If you own SHW, you’ll get two more shares for each one you currently own. Unfortunately, the share price will drop by two-thirds. Our Buy Below price will fall to $250 per share. The split will take effect on April 1.

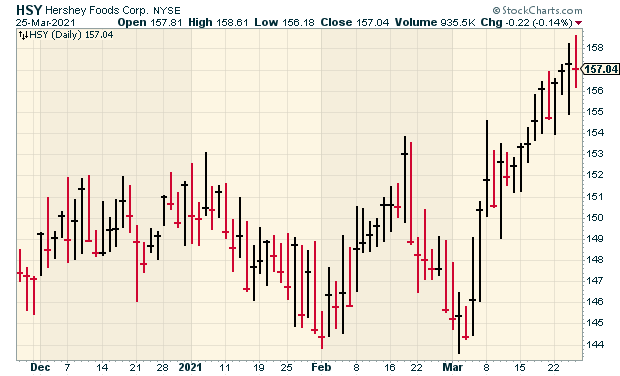

I don’t write about Hershey (HSY) as much as I should, but what is there to say? They have a simple business model that works. The stock has perked up in the last few weeks, and it’s close to a new all-time high. Hershey remains a buy up to $160 per share.

That’s all for now. The stock market will be closed next Friday, April 2 for Good Friday. This is a rare day when the market is closed and most government offices are open. Despite the holiday, Friday will be jobs day. That’s when we’ll get the unemployment rate and nonfarm payrolls for March. For February, the U.S. economy created 379,000 jobs and the unemployment rate fell to 6.2%. As usual, the ADP payroll report will be due out on Wednesday. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on March 26th, 2021 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His