Archive for March, 2021

-

CWS Market Review – March 19, 2021

Eddy Elfenbein, March 19th, 2021 at 7:08 am”Indicators of economic activity and employment have turned up recently.”

So said the Federal Reserve in this week’s policy statement. Actually, that’s a big deal for the Fed, to say publicly that things are getting better. You have to understand that central bankers are trained from birth to couch any statement in qualified, hesitant terms.

Fortunately for us, dear reader, your humble editor is well versed in the arcane language of Fedspeak. As such, I’ll translate this week’s Fed statement into plain English. The bottom line is that Chairman Powell tried to calm the markets, and it worked. On Wednesday, the Dow and S&P 500 both rallied to new all-time highs. The Nasdaq is still a few percentage points away due to Big Tech’s getting pinged last month.

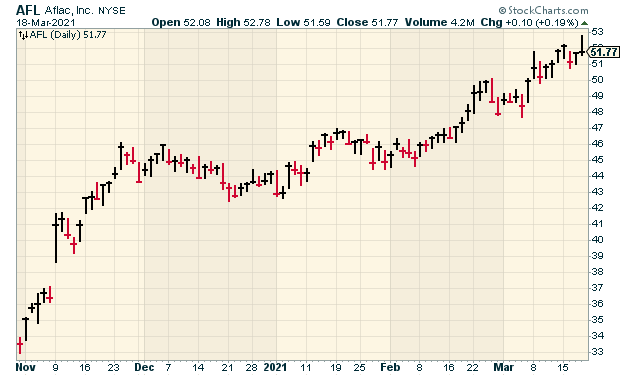

The bond market, however, is still a little nervous. The yield on the 10-year Treasury got as high as 1.75% on Thursday. I’ll explain what’s been going on. I also have some Buy List updates for you. Shares of AFLAC have been red-hot for the last few months. Higher bond yields are a big help for their business. Shares of Hershey have also perked up in the last few days. HSY has closed higher nine times in the last 11 sessions, and it just touched a new 52-week high. But before I get to all that, let’s look at what the folks at the Fed had to say this week.

The Fed Walks a Narrow Aisle

On Tuesday afternoon, the Federal Reserve released its latest policy statement. Along with it, the central bank also updated its economic projections for the next few years. I’ll warn you that the Fed has a pretty lousy track record predicting the economy, but still, it’s important to hear what it has to say.

In its policy statement, the Fed did acknowledge the improving economy. It also made it clear that it intends to keep interest rates low for a long time.

One of the less-discussed stories of the pandemic was the massive and early response by the Federal Reserve. Once the evidence became clear that the economy was going to take a massive hit, Fed Chairman Jerome Powell didn’t go in for any half measures. He immediately cut interest rates to 0%. In fact, he even effectively went below 0% by buying huge amounts of Treasury and mortgage bonds each month.

There’s no doubt that the Fed’s actions were more for Wall Street’s benefit than for Main Street’s. Still, the Fed’s response probably helped cushion the blow for a lot of rank-and-file workers.

Now we’ve come to a difficult position for the Fed. The economy is clearly improving, and COVID finally appears to be losing. In the newsletter from three weeks ago, I laid out the case for a rational optimism for the economy.

The Fed, however, had not yet acknowledged the improving economy. That’s why the line I put as this week’s epigraph was so important. According to the Fed’s December forecasts, it saw the economy growing by 4% this year. Several Wall Street investment houses now see much stronger growth. Goldman Sachs thinks the economy can grow by 8% this year.

This left Chairman Powell in a delicate position. He wanted to affirm that the economy is getting better while maintaining his commitment to low interest rates. Indeed, along with this week’s policy statement, the Fed also updated its economic projections. The Fed made it clear that it doesn’t see a need to raise interest rates this year, next year or even the year after that.

So the message from the Fed is, “yes, things are improving, but seriously chill out about interest rates.” With all the stimulus and vaccine news, Wall Street is still skeptical. The first policy to go could be the massive bond buying. In fact, that’s probably why interest rates on long-term Treasuries have climbed higher. In August, the 10-year Treasury got down to 0.5%. This week, it hit 1.75%.

This has had a big impact on the economy, most prominently with mortgage rates. In fact, mortgage-refinancing demand is down 39% in the past year. Personally, I think the bond market is very premature here.

There’s an old saying on Wall Street: “don’t fight the Fed.” That’s certainly true. Of course, they have a lot more money. This time, the Fed is on the side of investors. We should take the hint.

What’s happening is that everyone seems to be reacting to events that are expected to happen but that haven’t happened yet. For example, everyone thinks the economy will get better, but there are still millions of Americans out of work. The stimulus checks are expected to help, but they’re only now getting on their way. The bond market is reacting to inflation which simply hasn’t appeared yet. The stock market is rallying on earnings which aren’t here but that are expected to arrive shortly.

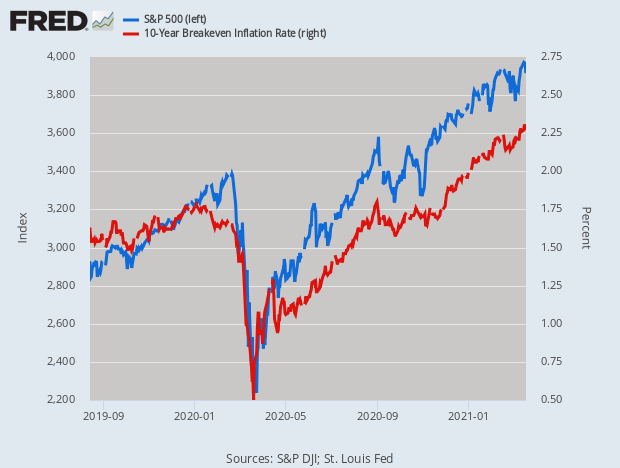

Here’s a fascinating graph that explains much of where the market is right now.

This shows the S&P 500 in blue along with the 10-year breakeven rate in blue. The two lines are nearly like waltzing partners. The breakeven rate is the market’s guess as to the inflation rate over the coming 10 years. What this shows is how closely aligned inflation expectations and the stock market are.

If the stock market is nothing more than earnings expectations, you could say that earnings expectations have become inflation expectations. It’s not me saying that. It’s the financial markets.

I used to talk often of the spread between the two- and ten-year Treasury yields. Whenever that goes negative, it’s often a precursor to a recession. This simple indicator has a very good track record. The spread turned negative in August 2019 and the recession was six months away. Now, however, the spread has grown very wide. That’s due to short-term rates staying where they are and longer rates going higher. Just this year, the 2/10 spread has nearly doubled from 80 basis points to 155 basis points.

The same formula for the market remains in place. Stocks over bonds. Cyclicals stocks over defensive stocks. Value over growth. Small-caps over large. This is a very good environment for our Buy List. Indeed, several of our stocks have touched new highs in recent days.

I expect the market to remain stable over the next few weeks. Things will heat up again as we get closer to Q1 earnings season in April. Now here’s a look at some recent news impacting our stocks.

Buy List Updates

AFLAC (AFL) had a solid earnings report last month. I probably should have raised the Buy Below then, but I’ve decided to do it this week.

One of the truths about investing in stocks is that their behavior can be highly erratic. My friend Louis Navellier described stocks as behaving like rabbits. They sit and sit and sit, and then they suddenly dash off. That’s pretty much what’s happened with AFLAC. The shares are up more than 52% in less than five months.

Last year, AFLAC made $4.96 per share. That’s up from $4.44 in 2019. AFLAC had a very tough year in 2020. Given what they had to deal with, the company performed admirably. The recent 18% dividend hike reflects that.

The higher bond yields are a benefit to an insurance company like AFLAC. This week, I’m lifting our Buy Below on AFLAC to $55 per share.

More good news for Disney (DIS). The company said that Disney World will reopen on April 30. More than 10,000 workers will go back on the job. That’s very encouraging news. Last week, Disney said that Disney+ now has 100 million subscribers. Not bad for 16 months. Disney remains a buy up to $200 per share.

Two weeks ago, I told you that Ross Stores (ROST) missed expectations and the stock took a hit. Well, it only took a few days for the stock to rally back to a new high. This is one of the great advantages of owning high-quality stocks. They’ll get knocked around, but they usually bounce back. The deep-discounter also reinstated its dividend, which they had canceled at the start of COVID. I’m raising our Buy Below on Ross to $130 per share.

FactSet (FDS) is due to report its earnings on March 30. This will be our only earnings report for a long stretch. We won’t see more earnings until mid-April when the Q1 earnings season starts. For the coming year (ending in August), FactSet sees earnings ranging between $10.75 and $11.15 per share. I’ll have a more detailed earnings preview in next week’s issue. FactSet is a buy up to $340 per share.

I love Danaher (DHR), but the stock’s been a little sluggish in recent weeks. At one point, the shares fell for eight days in a row. For all of 2021, the company expects revenue growth “in the low-double-digit range.” That’s pretty good. To reflect the recent weakness, this week I’m dropping our Buy Below on Danaher down to $230 per share.

Also remember that Sherwin-Williams (SHW) will soon be splitting 3-for-1. Shareholders will have three times as many shares, but the share price will drop by two thirds. Our $750 Buy Below price will split along with the stock and become $250 per share. The split will take effect on April 1.

That’s all for now. There are a few key economic reports due out next week, especially for the housing market. On Monday is the existing-home sales report, followed by the new-home sales report on Tuesday. The durable-goods orders report is due out on Wednesday. Then on Thursday, the Q4 GDP report will be updated for the second time. According to the last update, the U.S. economy grew by 4.1% in Q4. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: March 19, 2021

Eddy Elfenbein, March 19th, 2021 at 7:04 amBOJ Fine-Tunes Massive Stimulus in Long Drive to Boost Prices

Twenty Years On, EU Turns Cold on Mercosur Trade Deal

UK Set to Undershoot Towering COVID-19 Borrowing Forecast

Powell Determined to Fuel Growth Despite Inflation Fear

Powell Says Central Bank Digital Currency Must Coexist With Cash

‘The Market Seems Crazy’: Start-Ups Wrestle With Flood of Offers

House Flipping Is Suddenly a Hot Market for America’s Lenders

Education Department Scraps a Trump-Era Policy that Limited Debt Relief for Defrauded Students

Disney’s NFL Deal Is Victory for CEO Looking to Control Costs

Zuck Slowly Shrinks and Transforms Into a Corncob Ahead of Apple’s Looming Privacy Updates

Why U.S. Cruises Are Still Stuck in Port

Tired Goldman Sachs Underlings Beg to Work ‘Just’ 80 Hours a Week, Instead of 100

Behind the Back-Office Blunder That Cost Citigroup $500 Million

Michael Batnick: One Year Since the Bottom

Ben Carlson: Ray Dalio & The Power of Setting Defaults For Optimism

Be sure to follow me on Twitter.

-

The S&P 500 Closes in on 4,000

Eddy Elfenbein, March 18th, 2021 at 1:02 pmWe had five straight up days; now the stock market is looking at its second loss in the last three days. Still, the S&P 500 closed Wednesday at another all-time high. In fact, the index is getting close to 4,000.

For some context, the S&P 500 first closed above 400 on December 26, 1991. The index first closed above 40 on June 17, 1955 (that was the old S&P 90).

This morning’s jobless claims showed an increase to 770,000. Last week’s figure, which came very close to being the low for the last 12 months, was revised higher by 12,000.

Even though the report was higher than forecast, claims have generally been headed lower in recent weeks. This report tends to be “noisy.”

On our Buy List, we have new highs today from AFLAC (AFL) and Hershey (HSY). My friend Louis Navellier used to describe good stocks as acting like rabbits. They stand perfectly still and then suddenly, BOOM, take off. The recent AFLAC rally reminded me of that. It’s same the old duck, but it’s up 55% in less than five months.

-

Morning News: March 18, 2021

Eddy Elfenbein, March 18th, 2021 at 7:28 amBritain to Shake Up How Companies are Run and Audited

China Delivers on Threats to Rein in Internet Economy

Treasury Rout Deepens as Traders Brace for Inflation Overshoot

Unemployment Claims Remain a Distress Signal, Even as Recovery Takes Hold

U.S. Fed’s Powell Faces Political Test on Bank Capital Relief Question

Penny Stocks Are Booming, Which Is Good News for Swindlers

Higher Mortgage Rates Still Aren’t Cooling the Hot Housing Market

Sanders, Warren Reveal Bill to Tax CEO Pay During Income Inequality Hearing Targeting Amazon

Google’s Privacy Push Draws U.S. Antitrust Scrutiny

Google to Spend $7 Billion in Data Centers and Office Space in 2021

Carmakers Strive to Stay Ahead of Hackers

What Happened When American Investors Tried to Buy the World’s Oldest Bank

America’s Covid Swab Supply Depends on Two Cousins Who Hate Each Other

Michael Batnick: How to Break into the Industry

Howard Lindzon: Congrats To Brothers Yoni and Ronen Assia and Etoro.

Be sure to follow me on Twitter.

-

Today’s Fed Policy Statement

Eddy Elfenbein, March 17th, 2021 at 2:42 pmThe Federal Reserve is committed to using its full range of tools to support the U.S. economy in this challenging time, thereby promoting its maximum employment and price stability goals.

The COVID-19 pandemic is causing tremendous human and economic hardship across the United States and around the world. Following a moderation in the pace of the recovery, indicators of economic activity and employment have turned up recently, although the sectors most adversely affected by the pandemic remain weak. Inflation continues to run below 2 percent. Overall financial conditions remain accommodative, in part reflecting policy measures to support the economy and the flow of credit to U.S. households and businesses.

The path of the economy will depend significantly on the course of the virus, including progress on vaccinations. The ongoing public health crisis continues to weigh on economic activity, employment, and inflation, and poses considerable risks to the economic outlook.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. With inflation running persistently below this longer-run goal, the Committee will aim to achieve inflation moderately above 2 percent for some time so that inflation averages 2 percent over time and longer‑term inflation expectations remain well anchored at 2 percent. The Committee expects to maintain an accommodative stance of monetary policy until these outcomes are achieved. The Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and expects it will be appropriate to maintain this target range until labor market conditions have reached levels consistent with the Committee’s assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time. In addition, the Federal Reserve will continue to increase its holdings of Treasury securities by at least $80 billion per month and of agency mortgage‑backed securities by at least $40 billion per month until substantial further progress has been made toward the Committee’s maximum employment and price stability goals. These asset purchases help foster smooth market functioning and accommodative financial conditions, thereby supporting the flow of credit to households and businesses.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals. The Committee’s assessments will take into account a wide range of information, including readings on public health, labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Thomas I. Barkin; Raphael W. Bostic; Michelle W. Bowman; Lael Brainard; Richard H. Clarida; Mary C. Daly; Charles L. Evans; Randal K. Quarles; and Christopher J. Waller.

Here are the economic projections.

The median forecast for GDP growth for this year is now 6.5%. In December, the median was for 4.25%. That’s a big change.

-

10-Year Treasury Yields Hit 13-Month High

Eddy Elfenbein, March 17th, 2021 at 10:48 amYesterday, the stock market snapped its five-day winning streak. The market is down again today, but not by much.

The investing world is waiting on the results of the Federal Reserve meeting. The policy statement will come out at 2 pm ET. No change on interest rates or bond buying is expected. However, folks expect the Fed to revise its forecast for economic growth higher. Private forecasters have very optimistic outlooks for this year. Of course, that’s really recovering a lot of lost ground.

This morning’s housing report was a bit of a dud, but some of that was probably due to the lousy weather we had last month. For February, housing starts fell to an annual rate of 1.421 million. This was below expectations. Additionally, December and January were revised lower.

Applications to refinance a home are down 39% from one year ago. As interest rates on long bonds creep higher, so do mortgage rates. That’s starting to have an impact on the refi market. The 10-year Treasury just hit a 13-month high of 1.676%.

I used to talk a lot about the spread between the 2- and 10-year Treasury. This was especially true in August 2019 when the spread went negative. That’s often been a precursor of a recession. It was right again, but for very different reasons. In any event, the spread has dramatically widened in recent months, which should be good news for the economy.

-

Morning News: March 17, 2021

Eddy Elfenbein, March 17th, 2021 at 7:04 amBack to the ’70s As Fed Fuels Boom and Hopes for No Burns Marks

Congress Eyes Extending PPP Deadline for Businesses, As Billions Sit Untouched

Samsung Warns of Severe Chip Crunch While Delaying Key Phone

How to Clean Up Steel? Bacteria, Hydrogen and a Lot of Cash.

The High Costs of the Airline Bailouts

Analyst Says Volkswagen Will Overtake Tesla in Electric Vehicle Sales This Year

Learning Apps Have Boomed in the Pandemic. Now Comes the Real Test.

Teen Who Hacked Twitter to Within an Inch of Its Life Sentenced to Three Years in Prison

Trump’s Ailing Empire: His Fortune Slips to $2.3 Billion as Covid and Riot Take a Toll

Cullen Roche: Why Stocks and Bonds are the Core of any Portfolio

Nick Maggiulli: The Boy Who Cried Bubble

Ben Carlson: Why Housing is a Good Hedge Against Inflation

Howard Lindzon: TechAviv Roundtable This Morning NOON Eastern…Tune In

Michael Batnick: The Twenty Craziest Investing Facts Ever, It’s A Bubble & Animal Spirits: Super Bullish

Joshua Brown: Reverse Wealth Transfer on Steroids & Just Issue Those Stimulus Checks Directly To Coinbase

Be sure to follow me on Twitter.

-

The Fed’s Meeting Begins Today

Eddy Elfenbein, March 16th, 2021 at 11:17 amToday is the first day of the Federal Reserve’s two-day meeting. I don’t expect much to change in the way of the Fed’s policy. However, the Fed will update its economic forecast. Most private forecasters see the economy doing much better than the Federal Reserve’s forecast. The Fed will probably close the gap at this meeting. The statement will be out tomorrow afternoon.

We had two economic reports this morning. Both were hurt by harsh winter weather. Retail sales for February fell by 3%. We also learned that industrial production fell last month by 2.2%. A recent survey by Bank of America shows that investors fear inflation and the Federal Reserve more than they do Covid. I suppose that’s a change for the better.

Unseasonably cold weather gripped the country in February, with deadly snowstorms lashing Texas and other parts of the South region. The decline in sales last month also reflected the fading boost from one-time $600 checks to households, which were part of nearly $900 billion in additional fiscal stimulus approved in late December, as well as delayed tax refunds.

Excluding automobiles, gasoline, building materials and food services, retail sales decreased 3.5% last month after surging by an upwardly revised 8.7% in January. These so-called core retail sales correspond most closely with the consumer spending component of gross domestic product. They were previously estimated to have shot up 6.0% in January.

-

One Year Ago Today

Eddy Elfenbein, March 16th, 2021 at 10:57 am

Today is the one-year anniversary of Black Monday 2.0. On March 16, 2020, the Dow Jones Industrial Average plunged 2,997 points for a loss of 12.93%. The S&P 500 lost 11.98%. Only the 1987 crash was worse.

We're looking at a total wipeout this morning:

SPY -9.22%

XLE -9.91%

XLK -12.58%

XLF -12.19%— Eddy Elfenbein (@EddyElfenbein) March 16, 2020

As bad as it was, the market still had another week to go before it hit rock bottom. Still, even if you jumped into the market on March 16, the Dow is over 62% higher today.

If you’re familiar with the famous Variety headline “Wall St. Lays an Egg,” last March 16 was even worse. It was also on March 16 that the Federal Reserve went full Blutarsky: they lowered interest rates to 0.0%.

One year ago today, the VIX, the Volatility Index, closed at 82.69, an all-time high. On a four-day run last year, the VIX registered four of its seven highest closes.

-

Morning News: March 16, 2021

Eddy Elfenbein, March 16th, 2021 at 7:07 amXi Jinping Warns Against Tech Excess in Sign Crackdown Will Widen

How the U.S. Got It (Mostly) Right in the Economy’s Rescue

The Financial Crisis the World Forgot

Why This Week’s Fed Meeting Could Be ‘March Madness’ for Markets

Scorned 60/40 Model Finds Allies in Biggest Test Since 2016

These 10 Black Bankers Are Reshaping Wall Street

News Corp Inks Australia Facebook Deal, Signalling Truce After Blackout

How Amazon Crushes Unions & ‘There Was No Mercy’

Volkswagen Aims to Use Its Size to Head Off Tesla

Toys ‘R’ Us Has Been Sold … Again

Purdue Pharma to Use Public Trusts, Sackler Cash to Settle Opioid Litigation

Ben Carlson: The Most Important Investment Factor of the 21st Century

Howard Lindzon: Momentum Monday – Throw a Dart But Not At Tech Stocks

Joshua Brown: Everything’s Cool Til Three Percent on the 10-Year

Be sure to follow me on Twitter.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His