Archive for June, 2022

-

CWS Market Review – June 21, 2022

Eddy Elfenbein, June 21st, 2022 at 6:14 pm(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

The Worst Market Since 1932

The good news is that the stock market rebounded on Friday and today. The bad news is that that comes after a very sharp selloff. Last week was the worst week for the S&P 500 in two years, and this is the worst start to a year for the S&P 500 since 1932.

I know it’s painful, but to borrow from Hyman Roth in The Godfather 2, “this is the business we’ve chosen.” This is what markets do. Every so often, the stock market goes through a stretch where it can’t seem to do anything right. Fortunately, these periods don’t last long.

For prudent long-term investors, bear markets are very good opportunities. When other investors panic and sell, that usually offers a great chance to pick up bargains. In a bit, I’ll tell you about one of my favorites that just got an upgrade. Wall Street is the only place where a sale is announced and everyone runs out of the store screaming.

One of the important truths of the stock market is that it tends to rise slowly and drop off quickly. The old saying on Wall Street is that bulls walk up the stairs while bears jump out the window. Boy, is that right.

Today’s surge was a good example of a contra-trend rally. That’s a fancy phrase meaning all that stuff that’s been doing horribly did well today, and all the stuff that’s been doing well did poorly today. Bitcoin did very well today, as did Tesla. I’m not sure how long that will last. As we know, bear market rallies are common and mainly false.

You could even call this a “double contra-trend rally” because the previous trend was the opposite of the previous rally.

Confused? I don’t blame you. In this week’s issue, I’ll try to make some sense of what’s going on.

How to Break Down the Bear

Not only are bear markets sharp and quick, but even within bear markets, the most painful days are bunched together. The market crash of 2008 is a good example. I need to explain that I follow a slightly different chronology from convention.

I think it’s better to see the market blowup of 2008-2009 in three segments. There was the “initial selloff” from October 9, 2007 to August 28, 2008. Then came the “panic phase” from August 29, 2008 to November 20, 2008. Finally, there was the “retest phase” from November 20, 2008 until March 9, 2009.

The initial selloff lasted 224 days and the S&P 500 lost 16.90% (blue line). The panic phase lasted 59 days and the market lost 42.15% (red line). Ouch! The retest phase was 72 days and the market lost 10.09% (green line).

(There’s nothing official about those phases. I just made them up, but I think it’s a better way to analyze what happened.)

My point is that the panic phase was by far the worst of the worst. By no means do I want to ignore the other two periods, but those were fairly standard lousy markets.

Which brings me to 2022. I suspect that we just came through our panic phase. In seven days, the S&P 500 lost 11.9%. That’s slightly more than half of the entire bear market (-23.6% through last Thursday).

In plainer terms, it took more than 100 days to make half of our losses. It took seven days to make the other half. The panic phases are sharp and unpleasant, but they tend to be short-lived. It looks like we may be past ours. The hard part is that we’ll only know for sure in retrospect.

Historically, the worst parts of a bear market don’t happen at the start. More often, the pattern is that of a slowly rolling snowball that turns into an avalanche. That happened in both 1987 and 1929. As the small losses mounted, the panic spread and those small losses became big losses.

The market panic of two years ago is an exception. Once the world understood the gravity of Covid, the market quickly tanked. In March 2020, the Dow Jones Industrial Average had two of its worst five days in market history. There’s a famous Variety cover from 1929, “Wall St. Lays an Egg.” The market drop of March 16, 2020 was worse than that.

The Fed Holds the Key

How much will the selling go on? That’s impossible to say. The Federal Reserve holds the key. Since 1950, the S&P 500 has had 17 drops of 15% or more. Of those drops, 11 times the market reached its low as the Fed started to lower interest rates.

For now, the market expects the Fed to hike rates by another 2% before the end of the year. As long as inflation is a threat, then pressure will be on the Fed to raise rates, and there’s no sign that inflation is abating. Companies are feeling the pressure. According to FactSet, 417 companies mentioned inflation during their Q1 earnings calls.

What really spooked the Fed was the recent report from the University of Michigan on consumer sentiment. It said that households expect inflation to run at 3.3% for the next five years.

This is major a concern because so much of inflation is self-fulfilling. When consumers expect inflation, they get it. Jerome Powell talks a lot about expectations for inflation. Once expectations take hold, they’re not so easy to change.

The unpleasant reality is that the Fed has a very poor track record of attacking inflation without causing a recession. To a limited degree, you can say that may have happened in the mid-90s. Outside that, the evidence is not in the Fed’s favor.

I don’t think an economic inflation is imminent, but the odds of one starting within the next 12 months are high. Goldman Sachs just said it placed the odds at 30%, but that’s an increase from where they had it at 15%. For a recession within two years, Goldman placed the odds at 48%. Historically, stocks have fallen 24% during recessions. We’ve nearly done that without a recession.

Church & Dwight Is an Ideal Defensive Stock

Recessions are Wall Street’s most honest auditor. That’s when you really see which companies are strong and which are not.

Recessions also reveal which companies are closely tied to the economic cycle. During a recession, you want to make sure you own plenty of defensive stocks. These are businesses whose fortunes don’t depend so much on where we are in the economic cycle.

Speaking of defensive stocks, we had good news today for one of the best defensive names on our Buy List. Shares of Church & Dwight (CHD) were upgraded by Wells Fargo. The firm raised CHD to a buy from neutral.

Like so many other stocks, CHD has struggled this year. At the start of the year, CHD was close to $105 per share. Lately, it’s been as low as $80 per share. Wells Fargo said that its stable of businesses is poised to withstand any setback in the economy.

Church & Dwight is about as defensive a stock as you can get. The company makes condoms and baking soda. When will that lose demand?

For Q1, Church & Dwight had earnings of 83 cents per share. That beat expectations of 77 cents per share.

For the year, C&D sees earnings growth at the low end of their 4% to 8% range. The company said that’s due to the pressures from inflation. For Q2, CHD expects sales growth of 5% to 6% and earnings of 70 cents per share. I think they can beat that.

While CHD has been selling a lower volume of products, thanks to price increases, revenue is up. Last quarter, net sales increased 4.7% to $1.28 billion.

Thanks to the upgrade, shares of Church & Dwight rallied 4.6% today. The next earnings report is due out late next month.

If you want to learn about the other names on our Buy List, then please sign up for a premium subscription: $20 per month or $200 for the whole year.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

-

Morning News: June 21, 2022

Eddy Elfenbein, June 21st, 2022 at 7:07 amCompanies Find Leaving Russia Difficult, Though Many Are Trying

US Sanctions Help China Supercharge Its Chipmaking Industry

Dutch Government Activates ‘Early Warning’ Because of Russian Cutbacks on Gas

Italy Says Proposal to Cap Gas Prices Is Gaining Support in EU

Biden Says He Is Considering Seeking a Gas Tax Holiday

Are High Prices Unpatriotic or as American as You Can Get?

Inflation Collides With Growth Fears to Trigger Big Swings in the Bond Market

Morgan Stanley, Goldman Strategists See More Stock Market Losses

Goldman Warns US Recession Risk Now Higher and More Front-Loaded

Crypto’s Latest Meltdown Leaves Punters Bruised and Bewildered

US Home Prices to Sink by 2023 as Mortgage Rates Hit 6%: Analyst

Why You Might Buy Your Next Car Online

Anticipating U.S. Downturn, Elon Musk Details Tesla Staff Cuts

Kellogg to Separate Into Three Businesses

Vegas Company Promised Fast Internet. Rural America Waits…and Waits

Nobel Peace Prize Sold to Help Ukrainian Kids Shatters Record at $103.5 Million

Be sure to follow me on Twitter.

-

Morning News: June 20, 2022

Eddy Elfenbein, June 20th, 2022 at 7:09 amEurope May Shift Back to Coal as Russia Turns Down Gas Flows

French Nuclear Power Crisis Frustrates Europe’s Push to Quit Russian Energy

More Than Half of Global Consumers Didn’t Save During Pandemic

Hot Housing Market Keeps Home Foreclosures at Bay

Nerve-Racking Week Leaves Bond Investors Calling for Fast Rate Hikes

US Recession This Year Is Now More Likely Than Not: Nomura

Wall Street’s Classic Strategy Set for Worse Quarter Than 2008

Stocks Historically Don’t Bottom Out Until the Fed Eases

U.S. Banks Expect a Clean Bill of Health After Fed’s Stress Tests

When Customers Say Their Money Was Stolen on Zelle, Banks Often Refuse to Pay

‘Banking While Black’ Is the Next Target for Civil Rights Lawyer

Small Businesses Fall Behind on Hiring as Inflation Takes a Toll

Labor Shortage Stymies Construction Work as $1 Trillion Infrastructure Spending Kicks In

Red Flags for Forced Labor Found in China’s Car Battery Supply Chain

Apple Workers at Maryland Store Vote to Unionize, a First in the U.S.

Chinese Splash Out on Tech Goods, Camping Gear in Shopping Fest

U.S. Investors’ Buy of Chelsea FC from Roman Abramovich Puzzles Wall Street

Be sure to follow me on Twitter.

-

Morning News: June 17, 2022

Eddy Elfenbein, June 17th, 2022 at 7:02 amWTO Strikes Global Trade Deals After ‘Roller Coaster’ Talks

BOJ Maintains Ultra-Low Rates, Warns Against Sharp Yen Falls

Russia Slashes Gas Flows, Aiming Economic Weapon at Europe

High U.S. Fuel Exports Are Contributing to $5-a-Gallon Gas

One of China’s Most Famous Hedge Funds Is Springing Back to Life

U.S. Economic Growth Shows Signs of Slipping

Wall Street Shudders as Focus Returns to Recession Risks

By Design, the Fed May Be Tightening Too Much

One More Sign the Housing Market is Cooling Off

Gun Control Advocates Have More Money Now, but Money Can’t Buy Zeal

Amazon CEO Andy Jassy’s First Year on the Job: Undoing Bezos-Led Overexpansion

Why Amazon Isn’t Expecting a Robust Prime Day This Year

Elon Musk Talks Staffing, Free Speech, Remote Work in Twitter Employee Meeting

How Free-Wheeling Texas Became the Self-Driving Trucking Industry’s Promised Land

How a Religious Sect Landed Google in a Lawsuit

Be sure to follow me on Twitter.

-

Morning News: June 16, 2022

Eddy Elfenbein, June 16th, 2022 at 7:06 amTriple-Whammy for European Gas Supplies Sends Prices Soaring

Germany Appeals for Gas Conservation After Russia Tightens Flows

Swiss National Bank Hikes Rates by Half a Point, Franc Surges

Bank of England Hikes Rates For the Fifth Time in a Row as Inflation Soars

Powell Sets Path to Restrain Economy and Stop Runaway Inflation

Six Takeaways from the Fed’s Big Meeting on Wednesday

Bear Markets and Recessions Happen More Often Than You Think

U.S. Retail Sales Declined in May as Inflation Stings Consumers

Rising Interest Rates Could Cool Industrial Investment, Executives Say

Private Equity Faces ‘Crisis of Value’ Over Inflated Prices

Jim Chanos On Why Some of the Worst-Hit Stocks Still Have a Long Way Down

Robinhood’s Stock Is Now Worth Less Than Its Cash on Hand

Ethereum Mining Is Going Away, and Miners Are Not Happy

Inside a Corporate Culture War Stoked by a Crypto C.E.O.

Bill Gates Says Crypto and NFTs Are a Sham

Workers Don’t Feel Quite as Powerful as They Used To

Cosmetics Maker Revlon Files For Chapter 11

Be sure to follow me on Twitter.

-

The Fed’s Track Record

Eddy Elfenbein, June 15th, 2022 at 2:19 pmI often point out that the Fed doesn’t have a very good track record in predicting the economy. Here’s the trend of the Fed’s projection for inflation in 2022:

Sep 2019: 2.0%

Dec 2019: 2.0%

Jun 2020: 1.7%

Sep 2020: 1.8%

Dec 2020: 1.9%

Mar 2021: 2.0%

Jun 2021: 2.1%

Sep 2021: 2.2%

Dec 2021: 2.6%

Mar 2022: 4.3%

Jun 2022: 5.2%(Note that the Fed prefers to use PCE instead of CPI.)

The Fed currently expects inflation of 2.2% in 2024.

-

The Fed Hikes by 0.75%

Eddy Elfenbein, June 15th, 2022 at 2:07 pmThe Federal Reserve decided to raise interest rates by 0.75%. The new range for the Fed funds rate is 1.5% to 1.75%. This is the first time since 1994 that the Fed has increased rates by this much.

Overall economic activity appears to have picked up after edging down in the first quarter. Job gains have been robust in recent months, and the unemployment rate has remained low. Inflation remains elevated, reflecting supply and demand imbalances related to the pandemic, higher energy prices, and broader price pressures.

The invasion of Ukraine by Russia is causing tremendous human and economic hardship. The invasion and related events are creating additional upward pressure on inflation and are weighing on global economic activity. In addition, COVID-related lockdowns in China are likely to exacerbate supply chain disruptions. The Committee is highly attentive to inflation risks.

The Fed said it plans to continue to raise interest rates. The median forecast sees rates at 3.4% by the end of this year, and 3.8% by the end of next year. The cut has also cut back on its estimate for economic growth for this year, and it sees unemployment rising by a little bit.

The Fed sees inflation for this year at 5.2%, but it sees inflation falling to 2.2% by 2024. Esther George dissented from today’s statement. She wanted to see an increase of 0.5%.

-

Retail Sales Unexpectedly Fell in May

Eddy Elfenbein, June 15th, 2022 at 10:49 amThe big news today is the Federal Reserve meeting. The policy decision is due out at 2 p.m. Most of the world expects the Fed to increase rates by 0.75%. This would be the largest increase since 1994. The Fed will also update its economic forecasts.

However, we got a surprise this morning when today’s retail sales report came in negative. Sales dropped by 0.3% during May. Wall Street had been expecting a gain of 0.1%. Taking out cares, sales were up 0.5%. These numbers aren’t adjusted for inflation.

Sales were well below the pace in April, which posted a downwardly revised 0.7% increase from the initial 0.9% estimate.

Spending for the month declined even though sales at gas stations increased 4% due to fuel prices that scaled new heights, with regular unleaded hitting $4.43 a gallon in May and now running around $5. That growth was offset by a 3.5% decline at motor vehicle and parts dealers.

Miscellaneous store retailers saw a 1.1% drop in sales, while online stores posted a 1% decline. Bars and restaurants registered a 0.7% increase, part of a broader trend that has seen spending gradually shift from goods back to services.

Also today, I see that the yield on the 30-year mortgage rose to 6.28%. One week ago, it was at 5.5%.

-

Morning News: June 15, 2022

Eddy Elfenbein, June 15th, 2022 at 7:04 amAs Yen Tumbles, Japan’s Automakers Take Cost Burden Off Their Suppliers

What Europe’s Universal Charger Mandate Means for You

Romania Sees an Opening to Become an Energy Power in Europe

Denmark Overtakes Switzerland as World’s Most Competitive Economy

ECB Holds Emergency Meeting to Address Bond Selloff

Janet Yellen Is Struggling at the Treasury Job She Never Wanted

Fed’s Stern Message Amplifies Worries About Stock Valuations

Ben Bernanke: Inflation Isn’t Going to Bring Back the 1970s

Bitcoin’s Unrelenting Selloff Puts Prices on Verge of $20,000

MicroStrategy Denies It Received a Margin Call Against Its Bitcoin-Backed Loan, Report Says

Goldman Investigation Tarnishes ESG Halo as Investors Bail

U.S. Home Equity Hits Highest Level on Record—$27.8 Trillion

30-Year Mortgage Rate Surges to 6.28%, Up from 5.5% Just A Week Ago

Caterpillar to Move Global Headquarters to Texas From Illinois

Disney Wins TV Rights, Loses Streaming Rights for Indian Premier League Cricket

Mental-Health Startup Cerebral Investigated by FTC

Be sure to follow me on Twitter.

-

CWS Market Review – June 14, 2022

Eddy Elfenbein, June 14th, 2022 at 7:37 pm(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

It’s Official. We’re in a Bear Market

Yesterday was a terrible day for Wall Street. The stock market plunged, and it looks like the battle to defeat inflation will be a lot more difficult than many folks had originally anticipated.

On Monday, the S&P 500 lost 3.88% which made it the index’s second-worst day of the last two years. If you’re really into market history, it was the 161st worst day since 1928. In the entire S&P 500 on Monday, only five stocks closed higher.

More importantly, the S&P 500 closed below the 20% drawdown line which is the traditional definition of a bear market. At today’s market close, the S&P 500 is down 22.12% from its all-time high close reached on January 3 of this year.

Today was the lowest close for the stock market in more than 17 months. At one point, the stock market was up 26% during the Biden presidency. Now that’s all gone.

What driving the selling? The answer is easy. It’s the same thing that’s been happening, only more so. Inflation has spooked Wall Street and traders now believe the Federal Reserve needs to keep raising interest rates. To give you an example, since Friday, the yield on the two-year Treasury jumped from 2.83% to 3.45%. The two-year is often seen as a proxy for the market’s opinion for where rates ought to be. The two-year yield is now at a 15-year high.

Again, what we’re seeing is risky stocks getting slammed while more conservative stocks are down but not by nearly as much. On Monday, the S&P 500 Low Volatility Index fell by 2.97% while the S&P 500 High Beta Index dropped by 6.54%. The tech-heavy Nasdaq Composite is now down by one-third since November.

What’s really happening is that many stocks are giving back gains they never should have had in the first place. To give you an example, shares of Moderna (MRNA) are now trading at one-quarter of their value in August. Shares of Zoom (ZM) are down more than 80% from their high. Netflix (NFLX) is off by 70% just this year, and we’re not even at July 4!

Everything seemed so easy before that meddling inflation showed up! The bull market that recently ended was one of the fastest on record, and it was the quickest ever to double. Now the bill has come due.

Over four trading days (Wednesday to Monday), the losses got progressively worse. On Wednesday, the S&P 500 lost 1.1%. Then on Thursday, it fell 2.4% followed by another 2.9% on Friday. Today was the market’s best day of the last week, and that’s still a loss of 0.38%.

I’m pleased to say that our conservative-oriented Buy List keeps chugging along. Since June 1, the S&P 500 is down by 8.92% while our Buy List is off by “just” 7.30%. I know it sounds odd to point out that we’re down but by less, but that’s where a lot of long-term outperformance comes from. Our stocks are generally much higher quality and that protects them during a storm like this. I’ve used this quote before, but it’s a good one from Shelby Cullom Davis: “You make most of your money in a bear market; you just don’t realize it at the time.”

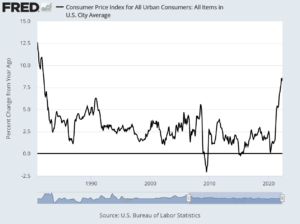

Worst Inflation Since 1981

What spurred the bad news on Friday was another troubling inflation report. There had been some hope that we might see some evidence that inflation had cooled off during May. Well, that didn’t happen. The government said that consumer prices rose by 8.6% in the 12 months ending in May. That’s the highest inflation rate since December 1981.

Digging into the details, the picture is not encouraging. Instead of cooling off, it seems that inflation is getting worse. The monthly rate of inflation increased from 0.3% in April to 1.0% in May. That’s the second-highest monthly rate of the last 10 years.

At that rate of inflation, if you’re paid in dollars at a fixed rate for one year, that means you effectively work one month of the year for free, and that doesn’t include taxes. Inflation is also taking its toll on wages. Last month, inflation-adjusted wages fell by 0.6%.

It’s true that food and energy have been driving much of the inflation, but the core rate also remains stubbornly high. For the 12 months ending in May, the core rate of inflation increased by 6.0% which was higher than expectations. For the month, the core rate increased by 0.6%. To give you an idea of how much things have changed, the core rate of inflation for the 12 months ending in February 2021 was just 1.3%.

Look for the Fed to Hike by 0.75%

The Federal Reserve is meeting again in Washington. The policy statement is due out tomorrow at 2 p.m. Yesterday afternoon, the stock market got another shock when the Wall Street Journal reported that the Fed was considering raising interest rates by 0.75%. I should explain that when the Wall Street Journal reports that the Fed is considering something, you can be pretty sure this is coming from the top.

A string of troubling inflation reports in recent days is likely to lead Federal Reserve officials to consider surprising markets with a larger-than-expected 0.75-percentage-point interest-rate increase at their meeting this week.

Before officials began their premeeting quiet period on June 4, they had signaled they were prepared to raise interest rates by a half percentage point this week and again at their meeting in July. But they also had said their outlook depended on the economy evolving as they expected. Last week’s inflation report from the Labor Department showed a bigger jump in prices in May than officials had anticipated.

The Fed was also shocked by two recent reports showing that consumers are starting to expect higher inflation. This is why inflation is so difficult to fight. It becomes a self-fulfilling prophecy. Once consumers expect it, they get it.

Before the WSJ scoop, investors had been expecting an increase of 0.5%. In fact, the Fed basically said so. In May, Fed Chairman Jerome Powell said that the Fed was not “actively considering” larger increases. Apparently, that’s all changed. One week ago, the futures market pegged the odds of a 0.75% rate hike at 4%. Now it’s at 94% and a slew of major Wall Street investment houses say they expect to see a 0.75% hike tomorrow. The Fed hasn’t done a 0.75% hike since 1994.

I’m glad to see the Fed finally realize the problem is more acute than they had initially believed. The problem is that the Fed’s main tool is short-term interest rates. That’s a very blunt tool. The Fed thinks it can enact precise fine-tuning with rate hikes. They think they’re using scissors when they’re really using an axe.

I think there’s a very good chance that we’ll see another 0.75% at the Fed’s next meeting in July. That would bring the Fed’s target range to 2.25% to 2.5%. How high will the Fed go? That’s a good question. The place to look is long-term rates. I would guess that the Fed wants to make the yield curve flat, even a little negative. With the 30-year yield at 3.45%, that means the Fed could go as high as 4% within the next six to nine months.

The larger story remains the same. The Fed overreacted to Covid by lowering rates to the floor. That radically changed the math on Wall Street as high-risk stocks became no-brainers. There was a big bull market in everything risk. Not just riskier stocks, but also crypto and NFTs. Higher rates are tripping up all those high-risk, high-volatility sectors. In less than two months, the price for bitcoin has been cut in half. Bitcoin is now down 69% from its peak. Remarkably, this is only its seventh-steepest correction in the last 12 years.

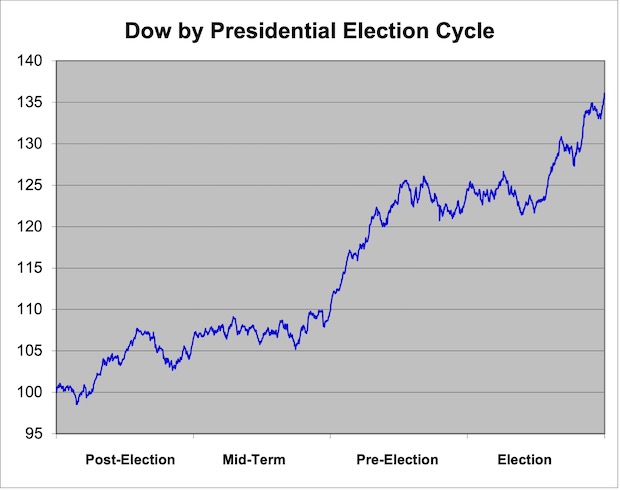

The Low in the Presidential Election Cycle

I’m not much of a fan of historical patterns in the stock market, but I’ll highlight one for you today. The stock market has traditionally reached a low point during midterm years in the presidential election cycle. As it turns out, this is one such year and the midterm elections are less than five months away.

I’ve crunched over 130 years of data on the Dow Jones Industrial Average and found that the low point of the presidential cycle comes on September 30 of the midterm year. Historically, the 15 months prior to September 30 of the midterm have been pretty blah for stocks.

However, after September 30, the stock market has done quite well. From September 30 of the midterm year until July 22 of the pre-election year, the Dow has gained an average of 19.3%. That’s more than half of the market’s entire gain coming in less than 11 months.

Here’s what the average presidential election cycle has looked like:

That’s the average of 125 years of the Dow. I set the chart to start at 100 on January 1 of the post-election year.

My point is not about timing the market. Rather, it’s that there tend to be broad cycles in the stock market. Though we’re in a painful bear market, this too shall pass. In fact, we’re seeing excellent bargains right now.

Last week, we had a very strong earnings report from Science Applications International (SAIC) which is our #2 performing Buy List stock this year. The company beat earnings and raised guidance.

That’s all for now. The stock market will be closed this Monday in honor of Juneteenth. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. Don’t forget to sign up for a premium subscription: $20 per month or $200 for the whole year!

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His