CWS Market Review – February 28, 2023

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

The Market’s Cold February Comes to an End

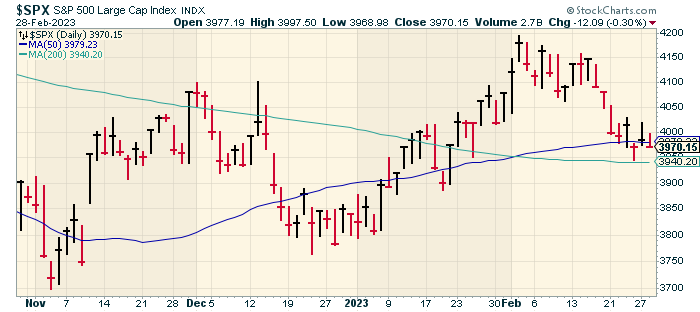

The month of February has come to an end, and I, for one, won’t miss it. Wall Street was squeezed by a lackluster earnings season and stubborn inflation. That’s a bad combo for stock prices. Apparently, the bulls saw their shadows and scurried off. Indeed, the S&P 500 lost just over 2.6% during February.

According to Bloomberg, Q4 earnings “were 0.1% below Wall Street’s forecast at the start of earnings season.” That’s very bad. Before the pandemic, companies had beaten forecasts by an average of 3.7%. Versus expectations, this has been on of the worst earnings seasons in years.

There are, however, reasons for optimism. My friend Gary Alexander points out that over the last 20 years, the stock market has done better in the three months from March through June than in the other nine months combined. We also shouldn’t forget that the stock market is still positive by 3.4% for the year.

The big market story for February is that we thought the Federal Reserve was close to the end of its interest-rate hiking. Now that appears not to be the case.

How much higher will rates go? Well, that’s still a mystery, but I suspect it won’t be too much longer. Make no mistake: the end of rate hikes will lift a major weight from the back of the stock market. There are few things bulls like better than the Fed slashing short-term rates. Some folks think we’ll see that before the end of the year.

The other big market story for February was the brief rotation away from high-risk stocks. Those sectors got off to a fiery start this year, but that trend got tripped up in February.

Investors need to understand that these two stories are related. The stock market has grown more conservative exactly as it has feared a more aggressive Fed. That’s one of the major reasons why our Buy List did so well against the stock market last year, and we’re beating the market again this year.

Inflation Is Still a Big Problem

Let’s break down some of the recent economic data. Last Thursday, the Commerce Department said that the U.S. economy grew, in real terms, at an annualized rate of 2.7% in the final three months of 2022. That’s a downgrade from the initial report which said that the economy grew at a 2.9% rate. For comparison, the economy grew by 3.2% in the third quarter.

While those numbers aren’t great, they’re not that bad. At least it’s not a recession. The first two months of last year showed negative economic growth—the economy receded, but that was more due to technical reasons rather than a broad slow down. There hasn’t been a recession yet, but that may soon change.

What can we expect for Q1? We’re already two-thirds of the way through Q1. Bank of America said it expects real growth of 1.3%. Goldman Sachs is a little more optimistic. They expect growth of 1.8%. The Atlanta Fed’s GDPNow model is the most bullish. Their model currently expects Q1 growth of 2.7%.

I have to stress that the economic data can often be confusing, and it seems to point in several directions at once. I’ve often been a guest on financial news shows and I’m afraid I don’t come off well. The producers want to have a bull line up with a bear and have them duke it out. It makes for great TV. Instead, they get me, and I’ll say something like, “Well, it’s hard to say at this point, and there are several conflicting trends at once.” That’s awful TV.

Back to the economy. The day after the GDP report comes out, the Commerce Department releases the numbers for the Personal Consumption Price index. This is important to watch because it’s the preferred inflation measurement for the Federal Reserve.

That data showed that inflation rose by 0.6% in January which means inflation accelerated from a 0.2% increase for December. The 12-month rate increased from 5.3% ending in December to 5.4% for the 12 months ending in January.

The core PCE rate rose by 0.6% in January and by 4.7% for the 12 months ending in January. Wall Street had been expecting a 12-month rate of 4.3%.

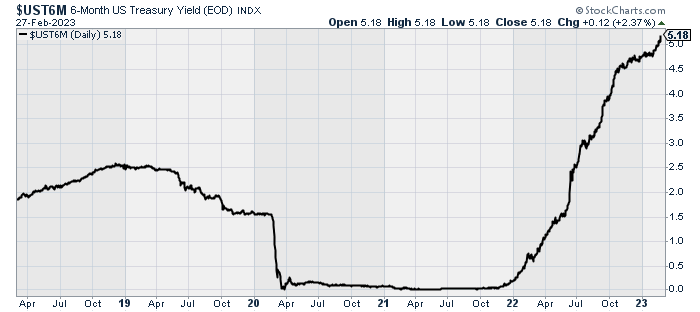

Wall Street, and the bond market in particular, did not take these numbers well. On Monday, the yield on the six-month Treasury got to 5.18%. For context, at one point in June 2021, the six-month bill was yielding just 0.02%.

The futures market now expects the Fed to increase rates by 0.25% at its next three meetings (March 22, May 3 and June 14). After that, traders expect the Fed to pause until the end of the year.

The labor market continues to be very strong. The last jobs report showed an unemployment rate of 3.4%. That’s the lowest in 53 years. Labor force participation has improved, but I’d like to see it climb higher. Initial jobless claims are down to 192,000. That’s quite good. That data series has trended lower since November.

The next jobs report won’t be out until the second Friday of the month which will be March 10.

On Friday, the Census Bureau said that new single-family home sales came in at an annualized rate of 670,000. That’s down 19% over the last year but it’s up 7% over December.

Over the last year, the average home price is down 5.3% but the median price is down just 0.7%. That suggests that the higher-priced homes are feeling the largest impact.

On Monday, we got the report on pending home sales. The National Association of Realtors said that pending home sales rose by 8.1% last month. That’s the largest increase since June 2020. Some of the increase is due to lower mortgage rates at the end of last year. Even with the increase, over the past year, pending sales are down more than 24%. From Bloomberg, “The jump beat all estimates in a Bloomberg survey of economists, which called for a 1% advance.”

On Monday morning, we got the report on orders for durable goods. The headline number was very bad. Orders for durable goods plunged by 4.5%, but that drop was almost all due to Boeing. In December, Boeing got a surge in orders, so that led to a slow January.

Airplane orders can be very volatile. If we exclude transportation, then orders were up by 0.7%.

From MarketWatch:

More important, business investment climbed 0.8% to mark the fastest gain since last August. Investment had declined in three of the last four months of 2022.

Still, the annual rate of growth in business investment slowed again to 4.3% from 5% — less than half the pace compared with one year ago.

These orders exclude military spending and the auto and aerospace industries.

The odds are low that the economy will avoid a recession this year, but it looks like those odds are rising. Now let’s look at a little-known stock that has proved to be a winner in good times and bad.

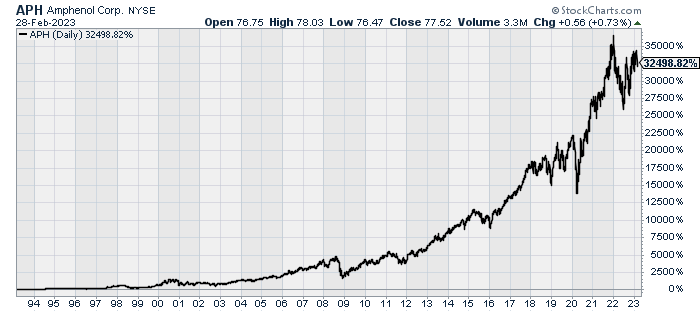

Stock Focus Amphenol Corporation

Last week, we looked at Illinois Tool Works (ITW) which is a big company that’s done very well but it seems to get overlooked. This week, I want to look at another such company.

This week, we’re looking at Amphenol (APH). Over the last 30 years, APH is up an amazing 326-fold. That’s more than 21% per year.

Despite its success, Amphenol doesn’t seem to get much attention. The stock is rarely mentioned in the media. Last year, it had sales of $12.6 billion. The name Amphenol comes from the company’s original name which was the American Phenolic Corporation. The company was founded by Arthur J. Schmitt in 1932.

Schmitt found that “insulating plastic could effectively be used to produce tube sockets in a quicker and simpler method than using Bakelite or ceramic.” The company made military equipment and radios during World War II.

Today, the company is a major producer of electronic and fiber optic connectors, cable and interconnect systems such as coaxial cables. Amphenol is based Wallingford, Connecticut and has 91,000 employees.

On January 25, Amphenol reported Q4 earnings of 78 cents per share. That beat estimates by three cents per share. For 2022, Amphenol made $3.00 per share. That’s up from $2.48 per share in 2021.

For Q1, Amphenol expects to fall by 2% to 4% to a range of $2.84 to $2.9 billion. Amphenol sees earnings between 65 and 67 cents per share.

For this year, Wall Street expects earnings of $2.99 per share, and it sees $3.30 per share for 2024. That gives the stock a decent valuation of 23.5 times next year’s estimate. Ideally, I’d like to see APH a little cheaper, but this is one of the most consistent stocks around.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want to learn more about the stocks on our Buy List, please sign up for our premium service. It’s $20 per month, or $200 per an entire year.

Posted by Eddy Elfenbein on February 28th, 2023 at 5:07 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His