CWS Market Review – August 1, 2023

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

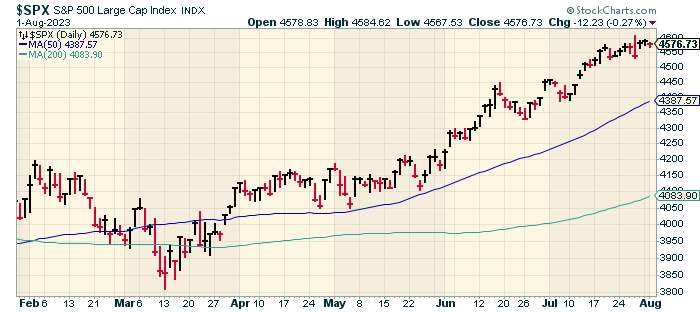

On Monday, the S&P 500 closed out July with another nice gain. This was the index’s fifth monthly gain in a row which is the longest monthly winning streak in two years. This is also the S&P 500’s best YTD gain through July since 1997.

It’s been a calmer stock market as well. On Friday, the Volatility Index closed at 13.33. That was its lowest level since January 2020.

I’ve been pleased to see the rally becoming broader, meaning that more stocks are joining in on the fun. Until recently, the market had been very narrow. It was rightfully criticized for being overly focused on a few large-cap tech stocks.

That’s not so true anymore. For the last two months, the S&P 500 Equal Weight ETF (RSP) has outpaced the rest of the market. Ryan Detrick, a great stat resource, points out that at one point last week, more than 89% of the stocks in the S&P 500 were trading above their 50-day moving averages. In other words, the minnows are joining the rally.

The Resilient U.S. Economy

The U.S. economy continues to hold up as well. I can’t think of a recession that’s been so widely expected yet so stubborn in refusing to make its appearance. Most of the recent economic signs have been fairly positive.

Just look at the earnings reports this season. This will be the busiest week of earnings season with 160 stocks in the S&P 500 due to report. So far, 82% of companies that have reported have beaten expectations.

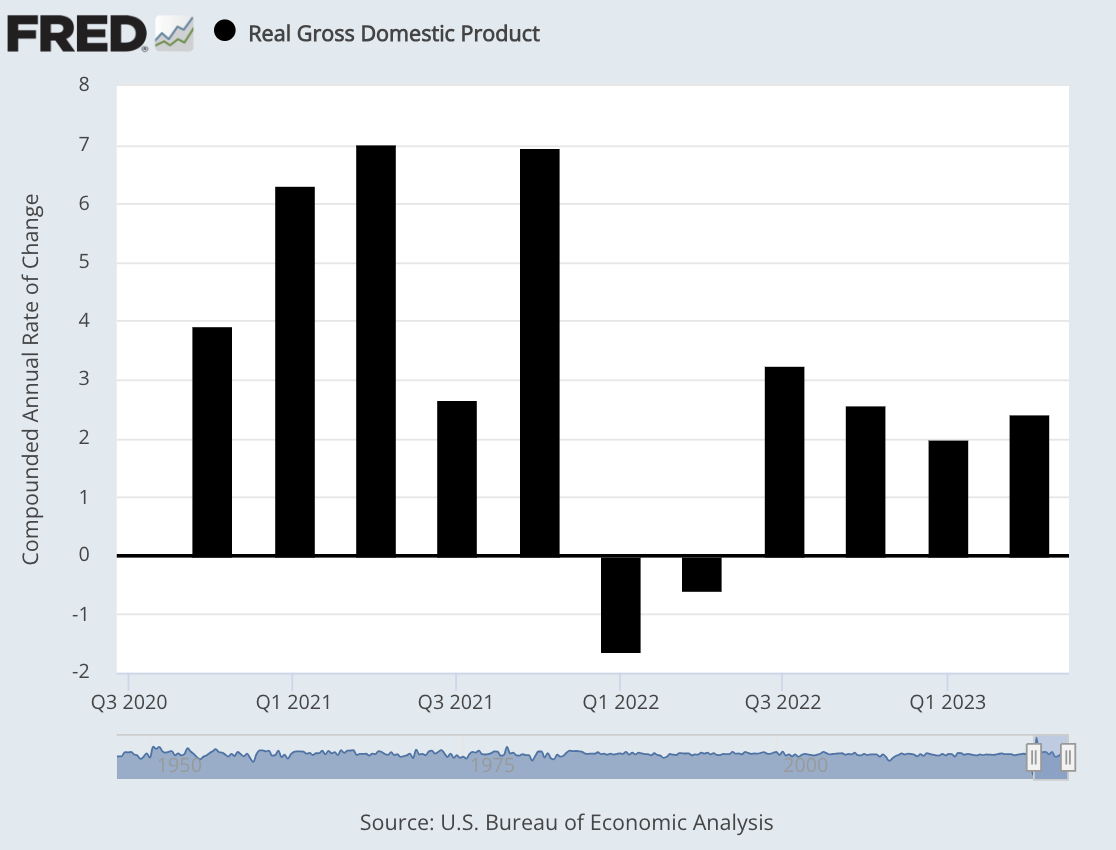

Last Thursday, the government reported that the U.S. economy grew at a real annualized rate of 2.4% during the second quarter. Wall Street had been expecting growth of 1.5%.

Some people thought this spring’s banking crisis would trip up the economy. Nope, that didn’t happen. Other folks thought all the tech layoffs would push us unto recession. Again, that didn’t happen.

The economy’s performance is especially impressive because not that long ago, many economists assumed that the economy would be well on its way to a recession by now.

In April, the Conference Board said the odds of a recession starting in the next 12 months were “near 99%.” Now, the Federal Reserve’s own staff no longer expects a recession to begin this year. In fact, consumers are pretty optimistic. The sentiment survey put out by the University of Michigan recently hit its highest level in nearly two years. That’s some recession!

If anything, economic growth appears to be accelerating. Growth for Q1 was 2.0%. In the Fed’s last policy statement, it described the economy’s growth as “moderate.” In June, the Fed said growth was “modest.” I realize this may sound weirdly technical, but such wording changes are a big deal on Planet Fed.

So what’s powering the economy? The answer is consumer spending. Last quarter, the economy was also helped by increases in nonresidential fixed investment, government spending and inventory growth.

During Q2, personal consumption expenditures rose by 1.6%. While that was lower than the rate from Q1, during Q2, the economy was running against higher interest rates. Since March 2022, the Federal Reserve has raised interest rates 11 times. Interest rates are now at a 22-year high.

Another good sign is that inflation has been cooling off. The personal consumption expenditure price increase rose by 2.6% during Q2. That’s down from 4.1% in Q1.

Investors got nervous last year when the economy had negative growth for two quarters in a row. Since then, the economy has rattled off four straight quarters of positive growth. We’ll learn more about the economy this Friday when the July jobs report will be out. The estimate is that the economy created 200,000 nonfarm jobs and that the unemployment rate will be unchanged at 3.6%.

More positive economic news came on Thursday when we got the durable goods report for June. That came in at 4.7% which was well above Wall Street’s forecast of 1.5%. On Friday, the Bureau of Economic Analysis said that personal income increased by 0.3% in June while personal spending increased by 0.5%.

Earlier today, the ISM Manufacturing Index for July was reported at 46.4. That was a little below expectations. Any number below 50 means that the factory sector of the economy is contracting.

What’s the Fed’s next move? Probably nothing. In the last three recessions prior to the Covid-led recession in 2020, the Fed had started cutting rates before the time the recessions had arrived. This underscores an important problem: the Fed’s major policy tool, adjusting interest rates, is highly imperfect.

For one, it takes a long time after the Fed makes any changes in rates to witness the intended results. This is one of the reasons why the Fed so often seems to mistime events. Just recently, the Fed was well behind the curve regarding inflation.

Fed Chairman Jerome Powell continues to sound stern. He recently said, “We think we need to stay on task. We think we’re going to need to hold policy at restrictive levels for some time. And we need to be prepared to raise further.” The market, however, isn’t so sure.

The Fed doesn’t meet again until September 19-20. For now, traders expect another pause from the Fed. In fact, the Fed might pause for a few meetings. Futures prices don’t see the Fed making a move until March, and that initial move is expected to be a rate cut.

The early evidence suggests that inflation continues to moderate. The issue is how quickly will the Fed finally recognize that inflation is under control. My view is that the rally is telling us the truth and that there are lots of reasons to be bullish.

Trex Rallies on Strong Earnings

Trex (TREX) is a valued member of our Buy List. The deck stock, like some people, has a habit of either running very hot or very cold. There’s not much in between.

Trex was our #1 performing stock in 2020 (+86%) and 2021 (+61%). Last year, it was our worst performer by far (-68%). This year, Trex is again our top performer (+79%).

If you’re not familiar with the company, Trex is a major maker of wood-alternative decking and railing. In my opinion, what they make looks a lot like wood, but it’s cheaper and involves a lot less maintenance.

Trex is also better for the environment. Pressure-treated wood still dominates which means there’s plenty of room for Trex to grow. It’s also nice to know that with Trex, you don’t have to take another tree out of the Amazon rainforest to make your backyard deck.

Trex is made from 95% recycled material. Every year, the company effectively takes 500 pounds of plastic out of landfills and uses it for alternative wood. It’s not just good for the planet, but it’s smart business.

Trex takes all those used bags and bottles, then combines them with recycled sawdust from cabinet and furniture manufacturers, and that’s what Trex is made of. By the way, this also saves a lot of water.

Some other key advantages are that Trex weighs less than wood and that it’s also more resistant to mold and insects. You don’t need expensive staining or sanding, and repairs are much less frequent. You’ll often hear people say that Trex looks fake. I think that used to be true, but it’s much less the case today.

The recent problem for Trex is that the Fed’s desire to crush inflation also crushed its business. That’s because higher interest rates squeezed the housing market. Last year, shares of Trex plunged by two-thirds.

The good news is that Trex is improving nicely. After the closing bell yesterday, Trex reported Q2 earnings of 71 cents per share. That topped Wall Street’s consensus of 53 cents per share.

Trex had quarterly net sales of $357 million. Although that’s down 5% from last year’s Q2, it was well above Trex’s own guidance range of $310 million to $320 million.

I’m also pleased to see that Trex isn’t reaching for sales by slashing prices. As investors, this is something we have to look out for. When some companies run into trouble, they’ll slash prices to goose sales at the expense of profit margins. Not so with Trex. The company’s Q2 gross margin increased by 220 basis points to 43.9%. Trex had an EBITDA margin of 32.8%.

Now let’s look at guidance. The company expects full-year sales to range between $1.04 and $1.06 billion. For Q3, Trex sees sales of $280 million to $290 million. Wall Street had been expecting $264.22 million.

Most impressively, Trex raised it guidance for full-year EBITDA margin to a range of 28% to 29%. That’s up from the previous guidance of 26% to 27%.

During Q2, Trex bought back 264,896 shares for $16 million. Trex’s board recently approved a massive buyback program of up to 10.8 million shares. That’s 10% of all the outstanding shares.

Shares of Trex jumped 10% today and reached a new 52-week high. We now have a 79% YTD gain with Trex. Thanks to our buy-and-hold philosophy, we have a three-and-a-half-year profit in Trex even after last year’s implosion, and we’ve beaten the overall market as well. Focus on good stocks and be patient.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want more info on our ETF, you can check out the ETF’s website.

Posted by Eddy Elfenbein on August 1st, 2023 at 6:19 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His