CWS Market Review – January 9, 2024

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Wall Street Gets Off to a Slow Start for 2024

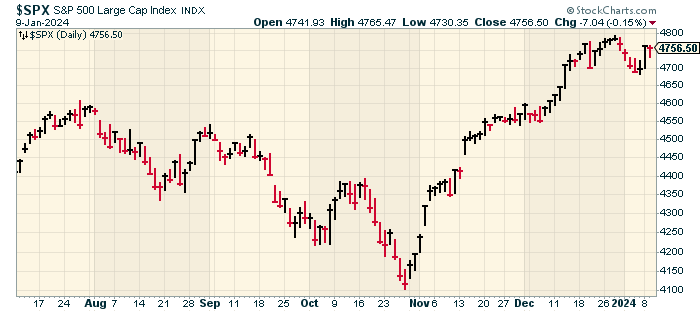

The stock market is off to a somewhat slow start this year. Last week, the S&P 500 snapped a nine-week winning streak. The index has now closed lower in five of the past seven sessions.

In reality, the current market action is closer to how we should expect markets to act, at least in the near-term. What was unusual about this market was the furious rally that closed out last year.

As late as mid-October, last year was looking to be a fairly standard year for investors. However, once it became clear that the Fed was done with its interest rate hikes, stocks started to rally. In less than two months, the S&P 500 jumped 16%.

As we got to the finish line for 2023, many of those prominent growth stocks and riskier “high-beta” stocks lagged the market. This trend lasted into the first few days of 2024 but has since reversed.

Q4 Earnings Season Is About to Begin

There are two events to look out for this week. The first will be on Thursday when the government releases the inflation report for December. For the most part, inflation has been better behaved, but I don’t want to call victory too soon. Older investors will remember how inflation kept coming back in the 1960s and 70s. In fact, each peak got progressively higher.

The other event will be the start of Q4 earnings season. This is unofficial, but on Friday, several major Wall Street banks and financial institutions will tell us how well they did during the final quarter of 2023.

Some of the financial institutions due to report on Friday include Bank of America (BAC), Bank of New York Mellon (BK), BlackRock (BLK), JPMorgan Chase (JPM), Citigroup (C) and Wells Fargo (WFC).

Overall, this looks to be a rather sluggish quarter for earnings growth. According to the latest numbers, Wall Street expects Q4 earnings growth of 1.82% for the S&P 500. That’s down from 2.85% from one month ago.

Within industry sectors, analysts expect 15.80% growth from Consumer Discretionary. That’s up from 13.52% from one month ago. For Tech, analysts have raised their estimate from 14.74% growth from one month ago to 15.08% now.

The big loser is the Energy sector. Profits for Energy are expected to fall 26.94%. As bad as that is, it’s dropping. One month ago, analysts had been expecting Energy’s profits to fall by 23.42%.

The first of our Buy List stocks to report will probably be in about two weeks. I’ll caution you that companies often need a little more time to compile their Q4 earnings reports compared with the other three quarters.

Don’t get worried if a company needs a little extra time. If a company reports its Q1 earnings on, let’s say, April 27, you can most likely expect its other earnings to be around July 27 and October 27, but the Q4 report may be a week or so after January 27.

The U.S. Economy Added 216,000 Jobs in December

Last Friday, the government said that the U.S. economy added 216,000 net new jobs last months. That was much better than expectations. Wall Street had been looking for an increase of 170,000 new jobs. The unemployment rate held steady at 3.7%. Wall Street had been expecting it to rise to 3.8%.

While the jobs numbers for December were decent, the jobs gains for October and November were revised lower to 173,000 and 105,000, respectively.

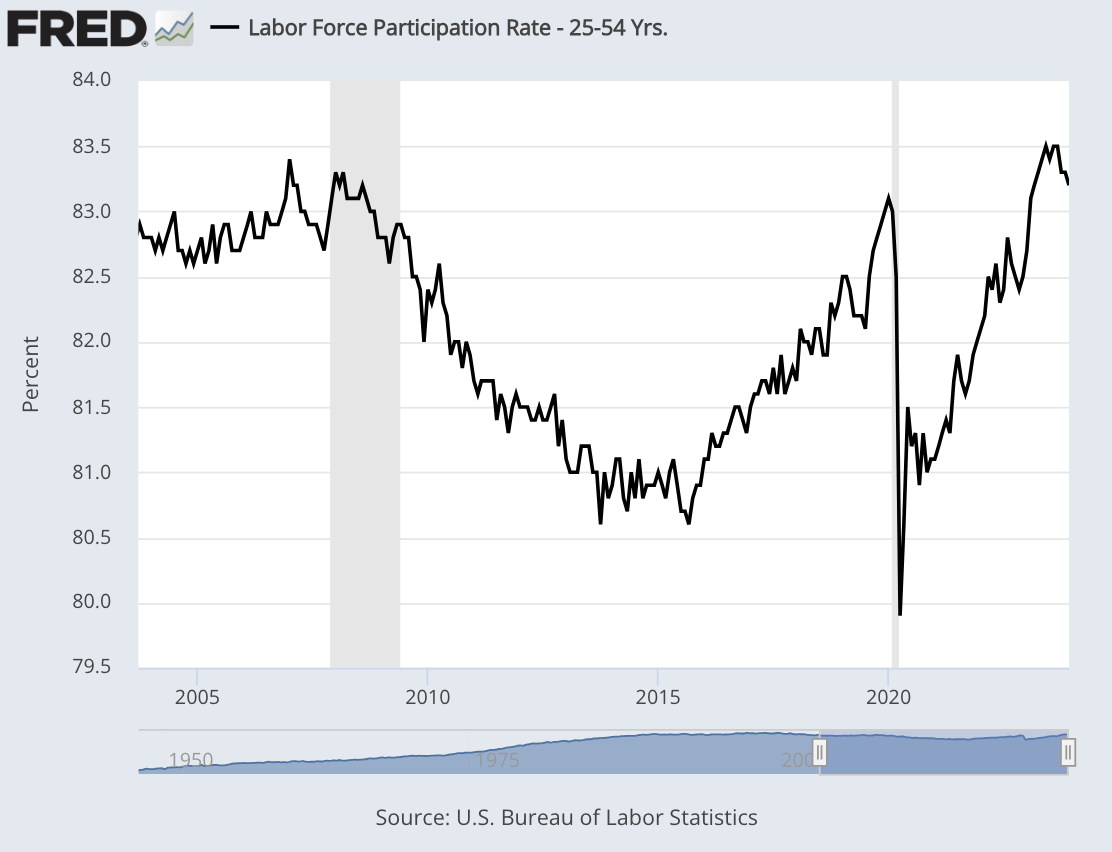

The U-6 rate, which is a wider measure of joblessness, increased to 7.1%. The labor force participation rate (LFPR) fell 0.3% to 62.5%. That number is now at its lowest point since February.

The labor force participation rate had been improving for several months. The problem with the LFPR is that it can be distorted by demographic factors. For example, more retirees will drive down the LFPR. If we look at it just for folks in the prime working-age category (25 to 54), then the LFPR is close to a 20-year high.

Perhaps the most important stat in the jobs report is average hourly earnings. Last month, average hourly earnings rose by 0.4%. That’s good, but I hope to see better. Over the last year, average hourly earnings are up by 4.1%. The problem is that so much of the wage gains have been eaten up by inflation.

One of the problems with this jobs report is that the job gains have been concentrated in a few areas while important sectors of the economy have actually seen job losses:

The December hiring boost as reflected in the Labor Department report came from a gain of 52,000 in government jobs and another 38,000 in health care-related fields such as ambulatory health-care services and hospitals. Leisure and hospitality contributed 40,000 to the total, while social assistance increased by 21,000 and construction added 17,000. Retail trade grew by 17,000 as the industry has been mostly flat since early 2022, the Labor Department said.

On the downside, transportation and warehousing saw a loss of 23,000.

For the year, the U.S. economy added 2.7 million jobs. That’s a noticeable drop off from 4.8 million in 2022.

The Federal Reserve meets again at the end of this month, and again, I don’t expect to see any changes to interest rates. The March meeting is a different story. Currently, the futures market thinks there’s a 64% chance that the Fed will cut rates. That’s down a bit from the odds before the jobs report.

Later this month, we’ll get the initial report on Q4 GDP growth. The Atlanta Fed’s GDP Now model said that the economy grew at a real, annualized rate of 2.2% for Q4.

The End of the Month Effect

One of my peculiar habits is that I maintain a very large database of historical market stats. For example, I have every closing for the Dow Jones Industrial Average since the index was birthed in 1896. That’s more than 30,000 data points.

At the end of each year, I update all the numbers. I then slice and dice the numbers several different ways to see how the market has performed historically. (I know…I need a better hobby.)

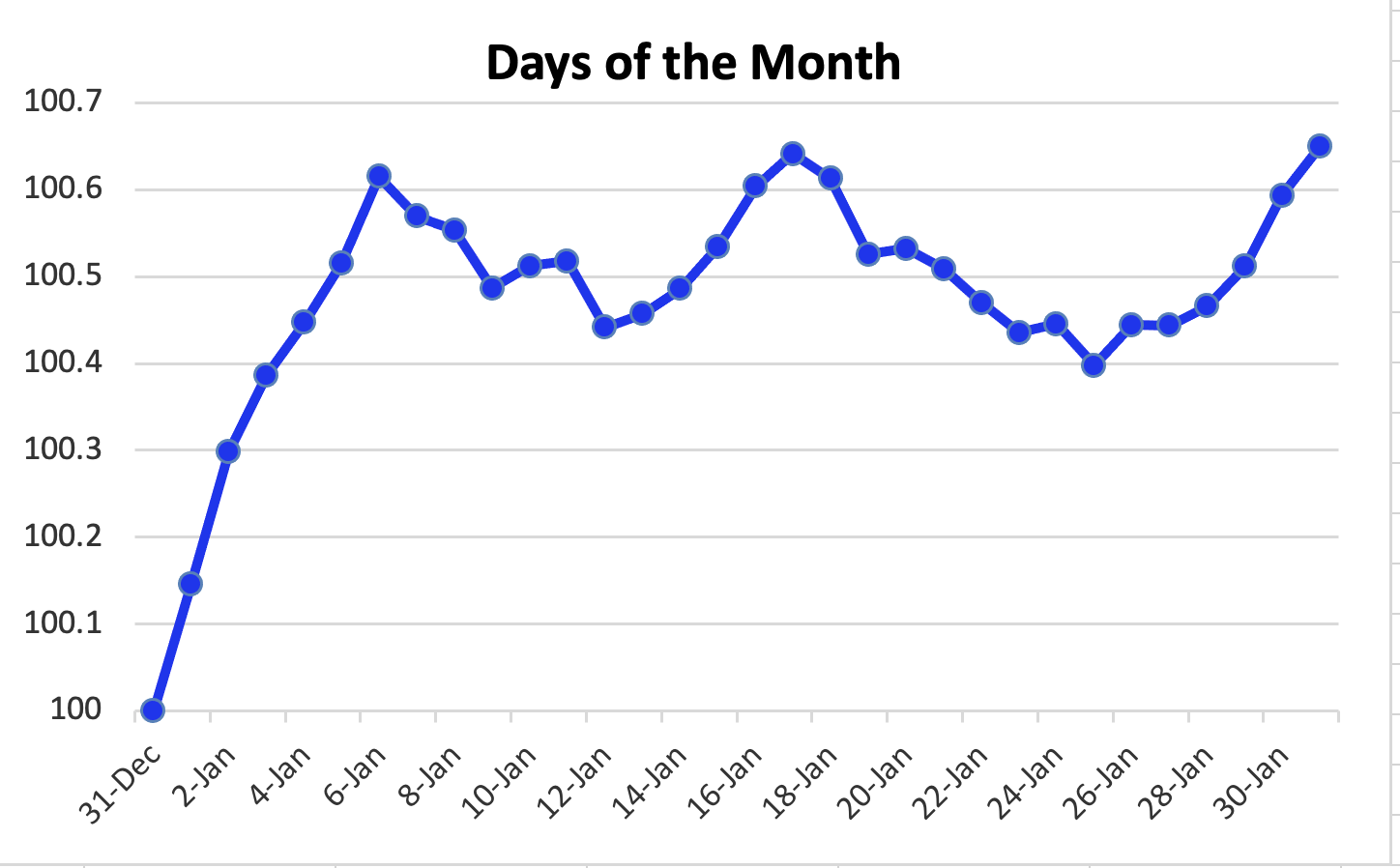

Today I wanted to share with you one of the more fascinating results I got which is the end-of-the-month effect. Very simply, all of the stock market’s gains over the last 13 decades have come on the first and last days of each month. The rest of the month has been net flat.

Make no mistake. I’m not advocating for some kind of trading strategy to try and profit from the end-of-the-month effect. I’m still a buy-and-hold guy, but I find the effect fascinating.

I took all the numbers and squished them together to show you what the average month has looked like for the DJIA since 1896. Here it is:

I used the days of January as a placeholder for the horizontal axis, and I started the series at 100 at the start of the month. On average, the Dow has gained 0.650% each month.

During the first six days of the month, the Dow has had an average gain of 0.615%. During the rest of the month, the Dow has eked out a miniscule 0.035%.

If we dig a little further, we see that the Dow has lost an average of 0.216% by investing from the 6th to the 25th of each month. That’s roughly one-third of the entire monthly gain. From the 25th to the 6th, the Dow has gained an average of 0.867%.

What causes this? I’m not certain, but I’d guess that that’s when investors have gotten new money to add to stocks. It’s amazing that 130 years of data shows such a large impact from the calendar.

That’s all for now. The stock market will be closed on Monday in honor of Dr. Martin Luther King’s birthday. He would have been 95 years old. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want more info on our ETF, you can check out the ETF’s website.

Posted by Eddy Elfenbein on January 9th, 2024 at 8:07 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His