CWS Market Review – March 26, 2024

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

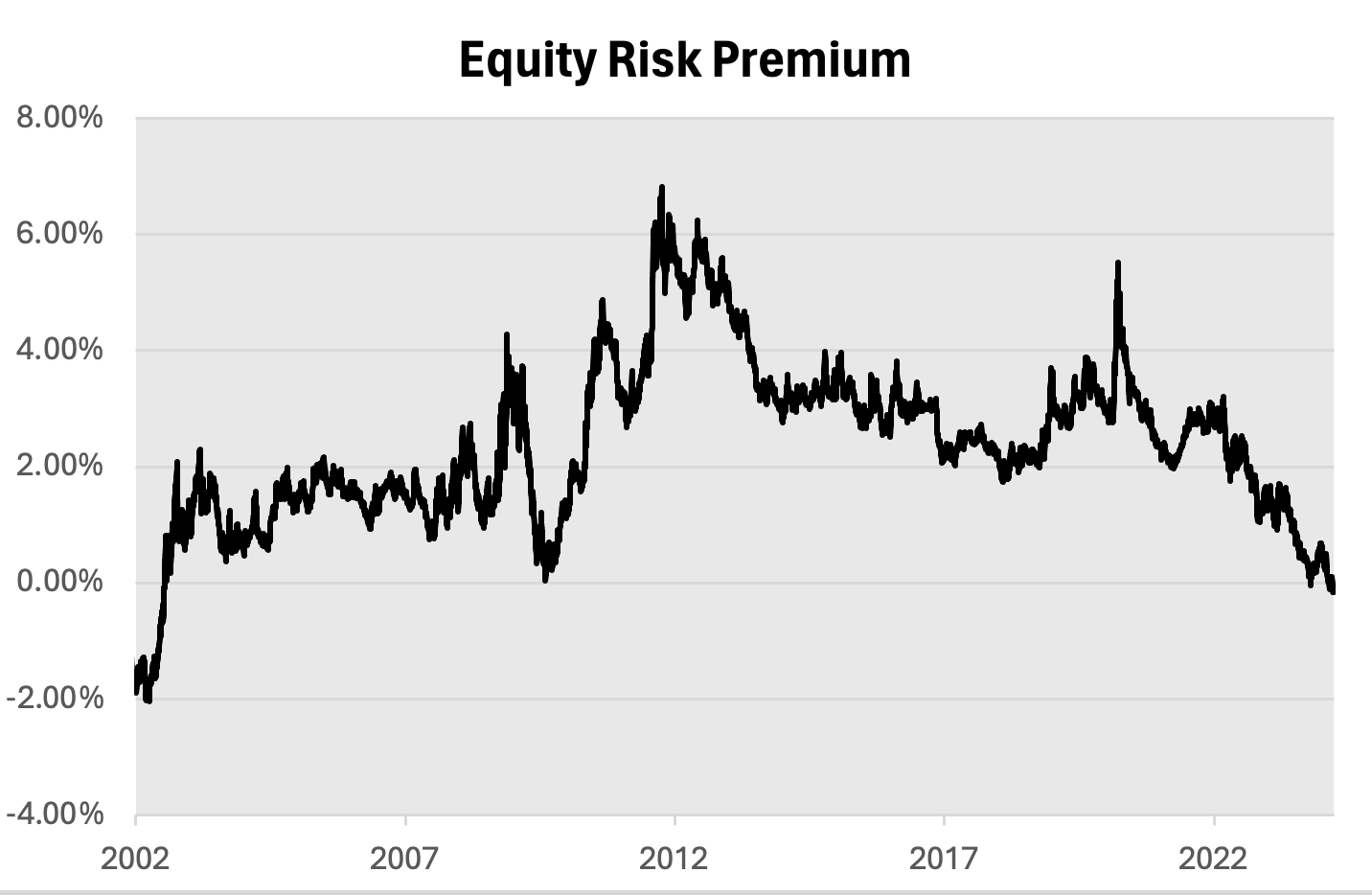

The Equity Risk Premium Goes to Zero

The stock market did something recently it hasn’t done in over 20 years. The yield on the 10-year Treasury exceeded the earnings yield for the S&P 500.

What am I talking about? Let’s dive in.

By earnings yield, I mean the S&P 500’s earnings divided by its price. That’s the inverse of the market’s price/earnings ratio.

To be more technical, the equity risk premium has gone to zero. Typically, one would expect a benefit from owning stocks. According to the theory, this is the reward shareholders get for shouldering more risk. Sometime the benefit is a lot, sometimes it’s a little. Right now, it doesn’t exist.

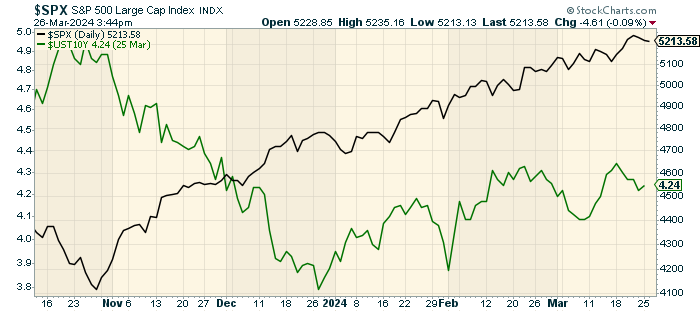

Here’s a look at the yield on the 10-year Treasury (in black) along with the S&P 500’s earnings yield (in purple).

Here’s how it works, or at least how it’s supposed to work (my apologies for getting mathy).

Take the 10-year Treasury yield. Right now, that’s around 4.25%. Add 2% to that for the risk premium (so 6.25%). Then take the inverse of that (1/0.0625 = 16) and that should roughly be the stock market’s price/earnings ratio. In this case, that’s 16.

Except, right now, it’s not even close. The stock market’s current price/earnings ratio is currently at 24. That’s roughly 50% higher than where the model thinks it should be.

As of Friday, the 10-year Treasury yield was 4.27% while the earnings yield of the S&P 500 was 4.10%. That means that investors are being punished by 17 basis points for owning stocks. This is also why we pay so much attention to what the Fed has to say about interest rates.

Let me add some very cautious words about this kind of analysis. I’m not a fan of trying to model the stock market. Many have tried but the market gods have left many a ruined spreadsheet in their wake. To quote Isaac Newton, “I can calculate the motion of heavenly bodies, but not the madness of people.”

The model isn’t saying that stocks are overpriced. Rather, it’s saying that stocks are richly valued relative to bonds compared with previous periods. That’s quite a different takeaway.

Here’s a look at the Equity Risk Premium which is how much stock investors are being paid to buy stocks instead of bonds.

Still, even bad models can make a point. This one is telling us a very basic fact that we can’t ignore. That is that stock prices have gone up a lot over the past five months. Meanwhile, bond prices have been creeping lower.

At some point, bonds are a better deal than stocks. I don’t know where that line is, but I do know two things: it’s out there somewhere, and we’re much closer to it than we’ve been in quite some time.

This isn’t to scare you. I have no plans to sell all my stocks, but it’s responsible to ensure that investors are aware of the current climate.

Interestingly, stocks reached their most recent low point in late October right as the 10-year Treasury peaked near 5%. (It came very close to breaking above 5% but couldn’t quite do it.)

Since then, stocks have rallied, and the 10-year Treasury yield fell, but that came to an end just before New Year’s. We went from Stocks-Up, Bonds-Up to Stocks-Up, Bonds-Down. The first one can last a long time, but the second one is a lot less stable. Last week, the 10-year yield got above 4.3%.

While I don’t plan on selling anything, I certainly can understand the mindset of some investors who look at the current prices and realize that they can sit out the volatility of the stock market and lock-in, say, a one-year Treasury for 5%. That’s the equivalent of 2,000 Dow points. For zero risk!

It’s not for me, but I get why some people are happy to take it. This shows us how distorting higher interest rates can be. This also tells me that sometime soon, the Fed will cut rates not because it wants to, but because it has too.

The odds of a rate cut in June are at 70%, and that rises to 84% for a cut by July. The odds for two cuts by July are low (now around 30%). It may soon be that we’ll get one cut, in June or July, but which month isn’t yet clear.

The Reddit Rally

Last week, I told you about the weakness in many defensive sectors. That’s exactly the outcome of diverging stock and bond markets. Last week, I mentioned how one of our favorite defensive stocks, Hershey (HSY), has been acting poorly of late. This is exactly the kind of stock that leads the market when the economy gets soft.

I mentioned that the chocolate giant has been squeezed by higher cocoa prices. Due to heavy rains in west Africa, there’s been a massive shortage of cocoa. That’s where 70% of the world’s cocoa comes from. So far, Hershey has been able to pass along some of these price increases.

Cocoa is outperforming Nvidia this year. Earlier today, BNP Paribas Exane downgraded Hershey from outperform to neutral.

The cocoa rally, however, has gone into overdrive, and Easter is one of the biggest times of the year for chocolate consumption. For the first time ever, cocoa is trading north of $10,000 per metric ton. Hershey says it predicts flat earnings this year. At some point soon, I expect cocoa prices to plunge back to earth.

But this is a different outcome from the same driver. Investors are ignoring risk. Cocoa isn’t the only place we’re seeing surging prices. Last week, Reddit (RDDT) went public, and the stock has performed very well.

I wanted to show you just how extreme some of the valuations are. Let’s take a closer look at Reddit’s business.

Last year, Reddit had revenue of $804 million and operating income of negative $140 million. In other words, the company is running at an operating loss. Add in $50 million in other income and Reddit lost about $90 million for the year. That works out to minus 57 cents per share.

Despite running a loss, shares of Reddit were priced at $34. Once trading started, the shares took off. Earlier today, the stock came close to $75 per share. That means the business is trading for more than 130 times its loss from the year.

I understand that one shouldn’t value nontraditional companies with traditional metrics. Still, at some point, one has to view this as extreme. This is exactly what happens when the equity risk premium goes to zero. When being risky pays off, the market will follow what’s working.

Reddit is worth $75 per share in the same way cocoa is worth $10,000 per metric ton, or the S&P 500 is worth 24 times earnings. “The voice of reason is small, but very persistent.” — Sigmund Freud.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want more info on our ETF, you can check out the ETF’s website.

Posted by Eddy Elfenbein on March 26th, 2024 at 6:34 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His